BSY - Nemetschek: A German Gem But Wait For A Better Price

2023-12-12 15:50:14 ET

Summary

- This relatively unknown German mid-cap has offered more than 1700% of capital appreciation to its long-term investors in the last decade.

- The company has very good long-term tailwinds as it requires digitizing the least digitalized sector: the construction sector.

- The company is well-diversified geographically, so we don't have to be worried about its exposure to Germany or Europe.

- There is a strong demand to upgrade the infrastructure globally, so software companies like Nemetschek are key players in making those improvements, so long-term tailwinds are guaranteed.

- I rate NEM as a hold; my sentiment toward the stock might be interpreted as "moderate buy" if investors prefer to start buying now and accumulate as the stock drops.

I rate Nemetschek (NEMTF) as a hold, as the stock price already incorporates decent revenue growth for the next few years. NEM has proved over many years to be a German champion, delivering very good long-term compounding returns for investors who held their shares for many years.

The architecture, engineering, and construction ((AEC)) industry, or, in other words, the construction sector, is the least digitalized compared to others given its high degree of fragmentation, its non-serial production processes, and its low profitability. Nevertheless, digital transformation is seen as a key competitive advantage by many players in the construction sector, and companies like NEM are called to lead this process of transformation in the industry.

NEM offers not only great long-term tailwinds but also strong competitive advantages that protect its business model from other competitors and future disruptions.

The company is in the process of increasing the participation of its subscription model from its total revenues, so it was understandable that there would be a slowdown in revenue growth for 2023 compared to 2022. This is a long-term benefit for the company, making its business model even more resilient and predictable.

I will explore NEM's business model and compare some key performance metrics with those of its main competitor in the construction sector. Finally, I will calculate the intrinsic value, assuming that I want to hold the shares until 2030.

Business Model

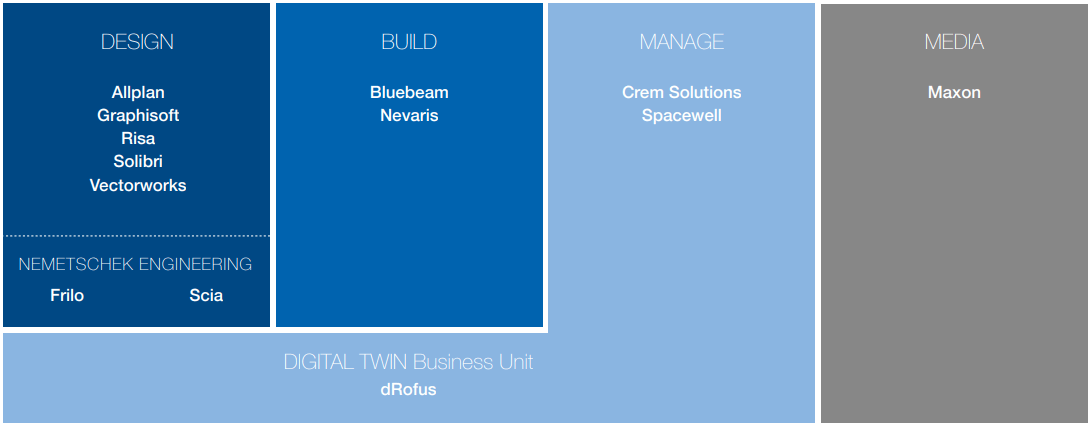

NEM offers software that covers the entire construction cycle: planning, designing, building, and managing buildings through its 13 different brands. The revenue breakdown as of 2022 by segment is the following:

Annual Report

It's clear that the design segment is the most important one, but the company is taking steps to reduce that concentration, pushing up other segments such as the build and media segments, as can be seen in the chart above. The 13 different brands are distributed across the different segments:

{kind=link}

The Design segment offers software, through 5 different brands, that is mostly used by architects, designers, engineers, owners, and general contractors to make planifications and designs for construction projects. NEM's updates in this segment are related to improving the coordination of workflows, particularly real-time workflows, among the different users of the same project to be more efficient and to enable a more sparing use of resources.

It's very interesting how these softwares are becoming key tools for customers as they need to face high prices of raw materials and the increasing demand for sustainability and energy efficiency in buildings. I can imagine that even in hard macroeconomic headwinds, these softwares are even more necessary to help construction companies reduce costs while supporting them to be more efficient in their capital allocation.

The Build segment, through the brands Bluebeam and Nevaris, offers software that is integrated from the bidding and award phase to invoicing, budgeting, scheduling, and cost calculation. NEM was working in this segment to develop cloud-based solutions; in this sense, this software enables users to work from anywhere while using any device.

