NTOIF - Neste: Opportunity Is Knocking At The Door

2023-05-25 14:15:56 ET

Summary

- I've been covering Neste for some time and been positive for a while as well, but never really "dug deep" into the company - at least not until now.

- Since my last article, Neste has seen a non-trivial double-digit share price drop. Remember that the company has a high energy correlation.

- The fundamentals in the sector remain attractive despite what seems like a massive decline for the company. I'm positive on Neste.

- I remain a "BUY" and here is Why.

Dear readers/subscribers,

If you recall my first articles on Neste (NTOIF), you'll know that I am, and why I am, positive about this particular stock. Neste is a world-leading company in certain fields of renewable energy. Investing in this stock, as with some companies that I write about demands that you have a long-term perspective. That isn't just a cop-out to prepare you for losses, as some investors seem to do when talking about companies that have seen declines.

Many of Neste's real projects won't pay off until, and we won't see results from some of the company's ambitions for several years. So this is an investment you'll want to focus on to hold for 3-5 years, at least.

On the valuation side, based on estimates, this company can look like a bit of a value trap - but I do not believe it is. Let me show you why.

Neste - Not a value trap, but an absolutely stellar potential

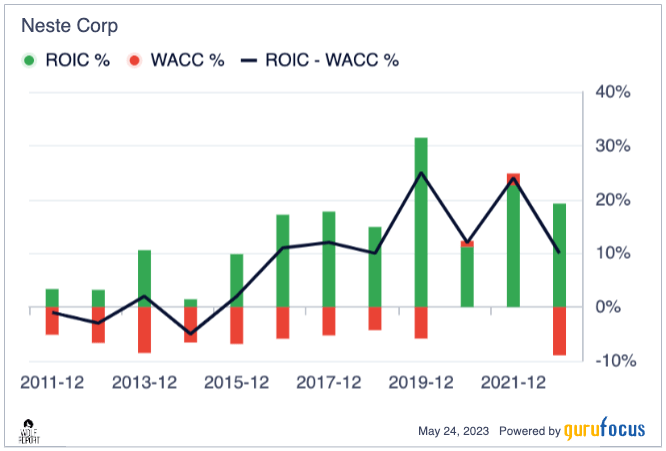

So, first things first. One of the reasons I am so positive one Neste is that the company is an extremely capable capital allocator with a proven track record of turning mud into gold, so to speak. What I mean by this is a proven, 10-year record of sector-beating profitability despite a rocky macro, and extremely good profitability at the very least since 2015.

{kind=link}

Unlike many other companies, the % of shareholder equity relative to the company's assets has actually increased over the past 10 years, meaning the company is very effectively rewarding and delivering good results from a shareholder perspective. Net Income has been a bit so-so. The company has very high COGS, which is the primary challenge for this particular business.

{kind=link}

They make up for this with a comparatively very lean OpEx and other costs and still maintain a 5%+ net income margin. Many of these things, if you've read my previous articles on the company, won't come as a surprise to you.

If you don't know Neste, a very quick recap for your newcomers.

