NNI - Nelnet: Transitioning To A Best-In-Class Capital Allocator

Summary

- Nelnet is viewed by the market as a finance company but is successfully transitioning to a collection of growing companies.

- Management has an exceptional track record of allocating capital and compounding book value per share.

- Nelnet is undervalued because of several hidden assets on the balance sheet, which creates an incredible buying opportunity for investors.

Overview

Generally, when I start an article I like to briefly describe the operating business, but given that Nelnet ( NNI ) is not a pure play, it's impossible to give a brief description.

Nelnet is a conglomerate with 5 operating segments that, due to regulatory requirements, are required to report on. Additionally, they have an "Other" segment with some extremely interesting hidden assets, which I will dig into as well.

The main strategy at Nelnet is to continue to use proceeds from their legacy credit/asset finance businesses to invest further into their fee-based businesses. This is the main transition that we will focus on. For better or worse, they're considered a financial company, but they are moving further and further away from being considered a financials company.

Let's first march into the operating segments so we can see the incredible businesses they have built and what you're buying with Nelnet.

Operating Businesses

I'm going to go in order of how similar each business is to one another, but the 5 operating businesses are as follows:

1. AGM - Asset Generation & Management AKA Nelnet Financial Services

Nelnet's core/legacy operating business is to generate interest income from its portfolio of student loans. The company has been servicing these loans since 1978, but this business will die since the passage of the Health Care and Education Reconciliation Act of 2010 (the "Reconciliation Act of 2010") discontinued new loan originations under the FFEL Program, effective July 1, 2010. From the outside looking in, this is what many investors see when they think or hear of Nelnet.

As of 12/31/2022, the company had $13.6 billion in its FFELP Portfolio. From those assets, Nelnet was able to generate a Net Interest Income of ~$455 million.

It is well known that eventually all of these loans will be paid off, but the company is doing an amazing job at replacing these loans with new loans, including consumer loans and HELOCs, which I will talk about in other sections.

2. Nelnet Diversified Services

Nelnet Diversified Services is their loan servicing division. What this means is that even though Nelnet may not house the loan on their books, they do servicing for other companies and collect a fee for doing so. Nelnet services loans for federally backed student loans, private education loans, and consumer loans.

Nelnet owns two of the six private sector entities that have student loan servicing contracts for the department of education. As of 12/31/2022, NDS services $545.4 billion of student loans for 15.8 borrowers, and NDS collects a fee for each unique borrower. The department of education is NDS's largest customer and represents 32% of their revenue and 74% of this segment's operating revenue.

Typically, I would say having this much customer risk would be a bad thing, but given that it's the federal government and their money supply is seemingly never-ending (for better or worse), I would say this is a good thing.

However, with that being said, their contract with the government is set to expire on 12/14/2023. They're currently in the process of applying to be the next provider, but if they're not chosen or the terms are worse, it would materially decrease revenue for the company. Given the company's long-standing relationship with the government, I expect them to be chosen. Additionally, management believes the company's scalable servicing platform allows it to provide compliant, efficient, and reliable service at a low cost, giving the company a competitive advantage over others in the industry.

Unfortunately, this business is experiencing some hardship due to the fact that the government has delayed repayments until October 2023. In their latest letter, they discussed why they want to stay in this business and really how amazing of a business this is:

"...Regardless of what happens with the payment pause, there is nearly $1.6 trillion in student debt owed by 44 million Americans. Over its nearly 30-year life, the Direct Loan program has become the most complex consumer lending program on the planet. Nothing compares to it. The variability of payment options, loan types, forgiveness initiatives for public service, military service, deferments, forbearances, income-contingent payment options, disability benefits, and interest rates and terms require trained experts like our teams, with state-of-the-art systems and infrastructure like ours to administer them. The public's need for our services is immense. And even if the Supreme Court approves the White House's loan forgiveness program, it does nothing to solve the underlying need for student loan debt. By most projections, $160 billion in new student debt will be borrowed in each 2023 and 2024-and presumably every year we can see into the future. As long as there are colleges and universities and students who need to borrow money to attend them, the need to help people navigate the myriad of options and pay off their debt is tremendous, and we are here to make sure people have the best resources and help available to improve their lives and make their dreams possible."

The student loan servicing business is both strong and resilient, and Nelnet has developed a wide moat.