The Manage segment is more focused on digitalizing the management of buildings, offering an innovative software portfolio. The brands Crem Solutions and Spacewell offer software that meets the increasingly pressing demand for more efficient buildings in a sustainable and environmentally friendly way while optimizing energy consumption. For instance, Spacewell Energy is a software as a service ((SaaS)) that helps detect, monitor, and reduce energy consumption in buildings by combining IoT sensors, real-time data, and artificial intelligence.

The media segment has been mostly strengthened by acquisitions in the last few years through the brand Maxon. This segment appears to be unrelated to the other segments, which are entirely focused on the construction industry. Nevertheless, I think that this media segment opens lots of future growth opportunities thanks to the very strategic acquisitions made by NEM.

Indeed, after the acquisitions of Redshift, which offers rendering solutions, and Red Giant, which offers solutions for motion design and visual effects, NEM, through its brand Maxon in the media segment, acquired Pixologic in 2021, whose brand ZBrush is considered the best 3D digital sculpting application among the experts. Sculping software is very popular among graphic designers and gamers since it can manage details in a way that would be impossible to do using traditional 3D modeling techniques.

NEM has integrated all the Maxon products into one package under a subscription model. As such, NEM has exposure to the growing 3D animation and the emerging metaverse markets with an end-to-end software portfolio along the digital content creation value chain.

In general, the NEM's strategy with all its different brands, particularly those smaller brands the company has been acquiring over the years, is to create value through cross-selling. Indeed, a small brand with a more local presence is expanded internationally through NEM's global network, jointly with other NEM's software.

Long-term Tailwinds and Moat

There are strong reasons to hold NEM for several years as the company enjoys clear long-term tailwinds:

www.elearning-journal.com

In the chart above, it's clear that the construction sector is at the bottom of the list for digitalization, as the construction sector is one of the least digitalized industries. The other sector that has a lot of room to digitize is the arts, entertainment, and recreation, so NEM was working to be exposed to that sector through its media segment, as it was mentioned before.

As such, the construction sector gives plenty of opportunities for players like NEM to offer more added-value software and to attract new clients. Also, regulations about building information modeling ((BIM)) in several countries are helping to ensure that BIM technologies become increasingly important in the construction sector. BIM is a digital representation of the physical and functional characteristics of a facility.

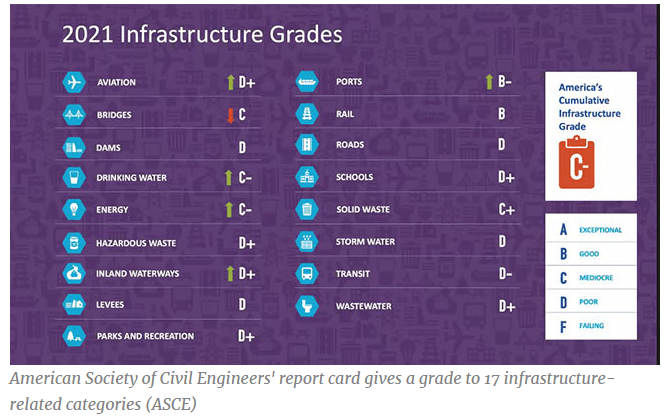

Another important factor is the inadequate infrastructure worldwide, particularly in those countries where NEM's revenues are exposed, like in the case of the US.

{kind=link}

The last report card made by the American Society of Civil Engineers ((ASCE)) was in 2021, assessing the infrastructure grade of C, which clearly indicates that the US infrastructure in several sectors requires upgrading. NEM has bought several companies in the US, such as Red Giant, Bluebeam, etc., in order to reinforce its market position in the US, representing around 34% of that market's total revenues.

Annual Report 2022

It's expected that the share of revenues that come from the US will not change significantly in 2023.

With regard to Europe, according to FitchSolution's study:

In the medium term, between 2023 and 2027, we expect the Europe region to average annual real growth of 2.1% below the global construction industry's average of 3.2%% y-o-y over the same period.

The main factors behind this performance are the macro headwinds and the high construction material costs. It's clear that if the US needs to upgrade its infrastructure, Europe might need to do so too to keep being competitive.

According to a study of the construction sector at a global level, it's expected that the building construction market will grow at 9.8% CAGR and residential building construction will grow at 5.4% CAGR in 2032.