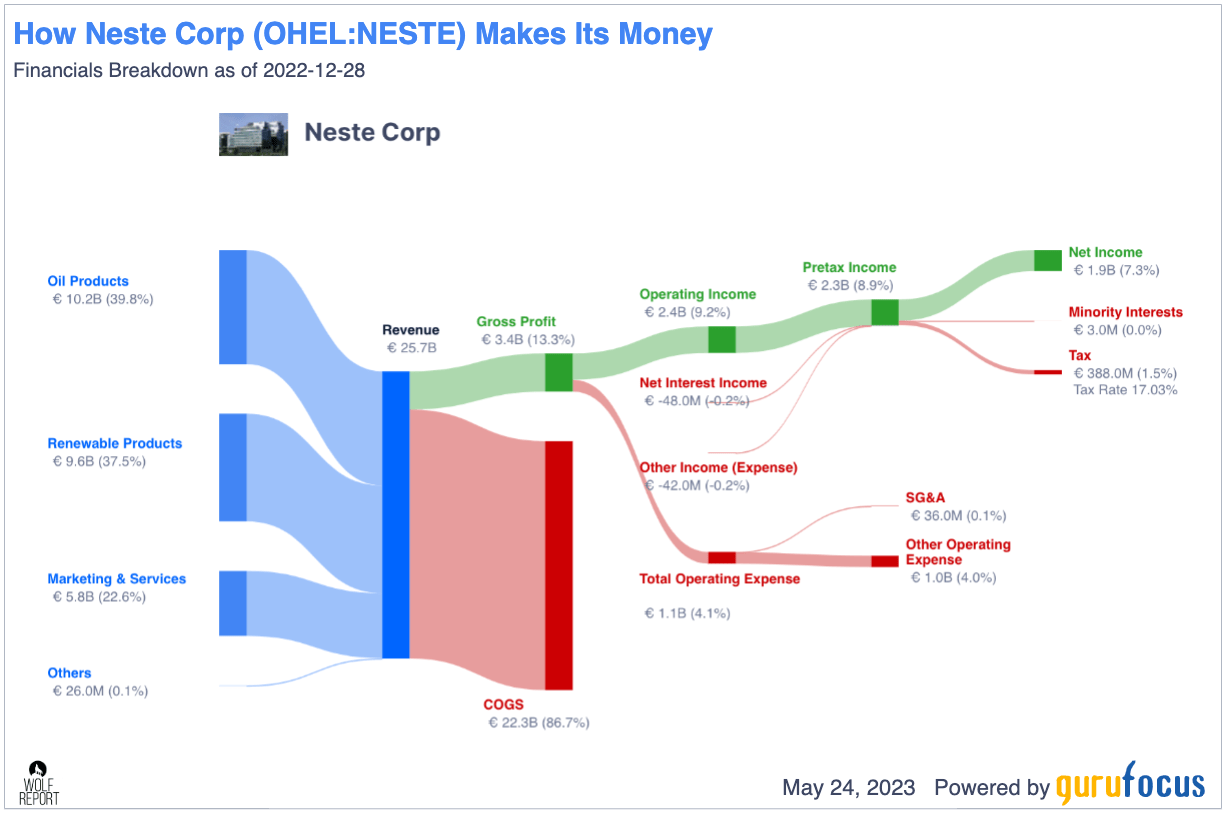

Neste is a Finnish company that focuses on the refining and marketing of premium, low-emission fuel. In a sense, the company is the world's leading producer of renewable diesel. Once, the company was actually part of Finnish energy giant Fortum (FOJCF) - but the company changed, and today it's a leader in all things renewable refining, taking recycled products and turning them into ESG-friendly fuel. What was legacy Neste has been sold off to other more traditional energy-space businesses, such as Chevron (CVX).

