EPRT - Net Lease REITs: Holding Off Until Cap Rates Stabilize

2023-10-20 13:40:33 ET

Summary

- It takes nine months (0.74 R-Squared) for interest rates to impact private real estate valuations. This mismatch between public and private valuations inhibits net lease REITs' ability to acquire accretively.

- Recent increase in interest rates indicates cap rates will expand by +73bps over the next nine months despite management commentary of stabilization on 2Q23 earnings calls.

- I'm holding off on buying net lease REIT shares until interest rates truly plateau for a period of at least nine months.

Unlike publicly traded net lease REITs that have their cost of capital marked-to-market more or less on a daily basis, private net lease real estate markets take significantly longer for their valuations to adjust to prevailing interest rates. This results in a mismatch where publicly traded net lease REITs see their cost of capital adjust to prevailing interest rates far sooner than the private real estate markets that they acquire assets in. This can lead to a "lag period" where publicly traded net lease REITs need to wait for private market valuations to catch up to public market valuations, so they can resume acquiring assets in earnest with an adequate "investment spread" to their cost of capital.

Historically, the end of this "lag period" presents an opportune time for investors to buy the shares of net lease REITs at rock bottom valuations just as public net lease REITs are able to turn on their external growth engines. This low valuation coincident with strong earnings growth typically leads to above average near- to medium-term returns for shareholders.