Nemetschek's moat

NEM has an interesting moat, which is based on the fact that it's really expensive for any of its more than 6 million users globally to switch to other providers. These kinds of software are learned in universities, colleges, and institutes in the fields of engineering, architecture, or design, and the learning curve to master them is very gradual. This contributes to having a very fragmented market, which strengthens the barriers to entry for new players.

Also, NEM reinforces that stickiness of users having a recurrent interaction with its users, which enables it to develop new features that add value to customers. For instance, that's how NEM identified years ago that one of the main obstacles to working with these softwares was the problems associated with the collaboration among different professionals on the same project. Now, NEM offers the possibility to have a way better coordination of workflows among members of a work team in real time about the same project, enabling the work team to be more efficient while using its resources better.

As such, the software is not easy to learn, and the company makes you stick to the brand while offering better and better improvements that truly add value to your work. However, there are other aspects that make NEM a company to be on our radar: NEM does not use stock-based compensations as many other SaaS companies do, so there is no dilution to shareholders.

NEM has specific requirements to buy potential subsidiaries, such as size, profitability, culture, vision, etc. Thus, it's not a surprise that NEM has enormously reinforced its business model with its very good acquisitions, as the company also lets those subsidiaries operate independently once they are part of the group. In addition, NEM buys most of these good subsidiaries at decent prices; for instance, NEM bought Abvent in 2022, paying 0.28x times sales, and DC Software in 2022 too, paying 1.31x times sales.

Annual Report 2022

I do not like how much NEM paid for Pixologic in 2021, a total of 121 million euros, which meant around 34x sales; however, I do understand that this acquisition was critical to reinforce NEM's media segment for long-term growth, and the high price does not affect NEM's financial situation, particularly when the company has generated a FCF of around 200 million euros in each of the last 2 years.

Although the price paid was high for that acquisition, NEM might take advantage of his global network to expand the operations of Pixologic to get the highest value possible, as it has done in each of its other acquisitions. Also, I know that it's not always possible to find very good potential acquisitions at decent multiples, so NEM has reinforced its strategy of investing in start-ups, which would enable it to get innovations faster.

Results Q3 2023 and Outlook 2025

NEM delivered a revenue growth of only 5.53% and a drop in its EPS of -10.8% as of September 2023 YoY. Normally, NEM delivers double-digit revenue growth. The reason behind this apparent not-so-good performance is the process in which the company is involved in migrating all its revenues based on licenses, which are mainly one-off payments, to subscriptions, which are recurrent. NEM is executing this transition very well, as a change like that could have reduced revenue and earnings growth, and most importantly, the free cash flow ((FCF)).

Annual Report 2022

In the chart above, I see that recurring revenues increased from 61.1% in 2021 to 66.4% in 2022. These recurrent revenues are expected to reach 75% in 2023 as part of this process. It's really interesting that even under these conditions where the FCF is pushed down as a subscription model implies, at the beginning, less cash from license payments, NEM managed to deliver a higher FCF, reaching 171 million euros, which represented a growth of 9.5% as of September 2023 YoY.

A higher proportion of subscriptions from the total revenues supports the company in establishing more accurate guidance while helping it to make its business model more predictable. This also contributes to delivering a more stable FCF and revenues, making the company's business model more resilient in difficult scenarios.