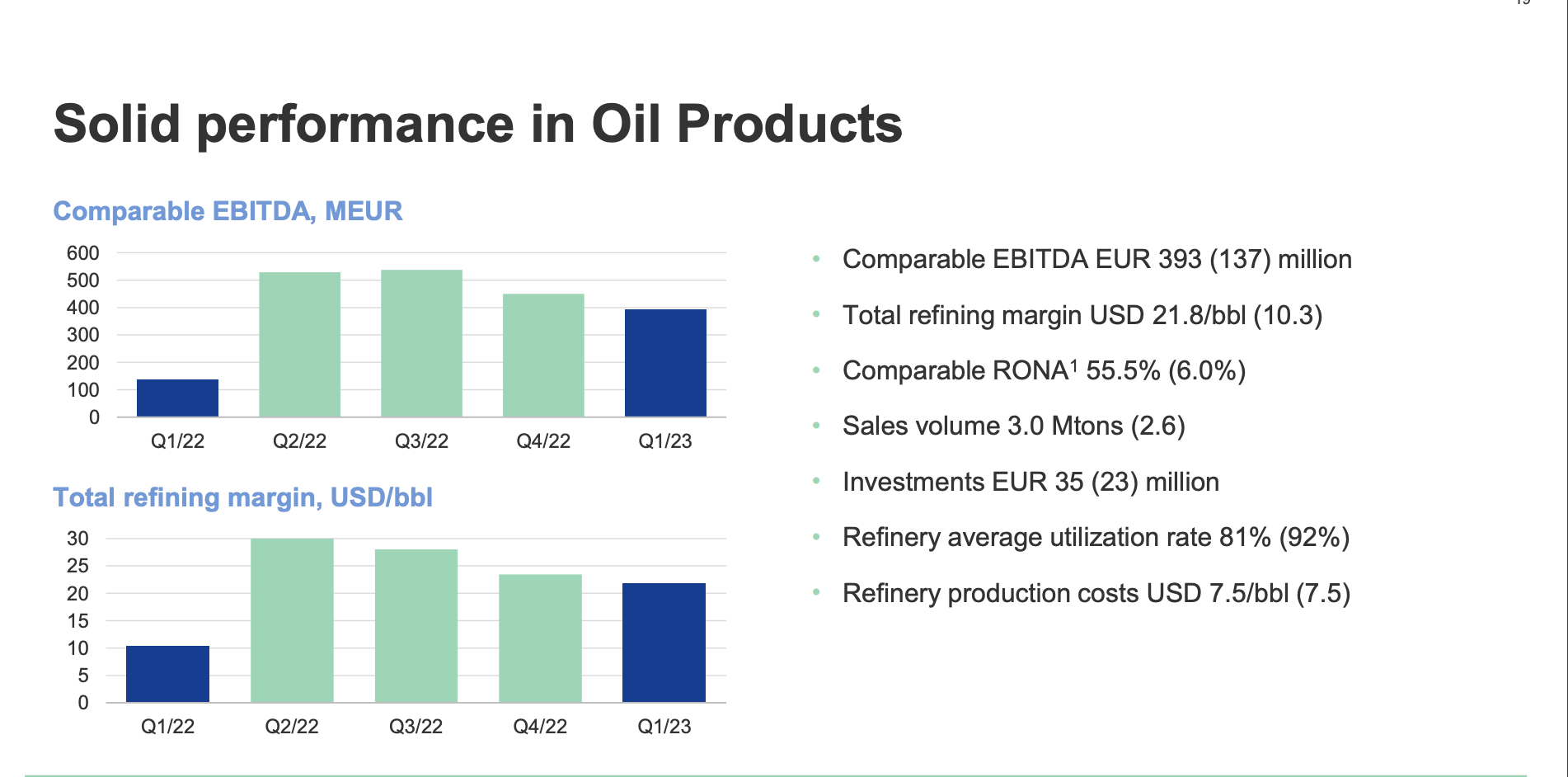

We have 1Q23 results, and as I see it, those results are very strong. The company delivered comparable group EBITDA of over €825M. More importantly, solid record-high margins on comparable sales on a per tonne basis, and continued good margins in the oil products segment (see the description in the graph above for segments).

