NTOIY - Neste: Remember Finnish Oil And Its Upside Reiterate Buy

Summary

- Neste is a company that has outperformed the broader market by at least 14% since I first wrote about the company nearly a year ago.

- You may still not know much about Neste - the company remains underfollowed and mostly, overall, undercover here in SA as well.

- I continue to believe in the fundamental upside of the company due to a mix of circumstances and good business.

- Here are my targets for 2023 for this year.

Dear readers/followers,

Finnish companies have typically been important components of my success in investing over time. Companies like Neste ( NTOIY ) have delivered returns to my portfolio because through a mix of luck and actual good stock picking, I've been able to pick up it and other finish businesses at attractive prices fairly frequently. Now, looking at the overall performance since my first investment in Neste, I'm up around 4%, which given that the market is down almost 15% in the same timeframe is a pretty good performance - same with the hard data for my article in the meantime.

The time has come to give you my 2023 stance for Neste. To read my previous analysis, read here and here.

Updating for 2023 on Neste

The energy and oil sector is a tricky one - and my exposure remains below par. I failed to capitalize on the overall negative sentiment on the oil sector back when giants were trading at cents on the dollar - and I've introduced processes into my investment strategy that will guarantee that I don't miss out on such a sector-wide negative sentiment again (as one might argue, is going on with IT/tech at this time).

Neste though is in a somewhat different place here. Its fundamentals are still great. Its production accounts for nearly 20% of all the production capacity here in Scandinavia, and its product mix and ESG focus have lent itself extremely well to the market. You might remember my initial article on the company, and Neste has continued to outperform here despite all the volatility going on.