3. Nelnet Bank

In March 2020, Nelnet was granted an Industrial Bank Charter by the FDIC and the Utah Department of Financial Institutions. When they received this charter, it was the first new industrial bank launched since 2008! This shows how hard it is to get this charter.

The bank is a virtual bank with only 1 physical location in Salt Lake City. In only its second year of operating, the bank reached profitability and had its assets top $900 million while continuing to maintain proper levels of capital and liquidity.

The successful operation of this bank is crucial to Nelnet's other businesses because it can be seen as a source of loan replacement as its legacy student loan portfolio runs off. The private student loan product now supports over 569 institutions that serve over 4.6 million students!

Additionally, the bank has announced that the bank now supports a consumer loan product. They expect to enter this market in early 2023, so it's possible that they are already operating, though, I don't see any information about this on their website.

Although it's only been two years, it seems the team is doing a tremendous job at gathering loans, keeping low credit losses, and sourcing new assets for their loan book.

4. Nelnet Business Services

Nelnet Business Services is where we begin to stray away from the credit/asset finance business and go into their fee-based businesses. Nelnet Business Services is a collection of software that has to do with payments and administration in education, faith, and charity, or what they call giving management.

This business is broken down into 5 main segments which include

- FACTS

- Nelnet Campus Commerce

- Nelnet Payment Services

- Nelnet Community Engagement

- Nelnet International

FACTS

FACTS is an incredible management software system for facilitating the daily needs of the administration at a private school (K-12 education). FACTS provides financial management, administration (including cybersecurity), enrollment and communications, advancement (donation), and education development for schools. Additionally, FACTS is clearly an incredibly sticky product and works extremely well, as the company grew revenue from $184 million in 2021 to $244 million in 2022.

Nelnet Campus Commerce

Nelnet Campus Commerce also focuses on education but specifically in helping colleges and universities with an integrated e-commerce solution suite for student payments. Although management admits there has been declining college enrollment, Nelnet Campus has continued to grow revenue, has done so by growing from $99 million to $113 million while keeping retention rates over 98%.

Others

The other 3 businesses represent less than $100 million in annual recurring revenues, however, each is in a growing industry, and clearly management has an incredible track record to continue to allocate capital.

Also, if we look at last year's revenue rates in this segment, we can see how incredible these businesses are:

Operating Segment Growth Rates (Shareholder letters)

So, in 2022, an incredibly challenging year, management was able to grow this segment by over 23%.

This segment is one of the main reasons I believe that the market is undervaluing this company. These are incredibly sticky, recurring revenue, fee businesses that would suggest a much higher multiple.

5. Nelnet Communication Services/ALLO

Now, we are moving even further away from their more traditional businesses of credit/asset finance and education. ALLO is an end-to-end fiber optic network for businesses and residences in Nebraska and Colorado with a specific focus on underserved markets. In a different article, I wrote about how great these businesses are because once they're integrated, they are effectively monopolies. Additionally, these businesses are experiencing an incredible macro tailwind because people are increasingly working from home, and moving out to more remote parts of the country to get additional space. As a result, management said the following:

Mature market shares and cash flow continue to exceed our initial underwriting expectations. The demand is accelerating for communication and entertainment solutions across business, governmental, and consumer channels. As such, new market investments to increase regional density remain an on-going focus. ALLO's construction teams are actively developing markets and working around permitting delays. Unmet customer demand for high-quality fiber service bodes well for ALLO's future customer growth. Additionally, new work, gaming, and other entertainment needs are driving existing customers to increase bandwidth and services. Low latency and fast upload speeds are vital to the customer experience now more than ever. Customer growth is expected to accelerate in upcoming years with revenue per customer also on an upward trajectory as ALLO realizes the benefits from the construction efforts. Meanwhile, the benefits of scale are keeping the cost to connect and support ALLO's customer base efficient.

The company recently sold off a portion of this business and now only owns 45% of the company, but they now own preferred shares and will continue to receive dividends and, I believe, continue to see appreciation. Additionally, if their preferred shares are not redeemed by April 2024, then their 6.25% dividend increases to 10% as per the latest 10-K.

Also, they've now sold this business, so their equity position is now buried in the balance sheet, which I believe is helping to create the discrepancy in share price.

Hidden Value

So, now I want to get into the company's "venture"/other bets/other portfolios.