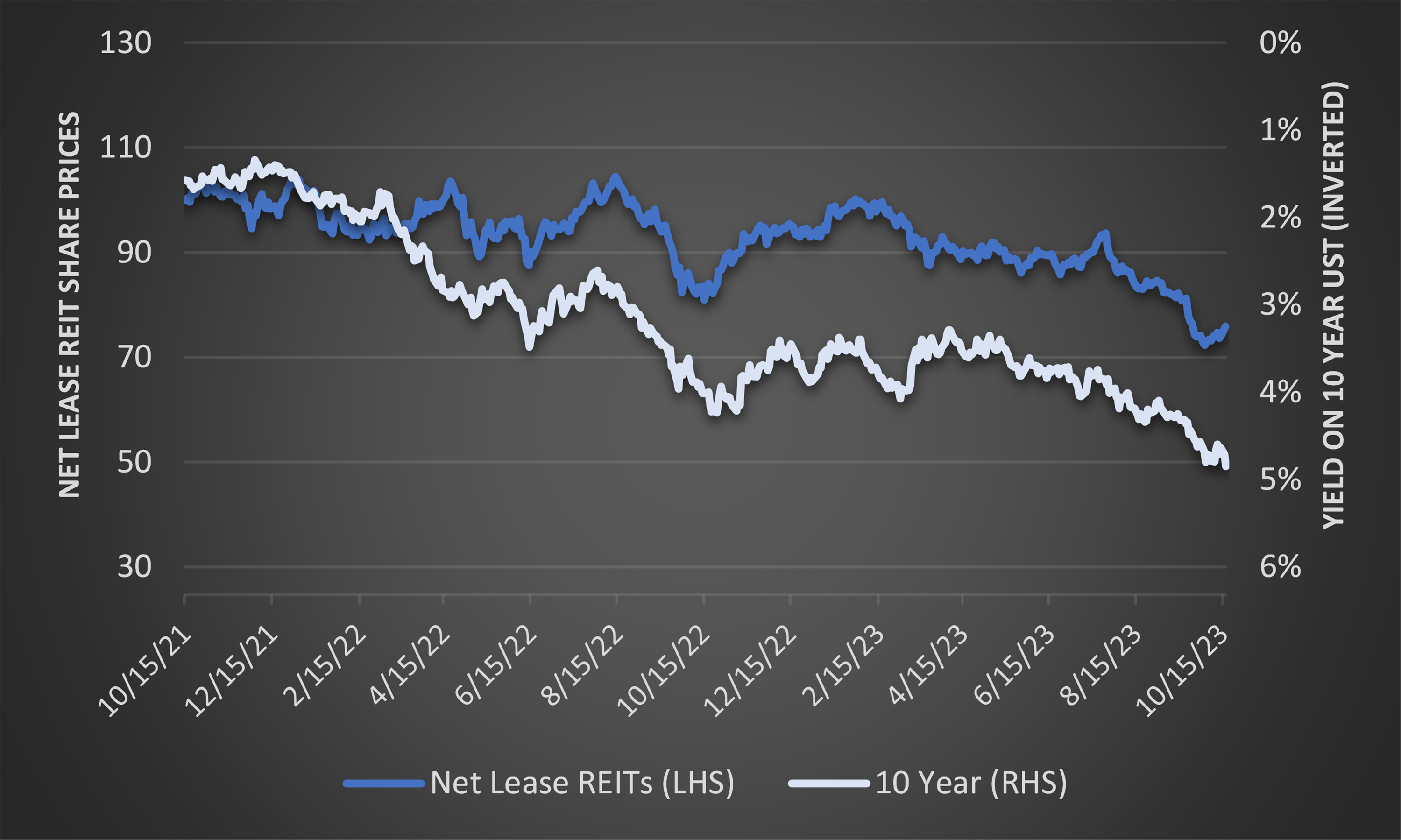

Looking at the past two years, net lease REITs (O, WPC, NNN, EPRT, ADC, SRC) have seen their share prices decline by -24% on average as yields on 10-year US Treasuries have surged +341bps from 1.6% in October 2021 to 5.0% currently.

