NSRGY - Nestle: Mediocre Q3-23 Downgrading To Hold

2023-10-20 13:39:01 ET

Summary

- Nestlé reported lower-than-expected Q3-23 sales, with negative internal growth and moderating pricing contribution.

- The company is struggling to reignite revenue growth due to organic growth slowdown and foreign exchange headwinds.

- I am downgrading Nestlé to a Hold, awaiting higher certainty regarding margins and volume acceleration.

Nestlé ( NSRGY ) ( NSRGF ) reported lower-than-expected Q3-23 sales, as real internal growth ((RIG)) remained negative, and pricing moderated more than expected.

The Swiss conglomerate is struggling to reignite reported revenue growth, as organic growth slowed down in the quarter, and foreign exchange headwinds increased.

I am downgrading Nestlé to a Hold, awaiting higher certainty regarding margins and volume acceleration.

Underperformance Year-To-Date

I started covering Nestlé back in February, claiming its ' RIG Growth In 2022 Signals It's Time To Buy ', as I found the company's ability to grow volumes despite major price increases to be a representation of its strength in the staples category.

It's been a rough ride since, reflected by the stock's 10 percentage point underperformance compared to the S&P 500. In general, the consumer staples sector is completely out of favor this year, in light of a major tech rally and growing demand for weight loss drugs, which leads some market participants to believe global food consumption might decrease.

As we can see, Nestlé slightly outperformed the sector's index, however, it's important to remember we're looking at an ADR here, which is exposed to the USD/EUR exchange rate. Nestlé's actual shares, which are listed on Switzerland's stock exchange, actually trailed the staples index slightly.

By and large, I view the staples sector's retraction as reasonable amid higher rates. Starting with a relatively high P/E ratio and combined with the fact the companies within the index are generally slow growers, a decline was due.

That being said, many staples companies, including Nestlé, are now trading at more sensible valuations. So, let's dig deeper into Nestlé's third-quarter numbers and see where it stands.

9M-2023 Highlights

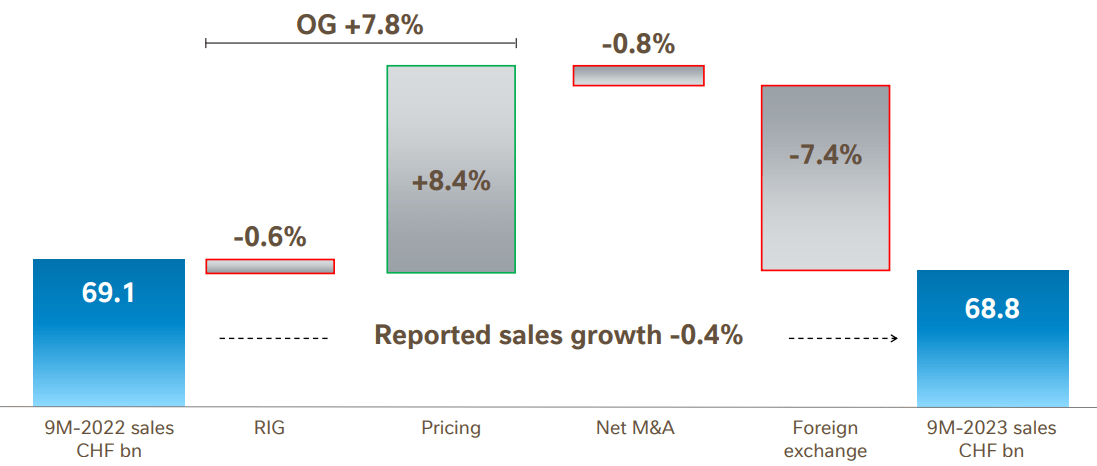

Nestlé reported consolidated revenues of CHF 68.8 billion for the first nine months of 2023, a 0.4% decrease compared to the prior year period. Looking at the third quarter by itself, reported sales decreased by 4.4% to CHF 22.5 billion.

