RTLPP - Necessity Retail: This Is Not The 14% Yield You're Looking For

2023-03-29 12:53:19 ET

Summary

- Necessity Retail is paying out a 14% dividend yield to its common shareholders.

- This is set against a tangible book value that has been under a sustained decline and fell by 28% year-over-year for its last reported quarter.

- The Series A preferreds offer a 9.1% yield on cost and are trading at a 17.3% discount to their par value.

Necessity Retail ( RTL ) last declared a quarterly cash dividend of $0.2125 per share , in line with its prior payment, and for a 14% forward yield. The New York-based externally managed REIT once traded as American Finance Trust, but changed its name early last year after the acquisition of a portfolio of open-air shopping centers. The current portfolio as of the end of the fiscal 2022 fourth quarter stood at 1,044 properties spread across 27.9 million rentable square feet in 48 states. It had a 93.7% occupancy rate with a weighted average remaining lease term of 7.2 years. As the name implies, Necessity is focused on retail properties with Truist Bank ( TFC ), Fresenius ( FMS ), and Mountain Express Oil forming its top three tenants.

Necessity's top ten tenants formed 29% of annualized fourth quarter straight line rent of $383.6 million , an improvement from a higher 38% concentration in the year-ago comp. There are a few things to like here. Firstly, the dividends have been stable and have stayed flat at their current payout level since 2021 when they switched from a monthly payout schedule. Whilst the REIT is rated speculative grade at ' BB ' by Fitch, its's funds from operations have been on the rise. Fiscal 2022 fourth quarter FFO per share was $0.27 , a beat by $0.03 on consensus estimates and growth from $0.22 in the year-ago quarter. This forms an 78.7% payout ratio, a material improvement from a 96.5% payout ratio in the 2021 comp.

The Tangible Book Value

Tangible book value is one of the most important metrics for REITs as this drives market capitalization. Necessity's tangible book value per share at the end of the fourth quarter was $8.56 , down sequentially from $12.16 in the third quarter and a 28% decline from $11.87 in the year-ago period. Hence, even though the commons are currently trading at a 29% discount to its tangible book value, this is under sustained pressure. The near-term outlook for this is not positive. Indeed, Necessity's percentage of fixed-rate debt was 83.6% as of the end of the fourth quarter. This was against a 4.4% weighted average interest rate which drove a quarterly interest expense of $34.5 million, a new record and up from $22.9 million in the year-ago quarter.

Critically, Necessity's external manager, AR Global, has not produced strong returns since the REIT went public with the stock down nearly 60% since this date. Whilst some of this weakness, mirrored by internally managed REITs and SWANs alike, is due to the rising rate environment, Necessity's eroding balance sheet provided a reason to not buy the commons even against its healthy dividend coverage and fat yield.

The 9.1% Yield Series A Preferreds

Necessity's 7.50% Series A Cumulative Perpetual Preferred Stock ( RTLPP ) pays out a $1.88 annual coupon for a 9.1% yield on cost. These started trading before the pandemic in 2019 and are coming up for redemption next year on March 26, 2024. Whilst the yield is 490 basis points lower than the commons, the preferreds offer a hedge against historical balance sheet deterioration with its price essentially anchored around their $25 par value.

{kind=link}

Hence, with the Series A currently at $20.68 per share, they're trading at a 17.3% discount to their par value. This opens up the preferred holders to another avenue of returns as together with the annual coupon, the yield to call at 28.86% is material and in excess of the common dividend yield. These are perpetual and there is no certainty to the REIT redeeming the Series A next year, however, the current discount to par represents a strong margin of safety.

They're down 18% over the last year on the back of rising Fed funds rate. Essentially, newly issued preferreds with the same risk profile would come with a higher headline coupon rate which causes current owners of the Series A to sell their position. Hence, the preferreds will continue to see weakness with rates likely set for a further 25 basis point hike. The inverse then stands to be true, rates will remain elevated but they'll eventually start to come down once inflation is stabilized at the Fed's 2% target rate. This opens up the prospect of stronger long-term returns.

{kind=link}

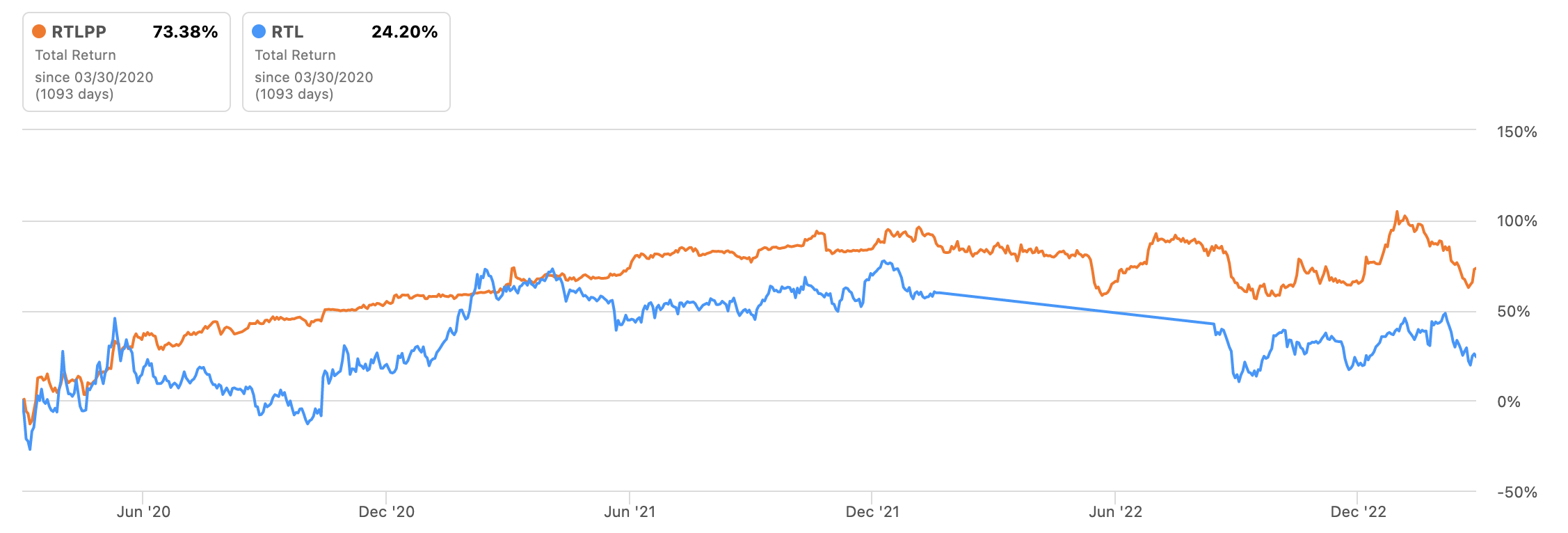

The preferreds are up 74% on a total return basis over the last three years versus a gain of 24% for the commons. Over the last 12 months the preferreds are sporting a loss of 4.87% versus a loss of 12.81% for the commons. I expect this performance dynamic will be reflected through 2023 as a still rising Fed funds rate continues to play out this year to hamper Necessity's book value. Against this, the preferreds form the better buy with the commons likely to see more short and medium-term weakness only partially softened by the fat 14% yield.

For further details see:

Necessity Retail: This Is Not The 14% Yield You're Looking For