NTOIF - Neste: Great Performance Looking Forward To 2023

2023-03-30 05:29:41 ET

Summary

- I've been covering Neste for over a year at this point. This company is Finnish, and active in the energy sector, with excellent fundamentals and a good long-term upside.

- In this article, I intend to review the 4Q22 results as well as the FY22 results, and look into what we might see in 2023.

- The short of it is - I believe we'll see improvements in the coming year and more - and in this article, I will show you why.

Dear readers,

In this article, I'll be updating for 4Q22/FY22 for Neste ( NTOIF ). Neste is, as of now, a relatively small investment for my portfolio - but a qualitative one. I've been reviewing the company for some time, and I mean to keep investing here.

Neste is a very qualitative sort of business. As renewable energy has turned into a long-term growth story, worldwide businesses have been moving to make it a priority across the board. The demand growth we've seen has been around for about a decade at this point, and renewables/biofuels are the fastest-growing sources of electricity and power today.

Neste isn't in electricity - but it's in renewable products, including things like oil products to a global market.

Let's look at 4Q22 and see how the company did.

Neste update for 4Q22/FY22

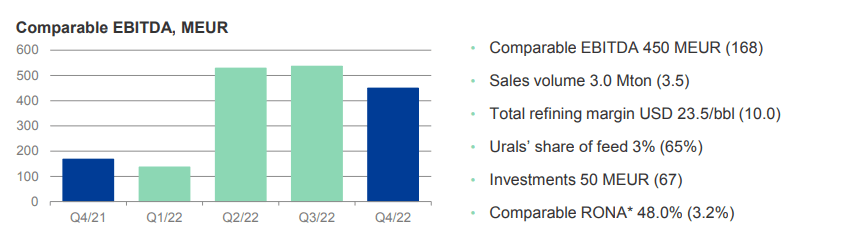

The company's full-year results came in positive, with EBITDA at over €3.5B, strong performance in all business segments - especially in oil products - with refining markets really shining. The company's SG&A also performed well during the quarter and the year, and the company's high-level strategy has been working out well.

This has resulted in Neste being able to pay out a full €1.52 per share, including an extraordinary and discretionary extraordinary dividend of €0.5/share, almost 35% of the dividend.

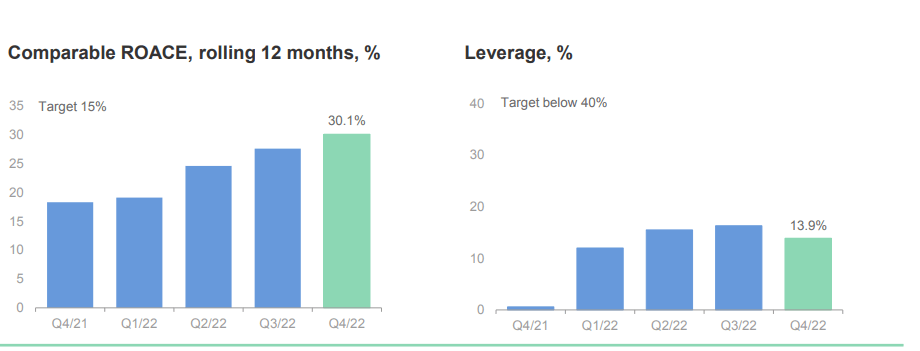

What you want to look at for a company like Neste is the returns in relation to how indebted the company is. Insofar as this goes, results and trends are absolutely solid. A word and some context on the renewable side of things - Neste is a Finnish company that focuses on the refining and marketing of premium, low-emission traffic fuel. In a sense, the company is the world's leading producer of renewable diesel. Once, the company was actually part of Finnish energy giant Fortum (FOJCF) - today, the renewable argument is based on renewable refining , with all of the company's products essentially being in the premium space. The company owns the world's largest renewable diesel plants in Singapore as well as Rotterdam with a combined capacity of 1600kt/y, which use NEXBTL technology for a new generation biofuel. The company also has a 45% stake in a 400kt/y base oil plant in the nation of Bahrain.

The legacy operations that the company once had and operated in traditional crude have been sold off, among other companies to Chevron (CVX). At its heart, the use of biofuels is a solution to the current ongoing energy shift - and most northern European nations have hopped on board this train for the past few years. This is also why Neste has become more important exactly for the past few years, and why this renewable "spin" has become so crucial not only for Scandinavia since 2012 and forward.