{kind=link}

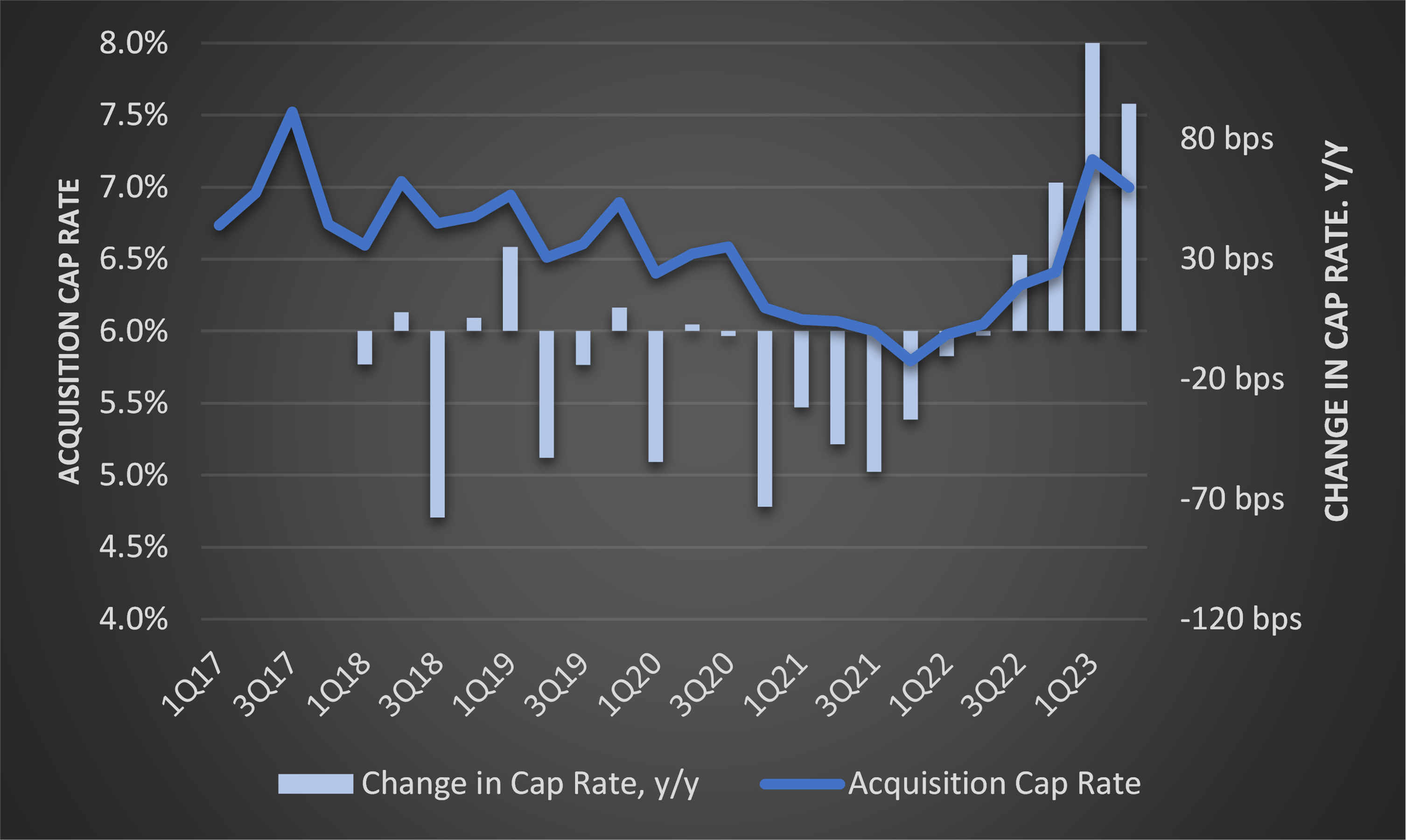

Taking the weighted average cap rate on acquisitions for the public net lease REITs (O, NTST, WPC, NNN, EPRT, ADC, SRC) shows that acquisition cap rates started expanding on a y/y basis in 3Q22 and finally got above 7% in 2023. Net lease REIT management teams have indicated on prior earnings' calls that starting at the beginning of this year they finally began to see sellers come back to the market willing to accept higher cap rates that are more in line with the current higher interest rate environment.

{kind=link}

However, listening to the public net lease REITs' most recent 2Q23 earnings calls indicates what appears to be a consensus view among net lease REIT management teams that cap rates may rise some from current levels, but that most of the increase in private market cap rates are behind us. Net lease management teams used the words like "stabilized", "plateau" and "leveled off" in unison to describe their current outlook on private market cap rates.

Realty Income ( O ) 2Q23 Earnings Call : " Cap rates in our acquisitions appear to have stabilized after a meaningful adjustment period to a higher interest rate environment.

Spirit Realty ( SRC ) 2Q23 Earnings Call : " I'd say that they're pretty stable right now." - referring to cap rate levels.

NNN REIT ( NNN ) 2Q23 Earnings Call : " With regard to the acquisition pricing environment, as I mentioned in the May call, we are seeing that cap rate increases started to plateau and stabilize ."

NETSTREIT Corp. ( NTST ) 2Q23 Earnings Call : " From a pricing perspective. While we believe cap rates have largely leveled off for assets that we pursue…"

Essential Properties Realty Trust ( EPRT ) 2Q23 Earnings Call : " But generally, the market is pretty stable , and I would expect cap rates to kind of be in that mid-7% range in the back half of the year."

