NSRGY - Nestle: H1 2023 Results Are Out Optimization Is On Track

2023-07-27 18:57:44 ET

Summary

- Nestle's H1-23 results exceeded expectations with 8.7% organic growth and CHF 2.13 EPS, demonstrating the company's strength in a challenging consumer environment.

- Nestle's strong results indicate the successful implementation of its optimization strategy focusing on high-growth, high margin products.

- The company upgraded its 2023 guidance and reaffirmed its long-term targets, which suggest there's significant upside in Nestle's turnaround story.

- It's not a potential ten-bagger, but Nestle should be a cornerstone in any long-term dividend investor's portfolio.

- I reiterate a Buy rating, with a price target of CHF 120 per share or $138 per ADR.

Nestle ( OTCPK:NSRGY ) ( OTCPK:NSRGF ) published its H1-23 results that exceeded expectations, reporting 8.7% organic growth and EPS of CHF 2.13, reflecting an 11.1% increase Y/Y.

The consumer staples giant demonstrated the strength of its offerings in a tough consumer environment, as price increases of 9.5% were answered by a lower-than-expected underlying volume and mix decline of 0.2%.

I reiterate a Buy rating, with a price target of CHF 120 per share or $138 per ADR.

Background

I initiated coverage on Nestle in February, claiming its ' RIG Growth In 2022 Signals It's Time To Buy ', as I found the company's pricing power much stronger than what the analysts' consensus reflected at that time.

I urge you to read that article, in which I described my investment thesis in detail, as well as the group's amazing portfolio of brands, long-term strategy, risks, competitors, and the major growth prospects I project for 2023 and beyond.

In short, my investment thesis in Nestle is based upon the immense pricing power it possesses with its portfolio of staple brands, as the steady demand for the group's products is resilient and isn't as sensitive to the economic environment.

In May, I updated my assumptions after the company published its Q1-23 results, which were better than expected. Since I rated the stock a Buy, it lagged behind the market, something investors should expect when the market is bullish, as Nestle is considered a safe haven and is the embodiment of a stalwart.

Now, let's focus on the company's results, see how my projections fared compared to the consensus, and see if it remains an attractive dividend investment.

H1-23 Highlights

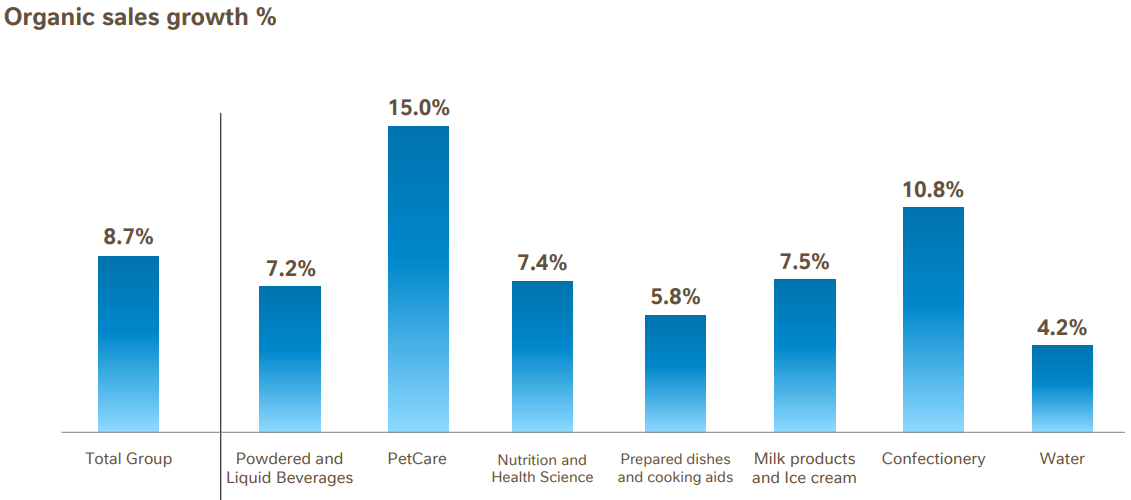

Nestle reported consolidated revenues of CHF 46.3B, a 1.6% increase from the prior year. Organic growth was 8.7%, reflecting currency and net divestitures impacts of 6.7% and 0.4%, respectively. Based on its historical seasonality, the Swiss conglomerate is on pace to deliver 7.5% organic growth for the entire year, right at the mid-point of management's updated guidance. Price increases amounted to 9.5%, which was offset by a 0.8% RIG decline, of which 60 bps were due to voluntary optimization.

