NSRGY - Nestlé: Dividend May Not Be As Sustainable As It Seems

2023-06-23 11:00:00 ET

Summary

- Nestlé faces stagnant growth and increasing debt, which may negatively impact its dividend and long-term prospects.

- The company's valuation is considered overvalued, with its growth and profitability lagging behind competitors like Mondelez, General Mills, and Hershey.

- Nestlé's future growth may depend on SKU optimization, the growing importance of the PetCare segment, and exposure to the rapidly growing Indian market.

Intro

Nestlé (NSRGY) is one of the world's largest companies, a leader in the food and beverage market. We are talking about a company with more than 150 years of history, whose brands are part of the daily purchases of millions of households and businesses around the world. Its operating business is branched into three main segments:

- Food and Beverage: this is the most relevant segment, as it offers most of the world-class brands: Nescafé, KitKat, Nestea, Maggi, Nesquik ; as well as Purina , an international cat and dog food brand.

- Nutrition and health science: this segment has a more specific target customer base, as it deals with medical nutrition products, specialized health products, and dietary supplements. In short, unlike the previous one, it is more exposed toward promoting values such as living well and healthy. The main brands are Optifast, Garden of Life, Peptamen and Meritene .

- Nestlé Professional: This segment provides food and beverage solutions for restaurants, hotels and catering services. The most popular brands are Chef, Nescafé Professional, Santa Rica , and Minor's.

In short, as soon as we set foot in a supermarket anywhere in the world we find a Nestlé product. Such dominance has been possible over the decades and it is unlikely that anything will change in the next few years.

In any case, as much as I esteem this company, I believe that objectively there is a problem related to its growth, and this could also negatively affect the dividend. In this article I refer to a long-term perspective rather than a short-to-medium-term perspective, which is why I will give more weight to annual results rather than the latest quarterly results.

Growth is becoming a problem

From a company with such leadership we might expect steady growth over the long term, however, this is not the case. While it has demonstrated pricing power during this inflationary period, the problem of zero revenue growth over the long term remains.

