OPI - Net Lease Office Properties: A First Look At The W. P. Carey Spin-Off

2023-11-13 12:30:52 ET

Summary

- W. P. Carey's spin-off of Net Lease Office Properties has destroyed shareholder value for WPC and left long-term investors scarred.

- WPC shareholders are now proud recipients of a bouncing baby called NLOP.

- We examine the setup for NLOP and estimate a starting FFO multiple.

When we last covered W. P. Carey Inc. ( WPC ) we gave our take on the horrendously executed spin-off.

WPC will likely trade between $55-$60 in the near future. We are lowering our fair value here to $55 as WPC has destroyed shareholder value by this transaction. We would use a bounce to sell calls on positions if you don't already have them in place.

Source: The Spin-Off And The Spin

That spin-off left long-term investors scarred and gave us the listing of Net Lease Office Properties ( NLOP ). Of course, investors have now inherited these shares and are wondering what to do with them. Let's look at the portfolio and the balance sheet and see if this is a keeper.

The Portfolio

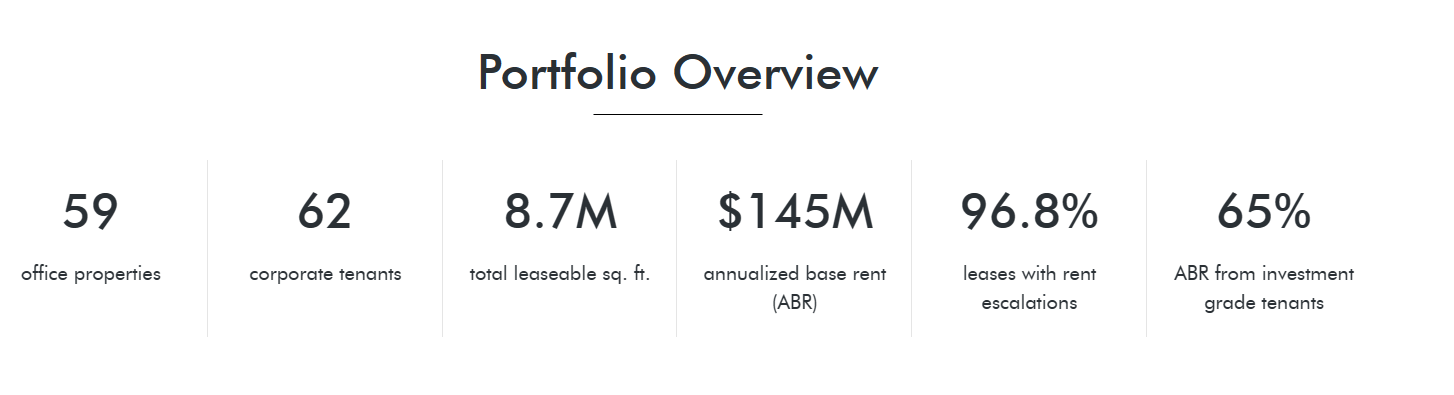

The great part about this spin-off is that you don't even have to wonder how much of the property portfolio is in the office. The NLOP name gives you a big clue. The current portfolio comprises of 59 office properties with some tenants sharing a building, giving us 62 tenants in total. As is typical with such leases, almost all of them have some form of rent escalations.