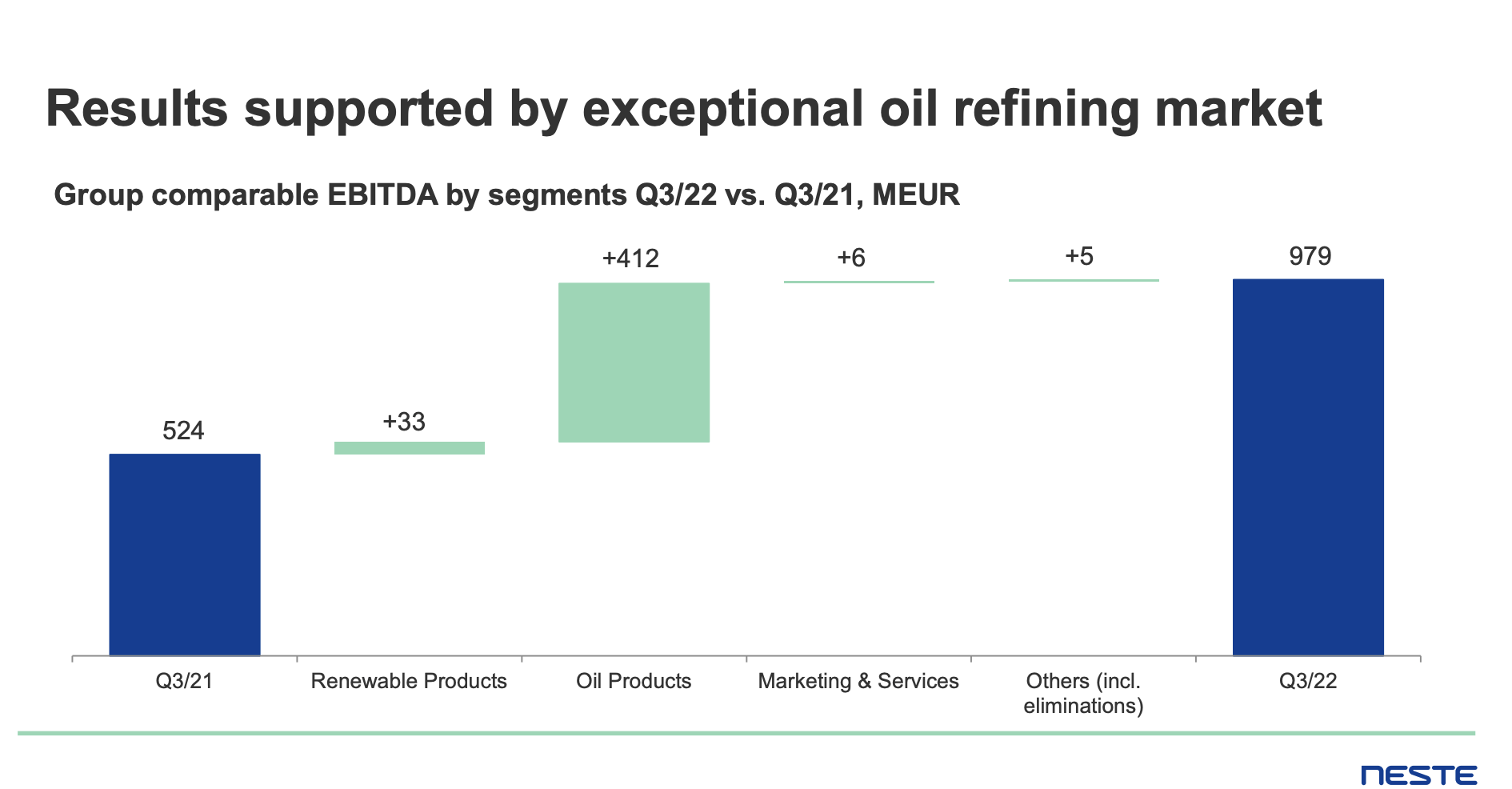

Neste generated just south of €1B in group EBITDA for 3Q22, and renewable products performed well despite overall challenges in terms of margins, increased hedging costs (naturally), and SCM issues that came in the form of logistical delays.

Return numbers, namely ROACE on a TTM basis is up to 27.6%, and this is up from barely 20% in late 2021, and leverage for the company remains well below 20%, with a target of sub-40%.

The combination of very attractive sales, underlying financials, and attractive overall operations with comparatively little Russia exposure ensures that Neste remains a very good operator in today's market. Given that Neste also operates refineries, the company's results are further lent strength from superb refining margins at this time. Usually, its renewables are leading the show, but in 3Q22 alone, the company generated over €400M of EBITDA from its oil product segment, which is responsible for the near-doubling of EBITDA on a YoY basis.

