NEMKY - Nemetschek: Hidden German Stock Market Gem

2023-08-22 10:00:34 ET

Summary

- Nemetschek is a German company providing software solutions for architects, designers or engineers as well as companies operating in the media and entertainment industry.

- The company has a wide economic moat based on switching costs and cost advantages as Nemetschek is operating in a niche.

- While management is expecting double-digit growth rates for the years to come, we should be cautious due to the slowdown in the construction industry in Germany or the United.

- The stock could be fairly valued at this point, but I would rather wait and the stock will remain on my watchlist.

In the last few months, I tried to expand my watchlist and covered several companies I did not cover before. A lot of inspiration came from the podcast “ Business Breakdowns ” but the following company is not part of the businesses analyzed in this podcast.

And as we are talking about a mid-cap business from Germany, I would assume most people outside the industry and outside Germany never heard the name. And even in Germany, I would guess a lot of people never heard about the company headquartered in Munich – Nemetschek SE ( NEMTF ). While the company does not seem to be on most investors’ radar, the business is fitting the criteria for wide moat companies clearly and could be a great long-term investment.

Business Description

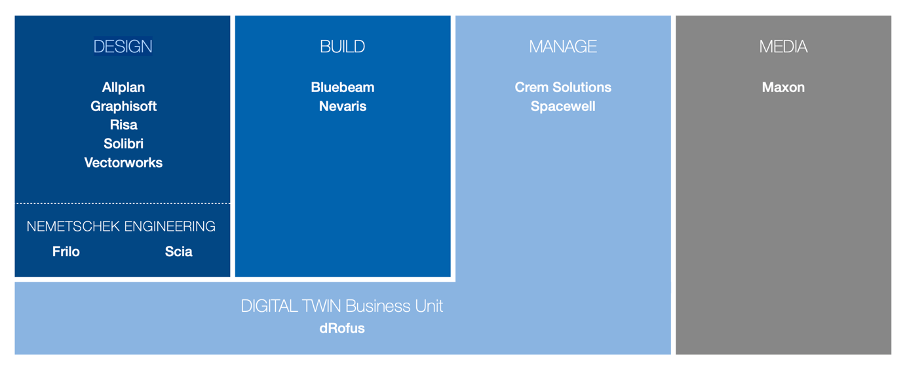

Nemetschek SE was founded in 1963 by Professor Georg Nemetschek - a civil engineer and professor at the University of Applied Sciences in Munich. Today, Nemetschek is not only a global provider of software solutions for the AEC/O industry – architecture, engineering, construction, and operation – but is also offering solutions for the media and entertainment industry. Nemetschek SE can be described as a strategic holding company that is clustered in four segments and has 13 different brands.