{kind=link}

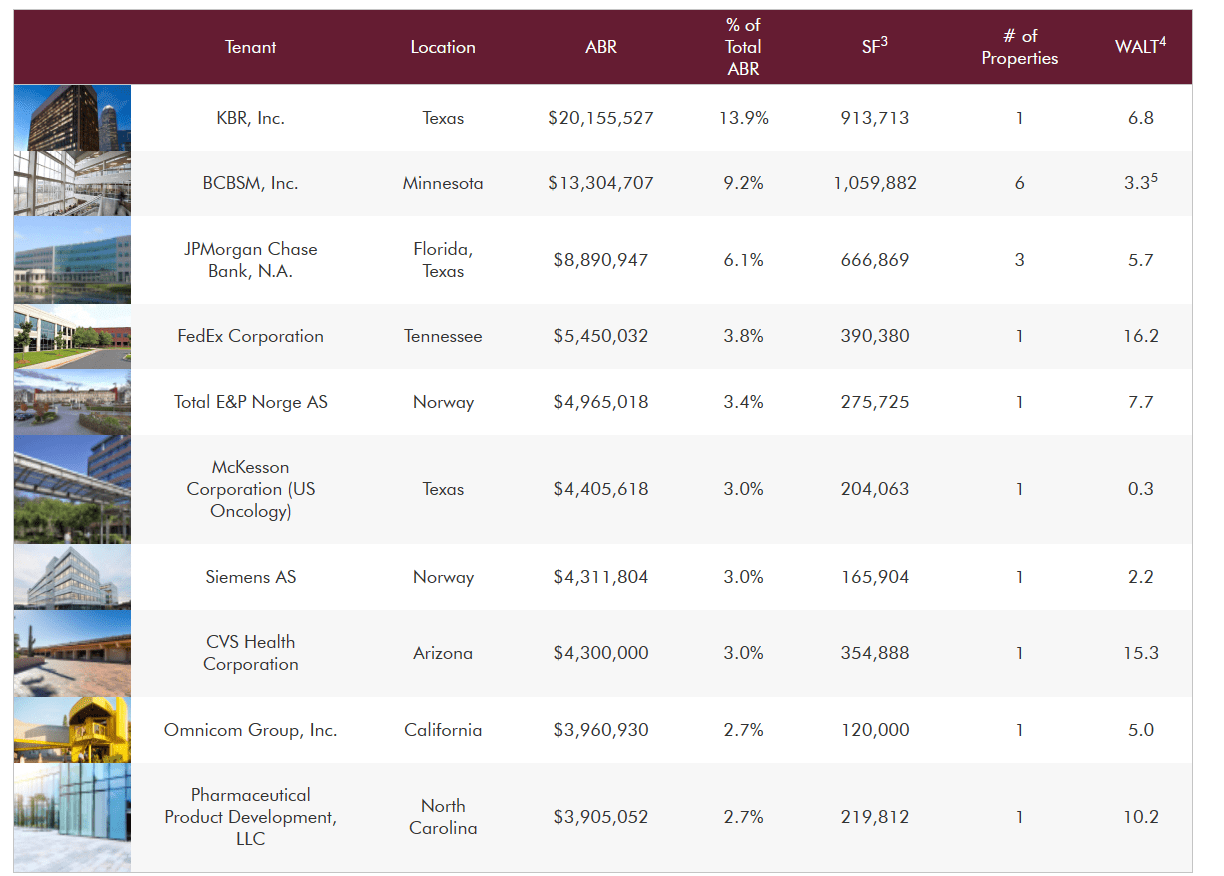

NLOP does mention that almost two-thirds of the total adjusted base rent comes from investment-grade tenants. You can indirectly gauge this also from their top tenants' list which is made up of many household names like KBR, Inc. ( KBR ), JPMorgan Chase & Co. ( JPM ), FedEx Corporation ( FDX ), and CVS Health Corporation ( CVS ).

{kind=link}

We will take the opportunity once more to reiterate that that is the most useless piece of information today. NLOP of course hopes to imply this reflects quality, but it does not. If anything, it might imply the opposite as these tenants have high negotiating power and are being wooed by countless other real estate brokers to fill in an empty space.

WPC was and still is, a global behemoth. NLOP's portfolio is a bit more local and 90% is within the US and three European destinations make up the remaining.

NLOP Website

So currency won't be as big a factor as it was for WPC. On a sector level, the REIT has tenants from every possible area with construction and engineering taking the top spot.

NLOP Website

The Setup

As you decide whether you want to hold or fold on NLOP, you have to first see how the balance sheet is structured. WPC wanted to make sure they extracted a last pound of flesh before sending this off into the wilderness. The rationale was that unless they unloaded some significant debt along with the lost office rent, their credit metrics would worsen. So NLOP was set up with this.

1) Existing mortgage debt attached to certain of the Office Properties, in an aggregate amount of $168.5 million as of June 30, 2023.

2) The $335.0 million NLOP Mortgage Loan, which is secured by first priority mortgages and deeds of trust encumbering the interests of the NLOP Mortgage Loan Borrowers in the Mortgaged Properties and by pledges of equity of the NLOP Mortgage Loan Borrowers (and, with respect to the NLOP Mortgage Loan Borrowers that are limited partnerships, the general partners thereof), NLO Holding Company LLC, and each of NLO MB TRS LLC and NLO SubREIT LLC.

3) The $120.0 million NLOP Mezzanine Loan entered into between the NLOP Mezzanine Borrower and the Lenders.

Source: 8-K (lightly edited for clarity) .

