RTL - Necessity Retail: A Mispricing In The Sub-Investment Grade Preferred Space

2023-04-24 02:46:26 ET

Summary

- Necessity Retail REIT is a retail REIT that owns single-tenant and shopping centre properties in the USA.

- The REIT is notorious for destroying common shareholder value but has two undervalued preferred shares yielding at least 9%.

- When compared to other REITs these shares are at least 7% undervalued which means double-digit returns until the call date look probable.

Introduction

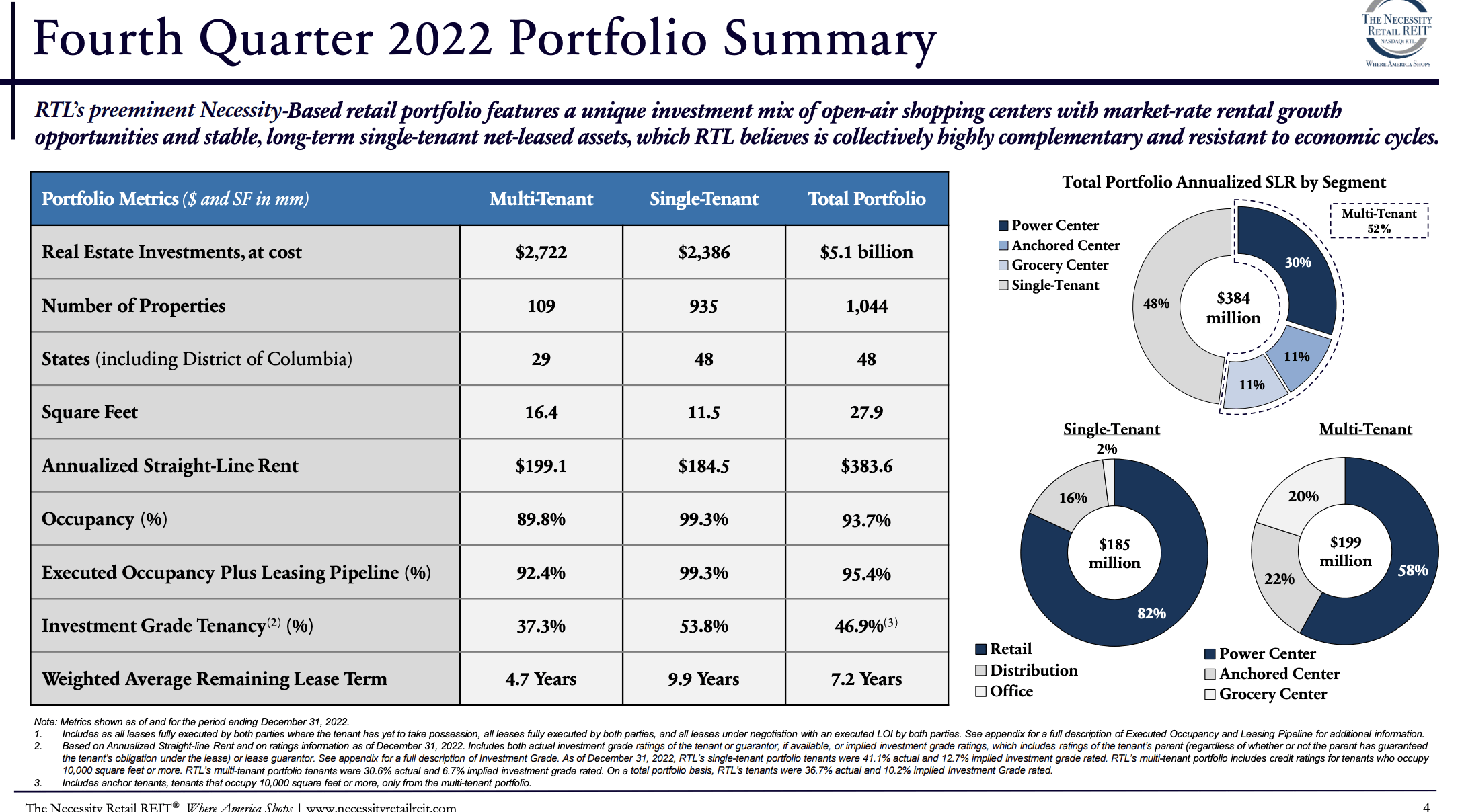

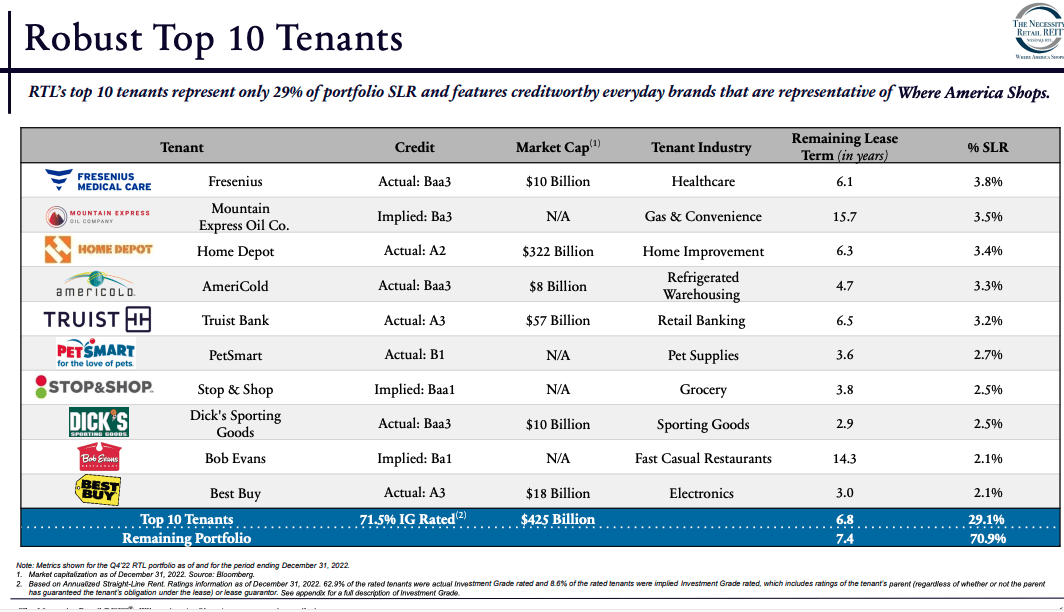

The Necessity Retail REIT ( RTL ) is an externally managed REIT in the U.S. that owns a diversified portfolio of freestanding single tenant properties with triple net leases and multi-tenant properties that consist of power and lifestyle centres. The REIT has properties geographically located among 48 states. As of 2022 FYE RTL owned 1,044 properties with an occupancy rate of ~94%. The average lease term on their properties is over 7 years and 71% of their top 10 tenants are investment grade. Main tenant focus is on "necessity" focused businesses that have less cyclicality and little e-commerce competition like grocery stores, retail banking, pharmacy, gas, convenience, and fitness centres. Top tenants include Fresenius Medical Care ( FMS ), Mountain Express Oil Corporation, Home Depot ( HD ), Americold ( COLD ), etc.

The Necessity Retail REIT Fourth Quarter 2022 Investor Presentation (The Necessity Retail REIT) The Necessity Retail REIT Fourth Quarter 2022 Investor Presentation (The Necessity Retail REIT)

{kind=link}

{kind=link}

One might wonder why with such a strong portfolio the common stock trades at a 19% discount to TBV and why it has badly lagged its peers and the U.S. REIT index over the last 5 years. What is even more curious is how the two peers shown below in RPT Realty ( RPT ) and SITE Centres ( SITC ) have BBB ratings (lower investment grade) while RTL is only rated BB (upper speculative grade) by the ratings agencies.

