NSRGY - Nestle: Exaggerated And Non-Existing Problems

2024-01-02 15:49:21 ET

Summary

- After yet another disappointing year for Nestle's shareholders, the stock appears very attractive as we enter 2024.

- The lack of revenue growth is hardly a cause of concern for investors with a long-term horizon.

- Business fundamentals have improved notably in the past few years and the higher leverage ratio is also a positive sign.

The past few years have been quite a disappointment for Nestlé S.A. (NSRGY) shareholders with total returns lagging those of the broader consumer staples sector. After appreciating nearly 30% in 2021, the share price has fallen sharply in 2022 and remained relatively flat during the past year.

Thus, NSRGY's total return now stands at 9% since July of 2020 , while the Consumer Staples Select Sector SPDR® Fund ETF ( XLP ) has delivered a total return of roughly three times that rate.

It seems that the market has been largely unimpressed by the company's topline figures over the past few years and at the same time large cap companies within the Packaged Food sector have experienced a multiple contraction in recent years, due to large increases in input costs.

Given Nestle's premium multiple and its enormous size, it is hardly a surprise that in such an environment the stock was severely punished. Given the high quality of the business, however, its ability to earn above-average return on capital and derive significant price premium from customers, I see this as a very good opportunity for long-term shareholders.

Don't Mind The Lack Of Revenue Growth

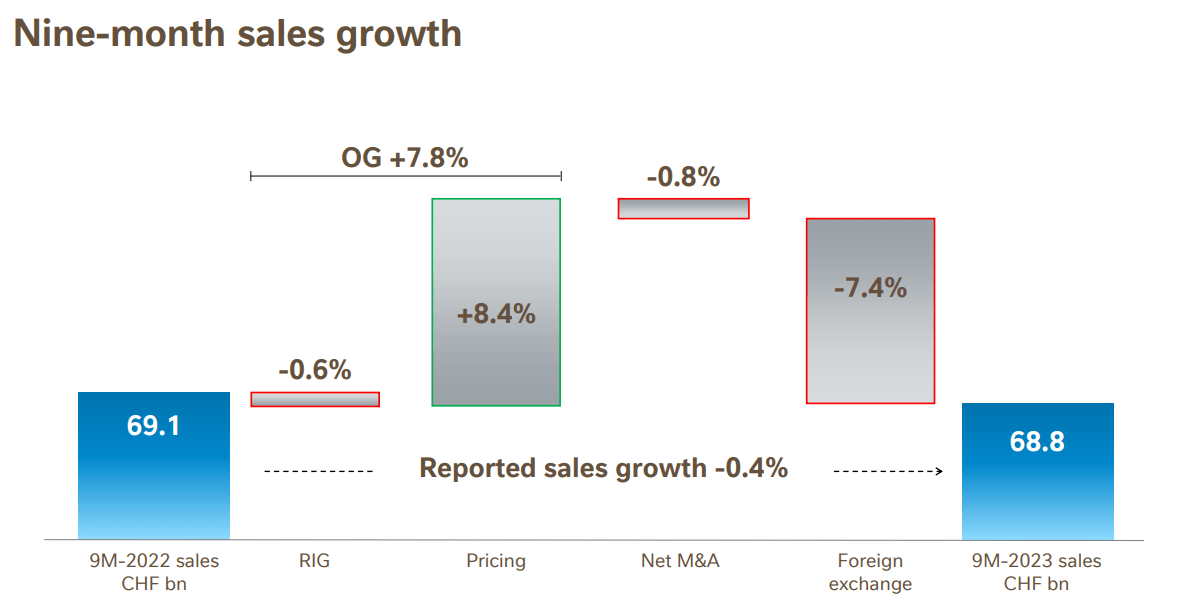

Investors who focus predominantly on short-term sales figures, are likely to have been very disappointed by Nestle's falling revenue during the first nine months of 2023 when compared to the prior period.

{kind=link}

The sales growth breakdown we see above, however, is more than enough to point us in the right direction when it comes to Nestle's competitiveness.

First and foremost, during the aforementioned period the company experienced a massive foreign exchange headwind. The 7.4% decline caused by the strengthening of the Swiss franc appreciation against many Emerging Market currencies is an event that is irrelevant for medium to long term holders. The reason being that changes in exchange rates tend to cancel each other out over longer periods of time.

The second part, is that Nestle's strong brand portfolio allowed for significant price increases, aimed at transferring the rising raw material costs onto the consumer. What is so impressive here is not the extent of the pricing tailwind - a positive 8.4%, but rather the muted response of the company's volumes - real internal growth ((RIG)).

