NCV - NCV: Troubled History But Novel Concept

2023-11-02 11:53:01 ET

Summary

- Virtus Convertible & Income Fund offers a high level of current income with a yield of 13.97%.

- The NCV closed-end fund heavily invests in convertible securities, providing income potential and upside potential of common equity.

- The fund has experienced disappointing performance, with a significant decline in share price and failure to cover distributions in recent years.

- The fund's leverage could be playing a role in its poor performance, as it amplified its losses in 2022.

- The fund is trading at a reasonable valuation right now.

The Virtus Convertible & Income Fund ( NCV ) is one of the more interesting closed-end funds, or CEFs, in the market for any investor who is seeking to earn a high level of current income. The fund’s current yield of 13.97% is certainly quite acceptable for anyone who wants to earn income from their assets, as it is competitive with some of the highest-yielding funds in the market. The fund’s uniqueness does not come from its yield, however, but from what it invests in. This fund is one of the few that heavily invests in convertible securities, which are a very nice vehicle for those investors who want both the income potential of bonds and preferred stocks but do not want to sacrifice the upside potential of common equity. These have generally been one of my favorite securities to invest in, but not all companies have them and they can be difficult to get a hold of. Fortunately, this fund provides easy access to a portfolio of them.

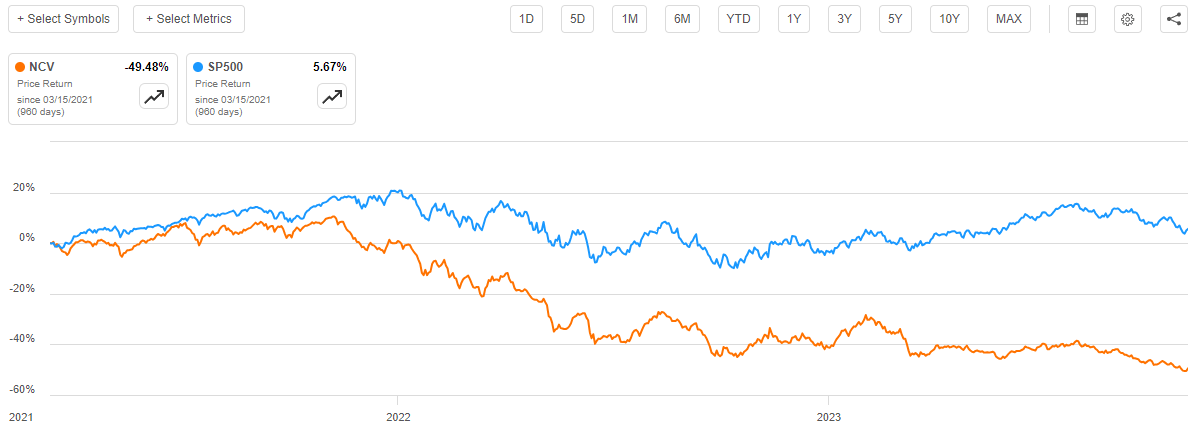

As long-time readers may recall, we last discussed this fund on March 15, 2021. It is hardly an understatement to say that the market is very different today than it was back then. Interest rates are substantially higher and for the most part stock returns are lower. That is especially true for non-dividend-paying stocks as high rates have made investors less patient with respect to the amount of time that they will wait to get their money back. As might be expected, the Virtus Convertible & Income Fund has delivered a very disappointing performance since that time. As we can see here, the fund’s share price is down a whopping 49.48% compared to a 5.67% gain in the S&P 500 Index ( SP500 ):