{kind=link}

As we can see, growth was broad-based across categories, with PetCare and Confectionary once again leading the way, despite ongoing capacity constraints in PetCare. Water continued to lag, suffering from supply chain constraints in Perrier, which are projected to normalize by the end of the year.

{kind=link}

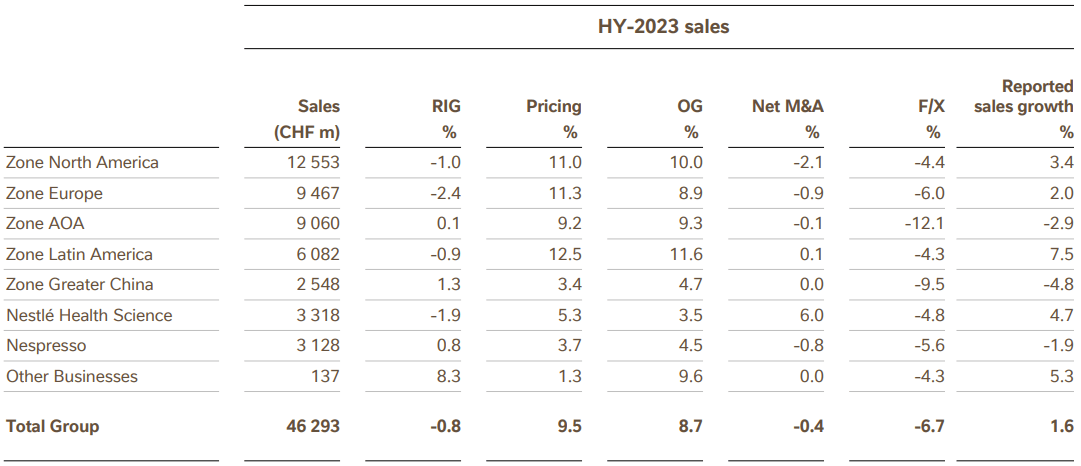

Looking at segments, we see that Latin America led organic growth with 11.6%, followed by North America with 10.0%. Looking at RIG, which represents the combination of price and mix, Nespresso, Greater China, Zone AOA, and Other Businesses came in positive, whereas Europe was the largest decliner at -2.4%. Overall, pricing contributed 9.5% to organic growth, but it was met with a weaker consumer, which resulted in slightly lower volumes and trade downs.

{kind=link}

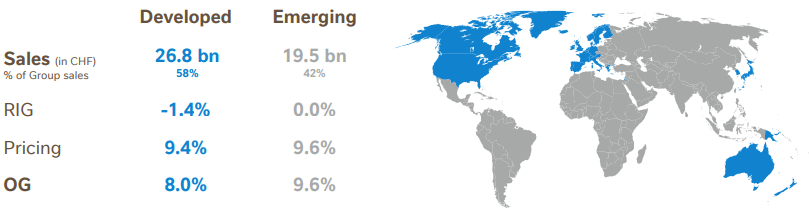

Emerging markets are becoming increasingly significant for Nestle, as it continues to gain market share, specifically with its more than 30 "billionaire brands" like Nespresso, Kit Kat, and Nesquik. Sales in emerging markets amounted to 42% of Nestle's total sales.

{kind=link}

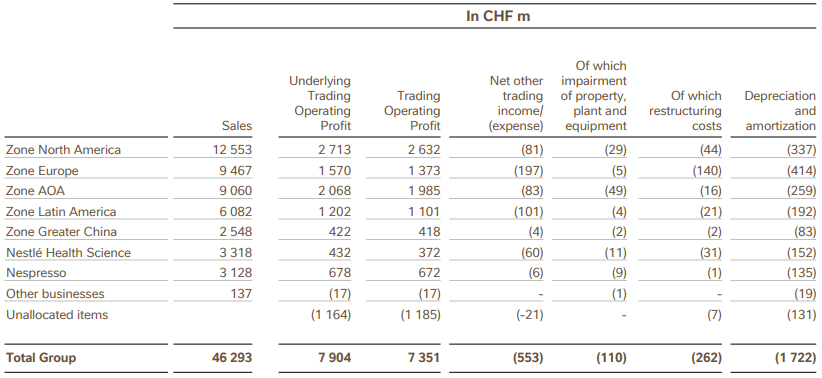

Looking at profitability, margins increased in 5 of 8 segments compared to 2022. The most notable improvement was in North America, as trading operating profit ((TOP)) margins reached 21.0%. Overall, TOP margins improved by 120 bps over the first half of 2022.