{kind=link}

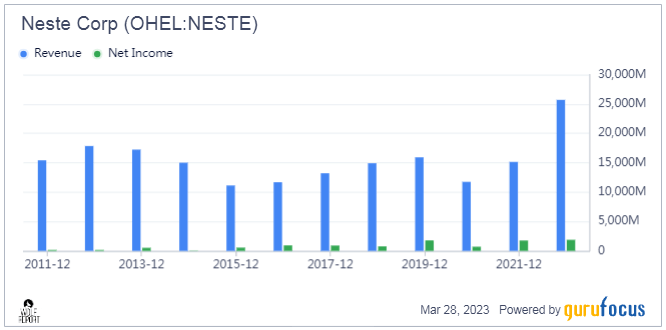

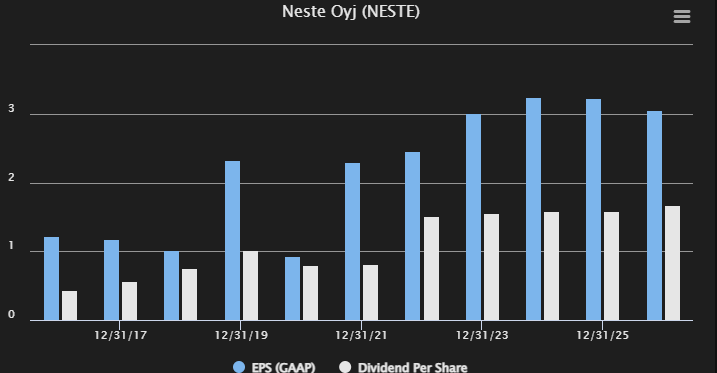

Just how good the company has been doing is easy to look at on a comparable basis. The full-year comparable EPS for Neste is almost double from 2022 to 2021 - and the share of profit we're seeing from renewable refining and renewable overall sources mean that you can really call Neste a renewables company - albeit not one with wind and solar, as some might think of.

Neste Revenue/Earnings (GuruFocus)

{kind=link}

The company's comparable leverage might be down, but debt is up on a YoY basis, with almost a billion euros increase in debt due to CapEx and new initiatives. A good FX has also been a strong part of the company's results, but most of the YoY improvements came in sales margins - prices for energy, which have been going up significantly.

Unlike other energy companies, some of Neste's feedstock correlation comes from things like Soybean, Used cooking oil, animal fats, and palm oil. The pricing for those feedstocks has exploded between 2019 and 2022, only to start declining now in 2023. Sales performance is supporting the margin here, and this is despite a utilization rate of 75%, down from 95%. Oil product sales performance, despite being down from 2Q and 3Q2, is still superb.

{kind=link}

However, it pays to remember that most of these positives are coming from significantly higher product margins, in themselves being due to high product margins and pricing volatility.

The company's strategy at this time is focusing on expansion - Singapore, especially. Also, the Rotterdam expansion project is going on track, and going to be able to start at the end of 2023. The company also has its Martinez Renewables JV that's expected to reach full capacity by the end of this quarter right at this time, with a retreatment capacity of 2.1 Million tons added to the company's overall capacity.

The company outlook for the coming few quarters includes a normalization of sales volumes - that means going down. The margins and the various feedstock markets are expected to remain volatile - especially with what we've been seeing from the global market in the first three months here, with fixed costs increasing on a YoY basis due to overall cost increases.

Still, demand is solid here. The oil product market is expected to remain volatile, but solid, some due to Ukraine, with similar levels to 4Q22. The company expects to continue to target M&As and JVs where necessary. The company has, as I said, actually increased its overall debt and leverage from a normalized EBITDA standpoint. Maturities are fairly close in time going forward.

