NEMTF - Nemetschek: Strong Secular Trend And Up/Cross-Selling Opportunities To Support LT Growth

2023-09-12 06:56:44 ET

Summary

- Nemetschek is a leading company driving digital transformation in the AEC/O industry, offering software solutions for construction projects.

- The company has shown consistent revenue and EBITDA growth, with positive financial performance and strong margins.

- The long-term growth potential is supported by the need for digitalization in the industry, and upcoming product launches like the Data digital twin will further drive growth.

Summary

Nemetschek (NEMTF) stands at the forefront of driving digital transformation within the AEC/O (Architecture, Engineering, Construction, and Operations) industry. Through its software solutions, the company encompasses the entire life cycle of construction and infrastructure projects, guiding its clients towards a future characterized by digitalization. All parties involved in a construction project can benefit from NEMTF solutions because they improve the quality of the construction process and streamline the digital workflow. I am recommending a buy rating for NEMTF as I foresee the secular trends to continue for a long time, and businesses in the industries would need to adopt digital tools eventually, or else they risk losing business to competitors.

Financials / Valuation

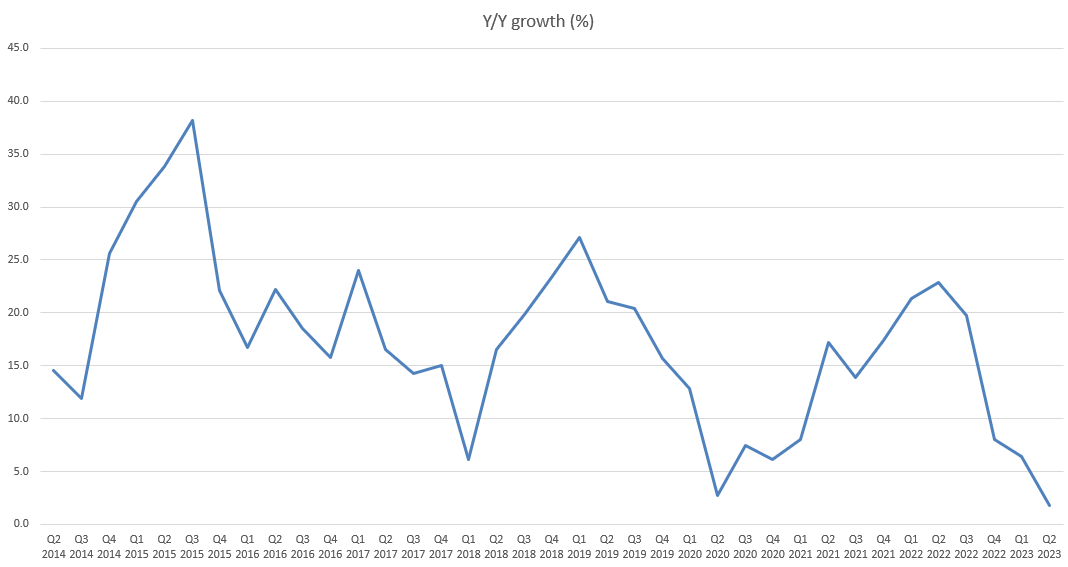

NEMTF has continuously printed positive growth since 2011, growing its revenue from $164 million to $801.8 million in FY22. Even better, EBITDA has grown at an even faster pace from $39.6 million to $256.9 million over the same period as margin expanded by 800bps from 24.15% to 32%. Recent 2Q23 results are consistent with the pattern. The company saw a 3.3% increase in total revenue in 2Q23. Due to one-time costs like personal spending and marketing expenditures, the EBITDA margin was only 27%. The company also restated its guidance for FY23, predicting a 4-to-6% increase in revenues and an EBITDA margin of 28%-30% (note that this suggests acceleration from TTM levels). The guidance staying consistent at the midpoint suggests the possibility of a growth acceleration in the latter half of 2023. This seems likely because NEMTF is expected to face more favorable comparisons in the second half of the year due to the anniversary of the Bluebeam transition at the end of the 3Q and easier design comparisons.

