ADSK - Nemetschek: A German Hidden Champion In An Underserved Industry

Summary

- The construction industry is very inefficient.

- Digitalization is not present in most construction companies and offers a large market opportunity.

- Nemetschek SE is a highly profitable hidden champion out of Germany.

- This family business could offer a lucrative investment opportunity.

Nemetschek SE (NEMTF) is a leading software company in the architecture, engineering and construction ((AEC)) industry. Nemetschek SE is considered a strong player in the AEC market and a potential investment opportunity in a growing, underserved market. In this article, I will show the opportunity ahead of Nemetschek and how the company can benefit from it.

An underserved market

Construction is one of the largest industries in the world. According to expert market research , the sector, valued at $12.74 trillion globally, is expected to grow at a 6.5% CAGR, driven by emerging markets. That's 12% of the global GDP ! Naturally, a market of this size that is essential in all parts of the world is very fragmented, with millions of different players ranging from small and midsize businesses ("SMBs") to large billion-dollar conglomerates.

Most players in the construction industry are old-fashioned and not up to date on modern technology. This is evidenced by the low adoption rate of digitalization compared to other industries.

Construction lagging behind Digitalization (Nemetschek Company Presentation)

What can technology do?

Yet there are multiple reasons why construction companies should embrace technology (data from Nemetschek):

- 90% of Construction projects are delayed or have higher costs than anticipated

- 40% of global CO2 emissions come from the construction industry (remember, it is just 12% of GDP)

- 35% of all waste in the EU is from construction and demolition

- >20% of materials are wasted due to remodeling and poor planning

- There is a lack of workforce in the industry.

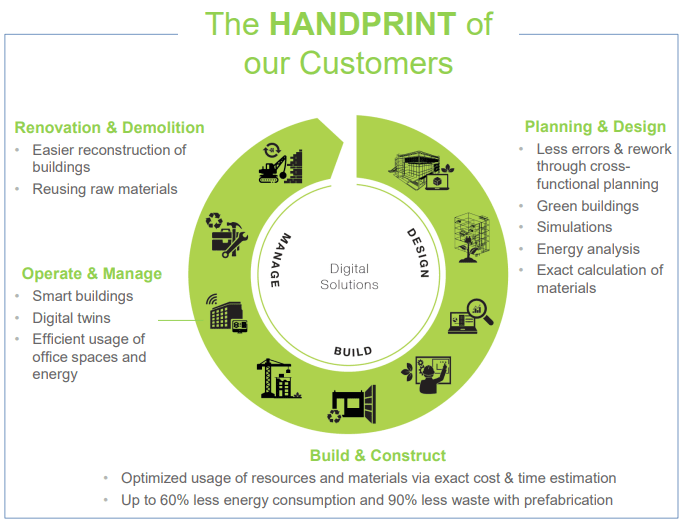

These points result in a significant interest of all stakeholders to increase the efficiency of construction projects. This includes not just the PnL of construction companies but also municipalities and all people who want to reduce the waste of resources. Nemetschek is a leading player in the entire lifecycle of a construction project. A construction project goes through several phases, starting with the planning and design process, where the project (be it residential housing, large office complexes, a manufacturing facility or a bridge) is planned and simulated. This is followed by the build & construct phase, where the project is built. Depending on the type of project, it also needs to be operated and managed, think office buildings or manufacturing plants. Lastly, the project will eventually need to be renovated or demolished. Nemetschek offers solutions for all of these needs.

Serving the entire lifecycle (Nemetschek Company Presentation)

{kind=link}

How big is the opportunity?

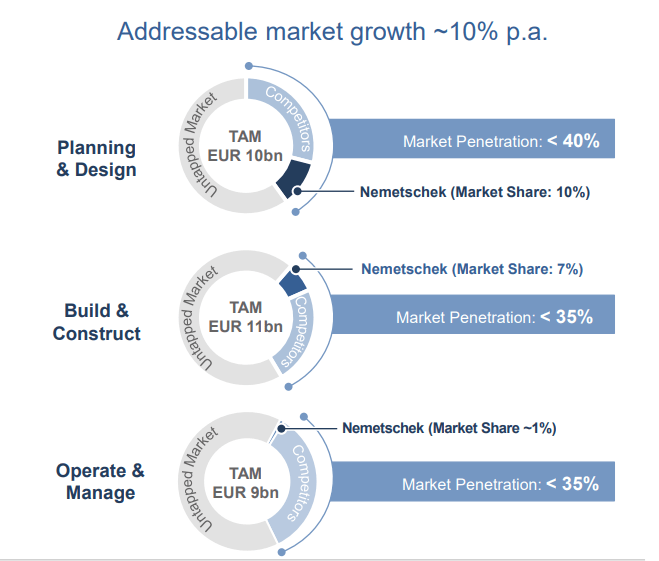

The market for software to aid the construction industry is around $30 billion currently throughout segments. On average, these segments are expected to grow at 10% per year and have a largely untapped market opportunity with under 40% market penetration in all sectors. Nemetschek is one of many players in all its segments, but it has the advantage of offering products throughout the entire life cycle of a construction project. This should allow the company to continue to grow with the market and take market share away from competitors.