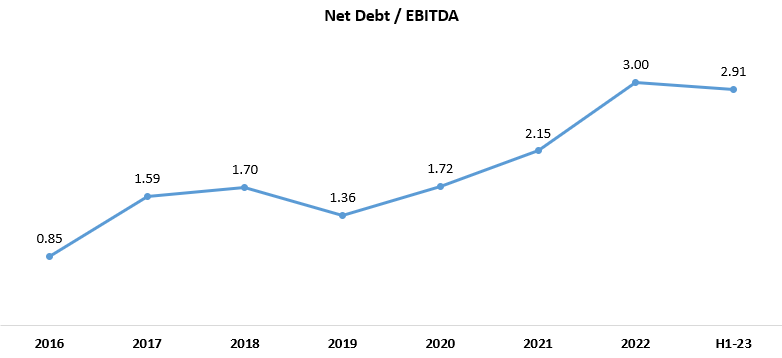

Created and calculated by the author based on Nestle financial reports; H1-23 net debt / EBITDA is based on my full-year 2023 EBITDA estimate.

{kind=link}

Transitioning to the balance sheet, Nestle's net debt increased once again, reaching CHF 55.2B, a 7.5B increase over the end of 2022. However, EBITDA is projected to increase significantly in 2023, so the Net Debt to EBITDA ratio is projected to decrease.

A significant portion of Nestle's debt was issued to finance buybacks, which made sense at a time of low-interest rates. However, as interest rates are rising, it seems less reasonable. Nestle still borrows at extremely low rates, with an average cost of debt of 2.6% up from 1.9% in the prior year. Still, I believe the company should put emphasis on deleveraging in the near term.

Bottom Line & Guidance

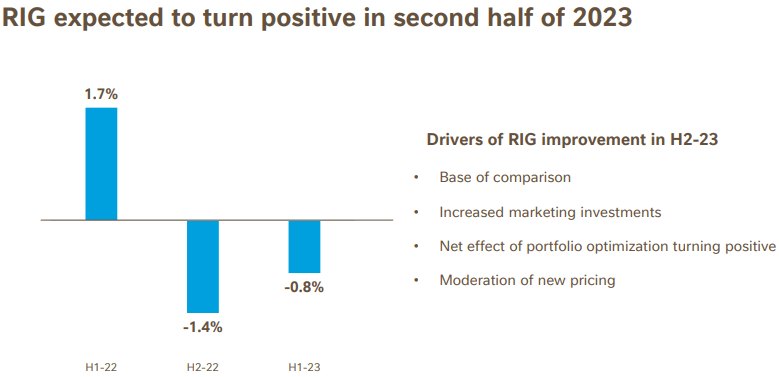

Overall, Nestle's strong results signal the company is on track with its optimization strategy, focusing on a smaller number of products, with higher growth and higher margins. According to the management, most of the negative RIG is a result of capacity constraints and optimization, as opposed to weakening demand.

{kind=link}

In the second half of 2023, management is expecting RIG to turn positive, primarily due to easier comparisons, increased marketing, and finally, positive contribution from optimization. Gross margin is expected to improve materially Y/Y. Furthermore, management reiterated its underlying EPS guidance for 8% growth at the midpoint and upgraded organic sales guidance to 7%-8% (from a prior 6%-8% range).

Important Notes From The Call

Very importantly, after several years of day-to-day crisis management, we have seen signs of further normalization in our operating environment in the first half. This allows us to be more strategic and more forward-looking in the way we manage our business. We're getting back to our proven virtuous circle of managing for steady and profitable growth.

--- Mark Schneider, Chief Executive Officer, H1-23 Earnings Call

To me, that's the most important statement that was made in the call. Finally, after several years of focusing on pandemic impacts, supply chains, lockdowns, commodity inflation, post-pandemic recovery, and the list goes on, we are nearing a point where Nestle returns to smooth sailing. And with a consumer staple stalwart, that's exactly what investors are looking for.

At-of-home consumption post-COVID has now normalized while out-of-home channels continue to see strong growth momentum with an organic growth rate twice as fast as a group average at 17.1%.

--- François-Xavier Roger, Chief Financial Officer, H1-23 Earnings Call

Adding more to the normalization signals, management is seeing at-home channels return to pre-pandemic trends. However, out-of-home channels are still enjoying the post-pandemic recovery, as pent-up demand is fueling higher out-of-home consumption.

At a time of significant inflation, it is relevant to look at the evolution of inventories as a percentage of sales rather than in absolute value terms. Inventory levels are starting to normalize following a temporary increase in the prior year linked to supply chain constraints. We expect this level to decrease at a faster pace in the second half of the year.

