NDMO - NDMO: 7.5% Yield And Tax Free To Boot

2023-11-09 16:42:27 ET

Summary

- Municipal bonds provide tax advantages for investors, and the Nuveen Dynamic Municipal Opportunities Fund offers a huge yield.

- The fund has struggled to generate returns, primarily as it was launched at the tail end of the ZIRP bubble.

- We examine the fund's distribution-paying abilities and give you our verdict.

Issued by the state or local governments, municipal bonds provide a tax advantage to its investors, as the interest earned from these is exempt from federal taxes. It could also be exempt from state taxes, if the bond holder resides in the state of issuance. This beneficial treatment applies to only interest income, and not any capital gains. The tax advantage is more pronounced for investors that fall in the upper echelons of the one percenters.

{kind=link}

Schwab

We have written about a few funds that cater to the municipal bond audience on this platform. BNY Mellon Municipal Bond Infrastructure Fund (NYSE: DMB ) being the most recent. We believe fixed income will trounce equities over the next several years, but we still decided to stay out of DMB.

The overwhelming leverage will continue to harass its bottom line, and we anticipate another distribution cut within a year. That said, we think this is a slightly better entry point as the combination of the bond price drop and wider discount improve prospects for the next 5-year returns to be better than the last 5.

Source: DMB: 3% Total Return Over 5 Years, But Prospects Improve From Here

Today, we will talk about another fund that is monogamous with municipal securities, and it goes by the name of Nuveen Dynamic Municipal Opportunities Fund ( NDMO ). The fund began operations in August 2020, and mandate allows for securities of any maturity. As of September 30, most of the portfolio was concentrated in longer dated holdings.

{kind=link}

NDMO

With around 17% of the portfolio having a possibility of being called within the next year.

{kind=link}

NDMO

NDMO also has carte blanche in choosing securities, credit quality notwithstanding. One stop gap in place is that a maximum of 10% of the total assets can be in "defaulted securities or securities of issuers in bankruptcy or insolvency proceedings at the time of investment". We can see below that as at September 30, the fund had exercised a modicum of restraint, with close to 50% in investment grade securities.

{kind=link}

NDMO

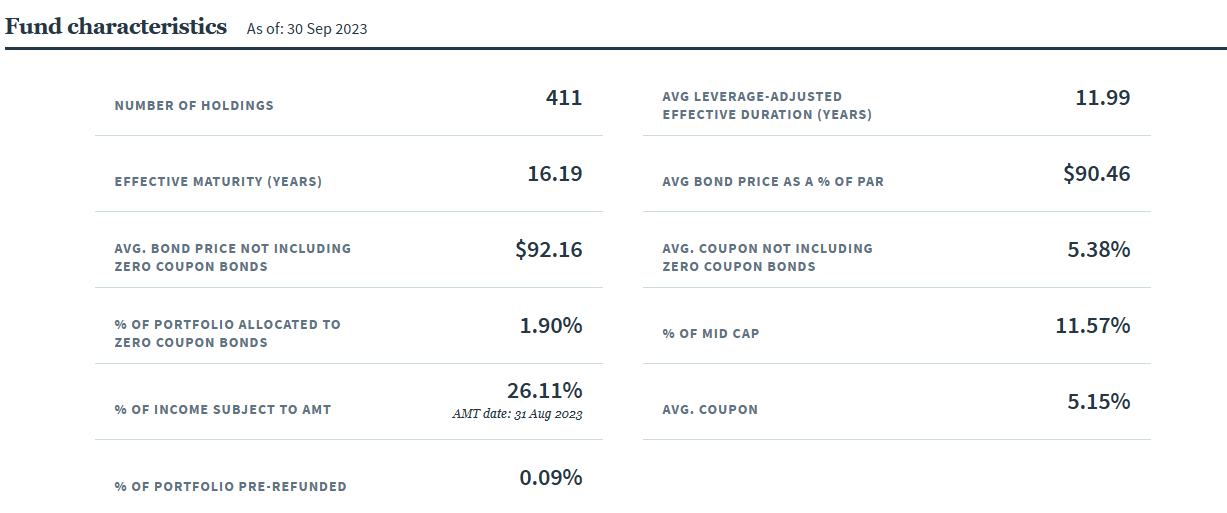

The balance half tied up in junk and unrated securities is on the higher side, compared to the other similar funds that we covered. DMB, for instance, had around one fourth of its assets in junk and unrated securities as of the same date. With 411 holdings, NDMO is well diversified, with the collective maturity of the portfolio coming in at a little over 16 years.