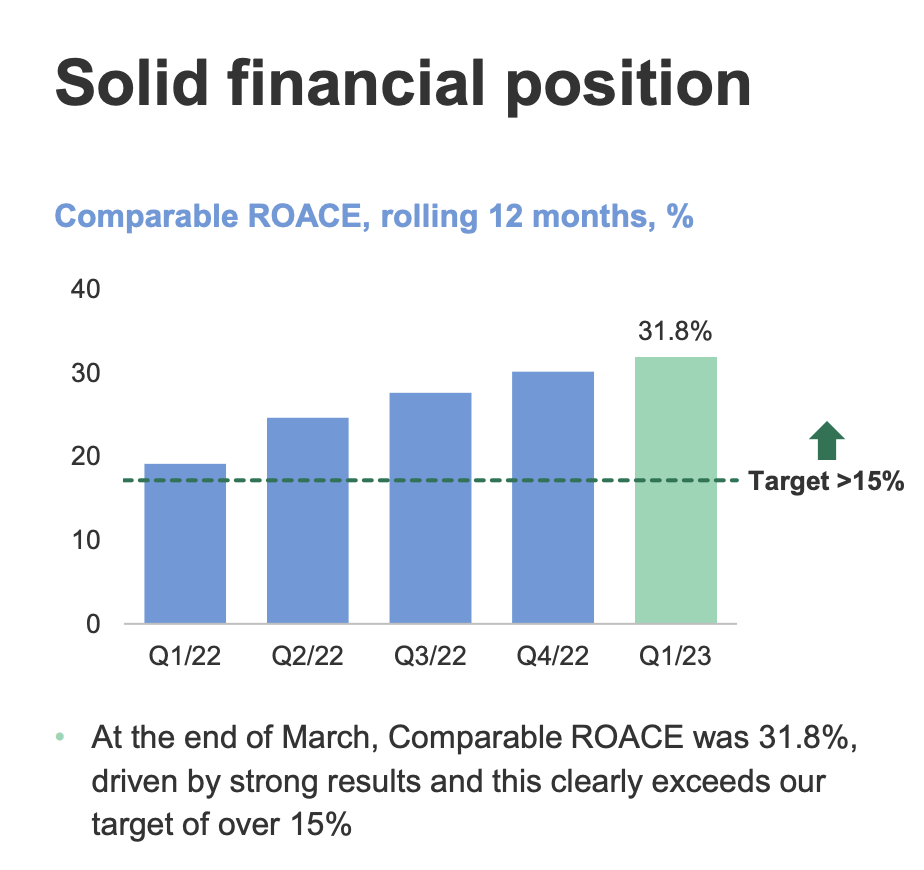

The company targets a ROACE, or Return on average capital employed, of over 15%. Would you like to know where that is today?

{kind=link}

What I am telling you clearly is that the company is substantially and continually improving its operations and taking advantage of macro to see some absolutely stellar margins. At the same time, the company's leverage, which is targeted to be below 40%, is now at 18.7%, which is less than half of the target.

As always, Neste remains a play on a number of commodities, these being waste and residue prices, which have been declining (the company's feedstock), and diesel, gasoline, and natgas prices, the output or comps. While Natgas prices have been declining, the decline seen in residue has not been mirrored by pricing in Diesel and Gasoline, which goes some ways to explain what is going on here.

This is what leads to a comparable EBITDA growth of 44% YoY, driven by both sales volume and margins in Oil products, Renewables (despite lower volume), resulting in some very impressive trends.

The company's main "headwinds" are related to higher fixed costs on a YoY basis, but as anyone who works in finance and accounting will tell you, that is what happens when a company is building up its organization on a global scale to prepare for some solid future growth.

The company recently issued two new green bonds, which went to enhance the company's liquidity and maturity profile, with 6 and 10-year maturity respectively, for a total of €1B. The company has no financial covenants in any of its existing loan agreements, which is another significant advantage.