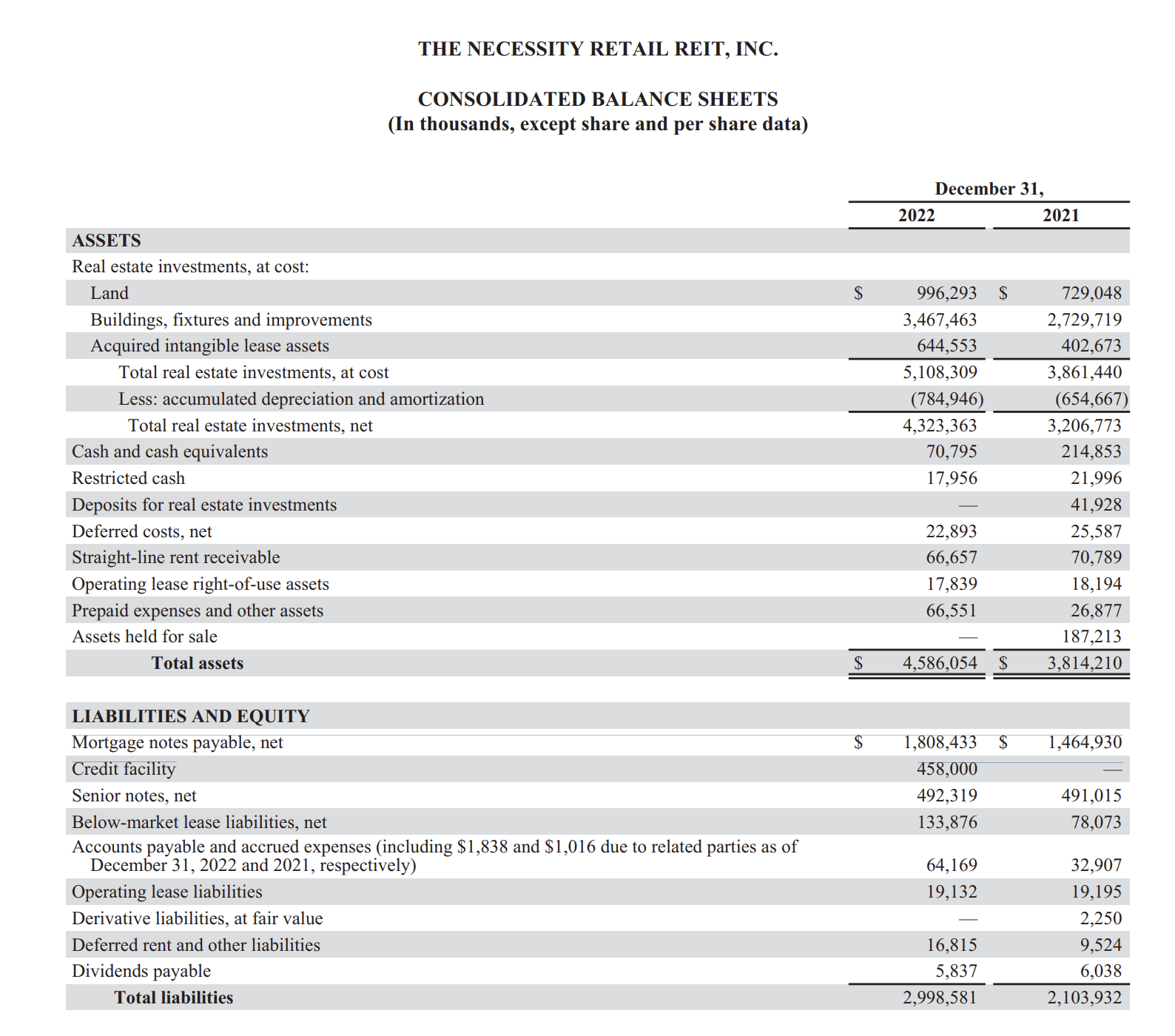

The likely reasons for this are the higher leverage RTL has a ~50% debt to assets and 9.3x Net debt to EBITDA which is pretty high for a retail REIT as the peers are not over 6x. RTL does have longer term leases and a more robust tenant profile which makes slightly higher leverage manageable. Although the dividend hasn't been cut since 2020 the AFFO payout ratio is still ~81% which is not particularly low. These factors don't make the 15% yield look particularly safe especially with a recession looming.

