NTOIF - Neste: The Opportunity Needs Time - But I Remain A Buy

2023-09-27 09:00:00 ET

Summary

- Neste's investment has not performed as expected, with double-digit price drops and negative impacts on earnings and growth.

- Despite the challenges, the company is still viewed favorably and has significant upside potential.

- Neste's financials and growth strategies are key factors in maintaining a positive outlook on the company.

Dear readers/followers,

My investment so far in Neste (NTOIF) has not materialized in the way that I expected it to do during early 2023. If looking at what companies have performed substantially worse than I expected them to, Neste would certainly be at the top of this list for this year so far. This is despite already witnessing double-digit price drops for the company.

I continue to view Neste in a favorable light - but the underlying fundamentals and what drives the company's earnings and growth clearly require more time given what negative impacts we've seen over the past 2 quarters.

In this article, I'll be revisiting my Neste thesis, and look at what I expect from here on out - and moreover, why I'm still investing in Neste, albeit at a relatively slow pace.

This is an update on my already-existing thesis for Neste, last covered in this article.

Neste - I continue to view the upside as significant.

I first started writing about Neste back in 2022. While the company has seen a decline since then, so has the S&P500. Since my first article, the company is down around 18%. Not a good RoR, but then again, underlying fundamentals and industry have not moved the way I, or other analysts, forecasted them to be. It's part of the challenge in the energy sector.

Why do I like Neste so much?

A few reasons. Part of it is that the company is Finnish, commands a €28B+ market cap, has markets around the entire world, and operates two large refineries in the Nordics which account for almost 20% of the Scandinavian production capacity. The fact that it's a financially and fundamentally sound business is certainly part of it as well. In a sense, the company is the world's leading producer of renewable diesel.

Once part of energy giant Fortum (FOJCF) and spun off around 17 years back, it's still state-owned to 40%. The Finnish, like the Norwegian and unlike the Swedish state remains a major investor in structurally important native businesses. The company hasn't applied for credit rating scores from any agency, and thus holds none -but Neste carries minimal debt, with significant borrowings in bonds at an average maturity of 3-4 years.

Unlike most energy companies, part of the company's issue is dividend yield. It has a very low yield, despite its share price decline and sector, which usually lends itself well to income investments.

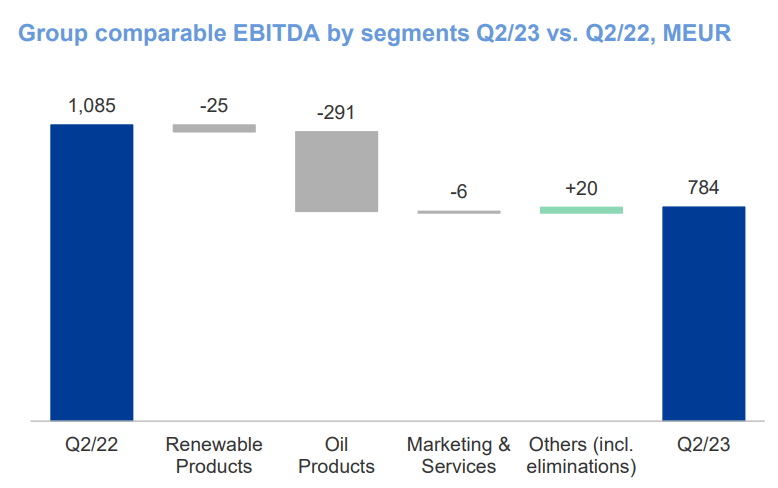

However, the latest set of results does not give encouraging trends in terms of earnings. We're seeing yet more declines in comparable EBITDA despite sales volume increases. The company does have bright spots in its report, including good results from marketing and services - but at the same, reported inventory losses. (Source: 2Q23 Neste )

Growth strategies have been part of Neste's plan for years here. The Singapore and Martinez capacities are things I have been covering in every article on the company - but as with other companies that begin their earnings call by touting their safety records and incident numbers, you usually can tell when the financial part of the results isn't up to par. So was the case for 2Q23 (Source: 2Q23 Neste ).

Company ROACE has dropped from over 30% to 27.4%. This is still stellar compared to a company target of around 15% or above, but here I say that the company is working with a far too low "bar". The company's leverage remains low - but again, it used to be around 10%. It's now 24.3%. So fundamental and relevant KPIs on the financial side are slowly growing worse, and this is part of what's putting pressure on the company's share price.

As a renewable fuel supplier using inputs such as vegetable oil, waste, and residue, the pricing for such feedstock and their logistics costs are a major part of what's driving trends here. Neste's main feedstocks are soybeans, used cooking oil, animal fat and palm oil, with outputs such as diesel, gasoline, and heavy fuel oil.

