NEON - Neonode: Walkthrough Of Assumptions In Lawsuit

Summary

- Neonode recently won a pivotal decision in their current litigation.

- Even after the recent move up past $10, we see a base case for a 100% return, and in a most bullish case the possibility of 10x upside.

- Neonode presents a litigation based speculation play with large upside.

Felix Lindberg co-wrote this piece.

Introduction

We give Neonode ( NEON ) a strong buy rating due to what we believe is a favorable risk-to-reward profile with its current litigation. Neonode is the inventor of the first touch screen for a mobile device. The alleged infringement upon the company's patents for this issue has led them to open up litigation against Apple ( AAPL ), Samsung ( OTCPK:SSNLF ), and Google ( GOOG )( GOOGL ).

On January 11th , Neonode jumped over 50% after its recent patent victory against Google ( GOOG ), just the latest chapter in a long story. Additionally, last month the company won a victory against Samsung ( OTCPK:SSNLF ). These two victories are the start of what we believe will be a string of victories that continue to raise the share price of Neonode and eventually lead to a gain of multiples for investors of the company.

Considering the recent success in the exciting ongoing lawsuit, we want to be clear and transparent with all the assumptions we make for our Base Case and Bull Case. We believe the lawsuit, for which we believe the probability of a successful outcome to be ~30%, could turn Neonode into a potential 10+-bagger. Hence, all numbers in the equation leading to a possible payout for Neonode are vital to examine. The core of the company's current lawsuits are against Apple and Samsung, so calculations will start with those companies and then work to add others.

Financials

Neonode currently has a market cap of just over $130 million, at a share price of roughly $10.50. According to the latest SEC filing of the company, the company has $11.3 million in cash balanced by only $1.9 million in total liabilities. The company lost $800 thousand last quarter, leading to a loss of $0.06 per share.

The Lawsuit

To understand the scale of the lawsuits and why we care about a currently small company in Sweeden, an investor must understand that in the last ten years, Apple and Samsung alone sold 1.37 billion phones and tablets in the United States. The lawsuit depends on relevant volumes of specific units dependent on things such as the time horizon of the unit, the specific unit, and what market.

Time Scale

The lawsuit was initiated in June 2020 over Neonode's 879 and 993 patents. The lawsuit can only claim damages from units produced up to 6 years back from the initiation of the lawsuit making the start date of the time range June of 2014. Additionally, the patent expires in May of 2024, making the end of the time frame for the lawsuit making the lawsuit over a roughly 10-year period. To help manage the enormous cost of the case, Neonode entered into a profit-sharing model for the winnings of the lawsuit.

The official invention date as of today is December 10th, 2002, for both patents. This date counts as starting date, even if the patent's date for prior art should change. Generally, a patent lasts 20 years from its invention date. However, the patent time can be extended if the application takes a long time. The 879 patent received a 3-year extension, while the 993 patent did not receive an extension.

This would make patent 993 valid until December 10th, 2022, while patent 879 would be valid until December 10th, 2025. If we put equal weight on both patents, the average end date would be May 10th, 2024. Considering that we now believe patent 879 is the most relevant, one could argue that we should use the applicable dates. However, as we are still not entirely sure of this, we choose to take both patents and their dates into account. This makes the total time available for the lawsuit in our calculations 9.9 years, starting in June 2014 and ending in May 2024.

Products included

The products included in the lawsuit are phones and tablets made in, used in, sold to, offered for sale in, and imported to the USA. We believe this is the same as tablets and phones sold in the USA.