{kind=link}

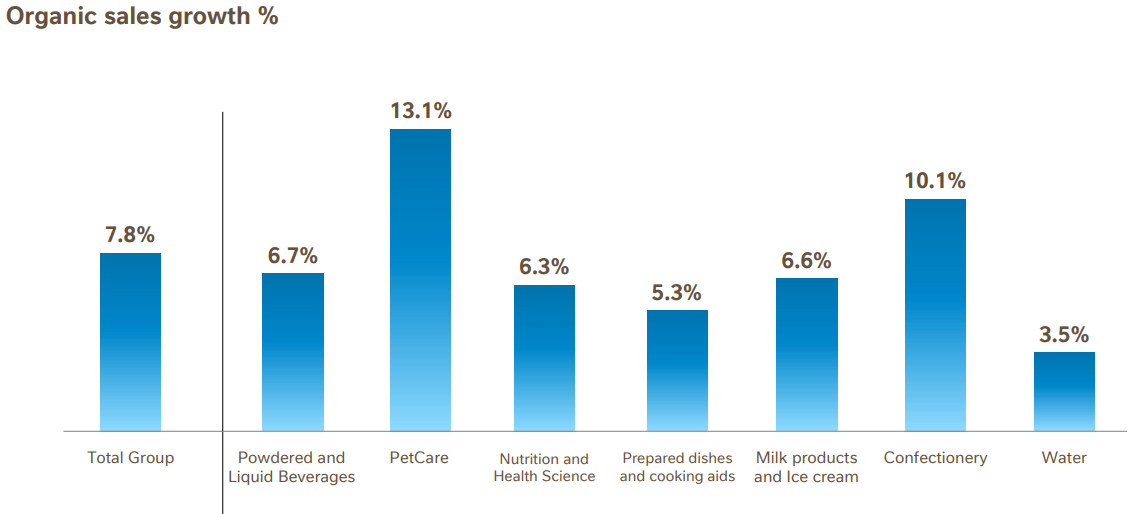

On a constant currency basis, Nestlé's nine-month revenues grew by 7.0%. Organic growth came in at 7.8%, as an 8.4% price contribution was offset by negative mix and volume, reflected in a 0.6% RIG decline.

{kind=link}

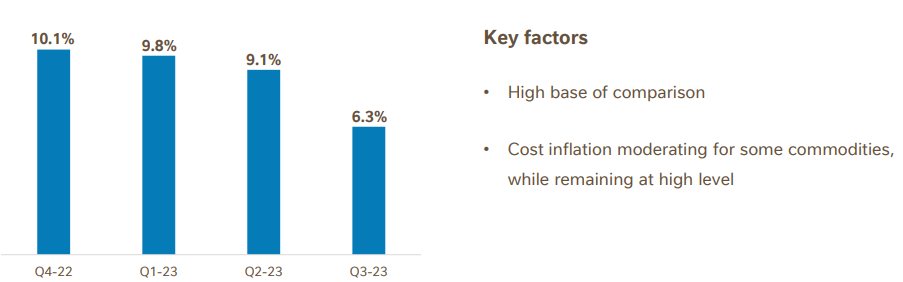

As we can see, growth was broad-based across categories, with PetCare and Confectionary continuing to lead the way. Of the seven categories, the only category that has seen growth accelerate in the third quarter is Water, with a notable deceleration from the first half in PetCare (15.7% to 13.1%), and Confectionery (13.5% to 10.1%). The deceleration comes as Nestlé's pricing actions are moderating, as we can see below:

{kind=link}

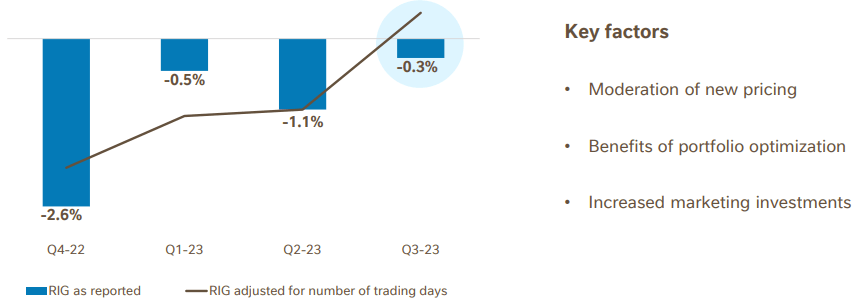

And while RIG is improving, it remains negative, and is far from offsetting the moderating pricing contribution, a trend that should continue into the fourth quarter, even though RIG is expected to turn positive.

{kind=link}

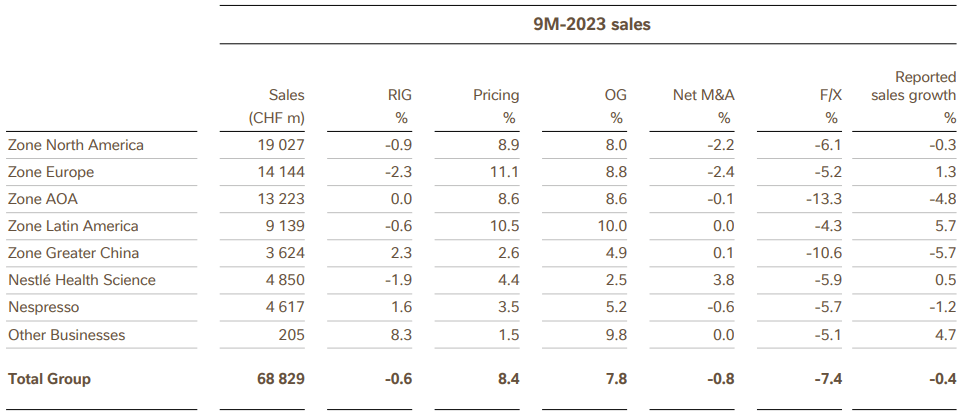

Looking at the company's reported segments, Latin America continues to lead growth, with organic growth and reported growth coming in at 10.0% and 5.7%, respectively. The only segments with positive RIG for the nine months were China, Nespresso, and Other, and the worst currency impact was in Zone AOA and Zone Greater China.

{kind=link}

Overall, Nestlé's results were mediocre. While FX headwinds are usually disregarded, they should be taken into account when investing in a global company, and it seems volatility in currencies is still ongoing.

Operationally, supply constraints are continuing and portfolio optimization is progressing. According to management, RIG in the third quarter would have been positive if adjusted for one less trading day. Still, while turning positive has its effect, RIG needs to increase to at least low-single-digits for Nestlé to sustain positive organic growth in 2024, as pricing actions are moderating.

In short, there are plenty of unknowns regarding the company's ability to improve GAAP margins and reported sales, which are, at the end of the day, the main drivers for the stock performance.

Important Notes

Nestlé confirmed its midterm objectives for its Health Science division, targeting high single-digit growth and underlying trading operating profit above 18% (reflecting a 7 percentage point margin improvement). The Health Science division was responsible for 7% of total sales in the first nine months of 2023, and a little over 5% of total trading operating profit in the first half. So, while it isn't the most important segment for Nestlé, a major improvement should be able to move the needle.

Management also reaffirmed its 2023 guidance, which at this point is nearly meaningless. Although organic and underlying numbers do reflect the true state of the business operations, they are significantly detached from the company's real financials. The difference between organic sales and reported sales is nearly CHF 6 billion for the first nine months of the year, and the difference between operating profit and underlying trading operating profit should be nearing CHF 1 billion.

Although they are not reporting P&L items in the third quarter, management confirmed that gross margins are continuing to progress toward historical rates, expecting a material improvement in the second half. However, as the company increases marketing spend, its interest expense rises, and FX continues to weigh on the top line, it could take another few quarters for a material bottom-line margin improvement.