Nemetschek also is a proponent of open data standards to increase collaboration and efficiencies. This allows customers to use Nemetschek alongside competitors' products without having to convince them to join a walled garden.

{kind=link}

Transition to SaaS

Nemetschek already has a very resilient business through its 65% share of recurring revenues. The remaining revenues are mainly software licenses with some consulting & hardware sales. In recent years, the company has been pushing the transition to Software as a Service (SaaS), which has grown from 5% of revenues to 25% as of the latest earnings report. The remaining 40% of recurring revenues are software services. The company recently introduced a new metric to track the transition: annual recurring revenues ((ARR)). SaaS has been growing much faster than the other parts of Nemetschek, at 49.5% CC in the first nine months of 2022, versus 21.6% CC for total recurring revenues.

Unlike many other companies that transitioned to SaaS, like Adobe Inc. (ADBE), or Nemetschek's biggest rival for many products, Autodesk, Inc. (ADSK), the company did not opt for a complete transition but rather a gradual one. With a fragmented industry far behind on digitalization, there are still customers who will purchase the old models like licensing. Eventually, Nemetschek is looking to upsell these customers. The transition will impact margins in the short term, but it should result in a better margin profile once the transition is completed.

Already a cash machine

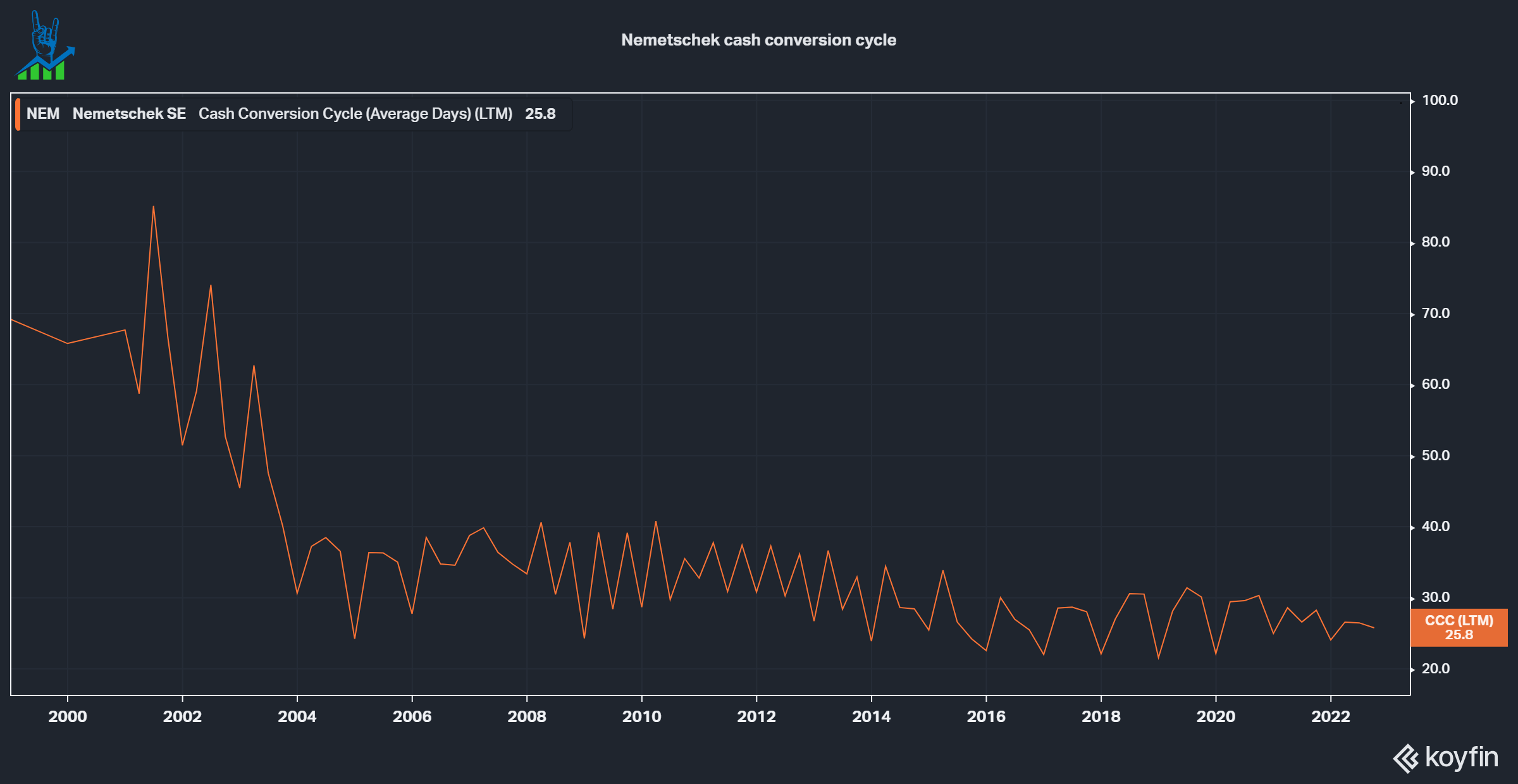

Unlike many other small/mid-cap growing software companies, Nemetschek is already highly profitable. The company generates a 33% EBITDA margin and converts a strong 86% of its EBITDA to free cash flows (27% FCF margin). Net income is lower than Free Cash Flow. I believe the transition to SaaS will drive the Cash Conversion Cycle lower, positively benefiting FCF conversion.