{kind=link}

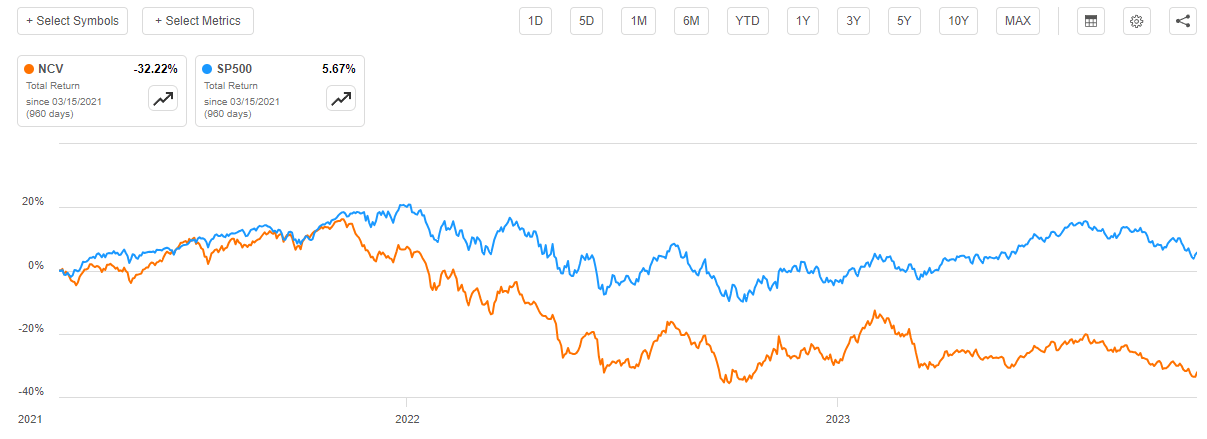

It is not surprising that the fund’s share price declined significantly, but admittedly that is quite a big decline. One obvious reason for this could be that convertible securities are frequently issued by start-ups and other non-profitable companies that delivered reasonable performance when money was freely available but generally fell flat as high interest rates have caused investors to actually begin demanding profitability. Another thing to consider is that closed-end funds like the Virtus Convertible & Income Fund typically pay out a substantial percentage of their investment returns to the shareholders. This is the cause of their high yields, but sometimes it can cause their share price to decline rapidly if something causes the value of their assets to decline. As such, we should generally evaluate the performance of closed-end funds with the distribution included since that tells us what an investor actually received. Unfortunately, in this case, the fund once again disappointed as investors who purchased a fund on the day that my previous article was published have lost 32.22% of their investment:

{kind=link}

This terrible performance will almost certainly cause some investors to wonder if it still makes sense to purchase shares of this fund. Let us investigate it further and attempt to answer that question.

About The Fund

According to the fund’s website , the Virtus Convertible & Income Fund has the primary objective of providing its investors with a very high level of total return. As is usually the case, the fund’s website includes a more in-depth description of its objectives and strategy:

The Fund seeks total return through a combination of capital appreciation and high current income.

Invests in a diversified portfolio of domestic convertible securities and high yield bonds rated below investment grade.

Under normal circumstances, the Fund will invest at least 80% of its total assets in a diversified portfolio of convertible securities and non-convertible income-producing securities and seeks to invest at least 50% of its total assets in convertible securities but determines its allocation based on changes in equity prices, changes in interest rates, and other economic and market factors. For the convertible portion, Voya Investment Management seeks to capture the upside potential of equities with potentially less volatility than a pure stock investment.

In searching for investment opportunities, the manager looks for issuers that will successfully adapt to change, exceed minimum credit statistics, and exhibit the most promising operating performance potential.

Thus, the Virtus Convertible & Income Fund can be best thought of as a hybrid bond fund that invests in both convertible securities and junk bonds. The fund’s description claims that it will generally favor convertible securities, however, as it promises to invest at least 50% of its assets in those securities whenever possible. This is the case right now. As we can see here, 78.64% of the fund’s assets are invested in convertible securities alongside a 67.39% allocation to high-yield bonds:

CEF Connect

It seems certain that the first thing that any reader will undoubtedly note is that the fund has a substantial negative cash position. This comes from the fact that this fund employs leverage as a method of boosting its overall portfolio yield. We will discuss the implications of this later in this article. For now, we can clearly see that the fund is favoring convertible securities over other asset classes, which is exactly what we want to see with this fund.

