NDMO - NDMO: Remain Disciplined In Early 2023

Summary

- NDMO looks like a true bargain play here. The discount to NAV is quite wide and the yield is very high.

- Despite these positives, there are reasons for caution. I expect a dividend cut to be forthcoming which could be a short-term headwind for the share price.

- Non-rated munis can often be of non-investment grade quality. These are the types of bonds most at-risk of a sharp recession. Therefore, investors should approach these investments selectively.

Main Thesis & Background

The purpose of this article is to evaluate the Nuveen Dynamic Municipal Opportunities Fund ( NDMO ) as an investment option. This is a diversified municipal bond fund with a variety of sector allocations and credit ratings. Its primary objective "seeks total return through income exempt from regular federal income taxes and capital appreciation".

I have covered NDMO multiple times in the past, including one-year ago when 2022 got underway. At that time, I was cautious on munis as a whole but especially NDMO. Looking back over the past year, my cautious outlook was dedicated to a degree, but, in reality, I should have been more bearish. Highly leveraged, non-IG quality funds took a real beating as a rule. NDMO was not immune to these macro-forces and suffered quite plainly:

Fund Performance (Seeking Alpha)

As I look at the year ahead, I would not expect such poor performance to continue. A drop near 30% for any muni fund in a year is unusual - even for leveraged options. As a betting man that is not just something I would expect. However, that doesn't mean the opportunity here is without risk. NDMO remains exposed to rising interest rates and a worsening credit environment. Further, I see a very real risk of a distribution cut in the short term. This balances out the view that the 8% discount to NAV offers buying a compelling buying opportunity. In short, I believe a "hold" rating continues to make sense.

The Value Looks Enticing

To start, let's look at some of the positives. Top of mind is the fund's valuation. Back in January '22, NDMO was sitting with a premium to NAV around 1%. I didn't find this valuation overly worrying, but it wasn't exactly "value" territory either. Today, that story is quite different, as NDMO sits with a discount to NAV above 8%. This is generally a buy signal for me personally:

{kind=link}

As the share price has declined, so too has the fund's current yield. The distribution rate has remained steady and the sharp decline in market price has left the fund offering investors a 9% yield on new positions:

| Current Distribution |

| Current Share Price (as of 1/3/23) |

| Current yield |

| $.0765/share |

| $10.21/share |

| 8.99% |

Source: Seeking Alpha

From a high-level standpoint, NDMO may seem too good to be true. A tax-advantaged yield of 9% with a buy-in point at a wide discount to NAV is indeed some characteristics I would normally view very favorably. In fairness, these are key points to why I am not bearish on this fund. Even with some risks present (which I will get to below), this will surely limit the downside if one buys now.

Top Concern For Me Is Distribution Cut

Getting to some of the headwinds, top of mind for me is the potential for an income cut. The good news here is that I believe NDMO will hold up reasonably well if the cut is modest. The discount to NAV and the reality that a drop in a 9% yield will still leave investors with a very enticing income stream. If we factor in tax savings, this fund could easily cut the distribution and still offer investors a real yield higher than what most fixed-income sectors could deliver.

Nevertheless, a cut to a distribution for any CEF usually results in a share price drop. This is fundamental to my "hold" thesis. I see an income cut coming and therefore, the strong potential for more attractive buy-in points ahead.

This may leave readers wondering why I am so confident in the potential for an income cut. Part of this has to do with the fact that many muni CEFs (including many from Nuveen) have already seen cuts in Q3 and Q4 2022. The fact that NDMO survived those rounds of cuts surprised me, and I don't see it holding on much longer without falling victim to that trend. Supporting this idea is the fact that the most recent data from Nuveen shows NDMO has over half its distribution coming from return of capital:

Income Metrics (Nuveen)

The counter-argument could be that if NDMO hasn't been forced to cut yet it might not at all. This is a fair point and one that readers should contemplate when deciding on NDMO's value here. If the fund doesn't cut, there is probably only upside going forward.

But the chances of a cut seem high in my opinion given that the Fed is likely to keep on hiking interest rates in the first half of the year. I would expect one or two more .50 basis point moves. This is broadly a positive for stocks and bonds longer term but poses a challenge in the early stages of this year.

The relevance here is inflation remains elevated. This continues to be a global problem and will likely force the Fed's hand to hike its benchmark rate again the next time it meets:

{kind=link}

Until we see this story change dramatically, the Fed will keep on its hawkish path and short-term borrowing costs will remain on the rise. This impacts NDMO because it uses quite a bit of leverage:

NDMO's Leverage (Nuveen)

This dynamic will pressure the income generation of the fund and is central to why I see a real probability of an income cut. In order for this thesis to change, I would need to see a dramatic downshift in inflation (and expectations from the Fed by extension) very soon. That doesn't seem likely to me, so I will not be buying NDMO just yet.