{kind=link}

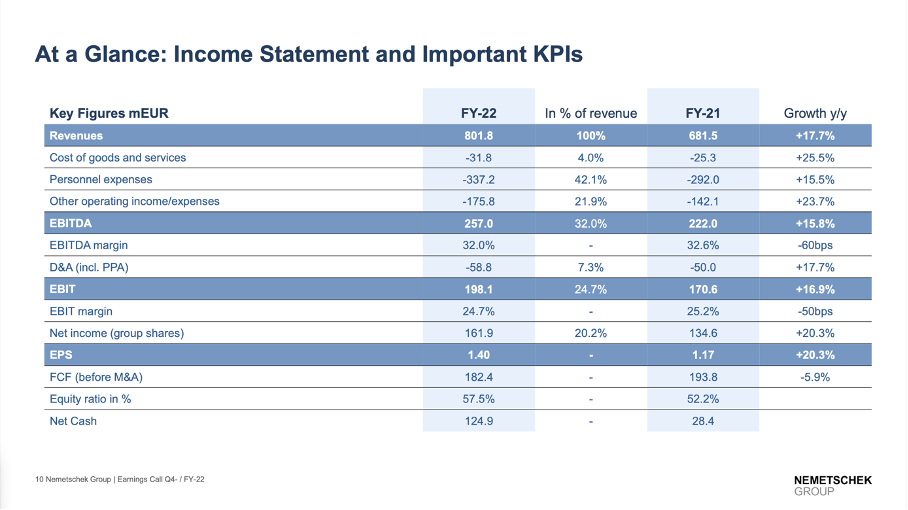

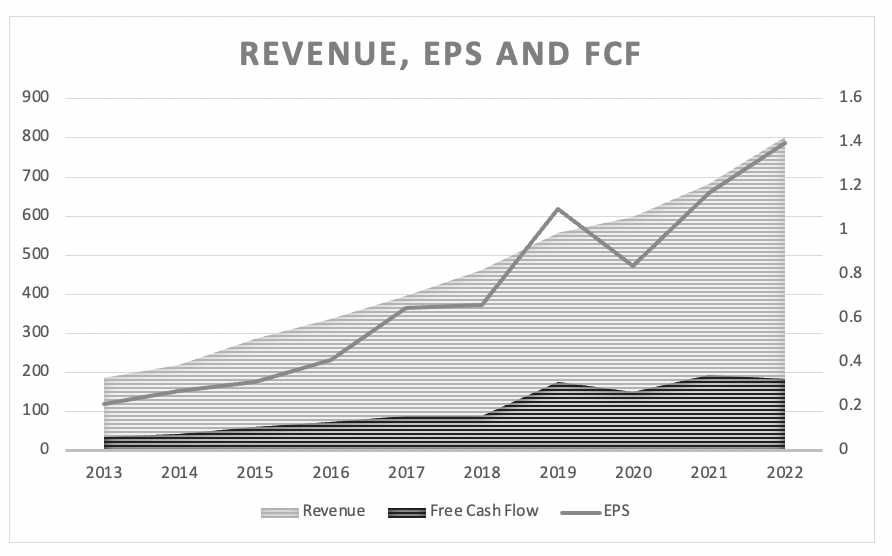

In fiscal 2022, Nemetschek generated €801.8 million in revenue and compared to €681.5 million in revenue in fiscal 2021, the top line grew 17.7% year-over-year. EBITDA increased 15.8% year-over-year from €222.0 million in 2021 to €257.0 million in 2022 while EBIT increased 15.2% YoY from €172.0 million to €198.1 million in 2022. Earnings per share increased even 20.3% year-over-year from €1.17 in the previous year to €1.40 in fiscal 2022. Only free cash flow declined slightly from €193.8 million to €182.4 million (and I am looking at the number before M&A investments).

{kind=link}

Nemetschek is reporting in four different segments:

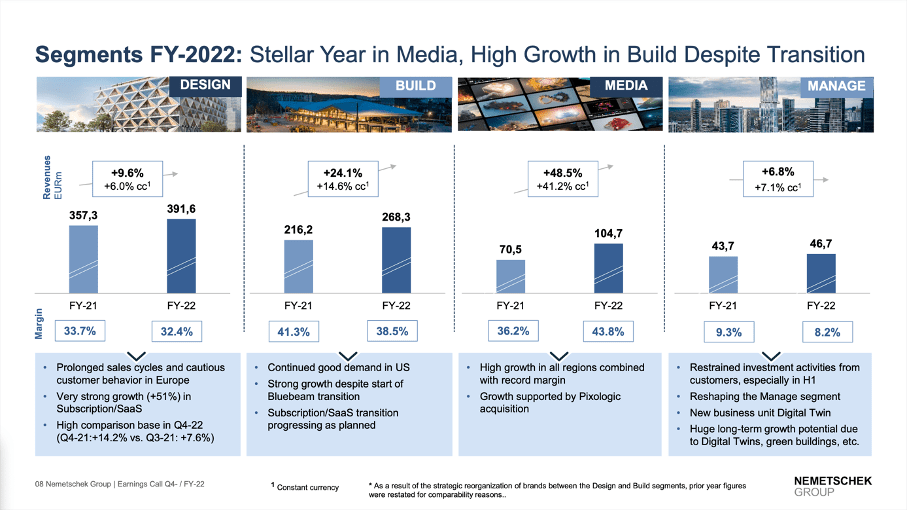

- Design : This segment targets a wide range of specialists within architecture, design and engineering disciplines and the key brands in this segment are Graphisoft, Allplan and Vectorworks. In fiscal 2022, this segment generated €391.6 million in revenue and reported an operating margin of 32.4%.