{kind=link}

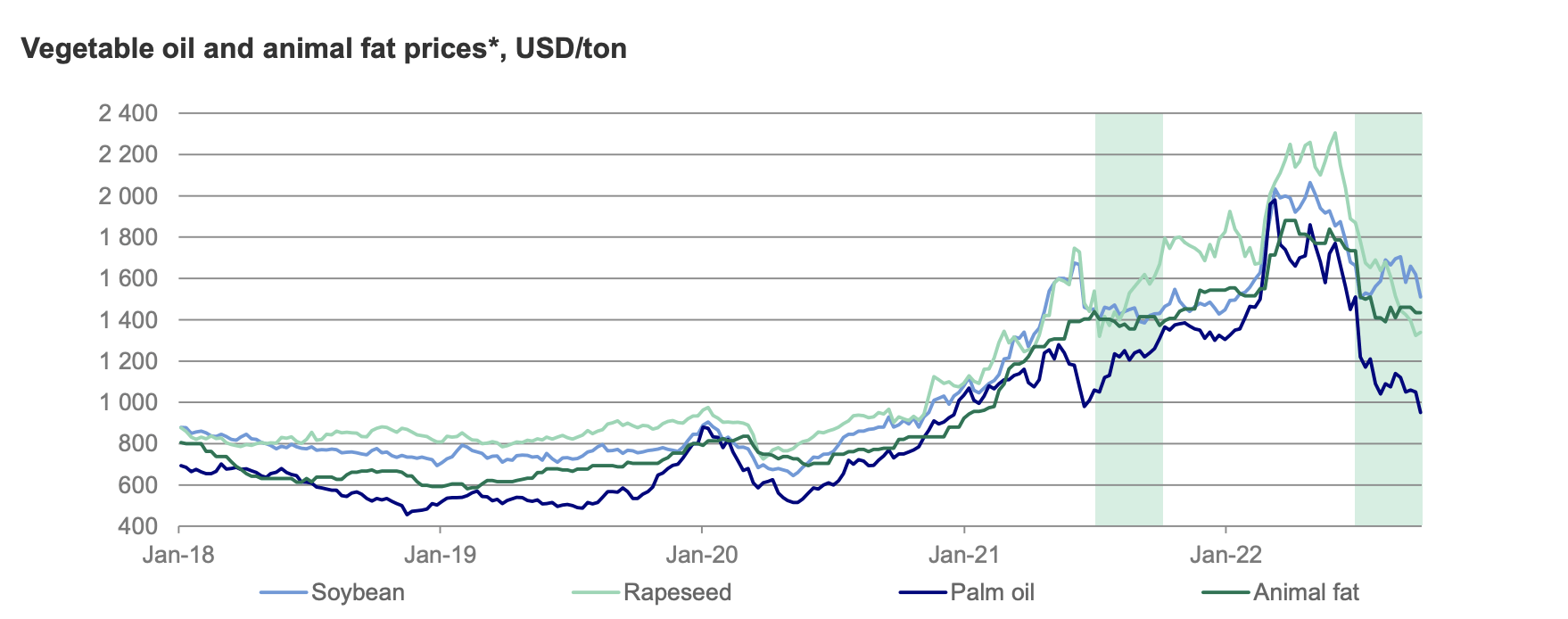

Margins were further supported by good USD FX and increasing sales margins. Segments showed strong performance as well. Renewables above all is what we want to look at here, and this segment was very good, with increases in margins per tonne, significant investments, and good EBITDA, even if the level was below that record we saw in the last quarter of 2Q22. Again, Neste remains fairly FX-exposed, and positive dollar development has a significant impact on the company.

Neste also isn't immune to inflation and cost increases - fixed costs were up significantly, and we're starting to see a softening in the feedstock market, meaning the company can probably start producing cheaper going forward.