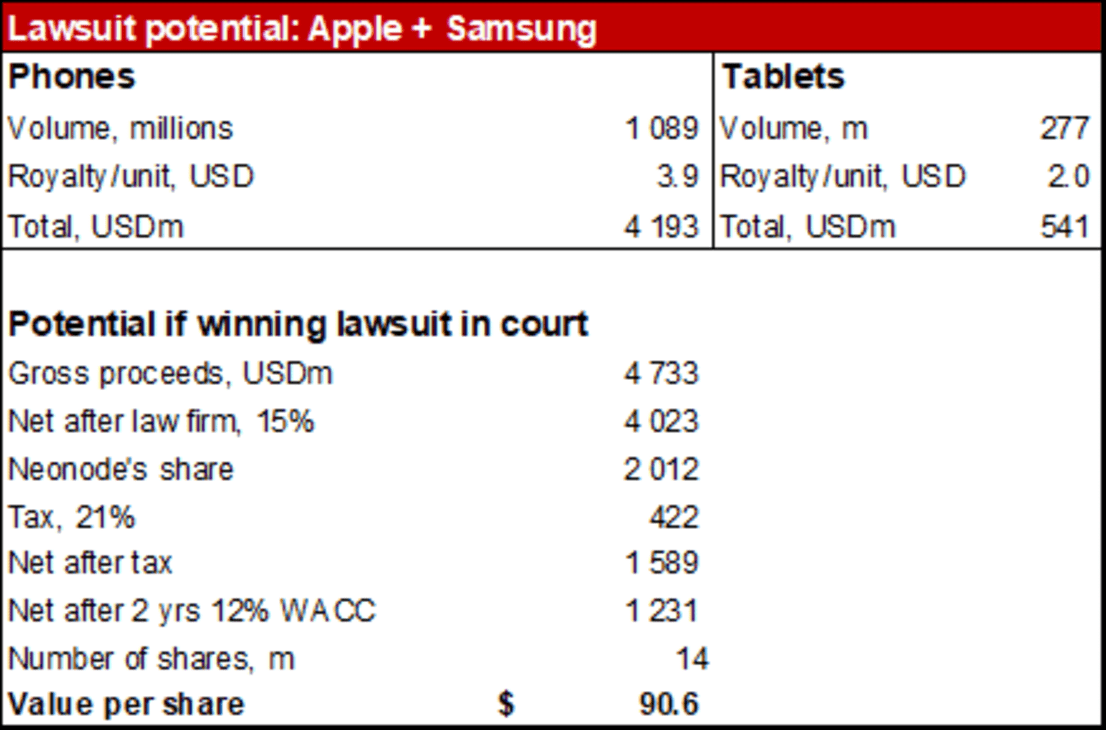

The products' interface includes devices with the Home Bar or Control Bar, iOS 13 or later, and iOS 8 or later having a third-party keyboard function, including the swipe function. The average yearly number of Samsung and Apple phones sold in the US between 2014 and 2021 is around 110 million, while the same for tablets is 28 million. Taking this for 9.9 years, it implies 1089m phones and 277m tablets.

Prices

The license agreement with Samsung shows that Samsung agreed to pay Neonode EUR 2 per unit, equal to $2.4 per unit at the time and $2.2 at today's exchange rate. From this, we use a royalty per unit estimation of $4 for phones and $1.5 for tablets, with the potential for multiplication with treble damage and inflation adjustments.

Price pressure on smartphone components decreases, but inflation could increase the price per unit. Since the first smartphones were commercialized, price pressure has been on the components. This argues for the EUR 2 in 2005 being worth less today. However, whereas this is true for unpatented and replaceable hardware components, it might not be the case for a patented solution that includes a combination of hardware and software.

Also, as the pricing of components is often set as a share of the selling price, and the costs of smartphones have risen since 2005, this should act as a cushion for holding up the value per unit.

The Neonode side, on the other hand, argues that the baseline should be to take the EUR 2.0 and then adjust for inflation. However, we think the development of the price of smartphone components is more accurate than general inflation as a whole.

Treble damages

By law, it is considered much worse for a company to infringe on a patent knowingly, i.e., if the infringer knew about the existing patent and yet infringed on it. This is called 'willful infringement' and results in so-called "treble damages" (triple damages).

Treble damages have the potential to triple the sum involved. I.e., if a company sues another for infringing on 1.4 bn units with a royalty fee per unit of $2, the lawsuit asks for $2.8 bn. Then, if the judge or jury rules that it was a willful infringement, the total claim increases to up to 3x the initial sum, thus up to $8.4 bn.

Evidence on treble damage for Samsung is strong, but not against Apple – 'treble-damage multiplicator' of 2. Since Samsung signed a license agreement for using Neonode's patent, Samsung knew about the patent. After Neonode AB (a Swedish subsidiary) went bankrupt in 2008, Samsung kept using Neonode's patented technology. Thus, we believe there is a good chance of some treble damages being included in the case.