- Build : This segment offers integrated complete 5D BIM solutions (including everything from the bidding and award phase to invoicing, budgeting, scheduling, and cost calculation). Main customers for this segment are construction companies, developers and building suppliers. In fiscal 2022, this segment generated €268.3 million in revenue and reported an operating margin of 38.5%.

- Manage : This segment offers software solutions across all commercial processes in property management and bundles the field of facility management and professional property management. Among the four segments it is the smallest with only €46.7 million in revenue in fiscal 2022 and an operating margin of only 8.2%.

- Media : This segment targets customers from the media and entertainment industry (like film and television studios, advertising agencies, video game producers and graphic designers). Under the brand name Maxon, the company is providing professional solutions across all phases of a creative project. In fiscal 2022, this segment generated €104.7 million in revenue and reported an operating margin of 43.8%.

{kind=link}

Economic Moat

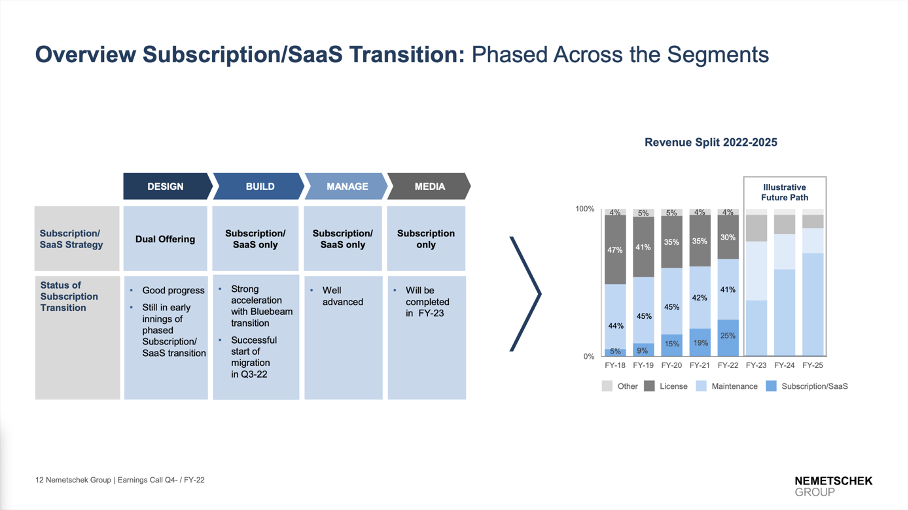

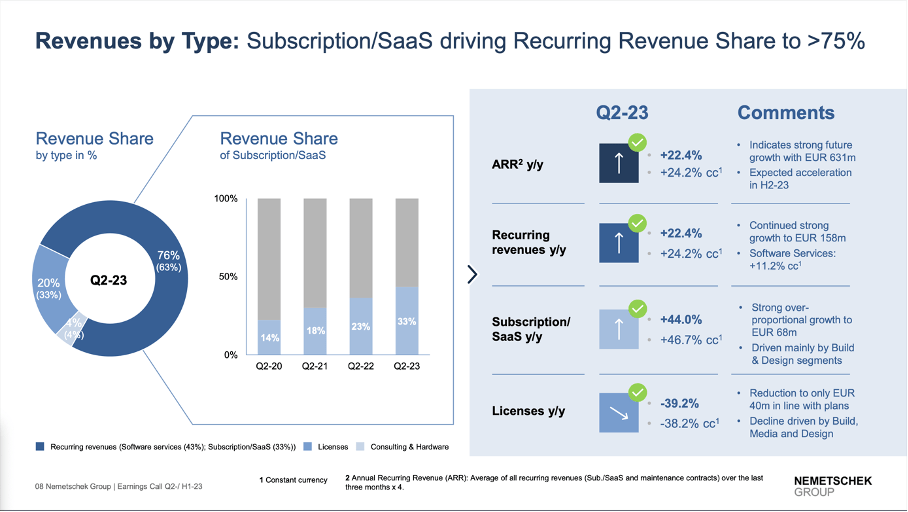

Right now, Nemetschek is generating 76% of its revenue from recurring revenue – this is including software services which are responsible for 43% of total revenue as well as subscriptions which are responsible for 33% of total revenue. The remaining revenue is stemming from licenses (20% of total revenue) as well as consulting and hardware (4% of total revenue).

{kind=link}

The long-term strategy of Nemetschek is to increase revenue generated from subscriptions or software services and therefore increase the recurring revenue for the business. And when looking at the last few years, the company could increase the percentage of total revenue that was recurring, which is increasing the switching costs for Nemetschek.