The REIT has also massively diluted shares since 2021 as the share count has increased 25% since mid-2021 and net debt increased almost 52% while AFFO/share increased only 4%. I prefer AFFO as it adjusts for accretion of market lease, straight line rents and financing costs.

{kind=link}

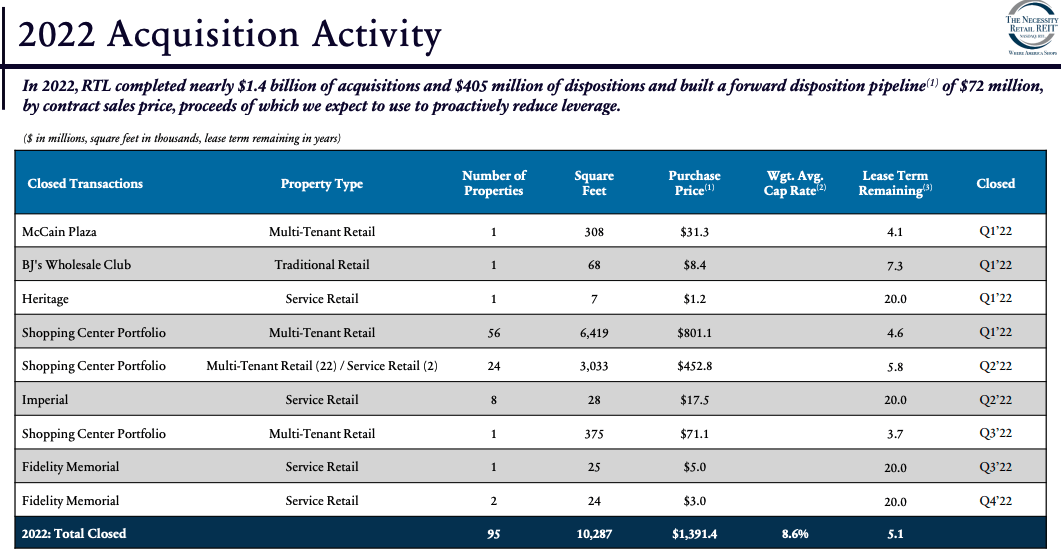

The reasons for the increase in the balance sheet was to finance the purchase of the CIM portfolio for $1.3 Million for a strategic shift away from a primary focus single tenant REIT causing management to abandon their deleveraging strategy initiated during COVID.

As a result of the acquisition 6,450,107 common shares were issued for $53 Million in proceeds for an implied price/share of ~$8.15 while the market price was ~$8.50/share for most of 2021. This may not seem like a large discount but keep in mind this was while the real estate market was still red hot with much lower interest rates than we see today. The going in cap rate was only ~6.8% on the portfolio and RTL decided to even increase the variable rate debt by drawing down $458 Million on their LOC by $458 Million bringing the percentage of fixed rate debt down to 84% from 100% the year prior. This is while the 15 and 30 year mortgage rates have gone above 6% which makes the spread on the CIM acquisition razor thin.

Safe to say management incentives are not fully aligned with shareholders and are essentially "empire building" to increase the size of the asset base to collect higher fees, regardless of whether it is accretive to FFO/share or not.

The Preferred Shares

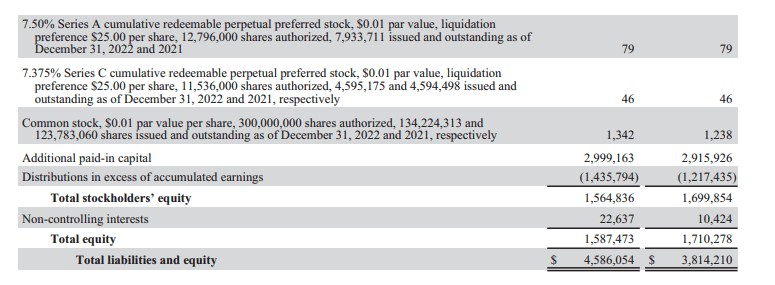

The external manager strategy does not always align with common shareholders but this does not have to hurt preferred shareholders. I discussed a similar opportunity with Imperial Petroleum's preferred shares ( IMPPP ) in October 2022 in my article titled Imperial Petroleum: A Juicy 11% Yield On Preferred Shares . Preferred shareholders can actually benefit as long as EBITDA rises faster than interest expense. This is because preferred shareholders have to be paid before the common, in fact RTL's preferred share issuances are cumulative and cannot suspend preferred shareholder dividends unless common are suspended first and all preferred dividends have to be caught up before common dividends can resume.