Based on author's own math

Based on my view of the business, NEMTF should be able to grow positively over the foreseeable future as the secular trend remains very strong. Growth will be slightly slower this year given the macro headwinds. As we move past the weak macro, I expect the secular trend to turn strongly each year as the need to be digitalized becomes more important. Growth should be further supported by upselling and cross-selling of solutions. Overall, I expect growth to accelerate back to mid-teens levels, similar to historical levels and management's FY25 target. EBITDA margin should follow a similar trajectory as the transition to subscriptions continues. NEMTF's earnings growth performance and long-term growth runway should support its current 26x forward EBITDA multiple. This multiple may seem high on an absolute level, but I note that this is in line with other solution providers in similar industries, such as Synopsys and Ansys.

Comments

Growth has slowed over the past few quarters, but I expect it to pick up again soon because NEMTF is positioned to take advantage of several structural tailwinds in the AEC/O industry. In particular, there is a long runway of growth ahead for the AEC/O industries that are heavily behind the digitalization trend. Construction projects have incurred substantial costs due to the slow adoption of digital tools. On average, 90% of construction projects are late or over budget, and 20% of all materials are wasted, as reported on the 3Q22 earnings call. I believe that the need for digitalization to improve efficiency is on the rise due to complex supply chains, labor shortages, and new sustainability regulatory requirements and targets, and that NEMTF is in a prime position to assist customers in addressing and managing these issues by providing solutions spanning the entire building lifecycle.

{kind=link}

I anticipate this secular trend will continue to be a growth driver, and NEMTF is working hard to develop innovative solutions to take advantage of it. The upcoming product launch that I see as a growth driver is the Data digital twin, which has its pilot version scheduled for release by the end of 2023, according to management. Information from multiple sources, including NEMTF software, will be merged into a single digital twin to shed light on a building's operation throughout its entire lifespan. This is important as it further eases the entire construction process by synergizing information all into one place. As it begins to generate substantial income in the coming years, I anticipate it will serve as a growth accelerator.

And the data will not only come from us, from our products, but it's an open cloud platform, which means that the data could come from any third parties including competition, and which is, Digital Twin will read all -- and have all the historical data of the building from the design, planning, and construction phase, but also all the live data coming from IoT and sensors, etc. Source: 2Q23 earnings3

Additionally, the sustained successful migration to subscription models should provide further backing for growth, even in the presence of macroeconomic uncertainties that are exerting pressure on the Design segment, particularly in continental Europe. The smart strategy adopted by NEMTF of providing varying subscription tiers with progressively more features and benefits to incentivize customers have contributed to this success. Keep in mind that NEMTF operates in a very sizable industry that relies heavily on established practices. Therefore, it is crucial to remove as many barriers to adoption as possible. Since the current workflow process (or solution) typically doesn't cost very much (for example, pen and paper), lowering the price is the most obvious obstacle to overcome first. This leads me to my next point, which is that the opportunity for upselling and cross-selling NEMTF will expand greatly as the product becomes ingrained in users' workflows and they come to appreciate its value. In my opinion, this up-and-cross-selling momentum will help the company achieve the double-digit growth management has set for 2024 and the mid-teens growth management has set for FY25.

Risk & Conclusion

The growth runway might be long for NEMTF, but the adoption pace could be a lot slower than I expected. The construction industry has been around for a very long time, and it has operated fairly well without the need for new digital solutions. Some businesses might delay adoption for as long as possible or never adopt digital solutions at all. Hence, the growth pace might be slower than expected. Overall, I believe NEMTF is well-positioned at the forefront of the AEC/O industry's digital transformation. Its comprehensive software solutions span the entire life cycle of construction and infrastructure projects, driving clients towards a digitalized future. The company's growth trajectory has been impressive, and it continues to demonstrate resilience even in the face of macroeconomic uncertainties, especially in continental Europe. I recommend a buy rating for NEMTF, with confidence in its ability to ride the strong secular trends in the industry. Although growth may experience some moderation in the near term due to macroeconomic headwinds, the long-term outlook remains robust. NEMTF's expansion is further bolstered by the potential for upselling and cross-selling its solutions, supported by its diverse subscription models. While there is a possibility of slower industry-wide adoption, the compelling need for digitalization in construction, coupled with NEMTF's innovative solutions like Data digital twin, positions it for continued growth.

For further details see:

Nemetschek: Strong Secular Trend And Up/Cross-Selling Opportunities To Support LT Growth