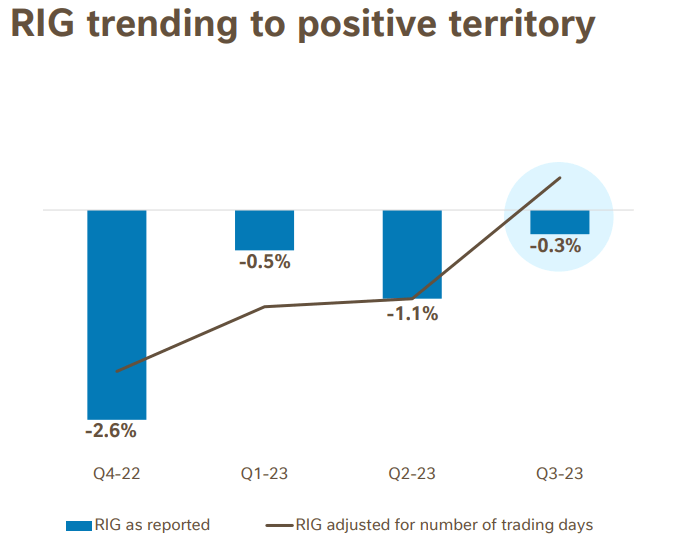

As we see from the graph below, Nestle's RIG has been a negative 2.6% during Q4 of 2022 and has already turned positive in Q3 2023 when adjusted for the number of trading days.

{kind=link}

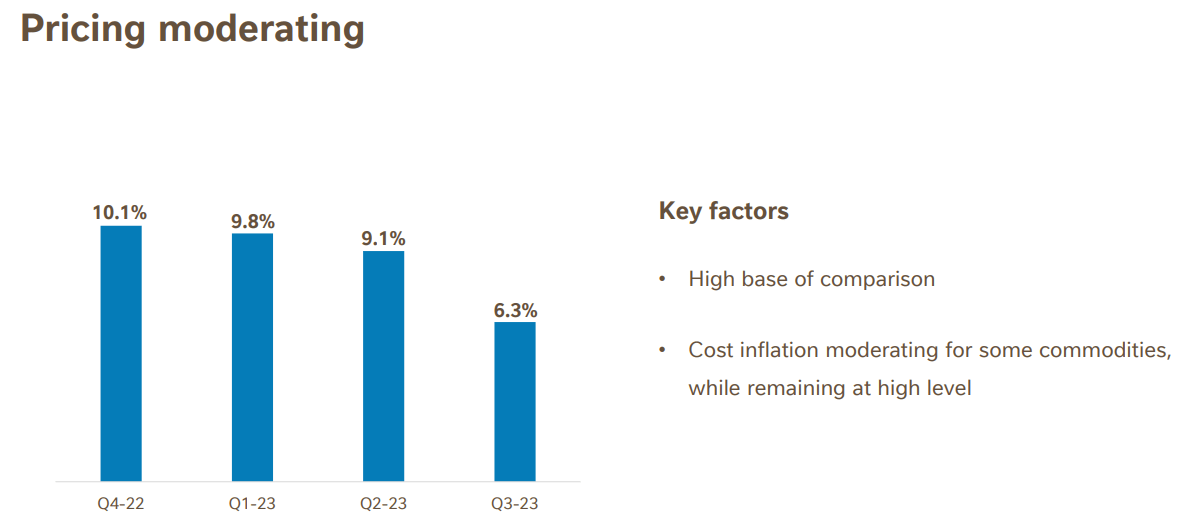

In the meantime, pricing remained high even after noting a sharp drop during the third quarter of 2023.

{kind=link}

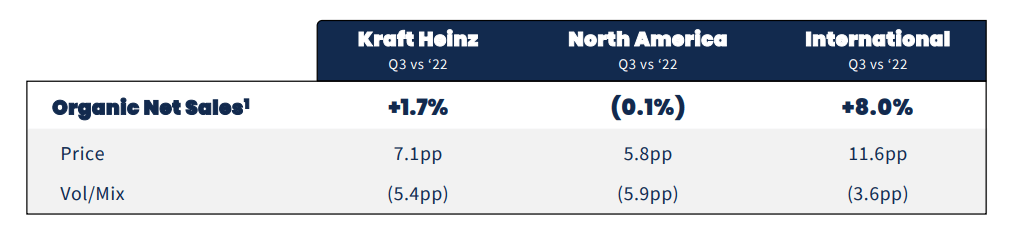

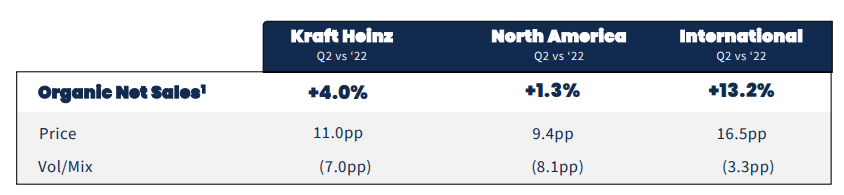

To get an idea of how this dynamic between pricing and volume/mix growth compares against peers, we could take a closer look at one of Nestle's major peers - Kraft Heinz ( KHC ).