The fund’s own description provides the reason why income-focused investors may be attracted to convertible securities. After all, these securities frequently have comparable yields to bonds or preferred stock, but they also have the ability to be converted into shares of common stock of the issuing company. This is one of the reasons why start-up companies may use them, as they will attract investors who want some sort of an immediate return on investment but still want the potential reward that can accompany a successful start-up’s common stock following an initial public offering. Tesla, Inc. ( TSLA ), for example, used these securities as a way to obtain affordable debt financing back in its early days. It is unlikely to be a surprise to anyone reading this that investors in these bonds are much happier with the conversion feature than they would have been with a fixed-rate bond that had a slightly higher coupon.

This brings us to the biggest downside of convertible securities. Their yield tends to be a bit lower than that of ordinary bonds. This is because investors agree to give up a bit of yield in exchange for the potential for much bigger rewards that the conversion feature provides. We can see this reflected by looking at the yield of the Bloomberg U.S. Convertible Cash Pay Bond > $250 Million Index ( ICVT ) against some of the other American bond indices:

| Index |

| Current Yield |

| Bloomberg U.S. Convertible Cash Pay Bond > $250 Million Index |

| 4.66% |

| Bloomberg U.S. Aggregate Bond Index ( AGG ) |

| 4.85% |

| Markit iBoxx USD Liquid Investment Grade Index ( LQD ) |

| 6.24% |

| Markit iBoxx USD Liquid High Yield Index ( HYG ) |

| 8.92% |

Thus, we can clearly see that convertible bonds will generally provide a bit lower income than comparable non-convertible bonds. However, if the company that issued the bond sees a successful performance in the common stock market, then the holder of one of these bonds will be far better off. As a result of this fact, convertible securities deliver a performance that is a bit different than that of ordinary bonds. In particular, they can appreciate in value if the common stock of the issuing company does, regardless of interest rates. Of course, since both common stock and bonds tend to move inversely to interest rates nowadays, this is not as big of an advantage as it was twenty years ago.

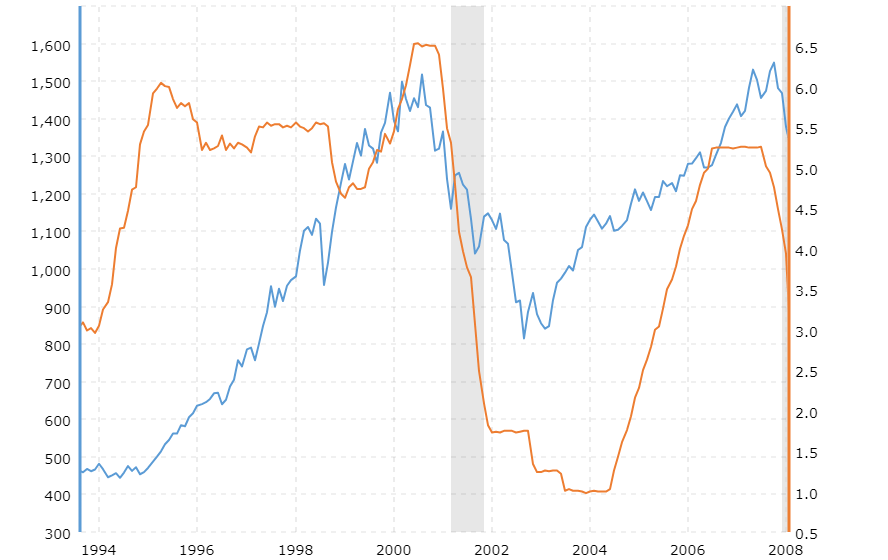

The above paragraph may immediately be confusing to some readers. After all, for a while now, we have been hearing that high interest rates are pressuring the stock market downward. That is certainly true right now because the economy has become addicted to easy money from the Federal Reserve. However, prior to the 2009 recession, the connection between stock prices and interest rates was very different. This chart shows the federal funds rate graphed against the S&P 500 Index from 1993 to 2008:

{kind=link}

As we can clearly see, the S&P 500 Index generally went up when interest rates went up and fell when interest rates declined. This is because high interest rates were a sign of a strong economy. The Federal Reserve cuts rates during a weak economy in order to stimulate it, and stocks tend to perform badly in a weak economy. At least, that was the case prior to the 2009 recession. As such, it is possible for the convertible bonds held by this fund to go up despite rising interest rates if the stock market is strong enough. This is something that could add a bit of diversity to a portfolio that is otherwise very bond-heavy, which some income-focused investors might have right now.