{kind=link}

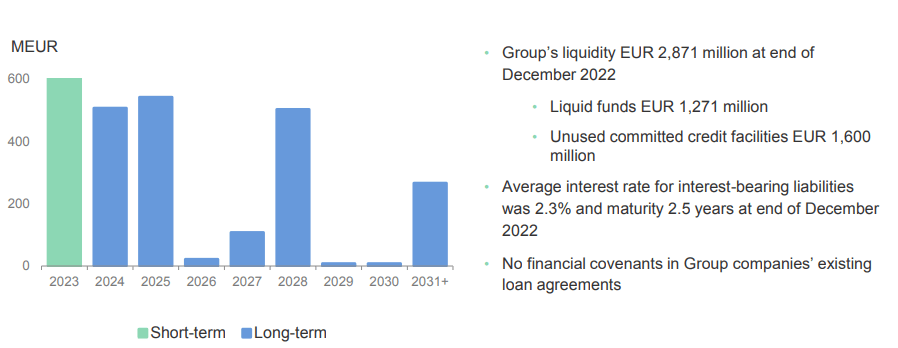

The company has liquidity of about €2.9B at the year-end of 2022, around €1.3B of which is liquid funds. The company's interest rate is low, and all of the company's debt comes without covenants.

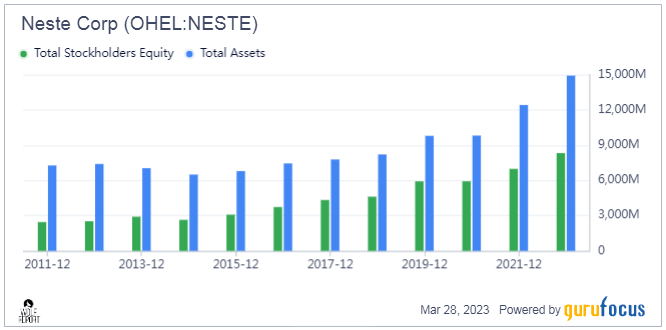

The positives extend way beyond debt and earnings. Company returns/ROIC have been improving for years. Before 2015, the company was often at negative ROIC/WACC, not it is consistently scoring positive variances between these two, implying that the company is making good money of its investments. Stockholders equity and assets are growing, and while we need to keep an eye on the company's debt, the overall picture that we see here is a positive one.

Neste Shareholder Equity (GuruFocus)

{kind=link}

The picture I want you to have about Neste is a slowly growing, profitable business with exposure to renewables, oil products, and a significant amount of marketing and sales services for the segments. The revenue split between the former two is very close, with 40% oil and 37.5% renewables, remaining in marketing and sales. The company's feedstock, business model, and operations mean that the company's COGS are high - over 86%, resulting in a GM of 13.3% and a net of 7.3%. This isn't the worst in the business, but it's also not among the best - with plenty of refiners and energy companies at higher margins than Neste.

Where the company shines is its ROIC, which is significantly better than average, and growing profitability as renewables are becoming more and more popular. Revenue is growing faster than we've seen before, and despite good results, we're still seeing some valuation upside (more on that later).

My own, and analyst forecasts have Neste growing not only its revenues but reach new heights in earnings, with the dividend also growing at impressive rates.

{kind=link}

Anything to worry about?

Not anything out of the ordinary, as I see it. We have an outage in Rotterdam which will impact sales volume, and the company's hedging given market volatility is getting more complex. We're expecting some buildup in overall inventories as the company prepares for the outage, but this of course binds capital, resulting in higher net WC. We're looking at what sort of profit and revenue levels, based on pricing, we can expect now that we're moving into a more normalized environment. Neste, prior to these years, has never really been any sort of massive yielder or business that a lot of people pay attention to.

Other risks or downside that we should highlight includes the company's reliance on specific tax credits and other things specific to the renewables industry. There is also the risk of a drawdown in ICE car sales, and what this does to renewable diesel sales - though some of that is likely going to commercial industries, where shifting will be slower. The company also still has plenty of work to do in securing supply contracts with major airlines and service companies, as well as securing the feedstock contracts for capacities beyond 3-5Mt per year.

So, a few operational-specific risks, and some high-level ones - which really require you to consider the valuation carefully.

Now, that's different. We'll have to keep a close eye on the company's quarterly results to see where these forecasts change - because that'll dictate how much we should pay for the business.

Let's look at the company valuation, and why I'm buying more.

Neste Valuation - it's very attractive.

Neste is impressively followed for a Finnish renewable/oil company. 21 S&P Global analysts follow the business, and they average a PT range of €39 to €65, ending up around €52.5. That's over €5 above the current share price. Out of 21, 11 analysts are at a positive rating of either "BUY" or an equivalent, positive rating.

