NDMO - NDMO: Few Reasons I'm Upgrading Outlook For This High Yield Muni Fund

2024-01-02 01:39:22 ET

Summary

- I evaluate the Nuveen Dynamic Municipal Opportunities Fund as an investment option.

- Income metrics are concerning, but the yield is high enough to be attractive even with a cut.

- The fund's valuation has improved, with the discount widening significantly to a double-digit discount.

- The fund's diversity in terms of credit quality and state exposure is something I view positively.

Main Thesis & Background

The purpose of this article is to evaluate the Nuveen Dynamic Municipal Opportunities Fund ( NDMO ) as an investment option. This is a diversified municipal bond fund with a variety of sector allocations and credit ratings. Its primary objective "seeks total return through income exempt from regular federal income taxes and capital appreciation".

I covered NDMO at the mid-year point and at that time I wasn't very bullish. I saw leverage continuing to be a headwind and not a positive attribute. Further, the fund's valuation and broader outlook for bonds kept a lid on my optimism. In hindsight, my outlook was vindicated:

Fund Performance (Seeking Alpha)

As we enter 2024, I took another look at NDMO and have decided that now is actually a reasonable time for an upgrade. Some of the headwinds from mid-2023 have diminished a bit and I think the backdrop for munis as a whole is more favorable starting this new year than last. As a result, I am placing a "buy" rating on this CEF, and I will explain why in more detail below.

Valuation Story Has Improved

A quick attribute that I view favorable for NDMO is the fund's valuation. This will come as no surprise to my followers because they know I enjoy purchasing CEFs at discounted prices. In the case of NDMO, it has had a discount for a while, but the point to emphasize here is this discount has widened significantly.

To illustrate, back in May (when I wrote my last article on NDMO) the fund had a discount under 5%. At time of writing, despite the fund registered a slight positive return in the interim, this discount has widened to over 10%:

{kind=link}

While discounts (or premiums) never completely predict where a fund is going to trade, a double-digit discount is hard for me to ignore. Further, despite NDMO not climbing much on the open market, this metric has expanded by more than 5%. That means the fund's underlying assets have been appreciating, and the market price has not kept up. That is precisely the type of environment I like buying into, and helps to support my upgrade for NDMO as January kicks-off a new year.

Bonds As A Whole Have Momentum

I will now take a more macro-view of the bond sector - which is inclusive of munis. For anyone following the market, they know that the end of 2023 saw a renewed surge in bond buying across the board. This came about as inflation metrics started to indicate "peak" levels and the Fed paused its rate-hiking cycle. While the Fed may not be completely done, the market sure thinks it is. In fact, investors are anticipating cuts from the Fed in 2024, as opposed to 2023 when the new year began with investor eyeing further hikes:

Future Outlook (Federal Reserve)

{kind=link}

What this means is that bonds have a nice tailwind going into 2024. While I personally think investors are over-estimating how far the Fed will cut in 2024, there is plenty of time for me to be proven wrong and/or for the market to price-in a better-than-actual scenario. What I mean is, bonds can still run for a while before the Fed disappoints and we see a reversal. That leaves plenty of upside left in the short-term for fixed-income, extending to NDMO as well.

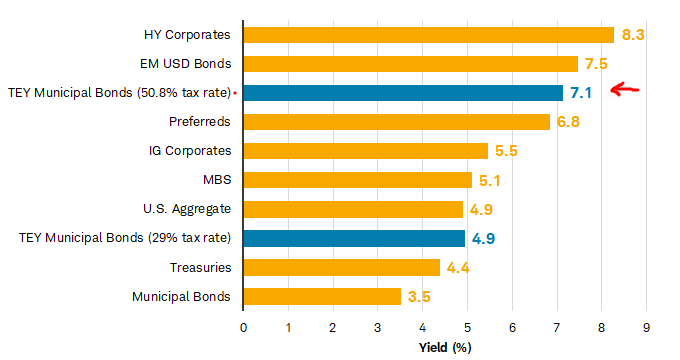

Corporate Credit Has Tight Spreads

Another macro-factor that can support muni bonds going forward is that alternative assets aren't quite as attractive. This is especially true for investors in higher tax brackets. Take corporate bonds as an example. In isolation, spreads are quite tight relative to history because investors rushed in to the sector en masse in Q4:

{kind=link}

What this suggests to me is that corporate bonds are getting a bit over-extended. As investors realize this and look for alternatives, munis could very possibly fill the void.

As I noted, the potential is definitely there for high-tax bracket investors. The narrowing of income opportunities in corporate bonds will shift their focus to munis if they are interested in after-tax yields. At present, munis offer some of the most competitive income streams on a tax-adjusted basis:

Current Yields (December '23) (Charles Schwab)

{kind=link}

My takeaway from this is that tax-exempt munis remain a viable alternative for many investors - especially high income investors - as we start a fresh year. That bodes well for the sector and especially for funds like NDMO that trade at healthy discounts to NAV.