{kind=link}

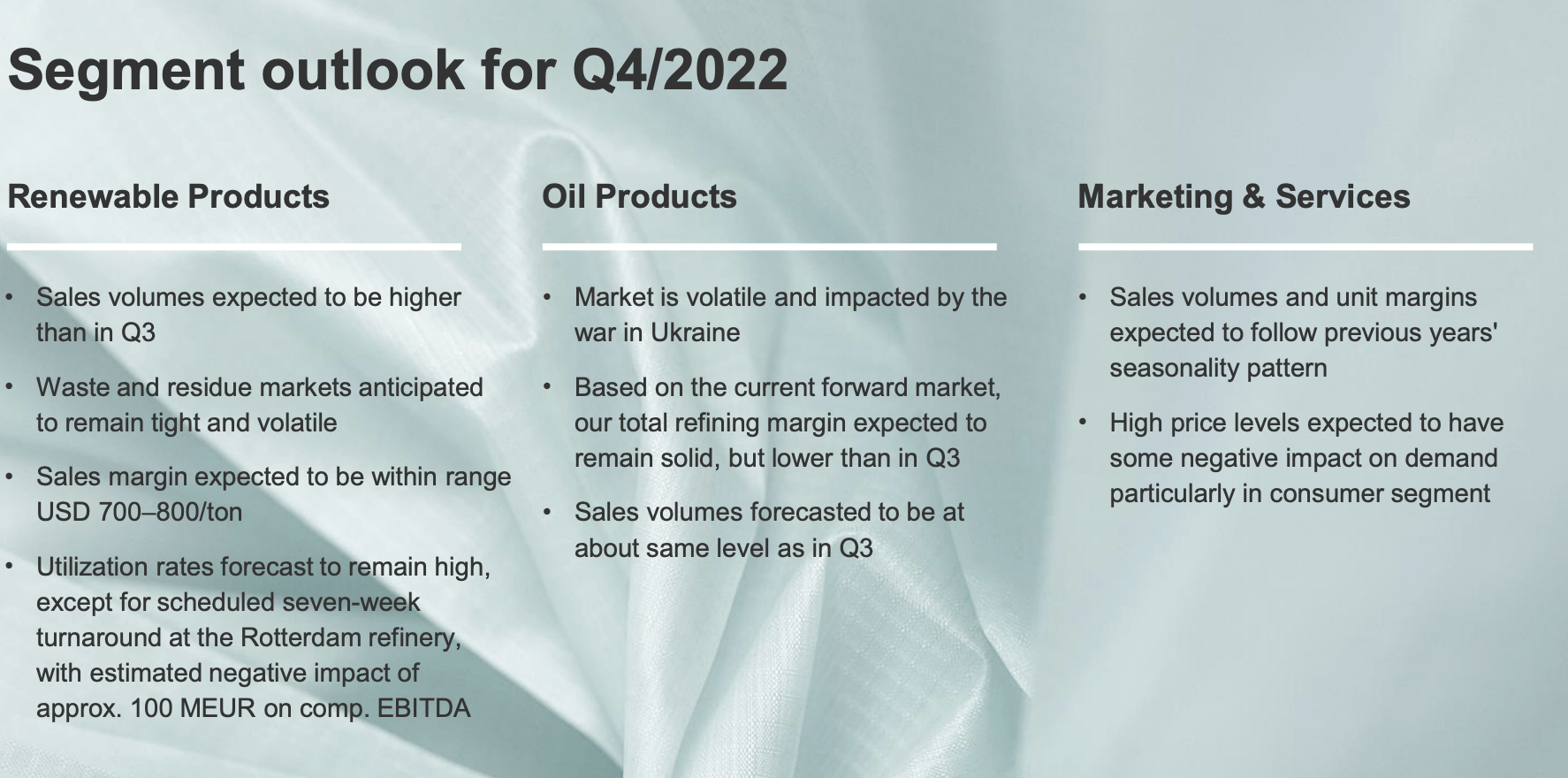

Hedging was a headwind here, but sales margins remained good, and the company's capacity had a utilization rate of about 80%. It's unfair to call anything the star of the show though, except Oil Products. The sheer difference in refining margins is what allowed the company to outperform as it did - without it, we would be looking at EBITDA numbers of perhaps €600M as opposed to nearly €1B. What I mean by this, is that don't expect this to last any longer than the currently positive market for oil products. The markets remain very volatile. Looking at the pre-war/conflict trends, it's clear to me that we'll return to normal levels once this situation winds down, and that means less than a third of the current refining margin.

The company also has its marketing & services segment, and that performed well also.

Neste is a global company, and its plans continue to execute well. The company's expansion project in Singapore is on track and will go online in 1Q23, this quarter, with a CapEx increase of €150M. In addition, the company closed on the Martinez deal, which will see JV operations start up early this calendar year.

The company is also continuing to review and change the nature of its asset base. The Porvoo refinery will be made into a circular/renewable site, with an end to crude refining in the early mid-2030s, still about 10 years off, but a good target.

Here is the current outlook for the full year, which is coming fairly soon.

{kind=link}

Overall, Neste remains a very appealing business in terms of its fundamentals and potential in a world focused on moving to the renewable sector for its energy needs.

At its heart, the use of biofuels is a solution to the current ongoing energy shift - and most northern European nations have hopped on board this train for the past few years. Demand for biofuel is expected to grow at single to double digits annually. The major difference between the EU and US space here is the market-based US approach, which incentivizes biofuel producers.

Neste owns over 800 fuel stations in Finland and 266 stations in Baltic countries (as well as Russia) with the station division acting as an outlet for the company's products. On a high level, the company manages sales of €10-€15B per year, with a 33/33/33 split between Oil Products, Renewable Fuels, and Marketing & Services. This makes up the company's split - and this is why the company is attractive for the longer term.

The primary hindrances to further company success has always been capacity limitations, which is why I am happy to see Neste scaling up operations at a relatively rapid pace, with new JVs and capacities coming online in 2023. The Biodiesel Tax Credit ((BTC)) brings an additional margin to US sales, as well as RIN D4 prices. The additional margin comes from Neste's ability to adjust its sourcing (e.g. waste vs palm oil) and its commercial position. Because of the company's ability to sell essentially 100% renewable Vegetable-oil based Diesel (HVO), makes Neste more resilient to market price fluctuations from crude flows.

But it of course doesn't immunize Neste completely, which is why we need to make sure that valuations, above all, remain attractive when we invest and that we have a solid upside before doing so.

Let's look at where the 2023 valuations currently are, and what we can expect from Neste.

Neste - Valuations are still somewhat attractive despite outperformance

Neste, despite outperforming the market, is still showing that due to growth, it may go far higher. You may recall that the company really had a bout of overvaluation during the COVID-19 EV/tech craze, at which point the company moved up to untold valuations and was something to stay away from.