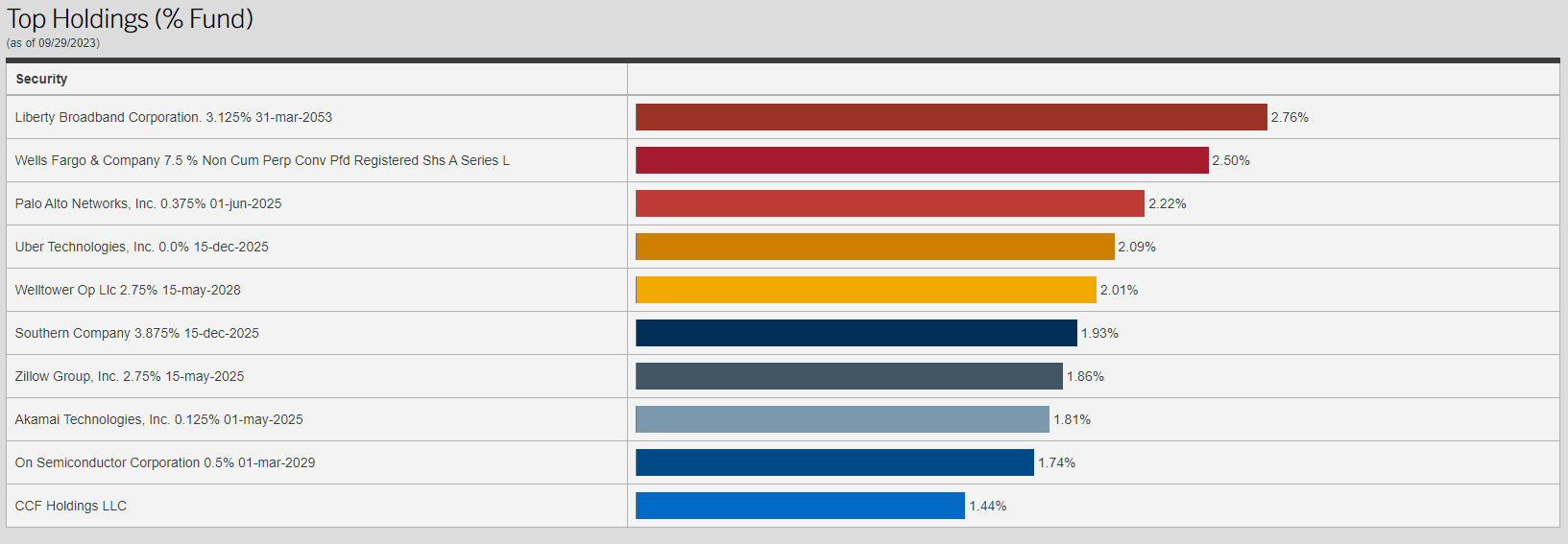

As already mentioned, it is fairly common for profitless start-ups or troubled companies to issue convertible debt. This is because the convertible feature is one of the few ways that these companies can actually obtain financing at a reasonable price. This is certainly what we see when we look at the largest positions in this fund. Here they are:

{kind=link}

Many of the companies on this list are quite young firms that only started operations within the last fifteen or twenty years. One exception to this is Wells Fargo ( WFC ), which has a convertible preferred stock offering on the list. The Wells Fargo Series L Preferreds (WFC.PR.L) were issued during the height of the subprime mortgage crisis, so it makes sense that investors in these securities would want some extra compensation for taking on the risk of investing in a bank around that time.