Nelnet Renewable Energy

Community Solar Explanation (Nelnet Renewable Energy )

Nelnet has been heavily investing in its renewable energy business. Here is a video that discusses their investment, and as of today, only has 47 views. In 2022, they committed to or funded a total of $634 million of tax equity to support the construction and operation of solar projects worth $2.45 billion. What they are actually receiving for their investment is obviously equity but also solar tax credits of either 26% or 30% of the cost when the project is placed in service.

Their strategy has been strikingly similar to their ALLO investment in that they're trying to create solar farm monopolies for small or underserved communities. Nelnet is pitching this to college towns, or small towns so that they don't need to pay for upfront costs, installation costs, maintenance, and insurance, and the subscriber still receives tax credits and saves on their energy costs. Notice how I used the word subscriber, as this is a subscription business. Once the solar farm is built, you pay a subscription recurring fee to this company.

Additionally, in the middle of 2022, Nelnet acquired 80% of GRNE Solar, a full-service engineering, procurement, and construction company providing solar services to residential homes and commercial entities. This allows them to be a vertically-integrated solar farm producer which will allow them to produce the farms at lower costs and be a differentiator in the market.

They are building a renewable energy utility business in front of our eyes and nobody is realizing it. Obviously, this isn't close to their main business, but in their latest letter, they've stated that they manage $278 million of tax equity (although $103 million is syndicated to co-investors in the solar projects), and even though these are loss-making projects, now management has found a way to make them accretive. See below:

Through December 31, 2022, we have recognized cumulative losses of $35 million on these investments, and our carrying value as of December 31, 2022, is negative $55 million. The tax laws require us to reduce carrying value by tax credits earned when the solar project is placed into service, and like ALLO, these investments also use the HLBV method of accounting. This in turn creates accelerated losses in the initial years of investment. We expect our current investments to generate $38 million in excess of our initial investment and approximately $73 million in GAAP income over the remaining years of the investment. It should be noted, we think this is a great use of capital; thus, we currently plan to make additional investments in solar in 2023 and beyond.

Management knows that this is hard to see on the balance sheet, so they have to spell it out for us in their latest letter. It's really incredible to see how talented management is to recognize an incredible opportunity like this which is completely outside of their core competency and create such a successful business in only a few years.

Hudl

Hudl develops cloud-based software that provides video and data on one connected platform. The company also provides online tools, mobile and desktop apps, smart cameras, analytics, professional consultation, and others for coaches and athletes to prepare for competitions. It offers Hudl to record and upload games, find key moments, start conversations, discover insights, access video anywhere, and showcase teams; Hudl Sportscode, a performance analysis tool that connects with a collection of online, offline, and real-time video and data analysis tools; Wyscout to analyze teams, matches, and players; and Hudl Assist that enables professional analysts to break down videos. The company also provides Hudl Focus, a smart camera to automatically record and upload games and practices to Hudl; Hudl Replay, a live video analysis solution to make data-driven decisions; VolleyMetrics for volleyball analytics; and Hudl Sideline, an instant replay system. It serves youth teams, high school, college, and professional team coaches in the areas of football, basketball, soccer, volleyball, wrestling, lacrosse, track, field, softball, baseball, hockey, and golf.

Because of the Lincoln Nebraska connection, NNI was in the seed round of this company to date has invested $83 million in various rounds, and in February 2023, purchased an additional $32 million in shares from existing shareholders. This investment is currently being held on their balance sheet but as the company says:

If Hudl were to complete an observable market transaction, we believe Nelnet would recognize a significant gain on this investment.

This company is private, so it's tough to assign a value, but the company has 2200 employees as per Capital IQ and has very well-known backers. I would be shocked if this company weren't already a unicorn, and Nelnet probably owns somewhere in the 10-20% range.

Rest of Venture Portfolio

So this piece wasn't talked about in the 2022 letter, but they gave us some insight into their so-called "black box" venture portfolio in the 2021 letter. I believe the reason they didn't talk about it this year was that they didn't do much in this space because of the wild valuations people were asking for, and even mentioned that we might be in a venture bubble. As a shareholder, I'm happy about this because it's telling me that they are only investing when they feel their capital is going to be put to good use.