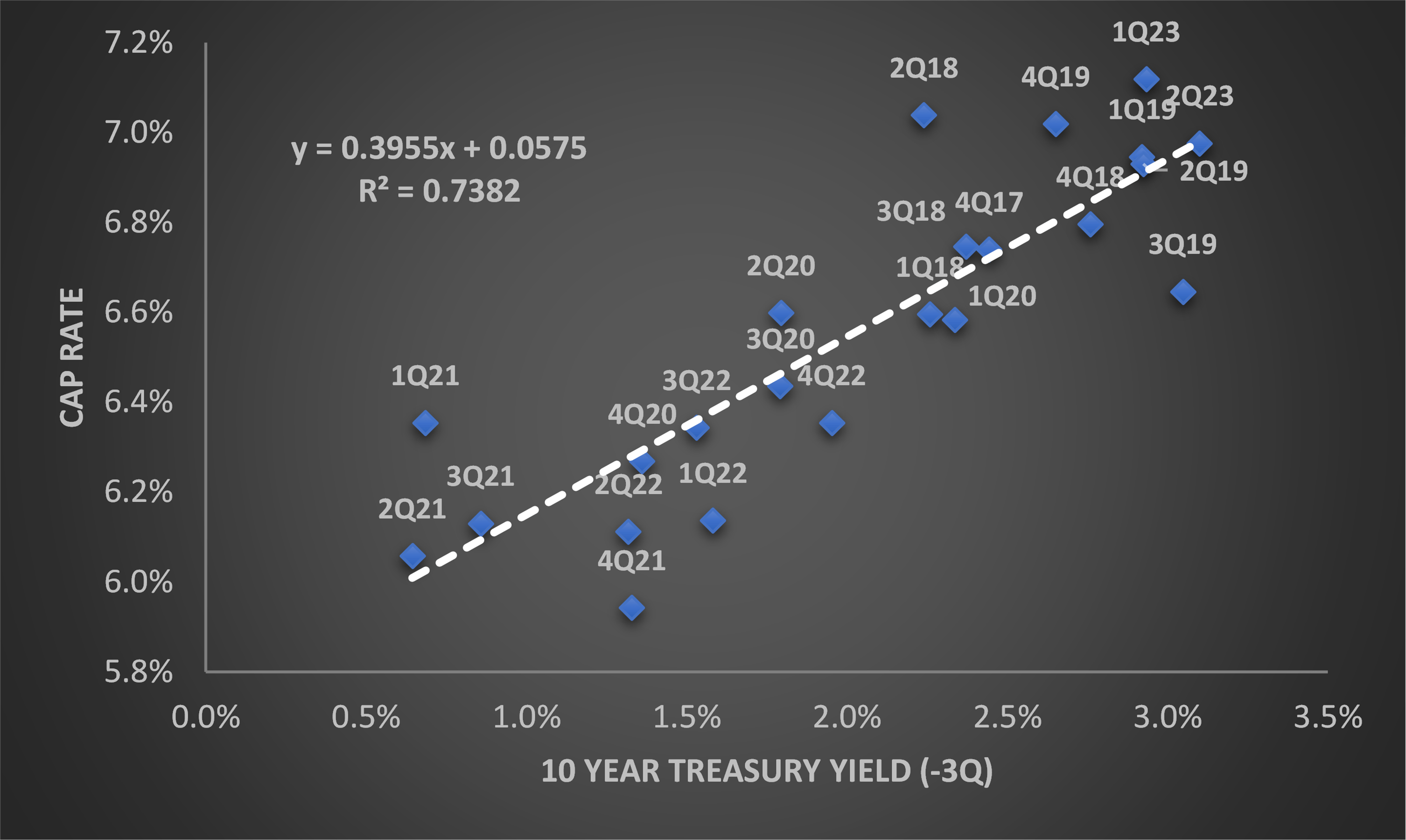

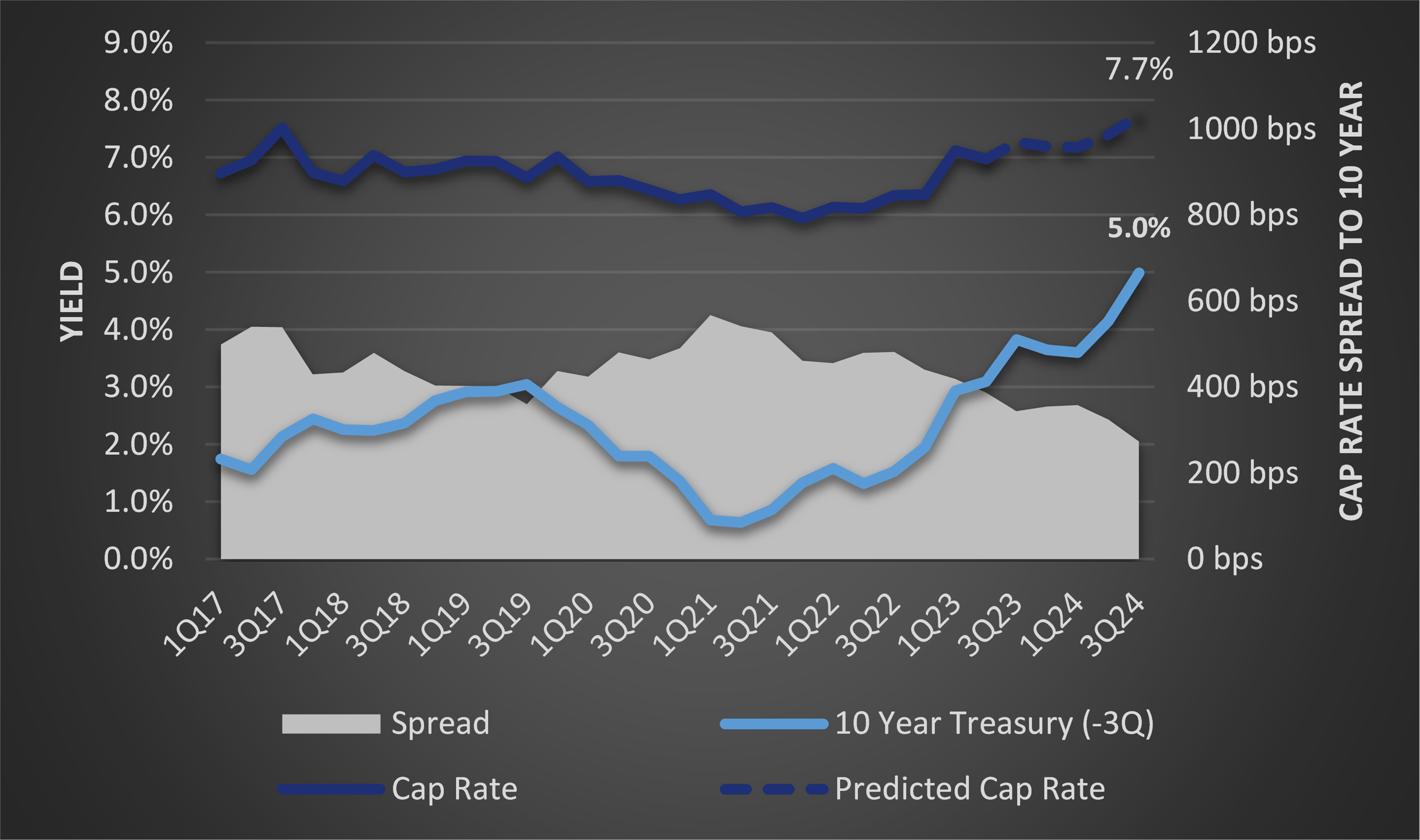

While Realty Income cites in its current investor presentation that since 1996, the company has noticed a 12-month lag period for acquisition cap rates to adjust to changing interest rates when running a regression on quarterly data since 1Q19, I found the highest R-squared (i.e., the coefficient of determination) of 0.74 when lagging interest rates by three quarters indicating that it is currently taking three quarters (i.e., nine months) for public net lease REITs' acquisition cap rates to adjust to prevailing interest rates.