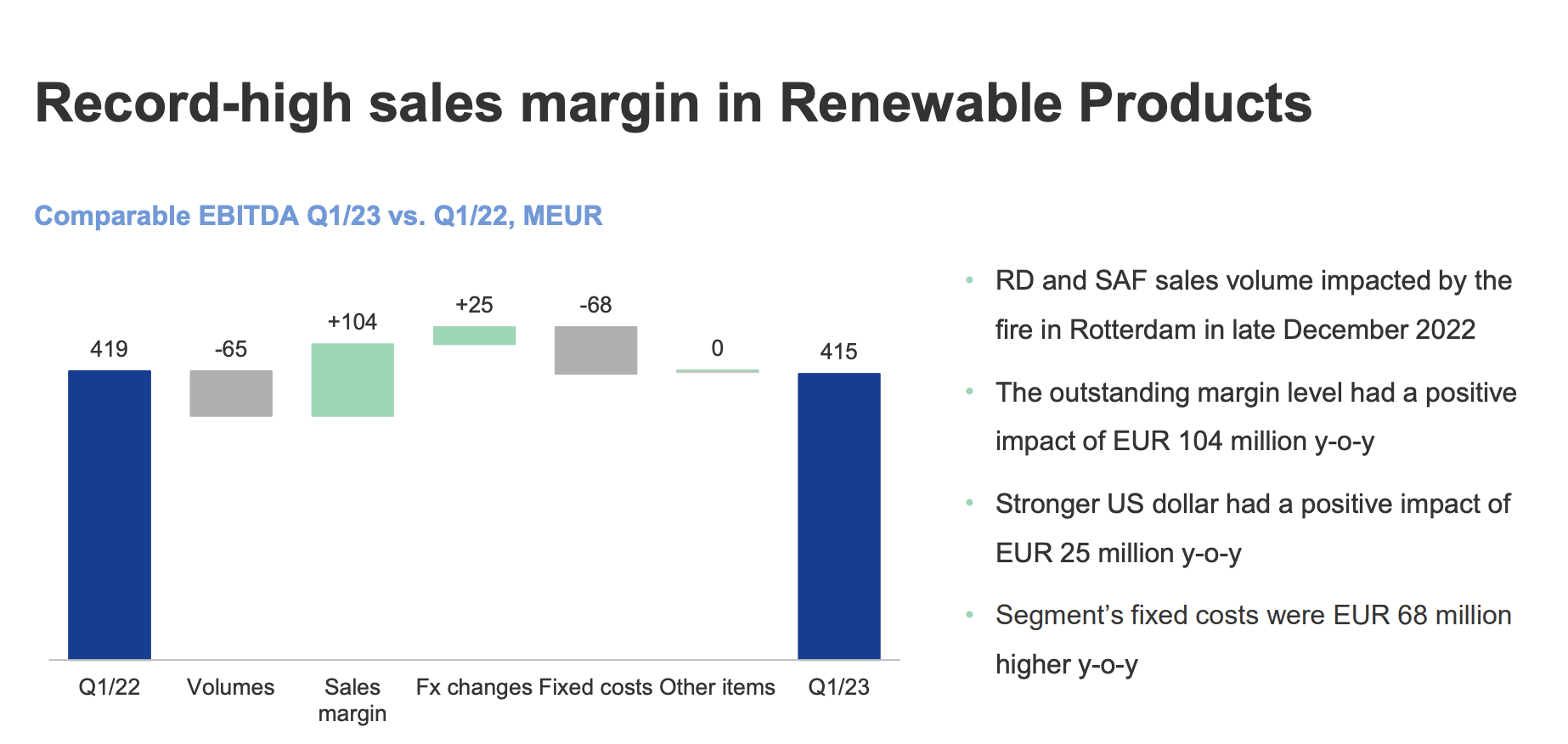

Renewable products as a segment have seen continued strong sales, with good margins. It's also seeing a significant utilization rate, despite dropping from its over 100%+ utilization rate YoY. The margin for renewables is what we should be focusing on this quarter because that was really quite excellent.

{kind=link}

With input prices declining in the first quarter, following the initial steep decline in pricing trends for vegetable oil, the company is seeing some advantages. Key drivers also include low carbon fuel standard credit, which continues to be a significant driver. Oil products also saw a significant recovery, and seem in no danger of falling back to the poor 1Q22 levels.

{kind=link}

The company is in a volatile segment, no doubt about that. Product margins and price differentials on a vs-brent basis are significant, since January of 2022, we've seen absolutely massive volatility in these segments. The latest trends include weakening diesel demand but an increase in demand for heavy fuel oil.

The volatility can be exemplified using a relatively recent piece of news due to a recent biofuel pull-back from the Swedish government. In order to contain inflation, Sweden has moved to ease its emissions for the 2024-2026 period which means that substantially lower amounts of biofuels - 40-60% to 6% - will be used in the mix. Because this market is a relatively major contributor to renewable diesel, it warrants a lower forecast for the company.