{kind=link}

NDMO

The duration is lower at around 12 years, giving a general idea on the extent to which the portfolio value will fluctuate with a 100 basis points increase in interest rates (inverse relationship). Using the average coupon (5.38%), the average price ($90.46) and the effective maturity (16.19 years), we can deduce that the portfolio had an approximate yield to maturity or YTM of 6.33%. This fund currently distributes 6.2 cents on a monthly basis, which comes to an annual yield of 7.56%.

NDMO decreased its distribution from 7.65 cents to the current amount back in April of this year and looks like there will be more of that in the next few months.

{kind=link}

NDMO

This is simple to figure out if we run the numbers. The portfolio earnings or yield are first used to pay the expenses of the fund, and the balance is what remains for its unitholders. So the fund is in a bigger deficit than just the difference between the distributions and the YTM. Around 28% of NDMO's portfolio is purchased with borrowed funds.

{kind=link}

CEF Connect

At 28%, it is hardly the worst offender in the land of closed end funds, but even that leverage has a cost.

{kind=link}

CEF Connect

The last published data shows the leverage costing this fund and its unitholders 1.52% annually.

{kind=link}

CEF Connect

If we consider YTM minus 2.75% in annual expenses, we can work out the approximate distributions it can generate from underlying bonds. The YTM is 6.33% but that is amplified by the leverage. The fund could generate about $53 million in "yield" every year. This yield is really the interest income and the capital appreciation towards par. If we subtract out the expenses we get to about $36 million in net returns which works out to about 6.00%. NDMO is distributing far more than that on NAV. How does it manage to keep its income investors happy? By returning their capital to them as a portion of their monthly distribution. This portion has been rising over the last two years.

{kind=link}

April 30, 2023 Semi Annual Report

Do note that our calculations are massively overstating the fund's ability to pay distributions as the interest expense ratios are a trailing measure. Realistically the fund probably can do 5% on NAV, so a big cut is inevitable.

Performance

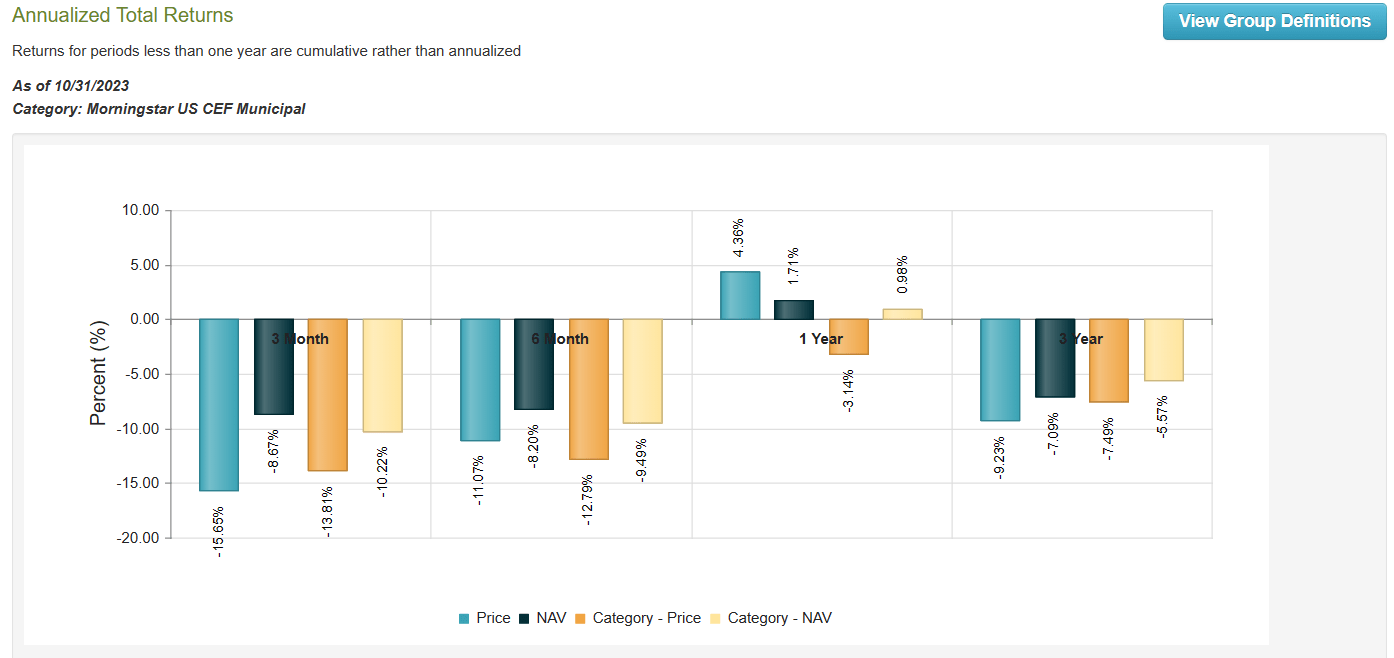

NDMO's NAV has held up well relative to its category in its brief history, positive returns have still been rare for both since 2020.