Nemetschek Presentation Q3 2023

{kind=link}

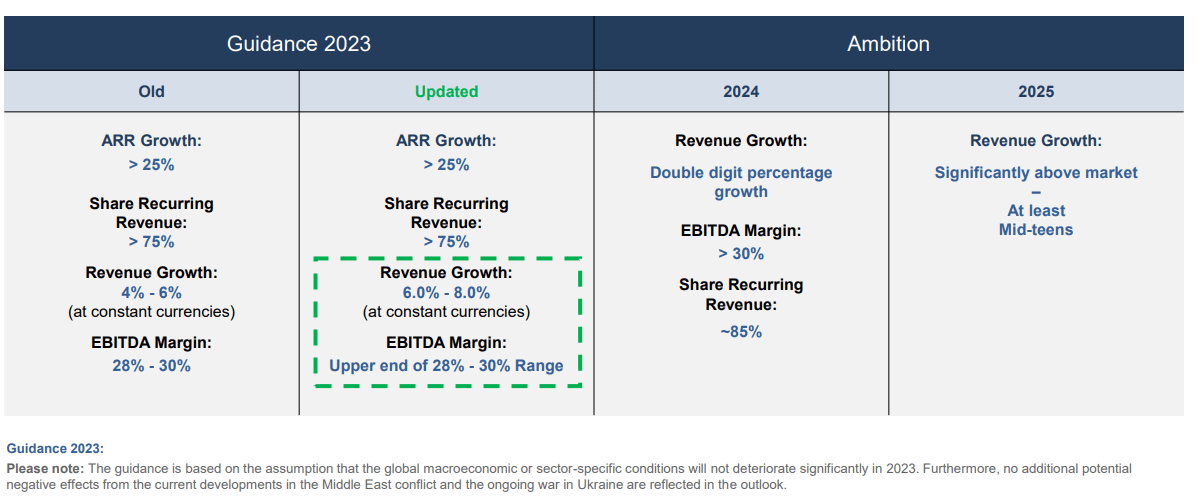

According to the guidance, NEM has given a revenue growth expectation of 4% to 6% for 2023 at the beginning of the year as a consequence of the migration to a subscription model from the license model. Nevertheless, NEM raised those revenue growth expectations to 6%–8%, which was taken very positively by the market. Also, the share of recurrent revenues is expected to reach at least 75% in FY2023, which indicates that the migration process is being executed as expected.

In addition, NEM has set other ambitious targets for 2024 and 2025, as the company expects double-digit revenue growth with a solid EBITDA margin and a share of recurrent revenues reaching 85% in 2024. I estimate that a conservative assumption might be a revenue growth of 10–11% for 2024. For 2025, NEM expects revenue growth of at least 15%, which means that the company has finished its migration process with higher recurrent revenues and even more opportunities to deliver new subscription-based services to current clients and new ones.

I will incorporate these estimations in our calculation of the intrinsic value.

Nemetschek's Closest Competitor: Autodesk

I've found that Autodesk (NASDAQ: ADSK) is NEM's closest competitor, even when both companies are mostly exposed to different regions. Most of Autodesk's revenues come from the US, and NEM has relevant exposure in the US but is mostly exposed to Europe.

{kind=link}

Looking into the table above, I may see that both companies have had very good returns on capital, low levels of debt, high FCF margins, and double-digit revenue growth in the last few years. Both companies spend similar ratios of R&D over revenues, which indicates that both are continuously investing in their respective businesses to maintain their market position.

However, I like more how NEM manages its business, as the company does not use stock-based compensations to attract talent, even when NEM is able to hire talented professionals who are attracted to its good name in the industry. On the other hand, I like that NEM uses most of its FCF to be reinvested in its own business, developing more valuable innovations to further reinforce the stickiness of its software.

Conversely, Autodesk has used more than 50% of its FCF in the last 5 years to make repurchases, so the company has less money to reinforce its business. In addition, part of the repurchases' effect is compensated by the dilution of the stock-based compensations granted to its employees.

In column 10, I notice that the subscriptions represent 92% of Autodesk's total revenues, whereas NEM is still in the process of increasing its revenue through subscriptions, leaving the company with more growth prospects as it might increase even more that proportion of subscriptions in the next few years. Autodesk made this transition in the years 2016–2019, which was not easy for the company as its revenues, net income, and FCF declined substantially, delivering negative ROE and ROIC as its equity was accumulating the negative income and it did not reduce its share buybacks, which are considered negative within the equity in accounting terms.

Of course, Autodesk is a more robust company now showing good performance since then, but the way those transitions are managed gives us a sense of the management's execution, and NEM is taking more gradual steps to migrate to a fully subscription model without affecting its financial performance materially, giving more confidence to its shareholders in the process.

Valuation

According to SA, all the multiples for valuation indicate that NEM is expensive compared to its peers:

{kind=link}

I know that NEM is a high-quality business, so most of these multiples assume that every company has the same quality, which is not true. So, I will calculate an approximate intrinsic value based entirely on NEM's own merits.

First, I will need to make certain assumptions:

- Outstanding shares: 115,500,000 (as of September 2023)

- FCF Margins: 22.67% (average of the last 5 years)

- I assume that NEM is held until the year 2030.

- Revenue growth for 2023: 6%–8%, according to management's guidance

- Revenue growth for 2024 and 2025: according to management's guidance

- Revenue growth beyond 2025: I assume 15% annual as I estimate that its migration process to a full-subscription model is completed.

- P/FCF 2030: 40x (average of the last 8 years)

- Discounted rate: 9%

{kind=link}

Based on our assumptions, I make a projection of revenue growth of 6% for 2023, 11% for 2024, and finally 15% for 2025 and beyond. So, I take the revenues projected for 2030, and then I multiply those revenues by the FCF margins of 22.67%. NEM has been very consistent in the last 10 years, so that FCF margins could be even higher for 2030; then, as a result, I get an approximate FCF of 454.8 million euros for 2030.