{kind=link}

An attractive buy

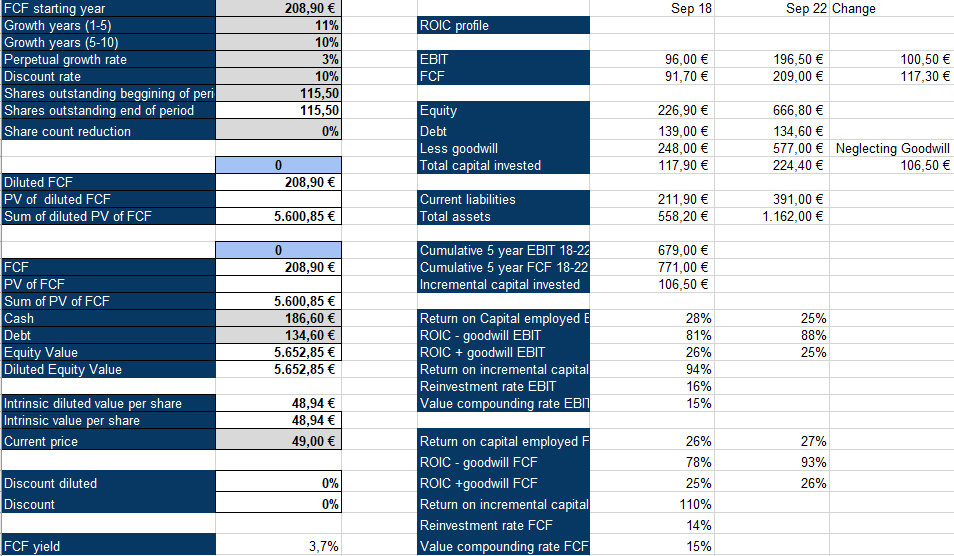

The graphic below shows an inverse discounted cash flow ("DCF") model (left side), which we will use to value the company and its Return on Capital profile (right side). Let's start with the valuation; for this, we use a 10% discount rate, a 3% perpetual growth rate and a 0% dilution (Nemetschek has never issued a new share and has a large anchor investor with over 50% of shares outstanding in the Nemetschek Family and Foundation). The company has an exceptional balance sheet with net cash and produces strong free cash flows. At the current share price, the market is pricing in an 11% CAGR for the next five years, followed by a 10% CAGR for the following five years. I believe this is very realistic, given the market growth rate of 10% CAGR and my belief that Nemetschek will be able to gain market share.

The company also produces strong returns on capital, measured with ROCE, ROIC and ROIIC + Reinvestment rate. I calculate these values with EBIT and FCF instead of NOPAT because those are the values I look at to value a company as well.

Nemetschek Inverse DCF Model and Return on Capital profile (Authors Model)

{kind=link}

A high-quality German compounder

I conclude that Nemetschek SE is a high-quality hidden German champion with a long growth runway. The construction market needs to change and Nemetschek can help. With its robust and profitable growth rates and high returns on capital, the company should be able to continue rewarding shareholders as it did in the past (38% CAGR over the last twenty years, even after a 50% drawdown). I am considering Nemetschek SE as a new position in my portfolio and might initiate a position in the stock soon.

For further details see:

Nemetschek: A German Hidden Champion In An Underserved Industry