The segment will remain volatile. What we should be focusing on is the company's long-term growth strategy, and that if and when diesel is used going forward, we're likely to see increased adoption of renewable diesel in the mix not just in Sweden, but globally. This makes this less serious than the piece of news suggests, at least in the longer term. Singapore was slated to and has started up in terms of its expansion in mid-April. The company's Martinez JV also started up, with a production nameplate capacity of 2.1 M will be met by the end of this fiscal.

The company is also, as you might have read, expanding its Rotterdam facilities, and the availability and treatment capacity of Waste and residue feedstock continue. To remind you, Neste turns waste products into fuel. Whenever you can take waste products and turn them into something people want, you have a business idea.

Neste has followed this particular one for a long time, and it's going well.

Let's look at the valuation of the company.

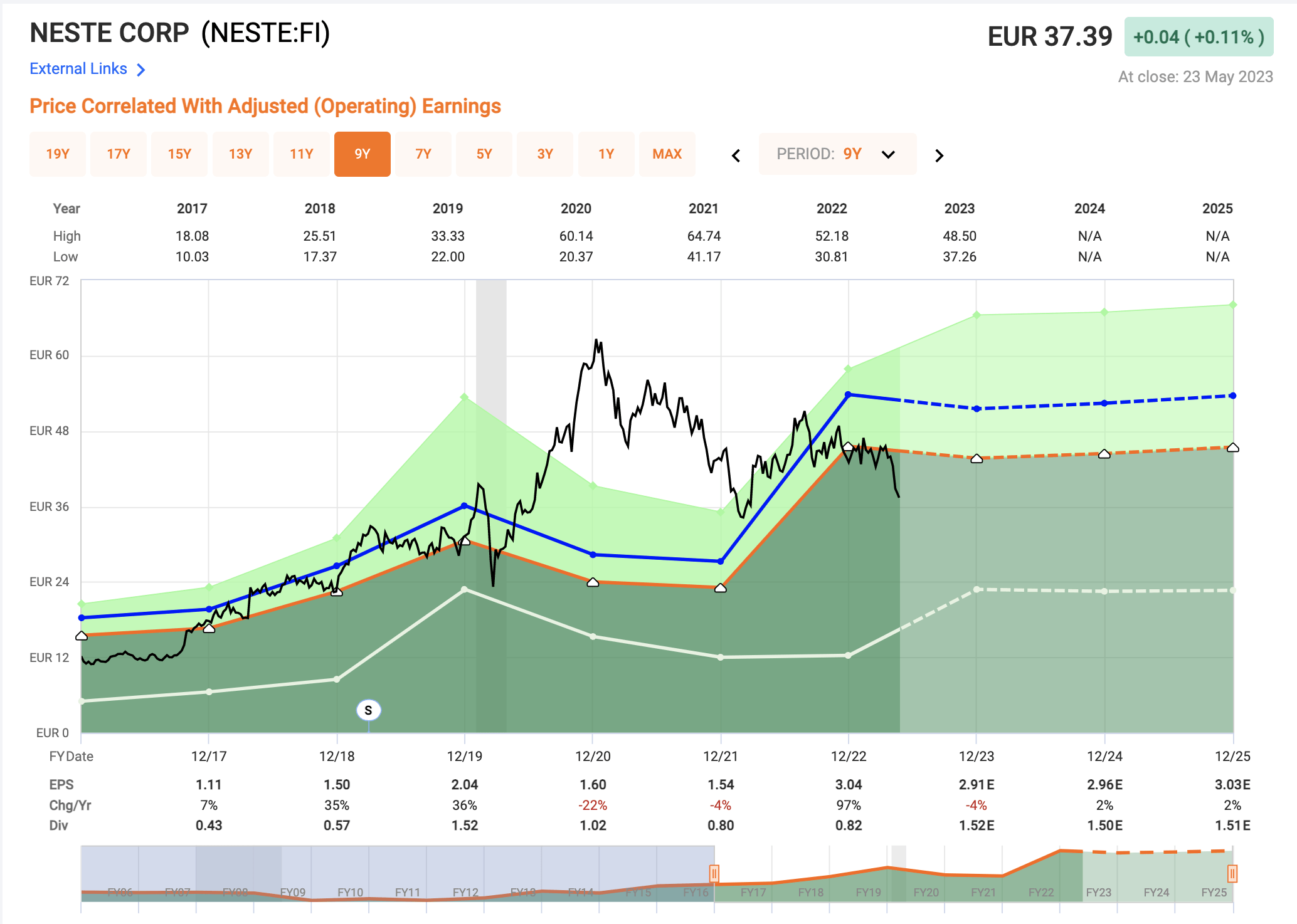

Neste valuation - It's superb when considering where the company may go.

Neste valuation (F.A.S.T Graphs)

{kind=link}

Looking at this picture, it's easy to understand why some analysts have a hard time valuing Neste. It's a company that ballooned to a massive level in COVID-19 due to its renewable focus, then normalized, but now is facing some years of uncertain growth.

What I want to point out here is that I don't believe the company will see massive earnings declines from here on out. And if we do not see massive EPS declines, then the previous share price levels from a few years back really aren't valid any longer.

Also, what I want to once again emphasize is the sheer returns this company manage, and the positive trends that are visible on a high level. We have things like an expanding operating margin, and good P/B and P/S ratio in terms of valuation, solid financial strength based on fundamentals. The fact that assets are growing faster than revenues does not faze me - that's the way of the world with a growth company in a growth stage. The company's current projects also cause some of the asset quality numbers, gross margin index numbers, and sales growth to look a bit "odd", causing some red flags in something like the M-score for Neste.

Again, this does not worry me for the company at this time, because looking historically, we can see such indicators bouncing up and down in a short timeframe, and the company is in exactly this sort of current trend that could cause this.