And when analyzing a business and trying to determine if a company (or stock) could be a good long-term investment, we must look for a competitive advantage or an economic moat around the business that can keep competitors at bay. In case of Nemetschek, the company seems to have a wide economic moat based on switching costs. Nemetschek is offering specialized software for a certain industry and the software the company is offering is often mission-critical for the customers. And as switching might lead to several days of not being fully operational, companies are trying to avoid such disturbances – as it would result in the loss of revenue.

Additionally, it often took several months or years of training to fully understand the software and being able to use the full potential of any software. By switching to the software of a competitor, all this knowledge would be gone and potentially hundreds of hours of new training might be necessary again. Combined with the risk of worse functionality of the new software, customers usually don’t switch just to save a few bucks – the risks are simply too high, and this is generating high switching costs for Nemetschek.

The company is also operating in a niche with a smaller addressable market, and this is keeping major competitors at bay. Big software companies won’t enter the market as it is not lucrative enough and with high upfront costs necessary to develop the software, Nemetschek also has a competitive advantage.

And of course, Nemetschek’s economic moat is also visible by looking at key metrics. For starters, when looking at the income statement in the last ten years, we see high levels of stability and consistency. Revenue increased every single year in the last ten years and while earnings per share and free cash flow fluctuated a little bit, I would also describe the bottom-line growth as rather stable.

Nemetschek: Revenue, EPS and FCF (Author's work)

{kind=link}

Since 2003, Nemetschek was profitable every single year and since 2009, the company also increased revenue every single year (during the Great Financial Crisis, revenue declined a bit).

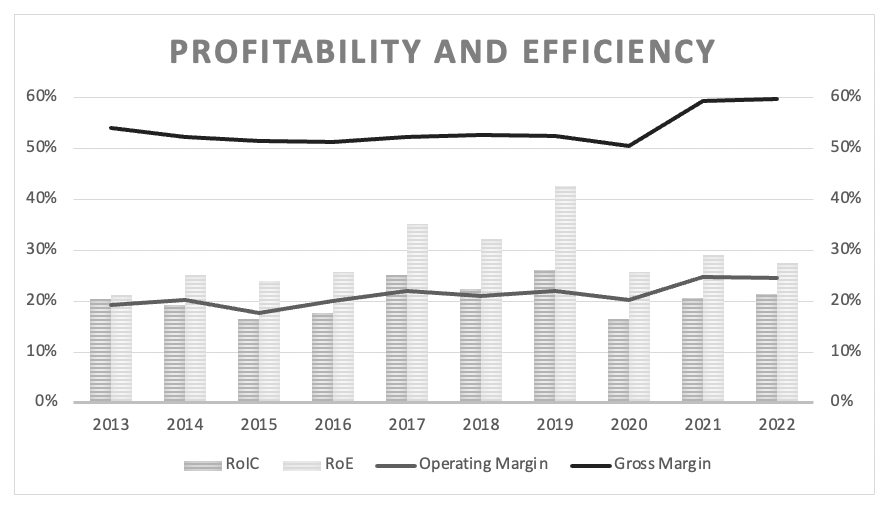

Nemetschek is also reporting stable gross and operating margins. Until 2020, gross margin was extremely stable but increased in the last two years and operating margin is also increasing over the last ten years.