Regarding Apple, we previously believed that the Neonode side would be able to produce documents proving Neonode's discussions with Apple. Such records would have strengthened the case against Apple and about claiming treble damages against Apple. However, we still think there is some chance that the treble damage could also apply to Apple.

Considering that Samsung's market share in the US is ~30% and ~50% for Apple, we apply this ratio to calculate our 'treble-damage multiplicator.' Only considering Samsung and Apple, Samsung constitutes 37.5% and Apple the remaining 62.5%. Using 3x for Samsung and 1x for Apple gives us a multiplicator of 1.75.

We estimate $3.9 for phones and $2.0 for tablets. Applying our 1.75x multiplicator on EUR 2.0, or $2.2, implies $3.9 per phone shipped.

As the damage fee per unit is measured and decided from the share of the selling price of the product, the damage fee for tablets is likely much smaller. We estimate a tablet's average selling price to be half that of a phone. Hence, we use $2.0 for the tablets.

The total potential of $94 per share for Neonode – or half in a settlement. For phones, the potential damage fee becomes 1,089m units at $3.9, leading to a total of $4,193m. For tablets, the potential damage fee becomes 277m units at $2.0, leading to a total of $541m.

The total potential damage fee could thus be $4.7 bn for Apple and Samsung combined. However, we estimate that 15% of this would go to the law firm. Of the remaining 85%, half would go to Aequitas, leaving 42.5% for Neonode. Thus, the potential income before tax for Neonode is $2.0bn. Applying a 21% tax on this, we get a total potential for Neonode of $1.6bn, equal to $117 per share. While this will likely directly add to the share price value, it will also likely add at a multiple because the increased cash gives the company an opportunity for more growth which will be priced in.

While a settlement would imply a relatively quick payout, we assume a payout in two years, i.e., early 2025. Applying our discount rate of 12%, we arrived at a value of roughly $91 per share today.

{kind=link}

If the lawsuit were to be settled with both Samsung and Apple, we estimate 50% of this sum would be applicable, corresponding to a value of $58.5 per share.

Adding Others

Alphabet and others add $19 per share to the total potential. Apple and Samsung constitute ~80% of the market, meaning the remaining companies, including Alphabet, make up ~20%. Should the Neonode side win the lawsuit or even settle, we think it will likely go after the remaining players on the market, too. This would naturally take a couple of years more. We arrive at the following value by adding 25% of the total potential (20% divided by 80%) but delaying this payout for two more years.

{kind=link}

Small upward adjustment for Base Case, but a significant lift of Bull Case

Our changes mainly affect our Bull Case, which we lift from $93.5 to $114. Our Base Case is lifted to $22.0 per share. It should, however, be noted that there still exists an upside to our Bull Case concerning the following things:

- Our scope only includes the USA – should other regions be included, the scope will increase. However, this would take time.

- We have used a 'treble-damage multiplicator of 1.75x. Should full treble damage imply for all, another 70% would be added.

- We have not included any inflation in the base rate of the royalty rate. Should the jury decide that this is applicable, additional potential is added.

{kind=link}

Risks and Conclusion

Like Netlist ( OTCQB:NLST ), when investing in small companies and companies dependent on the legal system, nothing is guaranteed, and there will be lots of volatility. Additionally, until a payout happens, all price movement is based on speculation and may not always be logical. This can both be frustrating but also beneficial. The more often Mr. Market quotes a price too high or low to the intrinsic value of a stock, the better the money-making opportunity.

The opportunities presented to investors in research-intensive small companies are where an investor can be at an advantage over wall street. Almost all funds are too large to move in and out of positions in a company like Neonode; therefore, most do not play in this game, making it prime real estate for retail investors.

In conclusion, Neonode presents a high-risk, high-reward opportunity. We have only scratched the surface of the information available. This is a stock in which a retail investor can gain an information edge through thorough research and, therefore, could be a worthwhile investment.

For further details see:

Neonode: Walkthrough Of Assumptions In Lawsuit