During Q3 and Q2 of 2023, KHC experienced a slightly higher pricing tailwind than Nestle - 7.1% and 11% respectively, however, the volume/mix headwind was far greater at -5.4% and -7.0% for each of the two periods.

{kind=link}

{kind=link}

This clearly illustrates the strength of Nestle's brand portfolio and puts the recent decline in total sales into perspective.

Record High Return on Equity

As Nestle's valuation multiples have deflated over the course of 2023, its underlying return on capital remained near all-time highs. Return on equity for the past 12-month period, for example, stands at 25% which is one of the highest on record.

prepared by the author, using data from annual and half year reports

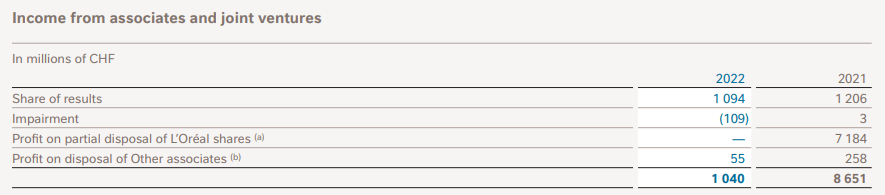

We should also ignore the 2021 period, when the net income figure included a CHF 8.6bn benefit from the partial disposal of L'Oreal ( OTCPK:LRLCY ) shares.

In 2021, divestments in L’Oréal relate to 22.26 million shares sold to L’Oréal

Source: Nestle Annual Report 2022

{kind=link}

If we ignore this one-off income from associated and joint ventures and compare the key drivers of return on equity, we could clearly see the notable improvement of the business model since 2021.

When compared to 2021, operating margin is up slightly while asset turnover of Nestle's tangible assets (excluding goodwill and reported intangible assets) is up significantly. Although the latter might not seem as much, we should keep in mind that tangible asset turnover ratios are very stable within the industry.

prepared by the author, using data from annual and half year reports

Lastly, leverage is also up significantly since FY 2021 and this is likely to be a cause of concern for some investors as interest rates are normalizing. However, it is very important to put things into perspective and properly account for Nestle's conservative capital allocation.

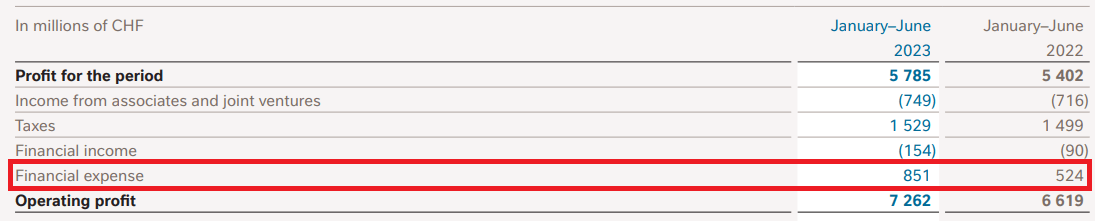

When looking at interest expense in isolation, we could easily be led to the conclusion that financial health of the company has deteriorated in recent months. The total financial expense of Nestle for the first six months of 2023 has increased by more than 60% from the prior year period - from CHF 524m in 2022 to CHF 851m in 2023.

{kind=link}

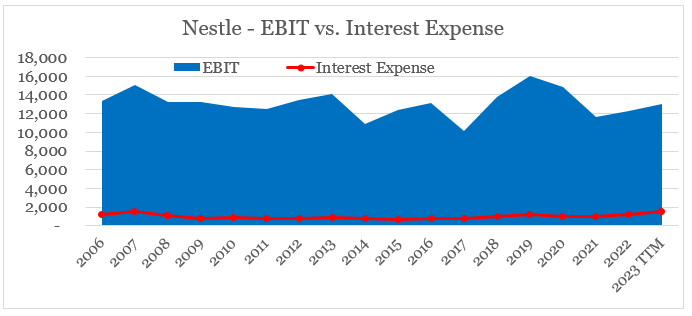

Having said that, however, Nestle's interest coverage ratio is at healthy levels and well-above the industry average .

prepared by the author, using data from annual and half year reports

{kind=link}

Thus, the recent increase in total debt brings the company's capital structure to more optimal levels which would continue to benefit shareholders.

Conclusion

Nestle remains as one of the best-in-class businesses within the Packaged Food space and the recent decline in the share price significantly improves potential for future returns. The lack of topline growth in 2023 is hardly a problem, once we dissect the company's organic revenue growth drivers. In the meantime, Nestle is achieving a record-high return on capital, without taking significant financial risk.

For further details see:

Nestle: Exaggerated And Non-Existing Problems