{kind=link}

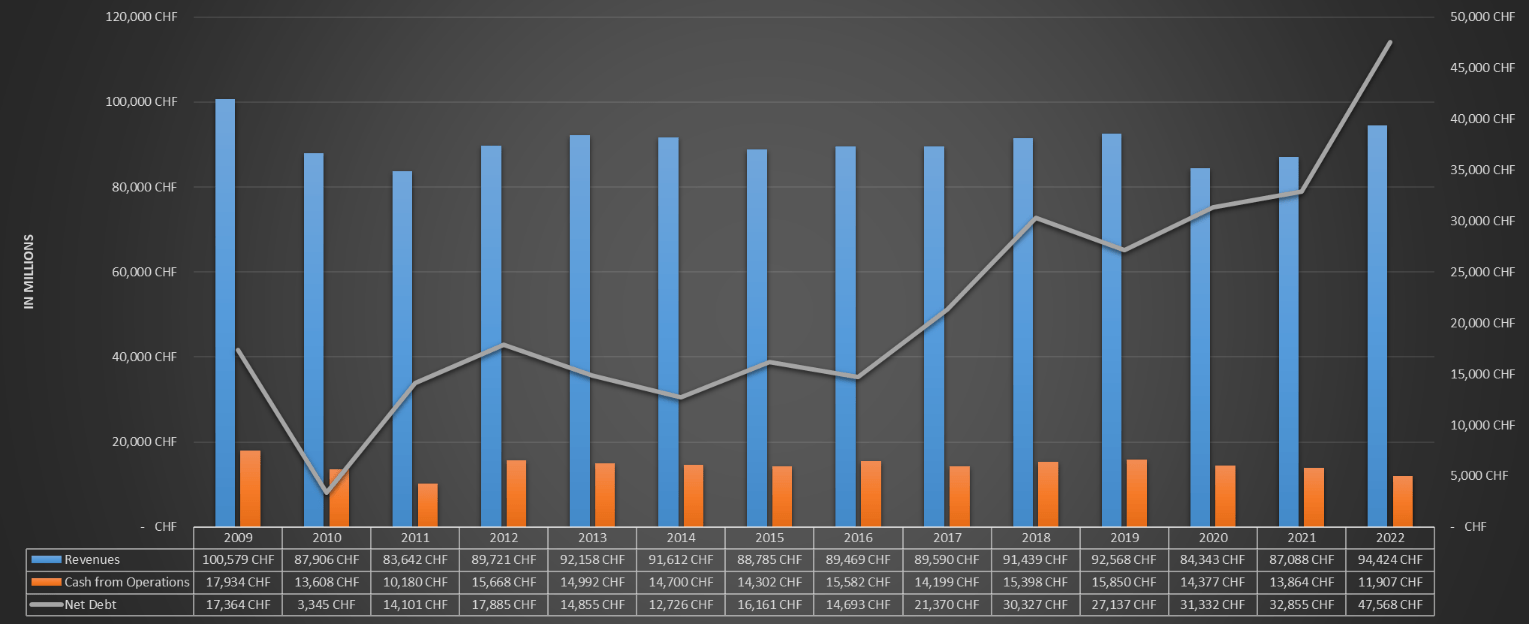

As we can see from this graph, from 2009 to 2022 revenues did not grow, on the contrary. They have fluctuated between CHF 83 billion and CHF 94 billion. In short, always very steady but not growing over the long term. For cash from operations the argument is similar, the only difference is that it is getting worse in the last 3 years.

In all this, while profitability has not improved, debt has increased: CHF 17.36 billion in 2009, CHF 47.56 billion in 2022. In short, about CHF 30 billion more net debt but stalled profitability.

