NTOIF - Neste: The Upside Is Still Very Attractive With A 'Buy'

2024-01-10 02:17:26 ET

Summary

- Neste, a long-term gem in the energy space, is likely to outperform in the long term.

- The company's 3Q23 results showed signs of strength and recovery, with growth in YoY results.

- Neste is undervalued and has strong potential for future returns, making it a positive potential investment.

Dear readers/followers,

My investment into Neste ( OTCPK:NTOIY ) has more or less normalized at this time, since I began investing in it over a year ago. This company remains an underfollowed, as I believe it to be, a long-term gem in the energy space, that over the long term , is likely to outperform. It's neither my largest nor my most significant holding in the space nor is it likely to become that. I value quality and safety coupled with historical stability too much, and the company does not offer this at the same degree that a business like say, Enbridge ( ENB ), does.

Enbridge, as an example, is my largest investment into this space, and very likely to remain such for the foreseeable future.

In this article, I'll update you on Neste based on the latest quarterly results, which happen to be the 3Q23, and I'll explain to you why I'm increasing my pace of buying Neste stock.

This is an updated article. You can find my latest article on Neste here . I have consistently, for a long time, stayed at a "BUY" here with the long-term thesis of outperformance based on operational strength coupled with biofuel and ESG-upside.

Let's see how this thesis has developed since my last coverage.

An update for Neste - 3Q23 indicating further strength

Neste has not been the most solid or impressive investment I have made in the past year. In fact, it belongs to my small list of underperformers, and my position is barely in the green, despite having bought it at what I consider to be a pretty good overall cost basis.

The company has had some mostly weak results for the past few quarters, but 3Q23 finally saw some strength in the overall picture. Results came in at growth to YoY , and we're seeing some preliminary signs of recovery.

Things in the energy sector remain volatile - but there is still good to be found here.

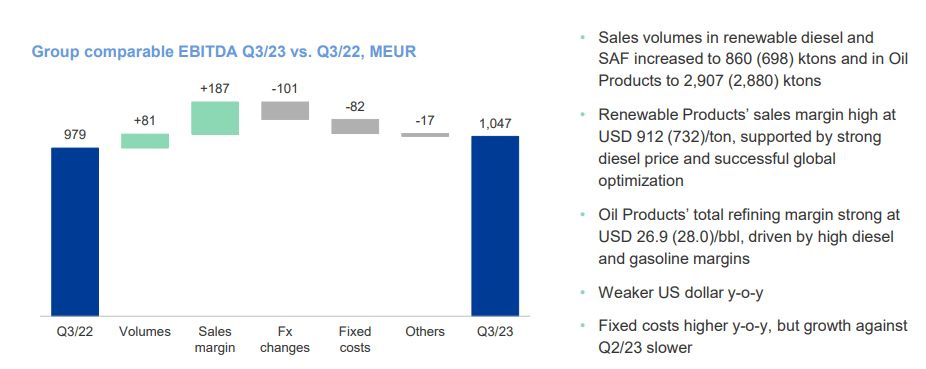

As usual, we begin with bottom-line profits, or Free Cash flow/FCF proxies. In this case, EBITDA, which came in above €1B for the quarter, which is above the YoY period of €980M. The company's renewable sales margins saw a strength at 912 USD per ton, supported by a strong diesel price, and the company executing strong optimization across the globe in feedstocks, markets, and products.

The company's refining margins are at 26.9 USD/bbl in oil products, driven by high margins in both diesel and gasoline, and the company's market & services segment also saw strong results, with inventory gains.

The company is obviously not without challenges. The ramp-up in Singapore continues to present some challenges, though the company was expecting the first production in the end of 2023, in November. Also, the construction activities in Martinez continue, and the company confirms the expectations of having a 730M gallon nameplate capacity by the end of the year.