We can see below EBITDA covered preferred dividend payments and interest expense by a factor of 1.63x in 2022. Despite the acquisitions not being accretive, it is not to the detriment of the preferred shareholders.

RTL has two preferred dividend issuances outlined below.

| Issuance |

| Ticker |

| Price |

| Current Yield |

| Call Date |

| YTC |

| The Necessity Retail REIT Inc 7.50% Series A Cumulative Redeemable Perpetual Preferred Stock |

| (RTLPP) |

| $20.33 |

| 9.22% |

| 3/26/2024 |

| 37.17% |

| The Necessity Retail REIT Inc | 7.375% Series C Cumulative Redeemable Perpetual Preferred Stock |

| (RTLPO) |

| $20.15 |

| 9.15% |

| 12/18/2025 |

| 20.90% |

There is no direct comparison to these preferred shares as there are few callable retail REIT preferred shares that are less than BB rated but I compare REITs with BBB rated debt that have callable preferred shares.

| Issuance |

| Ticker |

| Current Yield |

| SITE Centers Corp 6.375% Class A Cumulative Redeemable Preferred Shares |

| ( SITC.PA ) |

| 6.38% |

| Spirit Realty Capital Inc. 6.000% Series A Cumulative Redeemable Preferred Stock |

| ( SRC.PA ) |

| 6.43% |

| Rexford Industrial Realty Inc | 5.875% Series B Cumulative Redeemable Preferred Stock |

| ( REXR.PB ) |

| 6.18% |

| Median |

| 6.38% |

These preferred shares shown above certainly deserve a lower yield that RTL's as a result of their lower leverage. Is a spread of 270-300 bps over RTL's preferred shares really warranted given the spread between the US High Yield B Effective Yield and US High Yield BB Effective Yield is only 196 bps. Based on this logic both RTLPP and RTLPO seem extremely undervalued.

The preferred shares make up a minuscule proportion of total equity, but cap rates have gone up so the BV equity figure may not be accurate. Assuming an 8.6% cap rate is appropriate for valuing RTL's properties as that was the weighted average cap rate of their 2022 acquisitions and a run-rate NOI of $345 Million, the NAV would be $1,114 Million or $8.43/share which provides adequate protection in the event of a liquidation.

The Necessity Retail REIT Fourth Quarter 2022 Investor Presentation (The Necessity Retail REIT)

{kind=link}

{kind=link}

Despite the rise in interest expenses YoY by 40 bps, RPT only has 12% of its debt due in the next two years so should only see modest increases in interest expenses and certainly not large enough to impact their ability to make preferred dividend payments.

The Necessity Retail REIT Fourth Quarter 2022 Investor Presentation (The Necessity Retail REIT) The Necessity Retail REIT Fourth Quarter 2022 Investor Presentation (The Necessity Retail REIT)

Final remarks

So which issue of preferreds should you buy RTLPP or RTLPO?

The answer depends on your view on where interest rates will be over the next year. If you are one who expects the Fed to completely reverse course and start cutting rates within that time frame then RTLPP is for you with its call date being in March 2024 and an enticing yield-to-call of ~37%. Notice how it has the slightly higher current yield though at 9.22% versus 9.15% for RTLPO, that is likely because the market does not see this as likely. If you prefer to give up 7 bps to get an already strong yield until at least 2025 RTLPO is for you. I personally fall into the latter camp. These issuances do not convert to a floating rate once the call date is reached.

Using the US High Yield B Effective Yield of 8.58%, I believe that these preferred shares are worth at least $21.85 which means they are at least 7% undervalued. With a ~9% yield these shares should be able to deliver minimum annual 10% returns until called.

For further details see:

Necessity Retail: A Mispricing In The Sub-Investment Grade Preferred Space