{kind=link}

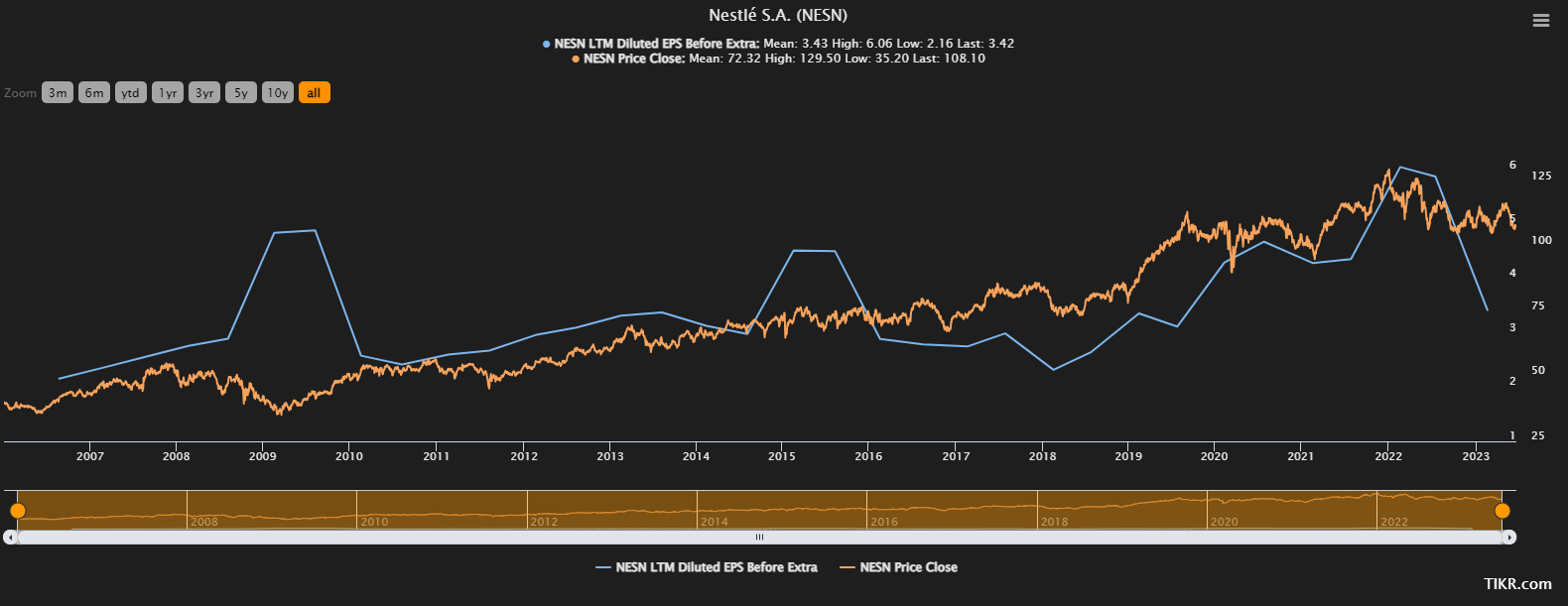

Overlaying the trend of diluted EPS and price per share, we can see that indeed something is changing for Nestlé. From 2006 to 2015, diluted EPS was steadily increasing over the long run and the price per share followed the same trend. From mid-2019 to mid-2023, diluted EPS did not improve at all; in fact, the price per share remained unchanged.

Practically, 0% capital gain in 4 years when the S&P500 rose about 60% over the same period. Being a defensive stock, we cannot expect mind-blowing performance from Nestlé, but I think such a result during a bull market does not please anyone. Moreover, considering the total return including dividends, not much changes.

{kind=link}

The dividend yield on cost in mid-2019 is 3.63%, which changes the situation relatively little. Moreover, on dividends I would personally question their sustainability.

As we have seen before, Nestlé is struggling to increase its EPS, so if it wants to issue an increasing dividend in the long run sooner or later it will be unable to do so unless it can find new growth catalysts.