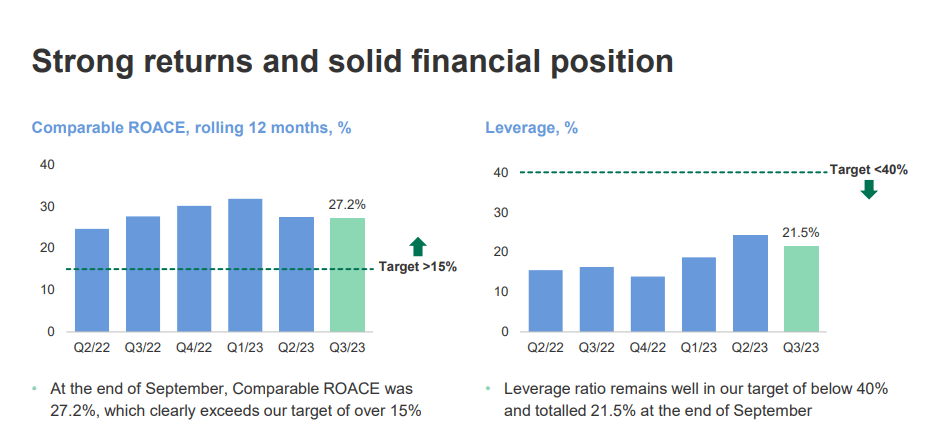

Neste continues to be primarily a play on the macro of energy. Its returns, like comparable ROACE, are driven primarily by this, and while we're not at the top that we saw at the end of -22 or early -23, we're stabilized well above the company target. The new set of initiatives and ramp-ups have added to the company's leverage, but it also remains well below the company's overall target.

{kind=link}

Neste IR ( Neste IR)

Given the company's operations in renewables, feedstock prices like used oil, soybean, palm oil, and animal fat also continue to decide the company's short-term margins and fates. The margins in heavy fuel oil and diesel have been increasing, while margins in Gasoline have been declining, at least toward the 3Q23 October/November period.

Any improvement for the company during the latest quarter was driven by the company's renewable segment - much like in previous quarters when declines were driven by the same segments in part. Oil products keep dragging here, but renewables added no less than €155M to the company's EBITDA, with barely any drag from eliminations, and a solid performance from marketing and services, which contributed to the positive bridge here.

This upside in renewables came not only from higher margins as mentioned, but also from higher sales volumes, continuing to imply interest and strength for the company's products here.

Here is the current 3Q23 volume bridge.

{kind=link}

Neste IR ( Neste IR)

The company can do nothing about FX, and fixed costs will develop given the company's growth strategy, but as the company itself has mentioned, it's growing slower against the YoY period, which is a positive.

Not so positive is the company's continued reliance on the LCFS credit price, along with other subsidies. The future of such movements, such as this one managed by the California Air Resources Board ((CARB)), has implied that they're tightening carbon targets even further, which should provide additional cushioning for Neste, with the current LCFS credit at 75 USD/ton, down from 86, and over 160 at its high.

Also on the current positives, a significant oil product margin improvement.

{kind=link}

Neste IR ( Neste IR)

With both Diesel and most other margins increasing as outages tightened inventories during 3Q23, the picture going forward here is a positive one, against the trend where the company is currently being valued. I also want to mention the significant increase in results by the Marketing & Services segment, which is a clear doubling in less than a single year. The segment has fully reversed, and there is no indication for another crash down to the €20M level, at least not at this time.

{kind=link}

Neste IR ( Neste IR)

But why do I like Neste so much anyway?

Well, there are a few reasons. The company's market cap of over €28B, its home geography of Finland, its history, its markets active across the entire world, its operation of two of the non-Norwegian refineries still remaining in the Nordics which account for almost 20% of the current native capacity, but most of all because of the simple fact that Neste is the largest player in the world in renewable Diesel.

Unlike most energy companies though, part of the company's issue is dividend yield. It has a very low yield, despite its share price decline and sector, which usually lends itself well to income investments. This is also why my investment remains fairly limited.

But let's look at the Risks and Upsides to the company both over the long and the short term.