Now, I take that FCF of 454.8 million to be divided by the outstanding number of shares of 115.5 million shares to get a FCF per share for 2030, getting 3.94. In this sense, I take the FCF per share of 3.94 and multiply it by 40, which is the NEM's average P/FCF of the last 8 years. Then, I get a target price of 157.5 euros per share in 2030, so I calculate the present value to bring it back to 2024, considering that 2023 is almost finished.

Thus, finding the intrinsic value:

Intrinsic value = 157.5/(1+discounted rate)^7

Finally, I get an approximate intrinsic value of 86.18 euros per share. The current stock price is around 77 euros per share, but there is not enough margin of safety. If an investor is attracted to the company, he might buy now but needs to be ready to buy more shares as the stock price declines. A sensitivity analysis could help us to know a more approximate range of intrinsic values, changing our main assumptions:

Author

I noticed that a P/FCF of around 33x is what the market is willing to pay in hard scenarios for this high-quality company; this is what I saw in the last quarter of 2022 when there was so much uncertainty about the effects of the fast interest rate hikes by the FED in the global construction sector. On the other hand, a P/FCF of 40x is an average multiple, so I build two scenarios, as is seen in the table above.

In addition, NEM's management stated that from 2025 on, they expect at least 15% revenue growth. Therefore, in a conservative way, I can set a range of intrinsic value, looking at the numbers shaded green, between 69.63 and 88.9 euros per share, roughly. I accumulated shares at a price of 60 euros per share to construct a margin of safety.

Of course, NEM is able to deliver a revenue growth of more than 15%, or the market might be willing to pay a higher multiple P/FCF than 40x in 2030, which would boost the intrinsic value to levels higher than 93 euros per share, but I need to be conservative in our projections to build up a margin of safety.

Risks

NEM operates in a very cyclical industry like the construction sector, so when the economy exhibits weakness with high interest rates, the construction sector might suffer, and all the players that are part of that sector might suffer too.

Nevertheless, NEM has a well-diversified pool of customers across 142 countries , so diversification significantly reduces this risk, as recessions do not affect every economy in the world with the same intensity. In addition, NEM's software has become an essential tool for engineers, architects, and designers to be more efficient in the use of their resources in scenarios with high costs of raw materials, among other uncertainties.

Competition might be another factor that could slow down NEM's revenue growth, as there are formidable players such as Autodesk, Bentley Systems (NASDAQ: BSY), or even Ansys (NASDAQ: ANSS). However, this is a very fragmented market with lots of growth opportunities for every player, given the huge long-term tailwinds of the construction sector, which turns out to be one of the least digitalized industries in the world.

On the other hand, NEM has demonstrated solid execution in its organic and inorganic growth over the past decades. Also, NEM has reinforced its moat through its continuous investment in strengthening engagement with its users and developing new innovative releases that turn out to be very valuable for customers. All of these could be seen through its high returns on capital of more than 20% consistently over the years, low debt levels, consistent revenue growth, high FCF margins of more than 20% consistently, etc.

Maybe what could represent another risk for some investors is the high stock volatility. Some investors who are more focused on the short term or middle term might find this stock unappealing, as the stock can move strongly, sometimes going up or down without any news. Nevertheless, this stock works very well for long-term holders, as every big drop can be harnessed to buy more shares while enjoying the long-term compounding benefit of a company that truly knows how to surf the macro headwinds since it was founded in 1963.

Final Thoughts

Sometimes, a short report on companies like NEM does not give us enough information to appreciate how good they truly are. In this article, I wanted to show that NEM might be one of those few European gems that truly deserves to be included in any portfolio with a long-term horizon.

The company is a cash cow machine that is able to deliver double-digit revenue growth consistently. Once its migration project reaches a full subscription model, NEM will have an even more resilient business model that will open up more opportunities to offer new subscription services while receiving more cash flows as part of its current software services.

It is not surprising that the market is willing to pay high multiples for this company, given that NEM combines solid revenue growth and FCF margins. There are lots of growth stocks out there, but most of them are relatively new with less than 15 years of operations. Conversely, NEM is a company founded in the 1960s that was able to adapt itself to all the megatrends experienced since then and is now working on the current megatrends: the development of cloud features across its different brands and various artificial intelligence initiatives.

For further details see:

Nemetschek: A German Gem, But Wait For A Better Price