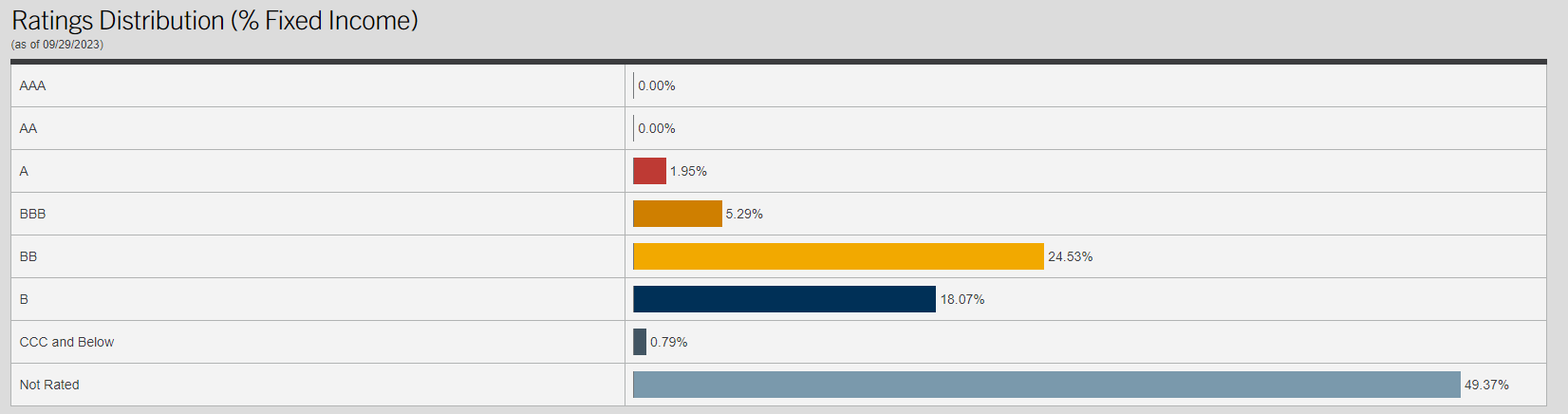

Earlier in this article, it was mentioned that the Virtus Convertible & Income Fund invests in a combination of convertible securities and junk bonds, although it tries to be more heavily weighted in convertible securities. However, convertible securities are typically issued by unprofitable start-ups or financially stressed firms. Thus, we can assume that most of this fund’s portfolio is invested in securities that have a below-investment-grade credit rating. That is indeed the case, as we can see here:

{kind=link}

An investment-grade credit rating is BBB or higher. As we can see, that only describes 7.24% of the fund’s portfolio. The remainder of the portfolio is invested in below-investment-grade or unrated securities. We can see though that just under half, or 49.37%, of the fund’s assets are invested in unrated securities. This adds an interesting twist as we are uncertain exactly what the credit ratings of these securities would be if they had one. In previous articles, I have speculated that unrated securities probably are the equivalent of junk bonds in quality. This is because most companies that have the financial strength to obtain an investment-grade credit rating will almost certainly pay to have their securities rated in order to save on interest costs. It is uncertain whether or not that is the case here, as the conversion feature alone may allow the issuing company to keep its interest expenses at an acceptable level. However, it is a fair assumption that most of the companies in the fund are more likely to default than a typical investment-grade company.

Fortunately, as we have already seen, the fund’s largest position only accounts for 2.76% of the fund’s total assets. In addition, the fund has 225 issuers represented in the portfolio right now. Thus, any individual default should have a negligible impact on the portfolio as a whole.

Leverage

As mentioned in the introduction, the Virtus Convertible & Income Fund employs leverage as a means of boosting its effective yield beyond that of any of the assets in the portfolio. I explained how this works in various previous articles on other closed-end funds. To paraphrase myself:

Basically, the fund borrows money and then uses that borrowed money to purchase convertible securities, junk bonds, or other assets. As long as the purchased assets provide a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably higher than retail rates. As such, this will usually be the case.