{kind=link}

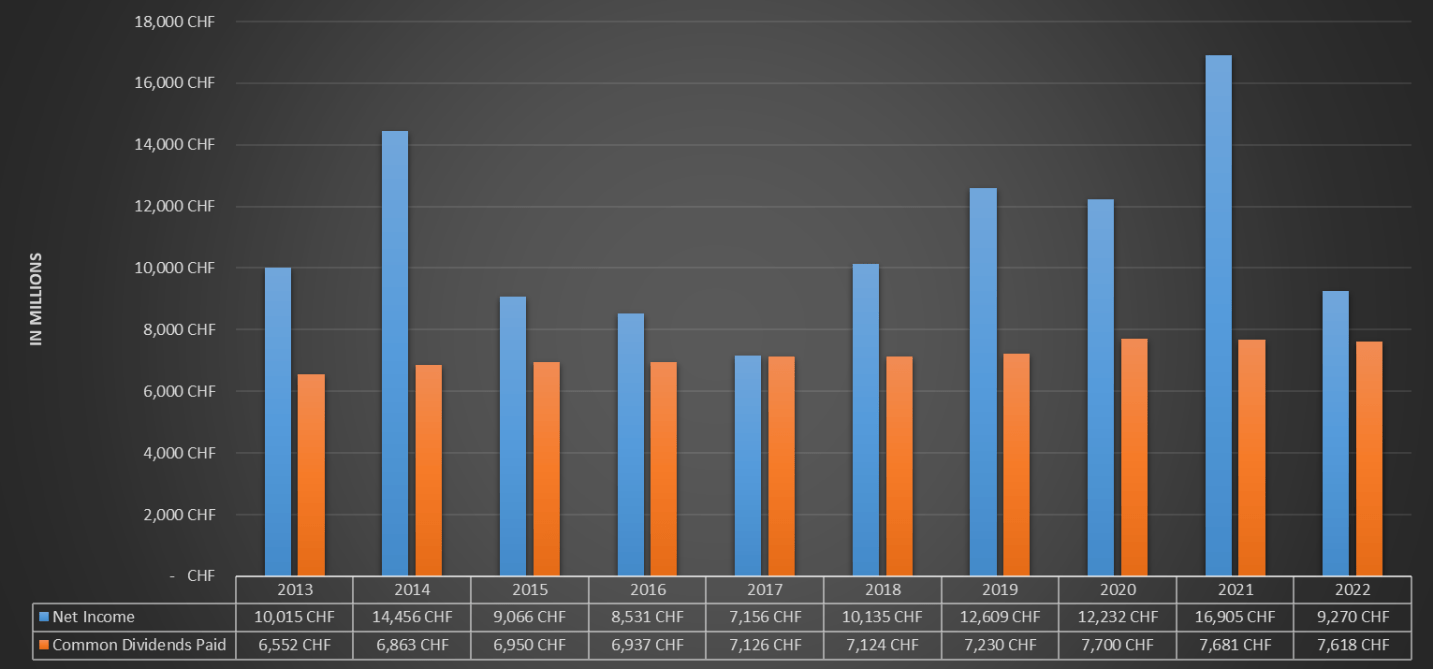

The dividend issued is the only thing along with debt that has grown steadily over the long term, and I doubt it can continue to be sustainable at this rate. Net income still manages to support the issuance of a CHF 7.61 billion dividend, but for how long can it do so? Nestlé has failed to achieve satisfactory growth in recent years; it has always alternated between good and bad times. Moreover, for those interested in the current dividend yield of 2.74 percent, they must consider the Swiss withholding tax of 35 percent, which greatly reduces the net dividend received.

Valuation

Since the dividend tax on Swiss companies is quite high, capital gain becomes the main driver for good returns by investing in companies in the Swiss territory. However, in my opinion, I believe this is not the case for Nestlé since I consider it to be overvalued.

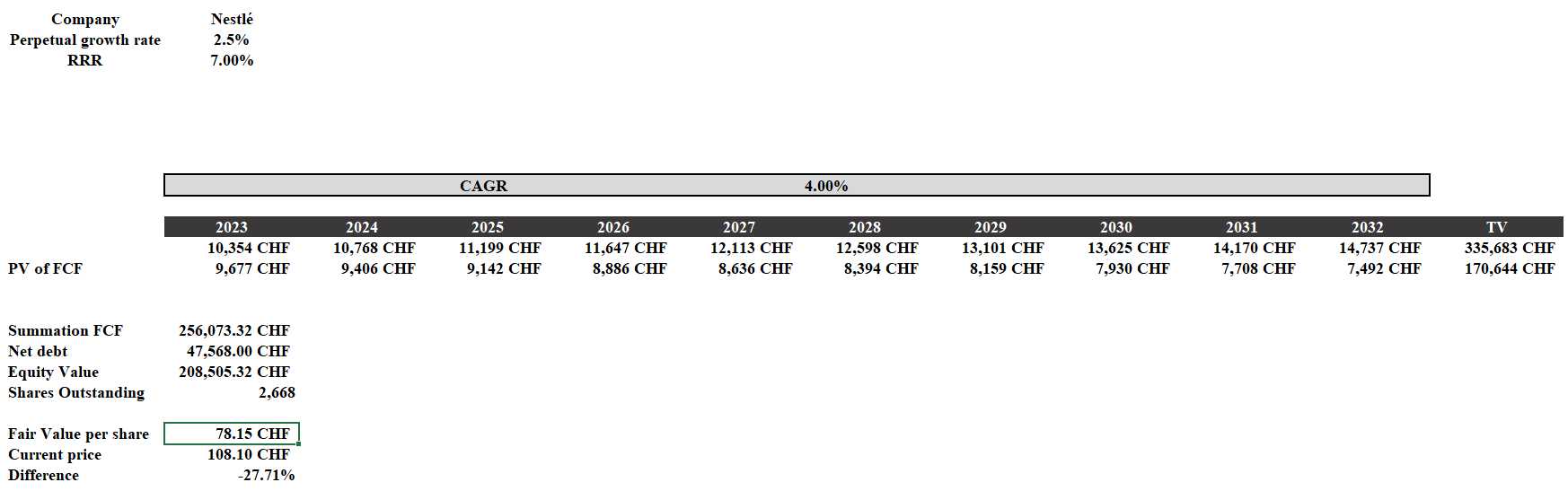

To calculate fair value I will use a discounted cash flow, it will be constructed as follows:

- RRR will be equal to 7%. Even if the cost of equity is lower, I personally prefer not to consider investments below 7% because they would be too far below the long-term average return of the S&P500.

- The growth rate will be 4% from the average free cash flow of the last 5 years, or CHF 9.95 billion. For perpetual growth the rate will be 2.50%.

- The source of net debt and shares outstanding is Seeking Alpha.

{kind=link}

According to these assumptions, Nestlé's fair value is about CHF 78.15 per share, so the stock is definitely overvalued. I agree with buying this company at a premium price given its competitive advantage, but at the current price it is way too much.