The latter of these has been at a negative margin on a versus-brent differential for over a year, and the margins have been compressing for the other two since late 2022 - though perhaps a better word would be "normalizing".

However, it's my view that the margin for Neste's 2Q23 was substantially weaker than in the sequential 1Q23, even if they were above certain averages for the longer term. We can't expect margins for fuel and oils to really normalize to Pre-2021 levels. At least not without significant macro changes. But the fact is that Neste is not realizing the potential many analysts saw over a year back.

Both revenues and earnings are down, with earnings as much as 50%, on a YoY basis. This drop is coming from both of the major segments of Renewable products and Oil products. The fact that Neste touts the performance of marketing/services, a less than 5% of revenue/EBITDA segment, shows you that things really aren't that good here - and that a 50%+ drop in operating profit actually means that the company really has held up pretty well compared to how much it could drop.

The problem is refining margins. The estimate is that once the new capacity in Singapore and Martinez are online, these will work to offset these negatives. From a margin perspective, the larger impact came most definitely from the oil products segment. Renewable trends weren't superb, but they weren't as bad.

{kind=link}

Positives? Do they exist here?

Of course, they do. I do maintain a "BUY" rating on this company after all, and I have no plans to divest my shares. I would not be as positive unless there were positives. In the longer term, the company is actually looking fairly decent. On a half-year basis, we're seeing higher volumes and sales margins normalizing at a level that would enable the company to be impressively profitable over time.

The main impacts over the longer term are related to fixed-cost increases. What's more, cash flow is improving. Neste has always been an effective manager of working capital, and it's showing this here. The company's NWC is down to 38.7 days from 56.4, and it's "softer" things like these that I want to point to for Neste advantages here - because these softer targets are mostly what we have to go on here.

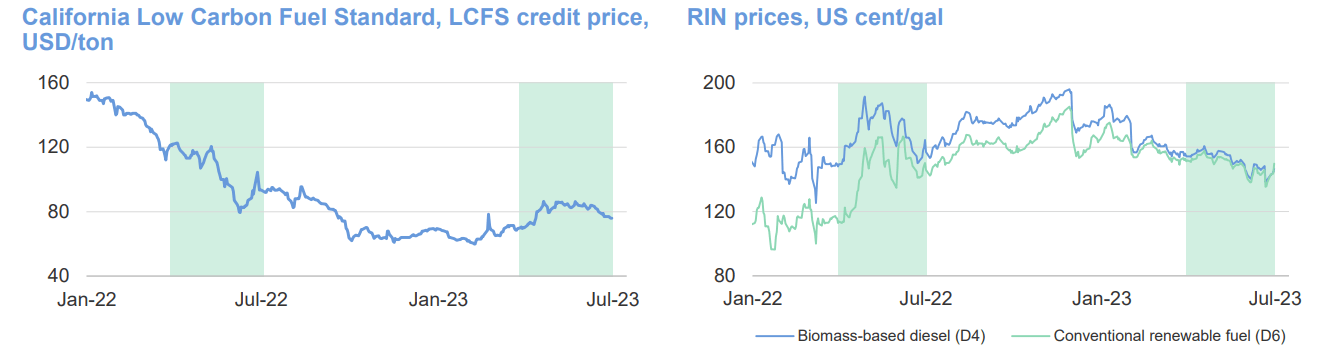

Neste isn't in an easy spot. While Renewable performance remains somewhat okay from the larger picture in terms of EBITDA and even margin, the oil segment is taking a beating. The previously very high LCFS credit prices for California, which have been driving company margins and sales, have also not recovered to any major sort of level, and you can almost retrace the company's share price by following these market drivers for renewables.

{kind=link}

Oil...that's a different story. Refining margins and comparable EBITDA are really in a freefall, despite comparable sales volume and 85%+ refinery utilization rates. The company is a very low-cost producer, with production cost at around $6.3/bbl down from $6.8 YoY, but margins are still driving things lower here due to fixed costs. New assets starting up will do some to normalize this on a company-wide basis, but I don't expect any sort of miracle on a forward basis. Instead, I would say there is still ample room for margins to trend down further.

Neste focus is on its growth ambitions.

{kind=link}

The outlook continues to dictate a complex forecast. 3Q23 volumes are expected to be lower, and fixed costs are expected to increase, with a 4-week maintenance shutdown in Rotterdam in 4Q23, margins are expected to be lower here as well.

The company's liquidity profile remains good - but when we start looking at valuation here, it becomes clear at least to me, that improvement in the company will take more time. There is an upside, but it's in 2024 at the earliest, not this year.