So that works out to $623.5 million and that would leave WPC with about $55 million in cash on the balance sheet. So net debt would be close to $570 million. The mortgage debt, like all of WPC's debt, has a rather brisk maturity profile and as shown below, all of it comes due by 2026.

{kind=link}

While the mortgage debt has a short maturity, the interest rates on that are rather small for now. The non-mortgage debt on the other hand (see 2 and 3 above) comes with rather incredible costs. WPC management's value destruction can be seen in the next paragraph.

We will incur an estimated $23.2 million of origination fees. For purposes of preparing the unaudited pro forma condensed combined statements of income, we have calculated interest expense using the effective interest method and the rate as specified in the Financing Arrangements, which resulted in an effective interest rate of approximately 14.9% , factoring in the defined loan principal repayment (which requires a payment of 15% and 25% during the first two years of the loan term). The stated interest rate is based on the adjusted 87 one-month Term SOFR rate as of September 18, 2023, of 5.32%, plus an assumed applicable margin of 5.0%

Source: 8-K.

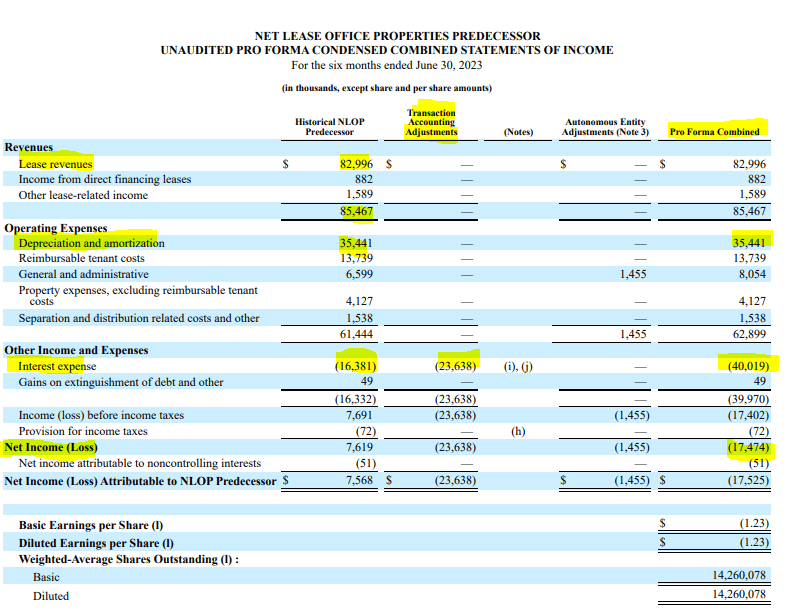

At 14.9% we have to wonder why did they even bother with this kind of a loan. Probably because getting a 21% interest rate credit card would have looked ridiculous. This impact will be quite significant as we look at the potential for funds from operations (FFO) from the new company. You can see below the predecessor assets and liabilities of NLOP had just $16.38 million of interest expense for the first half of 2023. This would jump to $40.02 million under new debt arrangements.

{kind=link}

While we have highlighted the negative net income, do note that if you add back the depreciation you get to about $18 million in FFO, which annualizes to $36 million. So that gets us to a starting price to FFO of 6.

Verdict

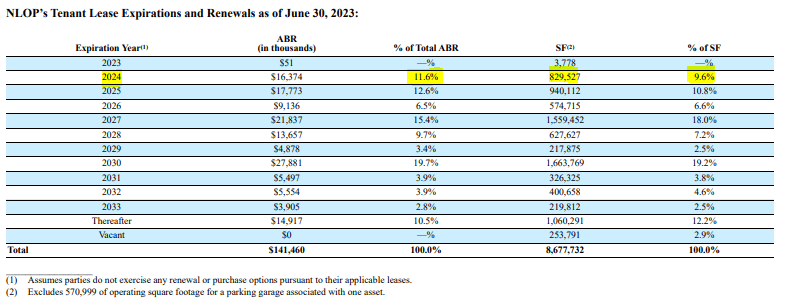

On the other side of the ledger is just how quickly will the existing leases expire. 2024 will see about 9.6% come up for renewal.