{kind=link}

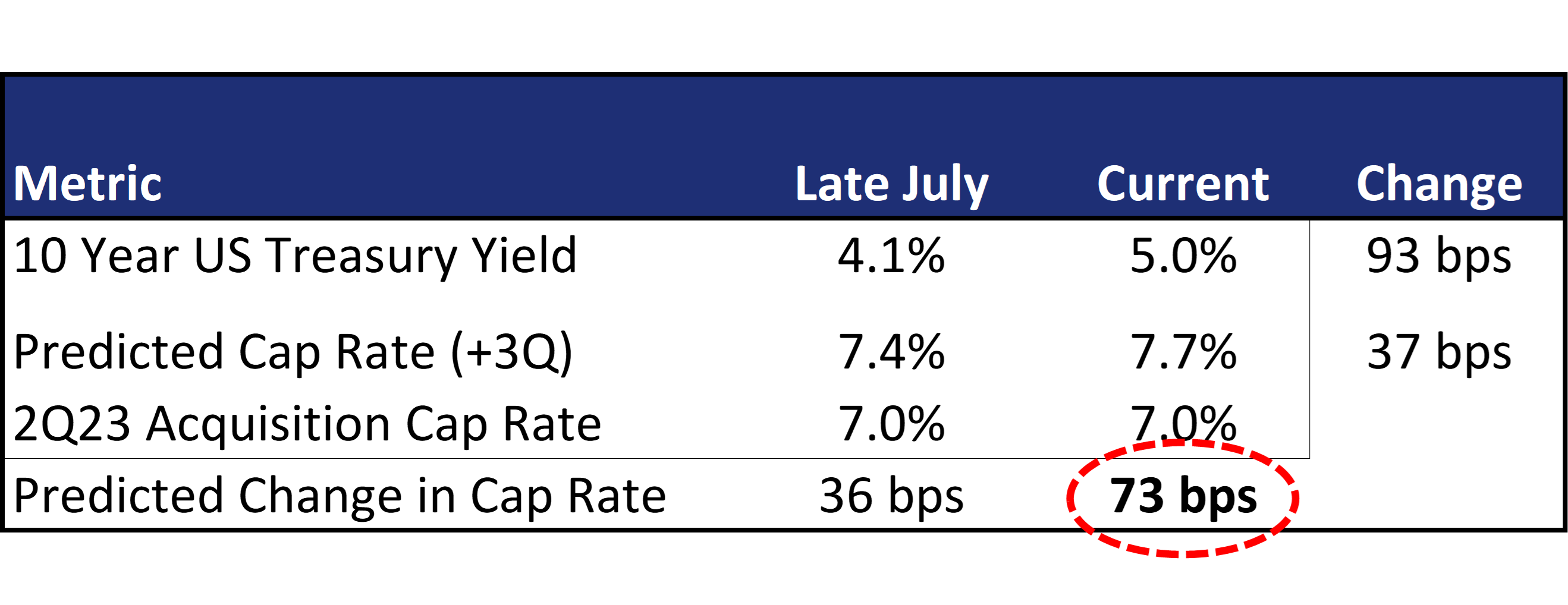

The value of this regression going forward, is that investors should be able to predict with fairly good accuracy what the level of acquisition cap rates will be in approximately nine months from now. When net lease REITs had their 2Q23 earnings calls in late July of this year, 10-year US Treasuries were yielding approximately 4.1% which utilizing the aforementioned regression formula would indicate cap rates nine months from now of approximately 7.4%, representing cap rate expansion over the next nine months of +36bps relative to 2Q23 levels of 7.0% (largely aligning with management commentary on 2Q23 earnings calls).

{kind=link}

However, given the recent increase in 10-year US Treasury yields to its current 5.0% level, the regression would indicate that if interest rates stay at their current high level, that cap rates could increase to as high as 7.7% in 3Q24 (9 months from now). Putting this into perspective, while REITs acquired assets at a 7.0% yield in 2Q23, current interest rates would indicate that assets of similar quality will be selling at 7.7% in 3Q24.

Converting the cap rates to actual real estate prices, a +73bps cap rates expansion would represent a -9.5% decline in real estate prices. Meaning net lease REITs should be able to acquire assets of similar quality to 2Q23 acquisitions for -9.5% less in the third quarter of next year.

{kind=link}

After listening to management commentary that cap rates are leveling off and stabilizing on the net lease REITs 2Q23 earnings calls, I became more constructive and started adding exposure to net lease REITs. However, the recent increase in 10-year US Treasury yields has me more cautious.

In my view the absolute level of cap rates is less important than the investment spread that net lease REITs can achieve when acquiring real estate assets. For this to occur I believe we need to see at least nine months of stable interest rate levels for public net lease REITs and private net lease real estate markets to be on the same page in terms of asset valuations, representing what I see as the opportune to time to buy the shares of public net lease REITs. From here I am looking forward to the public net lease REITs upcoming 3Q23 earnings calls to see if management teams change their tenor in terms of cap rate expectations going forward.

For further details see:

Net Lease REITs: Holding Off Until Cap Rates Stabilize