{kind=link}

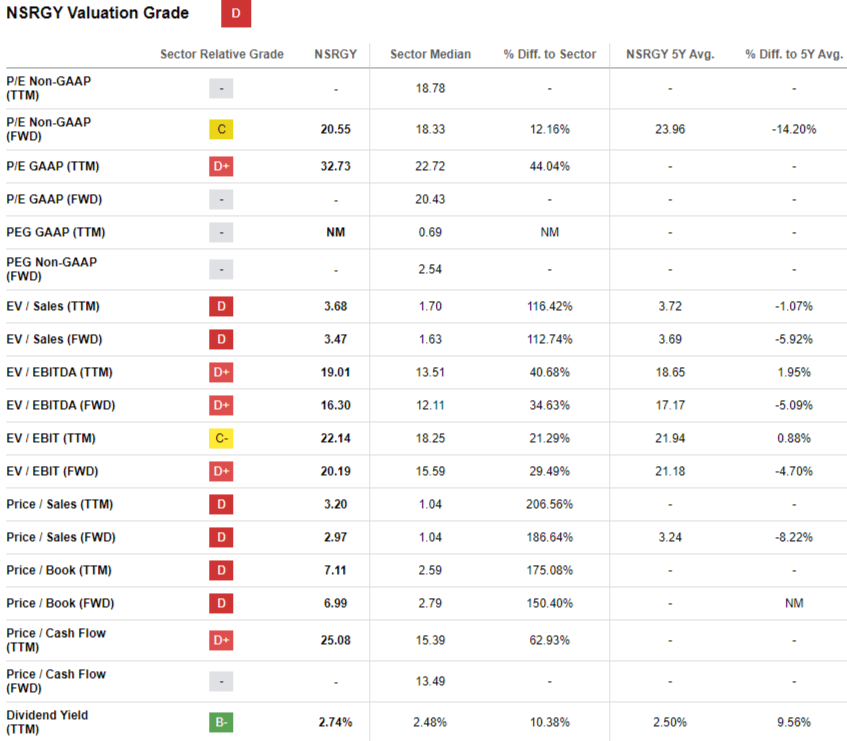

Indeed, the valuation multiples are also far too high compared to peers, albeit in line with the last 5 years. I would justify this result if Nestlé were growing faster, but as we have seen above, growth is its biggest problem.