DCF, as I've said before, doesn't really work with Neste, so I won't waste much time with it. There is too much volatility baked into the company's forecasts. A simple EPS DCF of 20 years, with a 1-2% growth rate and no more than that still puts the company at an FV of €78/share - this remains more than I'd be willing to pay for the company. Forecasts from FactSet and other sources call for the company to manage more or less the same sort of EBITDA and earnings for the next 2-3 years as we've seen this year, and this calls for a different set of valuation estimates.

Current targets are remarkably close to my own. 21 analysts follow the company with a range of €30 on the low side and €65 on the high side, with an average of €51. This implies a 36.2% upside here, and one I consider quite valid at a NAV/Share of 0.64x based on today's share price.

13 out of those 21 analysts have the company at a "BUY" based on this estimate, and I consider this very likely to result in outperformance compared to the market.

I'm slightly adjusting my PT based on the recent biofuel mandate from Sweden, which should lower profit and sales by around 15-25%, though I expect commercial flexibility and increased sales elsewhere will offset some of these drawdowns. My impact for the time being is €3/share, which leaves me at €47/share in terms of PT. It's a bump in the road, but nothing that changes the overall thesis if you're investing for the long term.

Based on around a 15-16x P/E, which I view as valid for the business, the potential is for a 15-17% annualized RoR, which when you consider where the company might go based on its segment, is a very attractive rate of return.

For that reason, I'm not shifting my target here, but reiterating it and my rating for Neste at this time.

Thesis

My thesis for Neste is now as follows:

- Neste is perhaps one of the most interesting oil/energy companies in Europe. They've found their niche, and they've pivoted at what I view as exactly the right time to serve a market that's going to need their products for the next few decades at the very least.

- Neste has strong financials and very strong potential. Even if the yield today isn't that impressive, future returns could easily go into high double or low triple digits.

- Neste stock is a "BUY" with a price target of €47 here, and I'm sticking to this price as of May of 2023, with the most recent drop in the company's valuation - even with the most recent biofuel mandate.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company now fulfills all of my criteria for investing in a business.

For further details see:

Neste: Opportunity Is Knocking At The Door