Neste - Positive valuation trends continue

Some analysts are calling for Neste to be a "HOLD" here. I would say that's too conservative/too negative on the company's fundamental valuation and trends - but at the same time, the potential for a near-double-digit drop in 2023E EPS is high.

With the company not even yielding 3% at this time, this is not a high-yielding energy company - and finding a 10% upside that includes a 5-8% yield in this sector is not especially hard in this market that we're seeing today.

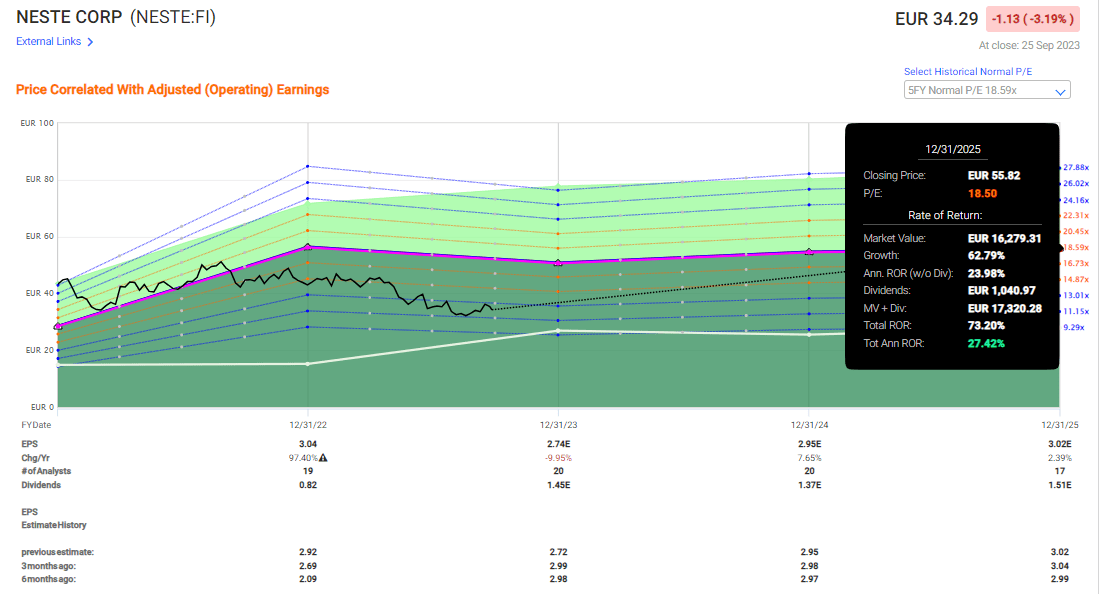

Neste has a few things going for it. It's premiumization is one of those things. Neste typically trades at 18.5x, currently at 12x. With a 3% EPS growth rate, it's not difficult to understand why investors may not be so keen on the business. At a conservative 13-15x P/E range, we're seeing an upside here starting at 10.8% per year, up to around 15.6% to 15x P/E on a forward basis with an implied share price of €44/share in 2025E. That remains the foundation of my positive thesis on Neste. The company is simply too cheap for what it offers investors and even a multiple 3-4x below the premiumized one still results in a double-digit upside.

This is the upside to a normalization of 18.5x

{kind=link}

So you can see, that you would need to essentially expect Neste to really underperform for a long, long time to see a long-term negative RoR here. That's why I continue to be positive about Neste as an investment. The upside, based both on forecasts, on historical valuations, and if we look at peers, it all shows potential upside.

Neste has 20 analysts following the company. Most of those - 15 - are either at "BUY" or similar "outperform" ratings. The average PT goes from €30/share to €60/share. My own PT was €47 in my last article - and I'm not shifting it here. The analyst average is €46.5, implying an upside of 36.4% as the stock trades at the time of writing this article.

I see the positives outweighing the negatives here. I continue to be positive on Neste both due to fundamentals as well as due to long-term growth prospects, as well as comparison to peers. I believe this, despite the lower yield, to be one of the better oil/energy investments that can be made here.

Thesis

My thesis for Neste is now as follows:

- Neste is perhaps one of the most interesting oil/energy companies in Europe. They've found their niche, and they've pivoted at what I view as exactly the right time to serve a market that's going to need their products for the next few decades at the very least.

- Neste has strong financials and very strong potential. Even if the yield today isn't that impressive, future returns could easily go into high double or low triple digits.

- Neste stock is a "BUY" with a price target of €47 here, and I'm sticking to this price as of May of 2023, with the most recent drop in the company's valuation - even with the most recent biofuel mandate.

- Despite more drops in valuation during 2H23, I continue to view it as a positive investment, and I am buying more here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company now fulfills all of my criteria for investing in a business.

For further details see:

Neste: The Opportunity Needs Time - But I Remain A Buy