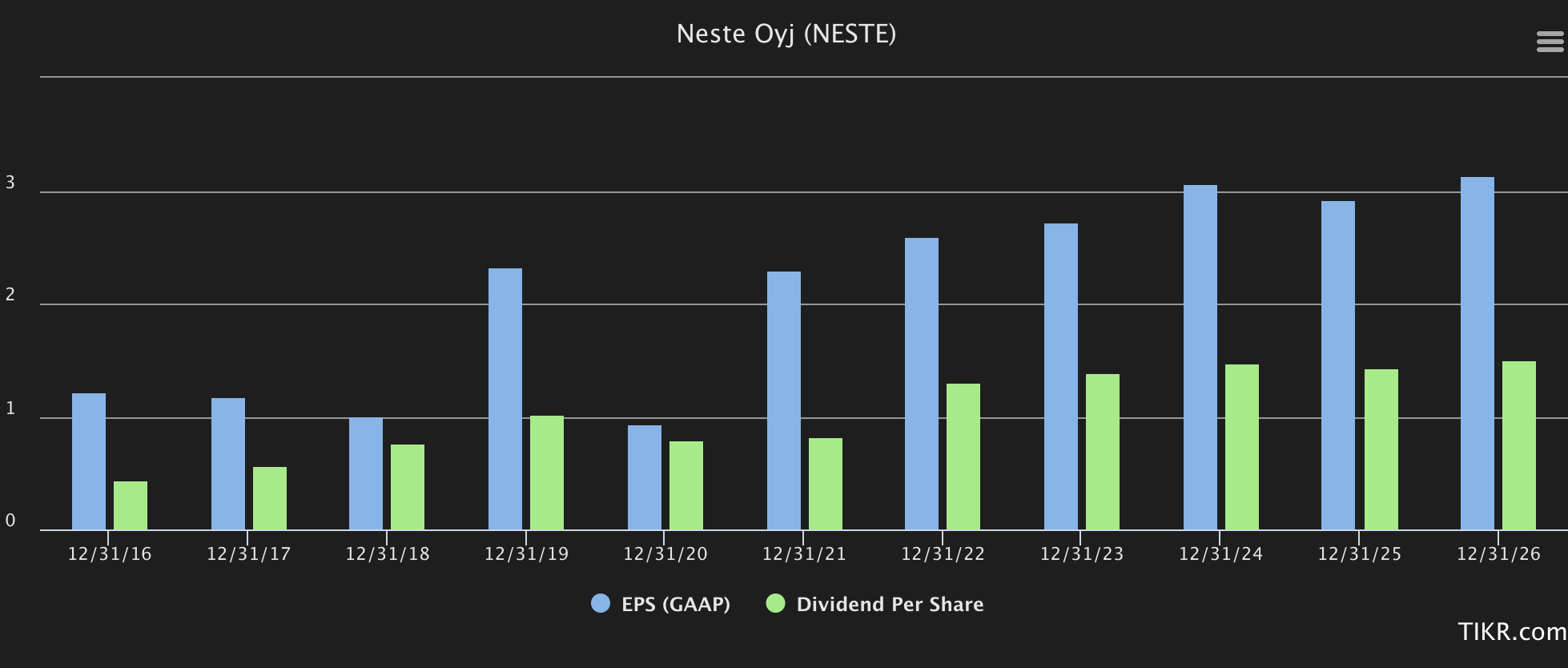

Not today though. I believe there are some issues with FactSet forecasts, as the analysts following the company are suddenly expecting an FY22 EPS drop in the double digits. In order for this to be realized, the entire market would have to reverse and crash - here are the current forecasted trends for Neste in terms of GAAP, which was what we saw before, and which is still valid as I see it. I've also added the expected dividend development for the company, which as you can see is also very positive.

{kind=link}

Converting Neste's output to oil barrel equivalent, the net margin (EBIT/output) in renewables was c. $80/bbl in 2019, against a mere $5/bbl for the oil products division.

We can look at a DCF model and look at an average of 4-6% EBITDA and sales growth for the next decade or so, and this is what I'm doing for the company due to a material increase in demand for biofuels. The company's WACC here is just over 8%, which when we couple it with the other variables in the model, comes to an implied EV range of €42-€49, with a current share price of €45. It's a difference from when I wrote about the company last, and when the price was at sub-€40 - however, we can consider other models as well.

Peers are almost impossible, because no company really has the mix that Neste does, nor does even what it fundamentally does. Comparing it to oil majors would be unfair, and comparing it to pure renewables wouldn't work either, even if it's slightly more workable. We can see some similarities in highly-valued Scandinavian renewable companies and Neste, which typically warrant a 25x P/E, which would imply the company is starting to approach a fair-value level here.

However, my first NAV valuation still holds water, which initially brought us to €42 on the higher end. Adding the new JV and the new operations in Singapore would be able to increase this by a few euros, but not by much - above €44 is hard to really argue for.

Analyst averages have traditionally been low, but have been increasing here as well. The company's current range is €41 to €65, and those at €65 are looking at giving the company's NAV or growth estimates a very high premium. Averages are currently at €52, which I also consider to be too high.

10 out of 21 analysts consider the company a buy here - my latest PT was €46, which would put the company very close to fair value at this time.

However, taking into account new JV's, and continued positive trends, I'm willing to bump this to €47.5, which would imply a somewhat larger undervaluation of at least a few percent. However, the company is no longer the no-brainer "BUY" it once was.

Still, here is my current thesis for Neste.

Thesis

- Neste is perhaps one of the most interesting oil/energy companies in Europe. They've found their niche, and they've pivoted at what I view as exactly the right time to serve a market that's going to need their products for the next few decades at the very least.

- Neste has strong financials and very strong potential. Even if the yield today isn't that impressive, future returns could easily go into high double or low triple digits. My own position is up pretty decently here.

- Neste is a "BUY" with a price target of €47.5 here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Neste is no longer cheap - but it still fulfills all of my other investment criteria, and I therefore consider it attractive at this time.

For further details see:

Neste: Remember Finnish Oil And Its Upside, Reiterate Buy