{kind=link}

CEF Connect

We compared it to a few of its brethren and that it has not done the worst, is the only silver lining.

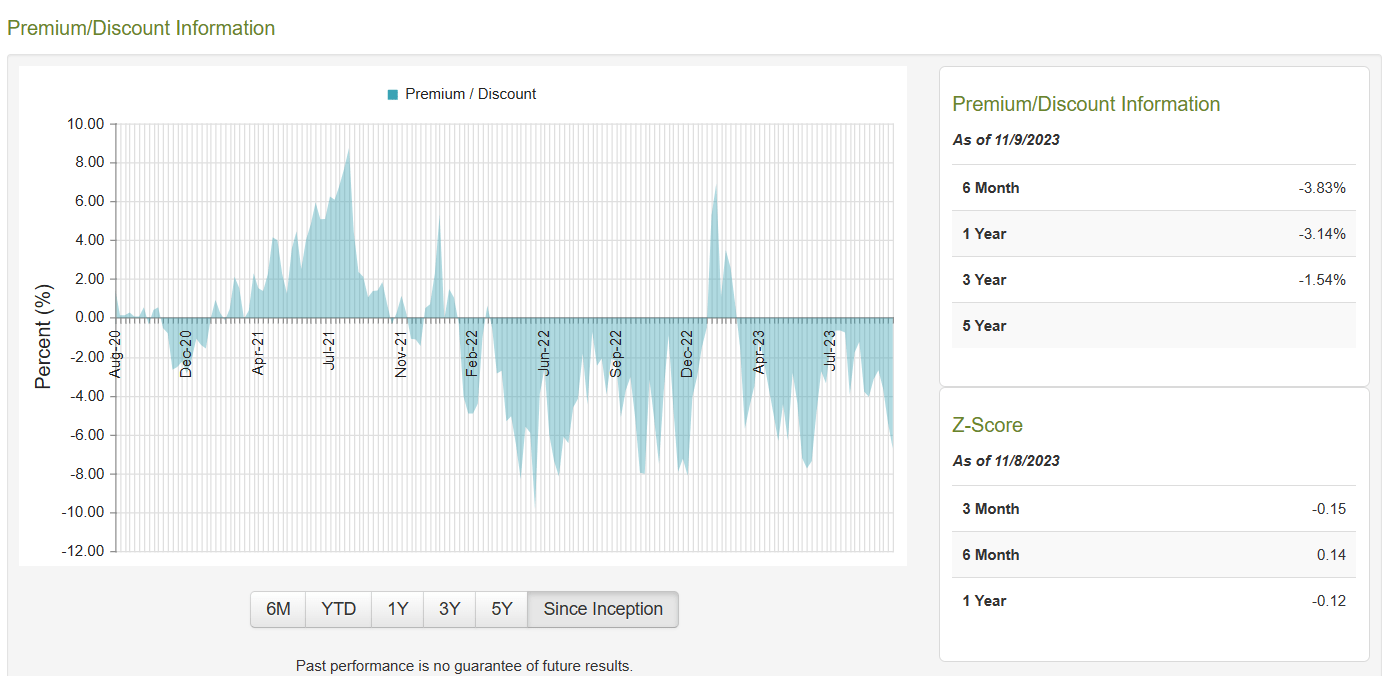

While NDMO spent most of 2021 commanding a premium, it has done the opposite since then.

{kind=link}

CEF Connect

With a Z-score of -0.15, investors should not expect any price fireworks to the upside for this closed end fund.

Verdict

We have generally not had a bullish outlook on Munis. The rationale was that investors had bid them up crazily during the ZIRP era and they were setup for extremely poor returns. They were setup for even worse returns than regular corporate bonds because of their tax status. As investors always bid up the price of these, way above corporate bond prices, the yields became extremely low in 2021. Bond investors know that the move from a 2% yield to 3% yield, hurts far more than a move from 4% yield to a 5% yield. Munis had no chance of making any positive returns (at least by our total return standard) and hence they were pure garbage in our eyes. Case in point, was the reversal of fortunes for PIMCO Municipal Income Fund ( PMF ), which has been dragged over the coals since 2022.

With its dissipating double digit discount causing pain to investors that paid the high price.

The distribution cut that came during this time just added salt to the wounds. Coming back to NDMO, with another distribution cut looking likely and expectations that the next set of financial statements will reveal an even higher leverage expense, we need a deeper discount on NAV to even consider this fund. The added stress of holding a lot of junk bonds into a recession is not something we are comfortable with either. We are staying far away for now.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

NDMO: 7.5% Yield And Tax Free To Boot