We can't or shouldn't really compare Neste to most peers. Its peer group includes Eni ( E ), Shell ( SHEL ), BP ( BP ), and similar oil majors - but Neste is, after all, different than your standard oil major. The significant comparative premium in terms of revenue multiples, EBITDA multiples, and P/E multiples, where Neste trades 3x higher than the aforementioned ones is really a product of the company's renewable focus - almost all of this company is really renewables or bio in one way or another. Either you validate or accept this, or you don't.

DCF doesn't really work with Neste. There is too much volatility baked into the company's forecasts. A simple EPS DCF of 20 years, with a 1-2% growth rate and no more than that still puts the company at an FV of €78/share - that's more than I'd be willing to pay at any one time.

Forecasts from FactSet and other sources call for the company to manage more or less the same sort of EBITDA and earnings for the next 2-3 years as we've seen this year.

So, where should a company trade that's expected to move in this manner in terms of earnings and sales?

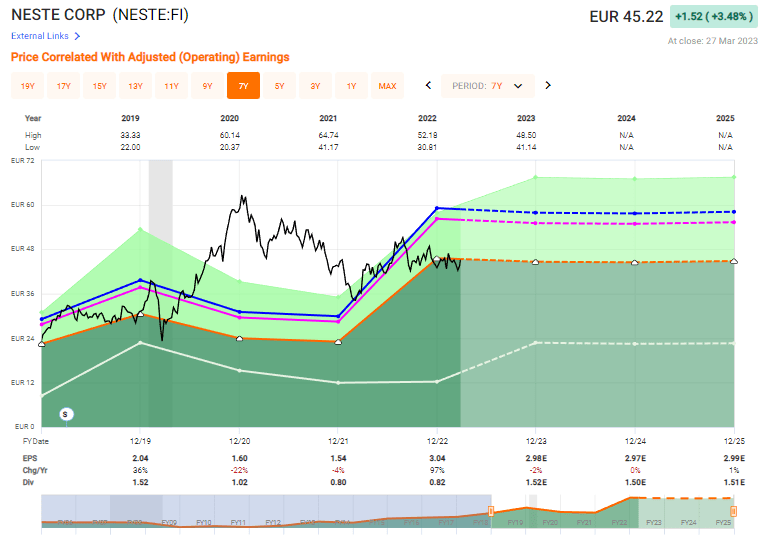

F.A.S.T graphs Neste Upside (F.A.S.T graphs)

{kind=link}

If you believe that this company should trade at 15x, then your returns in this case would be close to zero a few percent, that's all. You have to estimate or accept the premium that's applicable to renewables businesses - unless you do this, the upside isn't that compelling. With that, you have double-digit upside above 10.4% per year until 2025E, and that's on the base case in terms of income.

Since my last article when I doubled down on my position, I've seen little expansion or RoR on my position. Neste hasn't yet "popped", for lack of a better term. I do believe that the company will eventually pop though.

If you accept the non-commoditized nature of the business, Neste is undervalued on every single basis. This following a 1-year 20%+ drop in valuation and share price, and that hasn't changed since my last article. The reason for this decline is the strategic change for Neste for almost a decade.

Remember, the company was a major oil producer that went into and started focusing on renewable diesel. Initially, this was a large-scale "science project" for the company, but the market appreciation for this recycled product has been massive.

Converting Neste's output to oil barrel equivalent, the net margin (EBIT/output) in renewables was c. $80/bbl in 2019, against a mere $5/bbl for the oil products division.

And the spread is likely to increase going forward.

I continue to be positive about Neste. my previous targets were on the conservative side given how good the company's FY22 results came in, so I'm slightly bumping it to €50/share here, which was my previous "optimistic" target for the company. I'm making it my base case here, and this results in the following thesis on the company.

Thesis

My thesis for Neste is now as follows:

- Neste is perhaps one of the most interesting oil/energy companies in Europe. They've found their niche, and they've pivoted at what I view as exactly the right time to serve a market that's going to need their products for the next few decades at the very least.

- Neste has strong financials and very strong potential. Even if the yield today isn't that impressive, future returns could easily go into high double or low triple digits.

- Neste stock is a "BUY" with a price target of €50 here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I won't call it cheap, but I'll definitely call it buyable here.

For further details see:

Neste: Great Performance, Looking Forward To 2023