{kind=link}

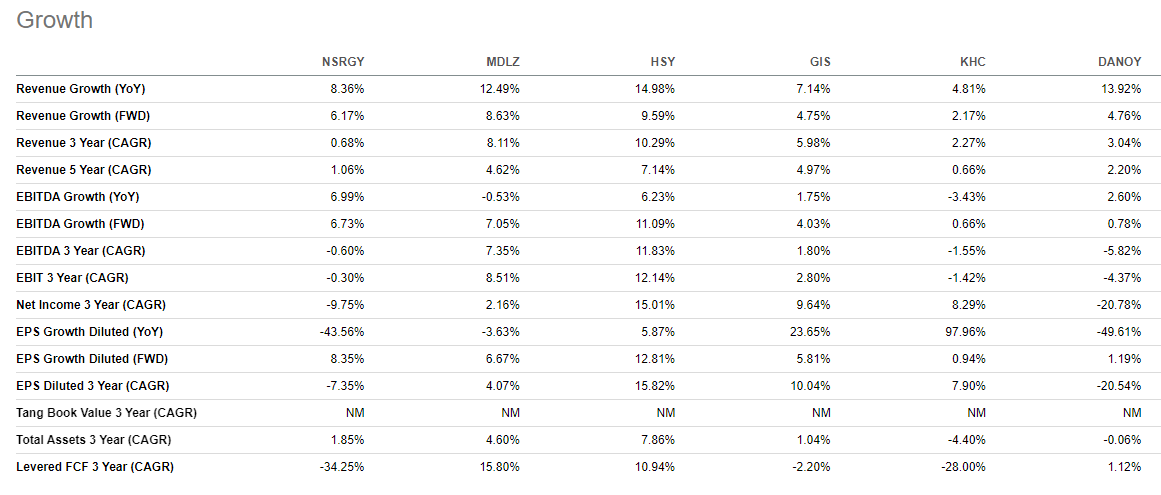

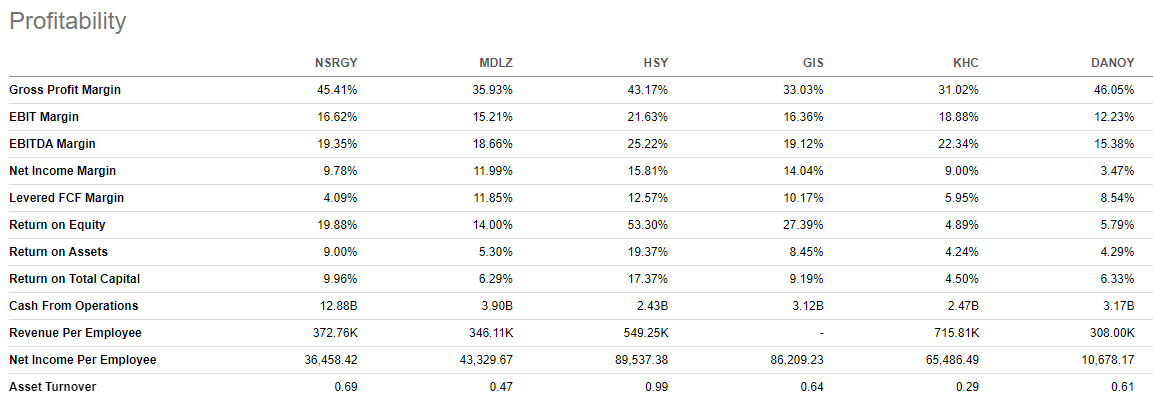

Mondelez (MDLZ), General Mills (GIS), and especially Hershey (HSY) have performed better on all fronts in terms of growth. But not only that, they also performed better in terms of profitability.

{kind=link}

Nestlé's net income margin does not reach double digits unlike its competitors. In short, for both growth and profitability reasons, I believe Nestlé has valuation multiples that are too high; therefore, I consider it overvalued.

The main factors that will influence Nestlé's future

Knowing the future is impossible, however, when we talk about a company like Nestlé we can make fairly reliable predictions. We almost certainly know that Nestlé will continue to be one of the leaders in the food and beverage market in the coming years; it is too big not to be. Also, based on previous observations, we know that revenues are very steady if not growing: the trend could continue. However, there are in my view some aspects that can unlock the static nature of this company, both for the better and for the worse.

Starting with the first, I have identified three.

The first is that SKU optimization could reduce Nestlé's unnecessary costs and increase profit margins. François-Xavier Roger ((CFO)) mentioned it several times during recent conference calls, as it is currently a primary goal for the company. Moreover, with the money saved, management could invest that money to spread the footprint of the company's most successful brands. Nestlé has acquired several companies over the years, but not all of their brands have been as successful as hoped. Continuing to market and publicize them comes at a cost that is not worth it, which is why it is better to remove them from the portfolio.