It is important to note though that this strategy is not as effective today with rates at 6% as it was two years ago when rates were essentially 0%. This is because the difference between the rate at which the fund can borrow and the yield that it gets from the purchased securities is much narrower than it once was.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt since that would expose us to an excessive amount of risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for this reason.

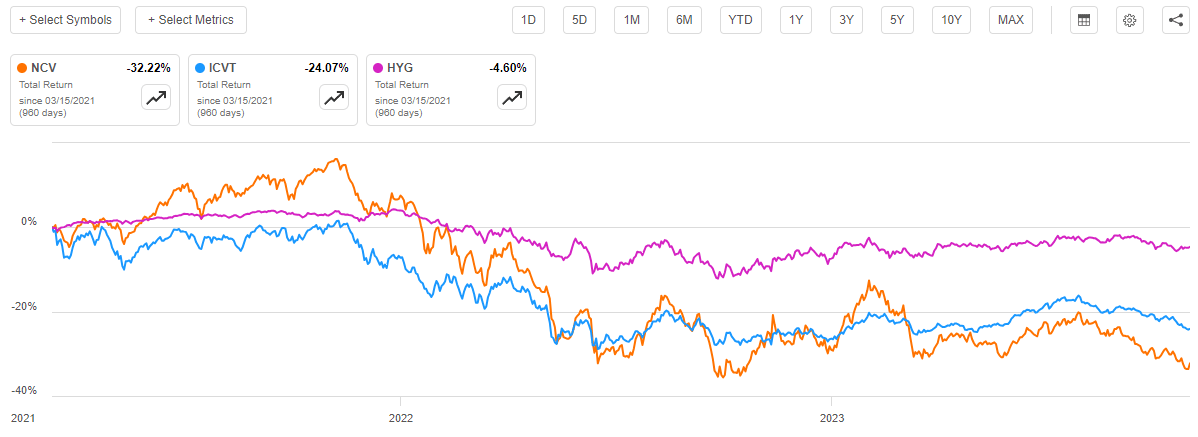

As of the time of writing, the Virtus Convertible & Income Fund has levered assets comprising 39.41% of its portfolio. This is quite a bit above the one-third level that we really like to see. As such, we can expect that this fund will be somewhat more volatile than the assets in the portfolio. In fact, we do see that by looking at the fund’s performance. The convertible bond index has delivered a negative 24.07% total return since the date that my previous article on this fund was published. However, this fund delivered a negative 32.22% over the same period:

{kind=link}

A simple look at this chart shows that the Virtus Convertible & Income Fund tends to move in the same direction as the index, but its moves are much more pronounced. That is almost certainly due to the compounding effects of the fund’s leverage over the period. This is the big risk involved with investing in this fund. It will provide a much higher yield than a comparable index fund, but movements in both a positive and negative direction will have a greater effect.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Virtus Convertible & Income Fund is to provide its investors with a very high level of total return. In order to achieve that objective, it invests in a portfolio that consists of convertible securities and junk bonds. Both of these asset classes deliver their returns in the form of direct payments to the shareholders, although convertible securities also have the potential to provide significant capital appreciation if the linked equity appreciates. The fund collects all of the payments that it receives from these securities as well as any capital gains that materialize following a conversion event. The fund applies a layer of leverage to boost these sources of income beyond what the securities actually provide. The fund then pays out all of this money to its shareholders, net of its own expenses. As such, we can probably assume that it would have a very high yield.