Risks & Upside to Neste

While one of the primary upsides is the valuation upside to the company, we'll go into that one later. One of the primary risks aside from the volatile macro of the energy sector is the company's recovery of its sub-par profitability. The company manages sub-par operating and gross margins in a sector where many companies have higher (Source: GuruFocus), if we're talking businesses in the Oil & Gas industry. The company also, despite being a market leader in renewable diesel, isn't a market leader in financials or fundamentals. Neste still has a distance to cover before its fundamentals, according to most fundamental valuation methods, can really justify a far higher price point than we're seeing here. Based on most sales models and valuation approaches, or a projection of its free cash flow relative to its peers, this company should trade in fact where it trades right now.

That means the risk here is that the company does not manage its operational improvements, such as Singapore and Martinez, along with other pushes.

But I view the company managing this over the long term as the likely scenario - and I believe the eventual upside if this does materialize, is significant enough to warrant interest here.

I believe the upside can be confirmed, at least on the short term, by the company's special call held about 3 weeks ago. During that call, management reiterated the forecast provided during 3Q23 as follows.

The outlook provided at our third quarter reporting at the end of October remains valid. All forward-looking outlook statements relating to the first quarter of next year as well as the full year of next year remain to be published in our financial year '23 financial statements released to be published on February 8 of next year.

(Source: Martti Ala-Harkonen, Neste Special Call)

All of the positive expectations with regard to Singapore and Martinez have been realized for the most part. A small fire at Martinez has set back some of the plans for full nameplate capacity, but it will be finished eventually - and 2 out of 3 lines at the facility are still operating as normal.

Let's look at company valuation here.

Neste Valuation

The company has many exciting projects in the pipeline, which also need to be taken into consideration when evaluating this company as an investment. To say that Neste is a "future-oriented investment would be an understatement. To my mind, it's one of "the" future-oriented investments in the biofuel space - its recent projects such as green hydrogen in the Finnish location at Porvoo only one of those upsides.

The company is being undervalued here - that's what most analysts, including myself, say here. Trading at almost just 1x sales and at a forward EBITDA multiple of below 9.9x, usually above 13-14x, is significant. 21 S&P Global analysts follow Neste, and out of those, 16 have the company at a "BUY" or equally positive rating, with a range starting at €30/share and going to €60/share, with an average of €44/share.

Recall that my previous target for this company was €47/share, and I am not reducing or adjusting this target at this time - I'm keeping it.

One of the key parts of being a successful value-oriented investor is recognizing undervaluation when it's present. I believe Neste is currently one of the most undervalued biofuel businesses with this sort of scale on the planet.

While the company is unlikely to generate massively significant earnings growth over the next few years due to both macro, but also investment-heavy years, I believe what will come out on the other side is a business with plenty of growth potential. The company's 3.1% yield is decently well covered under the normalized EPS level for the next few years of around €2.5-€3/share, which I believe to be a likely level for the years until and including 2026E.

Provided you allow the company to trade at least 13x P/E despite low growth, that means you could see a double-digit upside here. (Source: FactSet/F.A.S.T graphs)

Why should you allow this?

Because statistically speaking, Neste outperforms. Statistically speaking, this company manages to beat estimates over 65% of the time both on a 10% and 20% MoE on a 1-2 year basis. That's more than a coincidence, in my view, but an underestimation.

{kind=link}

Neste Outperformance (F.A.S.T graphs)

And it's the sort of underestimation I am happy to invest in.

Here is my ongoing thesis for Neste, mostly unchanged since my last article.

Thesis

- Neste is perhaps one of the most interesting oil/energy companies in Europe. They've found their niche, and they've pivoted at what I view as exactly the right time to serve a market that's going to need their products for the next few decades at the very least.

- Neste has strong financials and very strong potential. Even if the yield today isn't that impressive, future returns could easily go into high double or low triple digits.

- Neste stock is a "BUY" with a price target of €47 here, and I'm sticking to this price as of May of 2023, with the most recent drop in the company's valuation - even with the most recent biofuel mandate and further reductions in credits.

- I view the company as a positive potential investment for 2024E.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company now fulfills all of my criteria for investing in a business.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Neste: The Upside Is Still Very Attractive With A 'Buy'