Anyway, in 2021, they let us know the following:

Nelnet has invested approximately $115 million in early-stage companies over the last decade. In that time, the portfolio has returned just over $18 million with a remaining value of roughly $204 million. (The remaining value is based on "observable transactions," therefore, investments are held at cost until a new priced investment round or Nelnet determines that the company is no longer a going concern and the investment is written down.) This translates into a 1.94 multiple on invested capital (MOIC). Of the 91 investments Nelnet has made, 15 have exited, 23 have been written down or off, leaving 53 companies that are in various stages of growth.

So, clearly management has an amazing capability of identifying companies to deploy capital to, and I'm confident when valuations become depressed they will begin reallocating to this portfolio.

Real Estate

Amazingly, this is another venture in which they have been successful. In the past two years, Nelnet has recognized $45 million in gains from the sale of real estate, and their current portfolio has a carrying value of $80 million. However, like all of their other conservative accounting and hidden balance sheet assets, they believe that if they were to monetize this, they would recognize additional gains.

Capital Deployment/Shareholder Value

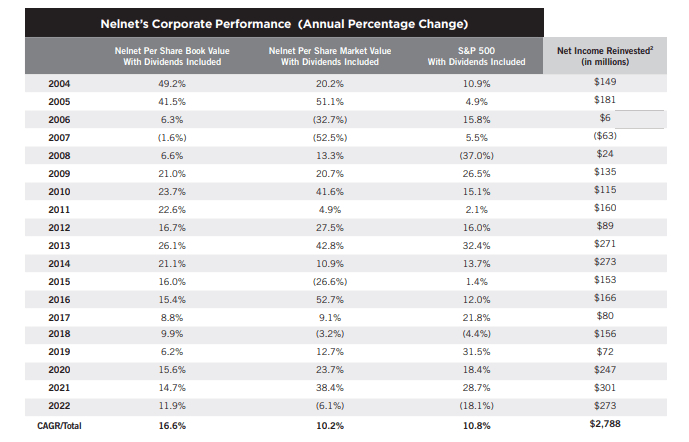

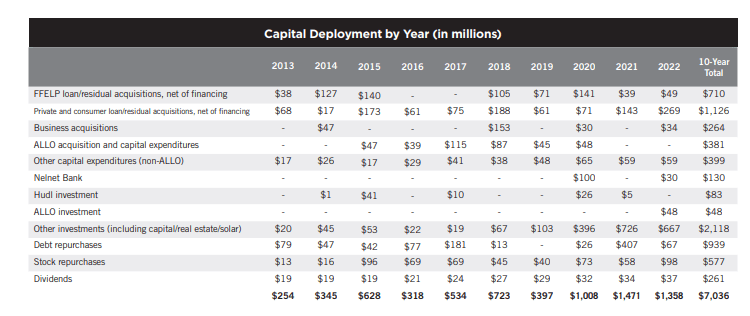

So, I know I've talked about the shareholder value they've created by going through all of their different businesses but now let's dive into the numbers. There are two very important charts that they focus on in every yearly update:

Corporate Performance (Shareholder Letters) Capital Allocation (Shareholder Letters)

{kind=link}

{kind=link}

Management tells you how they are deploying capital and shows you how it is helpful to shareholders. This company is incredibly shareholder friendly because the Chairman, Michael Dunlap, owns over 25% of the company. That's great for us because he is truly looking out for the shareholders since he's the biggest one!

Risks

To me, the biggest risk is what creates the opportunity which is that management is extremely conservative and can be a bit opaque in updating shareholders on the actual values of their investments. That being said, I'm fine with that because of the exceptional track record that management has.

Conclusion & Thesis

The book value per share is $86.16. So you're essentially buying a conglomerate with massively growing businesses at book value. Additionally, management has an incredible track record at compounding shareholder value. Lastly, management's incredibly conservative accounting plus hidden balance sheet assets are why this opportunity is created.

When the market realizes that this is no longer a finance company and is instead a collection of businesses with massive upside, there could be a massive revaluing of the share price to come more in line with multiples that their collection of businesses receive.

It's obviously tough to value this company, but by just using some common sense, you can see that AGM + NBS + HUDL is worth the current market cap of the company. You're getting the rest for free, and as a result, we could easily see shares revalued by 100% if we see something big get monetized or if the solar business is added as an operating segment (needed when it passes one of the 10% tests ).

In my opinion, this is a very compelling buy and now a core position in my portfolio. I can't see myself selling this for a long time and will continue to add more.

For further details see:

Nelnet: Transitioning To A Best-In-Class Capital Allocator