Regarding GLP-1 weight loss drugs, management sees a minor potential effect, claiming less than 20% of its total sales are exposed to a decrease in global food consumption. Furthermore, they emphasized that GLP-1 solutions for weight loss aren't infinite and that sustaining a healthy diet would be essential even for those who consume the drugs constantly. In their view, any impact from GLP-1 will be more than offset by increased demand for nutrition supplements in Nestlé Health Science, as well as their nutritious foods categories.

Also in light of GLP-1, Nestlé stressed the importance of their long-term nutritious foods targets, which they announced at the end of September. In short, Nestlé aims to grow the sales of its more nutritious products by CHF 20-25 billion by 2030. This represents about 50% growth over 2022 sales.

Valuation

Nestlé is trading at a 22.0x P/E over 2023 consensus GAAP EPS estimates, and slightly below a 20.0x P/E over consensus underlying EPS estimates. As discussed above, there is a material detachment between reported and adjusted numbers, as FX continues to be a significant headwind. For comparison, the PE ratio of the staples index ( XLP ) stands at 22.6x.

So looking at multiples, we don't see an obvious attractive opportunity, as Nestlé is trading in line with the sector. While its business is arguably higher quality than some other participants, its growth potential is relatively low, considering it's the largest consumer staple company in the world, in terms of sales.

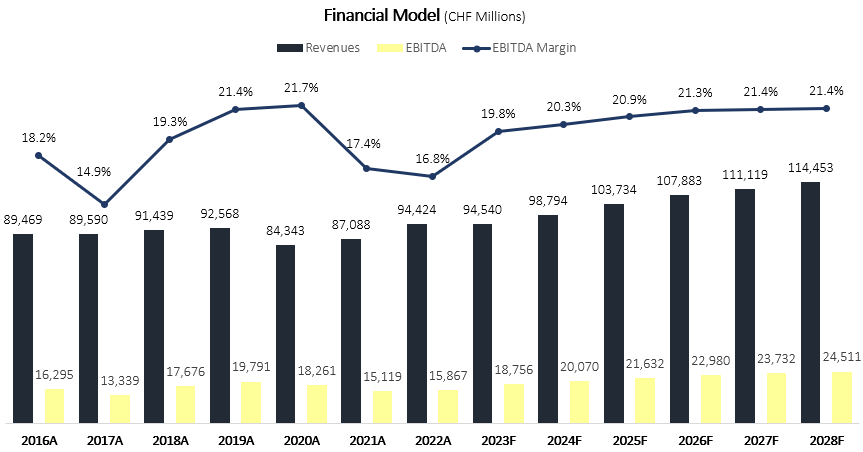

Created and calculated by the author based on Nestle financial reports and the author's projections

{kind=link}

Looking at my long-term financial model for Nestlé, which hasn't changed materially from the previous quarter, I see no room for major upside as well. As WACC increased to 7.2% due to higher rates, I estimate the company's fair value at CHF 104 per share, or $110 per ADR, reflecting an underwhelming 5% upside.

Conclusion

Nestlé is the definition of a stalwart. Nestlé provides resiliency, limited volatility, and consecutive dividend payments that will probably continue as long as humankind continues to eat and drink. On the other hand, its growth opportunities are quite limited by its sheer size and the overall staple market trends.

Unlike other sectors or smaller businesses, stocks like Nestlé have a hard time offsetting higher rates with the company's performance, as their steady slow-growing operations aren't able to outgrow the WACC drag.

While Nestlé should continue to improve fundamentally, as its portfolio optimization materializes and supply chain constraints ease, I believe the gross margin improvements and low-single-digit growth won't be enough to provide market-beating returns based on the current valuation.

Therefore, I downgrade Nestlé to a Hold.

For further details see:

Nestle: Mediocre Q3-23, Downgrading To Hold