Nemetschek: Margins and RoIC (Author's work)

{kind=link}

Aside from stable margins, Nemetschek is also reporting impressive return on invested capital numbers – not only was RoIC above 15% every single year during the last ten years, the average RoIC in the last ten years was 20.6%.

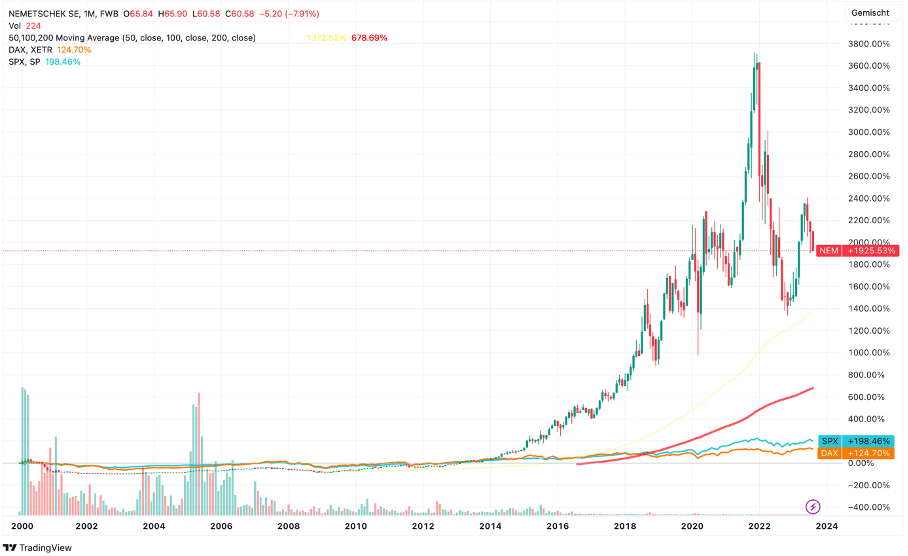

When looking at the stock performance since 2000, Nemetschek clearly outperformed the DAX-40 as well as the S&P 500. While Nemetschek increased 1,925% in value, the S&P 500 increased “only” 198% and the DAX-40 increased only 125% in the same timeframe.

{kind=link}

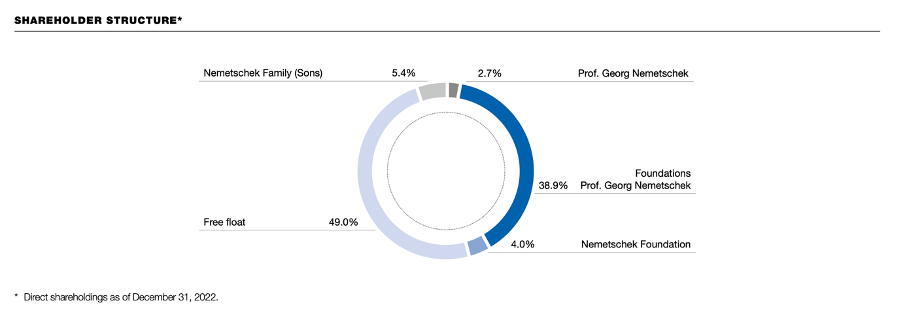

And when talking about an economic moat or competitive advantage, we also should take a look at the shareholder structure. Nemetschek is clearly a family-run business and as I have explained in detail in a past article , these types of companies are usually great businesses and great investments that outperform.