--- François-Xavier Roger, Chief Financial Officer, H1-23 Earnings Call

Another major topic point for Nestle was inventories. As we discussed in my previous articles, the company has built up inventories in order to sustain deliveries under a tough supply chain environment, which suffered from high freight rates, and commodity shortages caused by the Russia-Ukraine conflict.

I'm confirming, by the way, the fact that we expect to recover our gross margin to the level where it was before around 50%. I can't give you an exact timing for that. It will take some time, but the timing will depend on some external factors as well, but we are fully committed to that.

On the free cash flow, we expect this year to be around CHF10 billion of free cash flow. And I think that very quickly by 2025 at the latest, we should be around CHF12 billion, which means that we are well positioned in order to self-finance without any impact on our debt level both our dividend even going forward as well as share buyback.

--- François-Xavier Roger, Chief Financial Officer, H1-23 Earnings Call

Looking on a longer-term horizon, management reiterated its 50% gross margin target, and reaffirmed its focus on reducing its leverage, as it plans to self-finance future buybacks and dividends. Keep in mind that the company's leverage framework is to be in the 2-3 net debt to EBITDA range, so don't expect significant deleveraging. However, returning to the lower end of the range by the end of 2025 would be a positive sight in my view.

Valuation

In the May article, I provided my H1-23 projections for Nestle:

I now project H1-23 sales of CHF 48.0B, CHF 22.0B in gross profit, and CHF 6.1B in net income, all slightly higher than the consensus . Another important note for the near term is regarding cash flows. After knowingly increasing inventories in 2022 to prepare against possible constraints arising from the Russia-Ukraine war, Nestle should see elevated cash flows in 2023 as working capital decreases.

What I and the consensus didn't take into account is a 6.7% headwind from F/X. Without the F/X impact, Nestle came ahead of all of my projections. From now on, I'll provide projections referring to organic measures.

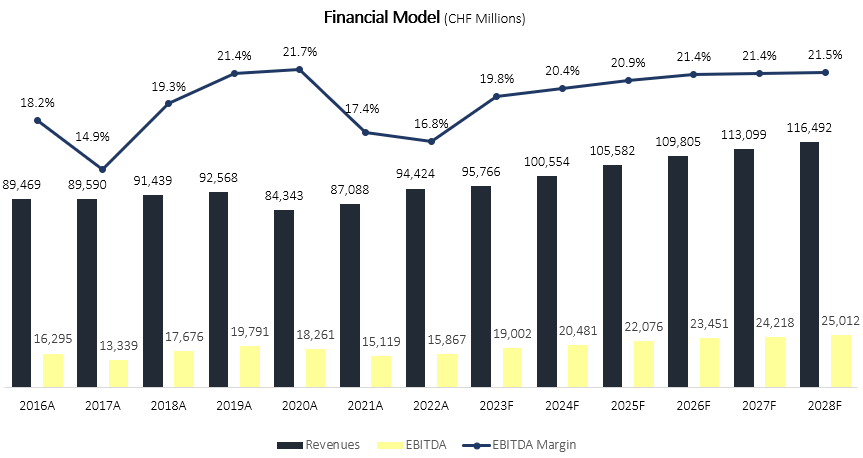

For the long term, I still project Nestle will grow revenues at a 4.0% CAGR between 2023-2028, which is at the low end of the company's long-term guidance for organic growth. I believe revenues will grow at this above-industry pace due to Nestle's significant investments in capacity enhancements, and shift in focus to faster-growing brands.

I project EBITDA margins will increase incrementally up to 21.5%, which is in line with the company's 2019 level, primarily due to better gross margins as a result of a better mix, and easing cost inflation. This results in an EBITDA CAGR of 5.7% between 2023-2028, reflecting operational leverage.

Created and calculated by the author based on Nestle financial reports and the author's projections

{kind=link}

Taking a WACC of 6.9%, I estimate Nestle's fair value at CHF 120 per share or $138 per ADR, based on the current CHF / USD rate. This reflects a 23.2x P/E ratio based on my projected 2024 EPS, which in my view, is a fair valuation for Nestle.

Conclusion

If you're looking for an exciting investment, then you came to the wrong place. Nestle is the definition of a stalwart. What you can expect from Nestle is steady growth, limited volatility, and consecutive dividend payments that will probably continue as long as humankind continues to eat and drink. Even with stalwarts, there could be significant upside. As Nestle is in the midst of a turnaround, which should lead to a material increase in margins and accelerated growth in the near term, I believe now is a great time to increase exposure to the staple giant. Thus, I reiterate Nestle stock as a Buy.

For further details see:

Nestle: H1 2023 Results Are Out, Optimization Is On Track