{kind=link}

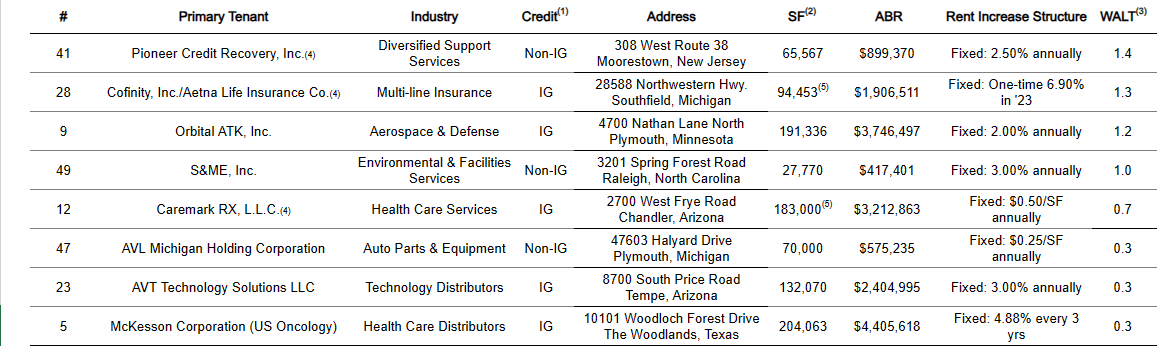

Lease maturities look manageable until you get to 2027. That does give them some breathing room. Digging a little deeper, we can see the specific properties that are coming up for renewal soon and their fate will show just exactly how much quality was there in the WPC office portfolio.

{kind=link}

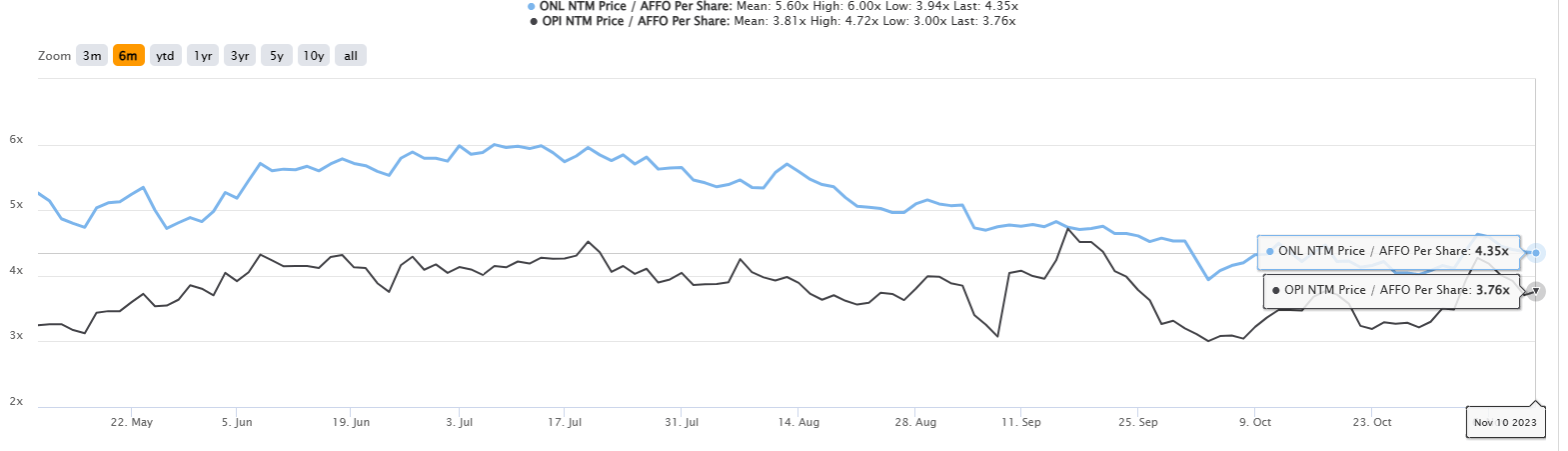

With $36 million of FFO, the total debt would require 15.6 years to be paid down completely. Of course, that is extremely simplistic as it ignores the fact that all leases may not be renewed. Even the ones that are renewed might require some massive capex and investments. Whatever the final outcome, we believe this would have been best done under the umbrella of WPC and not as a standalone entity. We would caution investors against being lured into the idea that the price to FFO of 6 is cheap. If you don't believe us, feast your eyes on the multiples of the other two single-tenant office REITs, Orion Office REIT Inc. ( ONL ) and Office Properties Income Trust ( OPI ) are trading at.

{kind=link}

We rate NLOP a hold and we have a few shares courtesy of the spin-off. Those are attached to special covered calls sold prior to the spin-off, so we are holding the shares to keep them covered. But there is no real risk of a runaway move here and we might sell these down the line.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Net Lease Office Properties: A First Look At The W. P. Carey Spin-Off