Non/Low-Rated Munis Warrant Caution

Digging deeper into NDMO brings me to my next reason for caution. This is the general make-up and holdings of the fund. Naturally, the reason for a 9% current yield isn't just a discounted market price to underlying value. It also stems from the fact that more than half of the holdings are either rated junk or not rated at all - which usually signals below IG quality:

NDMO's Credit Quality (Nuveen)

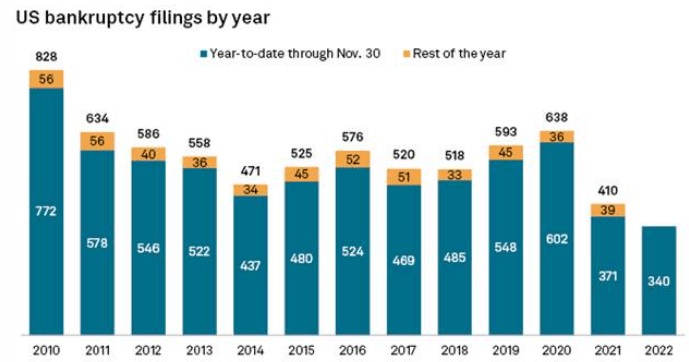

I am not trying to be overly alarmist here. Muni bonds - whether IG grade or below IG grade - tend to have lower default rates than similarly rated corporate bonds. There is a lengthy history of stability in this sector and that is likely to continue into 2023. Further, even within the corporate realm, the credit environment isn't terrible. After building up cash reserves during periods of ultra low rates, bankruptcies were down in the second half of 2022 on a year-over-year comparison:

Bankruptcy Filings (US Corporates) (S&P Global)

{kind=link}

My takeaway here is that both the corporate and muni sectors are supported well enough if we see some turbulence ahead. Both corporate and municipal issuers locked in borrowing at low rates in the past few years and a general economic recovery improved the cash reserves and "rainy day" funds of both. What this tells me is that there won't be as much volatility in credit markets this year as there was last year.

This comes with as asterisk, unfortunately. While I see a positive backdrop for credit this calendar year, that thesis falls apart if a severe recession takes hold. This will lead to a decline in corporate earnings as well as lower municipal tax revenues. The logic is that lower tax receipts will pressure lower rated munis first - and that is a problem for NDMO.

Aside from general weakness that could prevail in the muni sector, NDMO also has a hefty percentage to the Transportation sector. Roughly 1 in 7 of the underlying bonds in the CEF are in this sector. This is an area that offers investors some opportunity. If the economy improves, more people travel. Further, a growing workforce contributes to increased ridership on public transportation - such as rails, subways, and buses. Investors were careful when buying this sector in 2022, so there is some inherent value here. In this light, NDMO could be the right move for those who anticipate continued strength in the Transportation sector going forward. Normally, I'd be in this camp - and I am for the longer term. But as recession fears grow and the economy contracts, this is an area that will inevitably be hurt. Similar to my broader outlook that investors will be able to pick up NDMO at a better price if they stay patient, this outlook extends to Transportation muni bonds as well.

Munis Are A Reasonable Play If You Expect Stocks To Keep Dropping

My final thought considers muni bonds as a whole. This is relevant for NDMO or any other muni fund that readers are considering. As my followers know, I am a muni bull at this juncture and for 2023 going forward. This is especially true for investors who believe stocks are bound to keep on falling.

The logic here is that bonds tend to perform well when stocks fall - they are generally inversely correlated.

2022 Performance (Stocks & Bonds) (Yahoo Finance)

{kind=link}

What I am getting at here is that 2022 was an unusual year. Does that necessarily mean 2023 will be different? Of course not. We could be in for another year of broad losses in both categories. But history does not support that view, nor do underlying market fundamentals. With recession fears top of mind, there is a likelihood of equity weakness to start the year off (the first day of trading confirmed this to some degree!). If this continues, or volatility more generally picks up, then bonds could be a good place to hide out. This makes NDMO, and numerous other muni CEFs, a reasonable play.

Bottom-line

NDMO had a rough 2022 - and more pain could be on the way. The good news is that the big drop does offer investors a strikingly better opportunity to buy in than they had at pretty much any time last year. If munis see a broad rebound, NDMO will rally. The current yield and big discount to NAV are sure to bring in buyers at some point, but I would urge some caution. I see a distribution cut in the near term and this will almost certainly give investors a cheaper purchase price. In sum, I will keep NDMO on my radar as an income play, but stay patient in the hopes that I am able to pick this one up after another leg down.

For further details see:

NDMO: Remain Disciplined In Early 2023