{kind=link}

In case of Nemetschek, 51% of shares are being held in some way by the founder Georg Nemetschek and his family. About 43% of shares are held by two different foundations and about 8% of shares are held by the founder and his family. And it is always a good sign when the founder can call the shots as he or she has more than 50% of voting rights.

Maybe that comparison is a little far-fetched, but Nemetschek SE seems to have some similarities to Constellation Software Inc. ( CNSWF ), which I covered recently. Both companies are operating in a similar market and are offering specialized software for a market niche. Both companies have many small clients and are providing mission-critical software solutions. Of course, Nemetschek does not have the same “investment approach” as Constellation Software does, but for both mergers and acquisitions play an important role.

Growth

A wide economic moat is certainly important for a business to be a great long-term investment, but we are also searching for companies that are able to grow with a high pace. When looking at the growth rates in the recent past, Nemetschek reported impressive numbers. In the last ten years, revenue grew with a CAGR of 16.43%, while operating income grew with a CAGR of 20.94%. And finally, earnings per share grew with a CAGR of 23.97% in the last ten years.

Management is not expecting similar growth rates for the future, but they are certainly optimistic and see several long-lasting growth drivers for the business. First, Nemetschek is expecting that the growing world population combined with an increasing urbanization will lead to a higher demand for housing. Second, the ongoing transformation towards a sustainable world will require extensive investments in infrastructure. Third, state regulations might make the use of BIM (building information modelling) software mandatory for state-financed construction projects and the use of software of the entire building lifecycle might also be required by the BIM regulations. Finally, the level of digitalization is rather low in the construction industry, and it needs to catch up with digitalization that is already the norm in other industries.

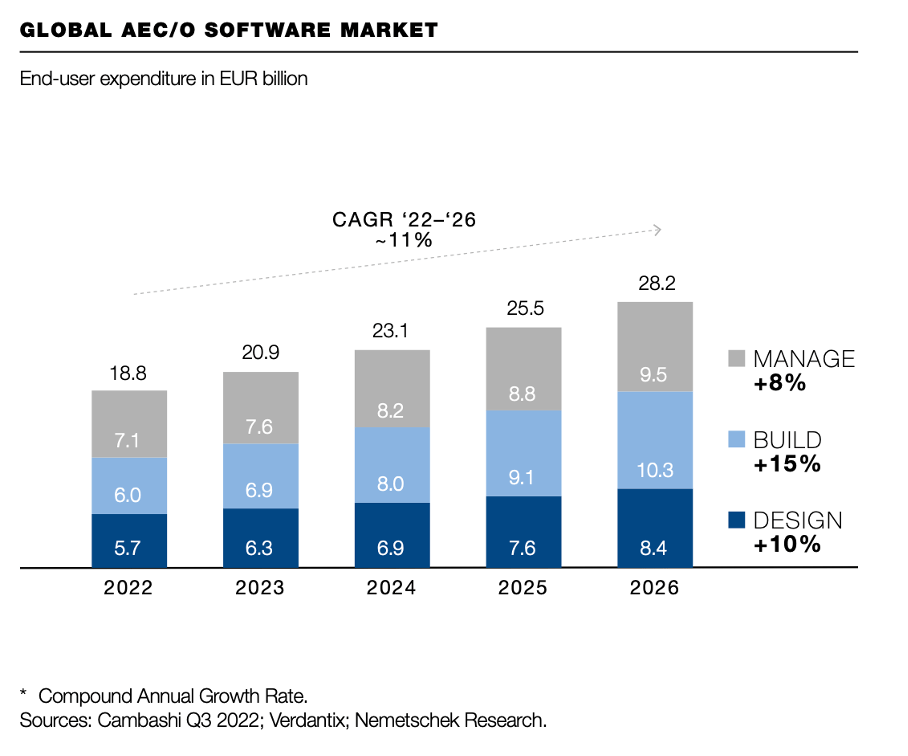

As a result, Nemetschek is expecting rather high growth rates for the next few years. The AEC/O software market is expected to grow with a CAGR of 11% in the next few years and especially the “Build” segment might grow with a high pace as the underlying market is expected to grow 15% annually.