NDMO Has Diverse Holdings

Another positive attribute for this particular fund is the make-up in credit quality. Of note, NDMO is not exclusively IG-rated debt. This is an important consideration that risk-averse investors need to weigh carefully. NDMO holds a significant portion of debt that is either not rated or below IG quality. That enhances the risk profile. But the good news is the fund is not exclusively junk or non-rated, as shown below:

NDMO's Credit Make-Up (Nuveen)

I personally think this is a good balance. While I am someone who prefers IG-rated debt generally, having exposure to a CEF that offers both IG-rated and non IG-rated debt allows one to amplify their yield without taking on excessive amounts of risk. Beyond that, "not rated" muni debt can often be of IG-rated quality, but the issuers simply choose to not have the bonds rating either due to expense and/or time constraints.

To be clear, I am not suggesting NDMO is not a more risk-on option for those in the muni space. With below IG-rated debt and not rated securities, along with leverage, this is a fund for those who can withstand above-average volatility and potential losses. But for those looking to amplify their income stream without going full-on into the junk debt category, NDMO could have a place.

The Income Headwind Persists

The challenge for those considering NDMO has got to be the income stream. This is something I have touched on before - when I correctly predicted an income cut would be coming in 2023 during my January review . Income cuts often hurt - and this can partially explain why NDMO's discount has widened and persisted. Investors who hold funds that cut their distribution can be shell-shocked and reluctant to either add to their position or get back in if they sold on the news.

I bring this up for two reasons. One, this headwind is not going to just disappear overnight. If those holding NDMO through the cut are waiting for more clarity on the protection of the current stream, they are probably going to wait a little longer. We don't just decide overnight that a risk is gone, so it could take some time for buyers to warm back up to this particular fund. Two, there are some signals that the pain is not officially "over". While the cut helped to even out NDMO's income production with what it pays in a distribution, it hasn't entirely corrected the problem. The most recent Section 19a notice from Nuveen still shows a high level of ROC from this fund - with roughly half of the distribution coming from this source. That is not a sustainable path and suggests that further corrections to the payout could be in the future.

The good news is that NDMO's distribution is quite large at the moment. This means it can withstand a cut and still offer investors a very attractive yield - especially on an after-tax basis:

Current Yield (Seeking Alpha)

The conclusion I draw here is that NDMO can survive a cut so that really doesn't need to be a massive sell signal at these levels. It seems to me that the market is already pricing it in - the fund trades at a 10% discount and has a yield above 7%. That shows a lot of bad news is baked in to the price. So while an income cut is never "good", it appears a likely scenario that the market knows is coming. That is why this isn't a major headwind for me as I see NDMO holding up reasonably well regardless, similar to how it performed in the second half of 2023 post-cut already.

New York An Opportunity?

The last topic to touch on here is how NDMO has seen a bump in its New York holdings. Going into 2024, the fund has about 14% exposure to this one state in isolation. This makes the happenings in NY's muni bond sector of definite interest to anyone who owns (or wants to own) this CEF:

NDMO's Top State Exposure (Nuveen)

This is a double-edge sword to be sure. On the one hand, having bonds from a high-tax state ensures some level of demand in most scenarios. Investors there - especially those who make a lot of money - will continue to be drawn to strategies that limit their tax bills. As we know, NY has some of the highest tax obligations in the country for wealthy residents. So anticipate muni demand remaining strong among that cohort.

But the flip side is this state constantly has budget "challenges". Deficits are not uncommon and negative headlines often persist among many media sources. But the truth is that NY has a history of making good on its obligations. And, despite spending a lot, it taxes its residents and visitors heavily to account for that spending. Further, NY made a point of pumping up its rainy day fund on the backdrop of federal stimulus/support:

{kind=link}

This shows me that fears over defaults among GO bonds from NY are a bit overblown. The state has the money it needs to make good on its current obligations. Can that change in the future? Absolutely - and I hope that NY takes a more prudent spending approach going forward. If we don't see improvement on that front, my opinion of these bonds may change. But in the short-term I think they will do just fine, and that supports a bullish rating on NDMO which owns a lot of these securities.

Bottom-line

NDMO has seen a modest gain since my last review but I believe better days are ahead. While risks associated with leverage, as well as a potential distribution cut, remain top of mind, I see enough positives to outweigh these risks. The fund sports a double-digit discount to NAV, has a high enough yield that it can remain attractive even with a cut, and it has a diversified balance sheet with NY bonds that are well supported. As a result, I am upgrading my rating to "buy" and recommend my readers give this idea some thought going forward to 2024.

For further details see:

NDMO: Few Reasons I'm Upgrading Outlook For This High Yield Muni Fund