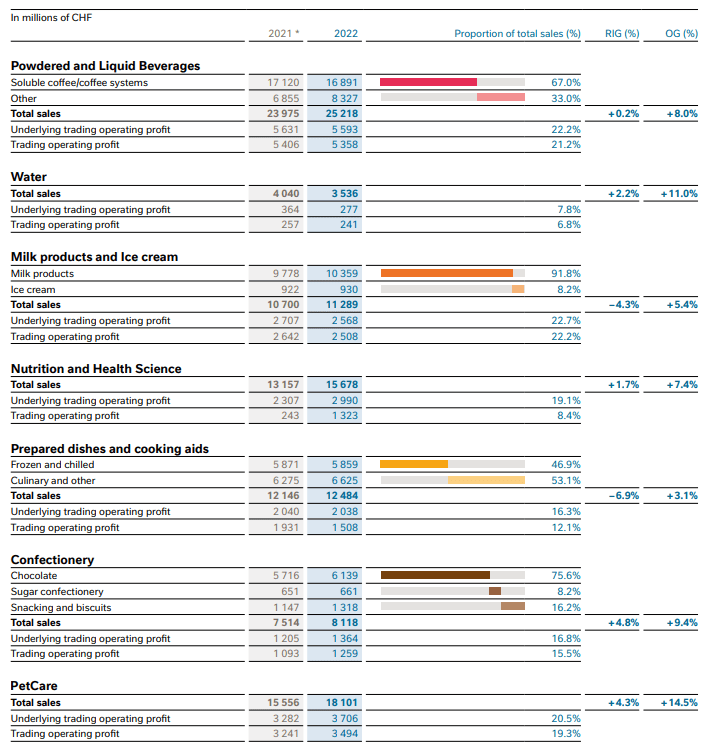

Another aspect that I think could drive revenue growth is the growing importance of the PetCare segment. In particular, the Purina brand is definitely the one with the greatest growth prospects. When we think of Nestlé, the first thing that comes to mind is not dog food, yet this segment has become critical for the company.

{kind=link}

Not only did it become the second largest in terms of revenue, but it also experienced the best organic growth in 2022. In short, the acquisition of Ralston Purina for $10.3 billion is paying off.

Finally, staying on the topic of acquisitions, perhaps not everyone knows that Nestlé owns 20.11% of L'Oréal (LRLCF) and is intent on keeping its stake. The French company is one of the most important in Europe and its numbers are flawless.

{kind=link}

The third and final aspect that I believe may prove to be a positive factor for long-term revenue growth concerns exposure to India. Since Nestlé mainly sells food and beverages, I attribute its poor growth over the past decade to the stagnant population in its core markets. After all, if the number of people needing staple foods does not increase, it is difficult to sustain sales volume growth. Especially when you are already the market leader.

United Nations Department of Economic and Social Affairs

India , however, does not have this kind of problem; on the contrary, the average age is very low and the population is soaring. Recently, India's population has even surpassed China's.

Given the vastness of this market, this is a huge opportunity and one that can potentially breathe new life into Nestlé. The latter, has exposure in this market through its 62.76 percent -owned subsidiary Nestlé India.

{kind=link}

The numbers seem to support my thesis, in fact, unlike the parent company, Nestlé India is growing very rapidly. India is in my view the biggest opportunity that Nestlé will have to exploit, and I believe it can succeed. Investments of ?5,000 crore are expected by 2025: management is serious about it.

Given the growth drivers, let us now turn to the aspect that concerns me most beyond the stagnant Western market due to the population slowdown.

This risk has to do with the last image I just showed you. If you notice, the growth in India has been pretty steady and increasing, except for 2015. What happened that year? The Food Safety and Standards Authority of India ( FSSAI ) banned the Maggi brand because it contained excessive levels of lead. It was a blow to Nestlé's reputation, as it owned 80 percent of the instant noodle market with that brand. Well, the risk is that a similar situation could happen again, not necessarily with the same brand. These kinds of events can easily deteriorate the reputation of any company, but if you are Nestlé you might risk even more.

Perhaps not everyone knows this, but Nestlé is one of the most hated companies in the world. Since the 1970s there have been a series of unethical scandals involving the company, which has annoyed quite a few consumers. I will not list them as I do not think it is relevant to this article, but simply tell you that they are many and also quite serious. As absurd as this all sounds, during the 1970s-80s was even established for 7 years the International Nestlé Boycott Committee . Although it no longer exists long ago, many consumers are still hostile to the company.

Well, considering this reputational problem, Nestlé can no longer make a mistake if it does not want to lose the trust of even its most loyal consumers. Moreover, it is good to remember that when such events happen, legal costs should also be considered.

{kind=link}

Technically, legal settlements should be expenses of an extraordinary nature, but for Nestlé they are now part of business as usual.

Conclusion

Nestlé is one of the world's most popular companies in the food and beverage market. Its dominance in the West is undisputed, but its revenues are now stuck a decade ago. Earnings are struggling to grow and this does not help the issuance of a growing dividend over time. Investment in new markets is needed, and India seems to be the main target now. In addition, the strategic stake in L'Oréal is proving to be a success.

Regarding valuation, at the current price I consider Nestlé to be overvalued, but my rating is a hold. In my opinion, shorting it would really make little sense given its low volatility and high fees to make this trade; selling as well could prove to be a mistake, especially for those who bought it at a low price with a long-term view. For the time being, dividends are sustainable, and this could be the small consolation while waiting for growth to return.

For further details see:

Nestlé: Dividend May Not Be As Sustainable As It Seems