{kind=link}

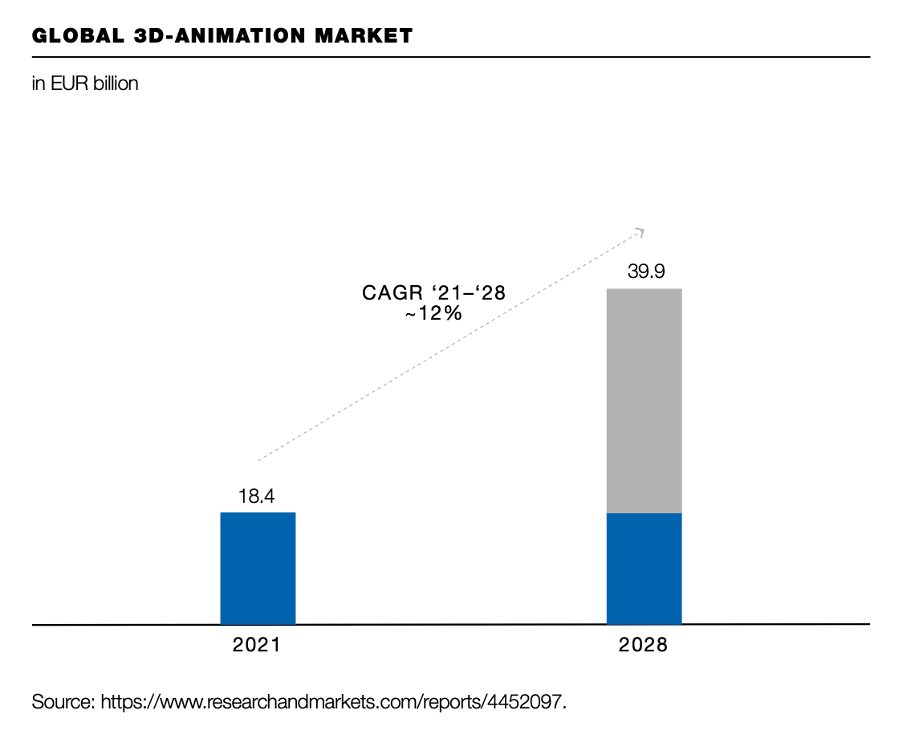

Additionally, the global 3D animation market is also expected to grow with a high pace: Between 2021 and 2028, Nemetschek is estimating a CAGR of 12% for its fourth segment.

{kind=link}

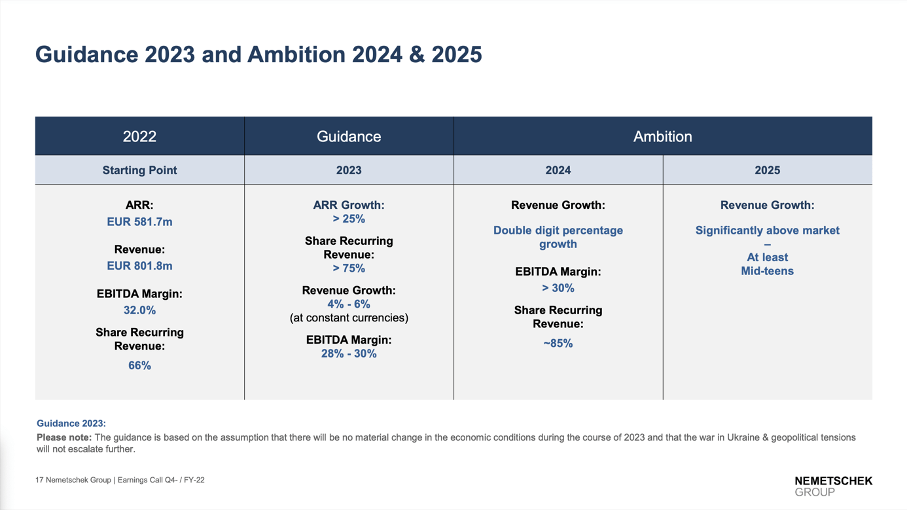

And for the next few years, the company is expecting revenue to grow in the double digits with bottom line growth being rather in the mid-to-high than in the low teens.