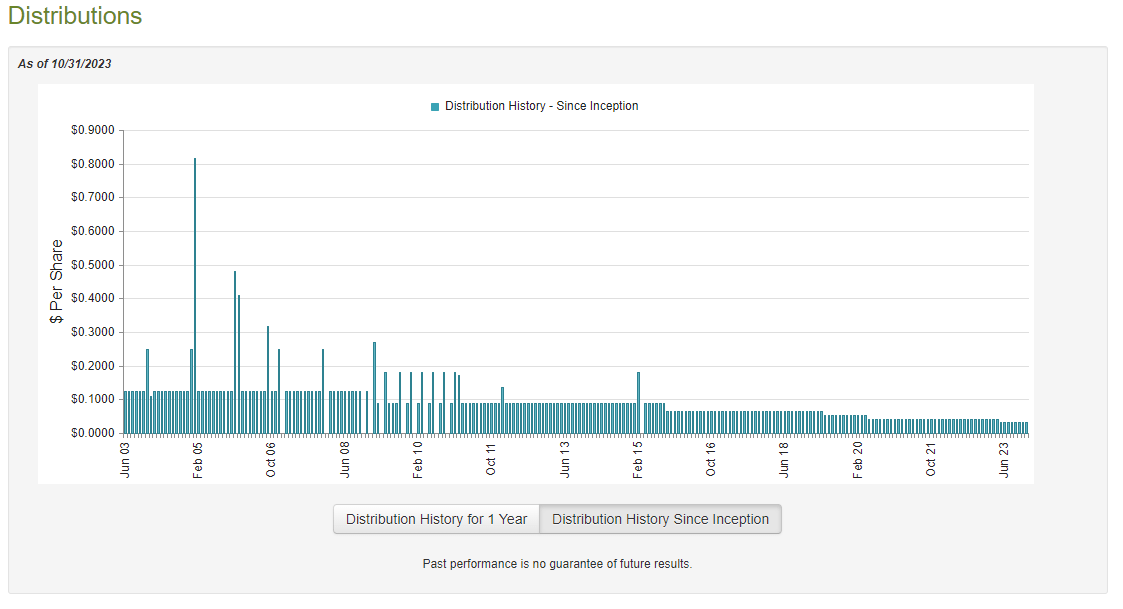

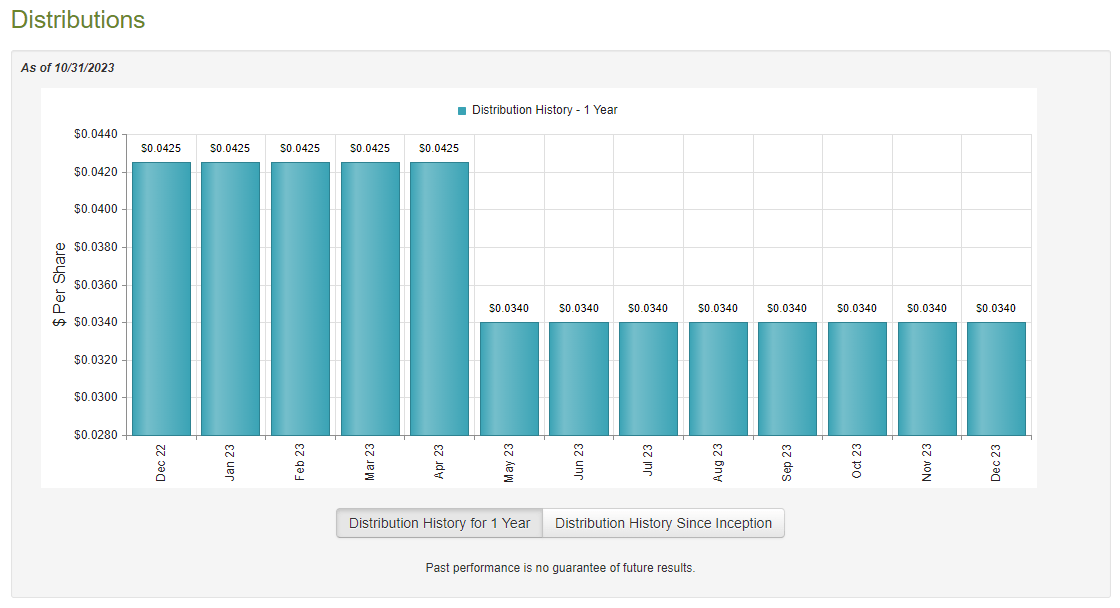

This is certainly the case as the Virtus Convertible & Income Fund currently pays a monthly distribution of $0.0340 per share ($0.408 per share annually), which gives the fund a 13.97% yield at the current price. That is certainly a very attractive yield for any income investor, but unfortunately, the fund has not been especially consistent with respect to its distribution over the years. In fact, as we can see here, the distribution has steadily declined since the fund’s inception:

{kind=link}

That is undoubtedly going to reduce the fund’s appeal in the eyes of any investor who is seeking to earn a safe and secure income from the assets in their portfolio. The fact that the fund cut its distribution earlier this year will intensify that reduction:

{kind=link}

With that said though, the fund’s past is not necessarily the most important thing. This is because anyone purchasing the fund today will receive the current distribution at the current yield. Any new investor will not be impacted by actions that the fund has taken in the past. As such, we should investigate its ability to sustain the current distribution at the current level.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on July 31, 2023. This is a pretty good period for us to analyze because the entire period was characterized by a great deal of strength in the stock market. Investors widely assumed that the Federal Reserve would quickly cut interest rates and so they bid up the price of various assets. In particular, a bubble formed in artificial intelligence and related technology stocks that could have allowed the fund to earn some capital gains. This report should give us a good idea of how well it managed to accomplish that task.

During the six-month period, the Virtus Convertible & Income Fund received $10.837 million in interest along with $1.460 million in dividends from the assets in its portfolio. This gives the fund a total investment income of $12.297 million during the period. It paid its expenses out of this amount, which left it with $5.917 million available for shareholders. That was, unfortunately, nowhere close to enough to cover the $19.973 million that the fund paid out in distributions during the period. At first glance, this is likely to be concerning as the fund obviously did not have sufficient net investment income to cover the distribution that it paid out.

However, there are other means through which this fund can obtain the money that it needs to cover its distribution. Capital gains is the most obvious one, since the market was reasonably strong, and the fund does have some significant exposure to technology companies. Unfortunately, it had mixed results here. The fund reported net realized losses of $25.655 million, which were offset by $32.308 million in net unrealized gains. This alone was not sufficient to fully cover the distribution, even when combined with net investment income. Overall, the fund’s net assets went down by $10.212 million after accounting for all inflows and outflows. This comes on top of a $132.841 million decline in net assets during the full-year period that ended on January 31, 2023.

Thus, the fund failed to cover its distribution over the entire trailing eighteen-month period. That is certainly concerning, and it explains why the fund saw fit to cut its distribution earlier this year. It is uncertain whether the distribution will prove sustainable at its new level or not. It may be prudent to be cautious, especially if rising rates continue to apply pressure to long-duration growth stocks.

Valuation

As of October 31, 2023 (the most recent date for which data is currently available), the Virtus Convertible & Income Fund has a net asset value of $3.39 per share but the shares currently trade for $2.97 each. This gives the shares a 12.39% discount on net asset value at the current price. That is a fairly large discount, although it is nowhere near as large as the 13.61% discount that the shares have had on average over the past month. Thus, it may be possible to get a better price by waiting a bit, but a double-digit discount is generally a reasonable entry point for any fund.

Conclusion

In conclusion, the Virtus Convertible & Income Fund is a high-yielding closed-end fund with a fairly novel strategy. The fund is one of the few ways to get access to a diversified portfolio of convertible securities, which do have a lot to offer investors. Unfortunately, this fund’s past performance leaves a lot to be desired. It took pretty heavy losses over the past two years, which were amplified by its leverage. It also failed to generate sufficient investment returns to cover its distributions since at least the start of 2022. Thus, the fund’s distributions themselves have been destructive to its net asset value. It should have cut the distribution sooner than it did. With that said, the current price is definitely a reasonable entry point if you want this fund in your portfolio.

For further details see:

NCV: Troubled History But Novel Concept