{kind=link}

Finally, switching to a subscription-based model (or software as a service) will also help and add to growth in the years to come.

{kind=link}

Struggling Construction Industry

But we should not be too optimistic and just assume Nemetschek to grow with a high pace forever. For example, we can look at the years 2000 till 2022 when Nemetschek had to report a loss three years in a row.

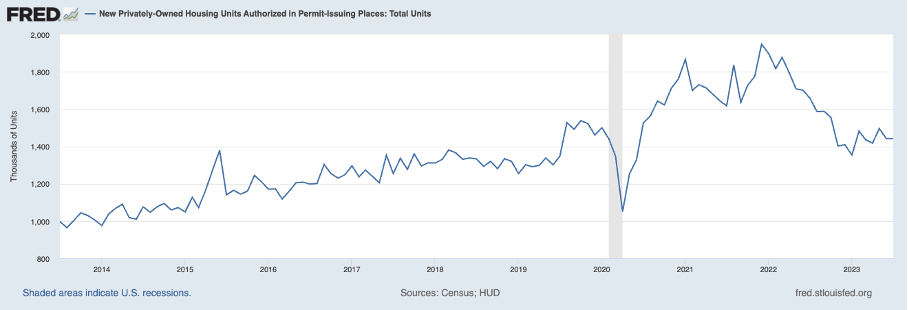

When looking at the numbers and metrics the construction industry is reporting right now, we certainly should be cautious. In Germany, the number of housing permits declined 27.2% in the first half of 2023 (compared to the same timeframe last year). And when looking at the monthly housing permits in the United States , the number of permits in July 2023 is about 26.0% below the previous peak.

{kind=link}

Although I don’t want to be too pessimistic, we should be a little cautious at this point. Nemetschek is expecting high growth rates for the next few years – however, there is the risk for lower growth rates. The housing market and construction industry had a strong run for a very long time – and Nemetschek profited from that trend. We should not be surprised if that trend will come to an end at some point.

Intrinsic Value Calculation

So far, we established that Nemetschek is a great business with a wide economic moat around it and the potential to grow with a high pace in the years to come. But as mentioned several times in the past, having a great business alone is not enough – we also need to purchase the business (or stock) for an acceptable price. At the time of writing, Nemetschek is trading for 43 times earnings per share and 38 times free cash flow. And while we can find more expensive stocks out there, Nemetschek is certainly not cheap, and we should be rather cautious if the stock is a good investment at this point.

To determine an intrinsic value for which the stock can be bought, we use a discount cash flow calculation. As always, we assume a 10% discount rate in our calculation and take the current number of outstanding shares of 115.5 million. As basis for our calculation, we can take the free cash flow before acquisitions from fiscal 2022 (which was €182.4 million) and I think this is a realistic assumption.

In order to be fairly valued, Nemetschek has to grow its free cash flow 12% annually for the next ten years, followed by 6% growth till perpetuity. Of course, for a wide economic moat company, 6% growth till perpetuity is realistic but we can ask if 12% growth for the next ten years is realistic. When looking at growth rates in the last 10 years, 12% growth seems like a realistic assumption, but we should be a little cautious.

In my opinion, we could assume 12% growth for the next ten years. However, we must take into account the decline of the construction segment that could last for several years and might have an impact on Nemetschek. Summing up, I would see Nemetschek fairly valued at this point, but not necessarily a “Buy”.

Conclusion

Nemetschek already declined about 60% from its previous all-time high and this is already a steep decline. And right now, the stock is still trading almost 50% below its previous all-time high. But I still would be a little cautious if Nemetschek is a good investment already and the stock will only remain on my watchlist for now.

For further details see:

Nemetschek: Hidden German Stock Market Gem