NTES - NetEase: A Good Deal At This Price Point

2023-07-15 05:12:45 ET

Summary

- Chinese video game company NetEase has a lot of potential for future growth in the mobile gaming industry.

- Solid financials also confirm that the company is being operated very commendably.

- NetEase's success in mobile gaming and its potential for innovation make it a promising long-term investment.

Investment Thesis

Over the last month, I have been playing Diablo Immortal and I noticed how I am enjoying it without the need to spend money so far. I wanted to dig deeper into NetEase’s ( NTES ) financials and see if there is a lot of potential for future growth in the form of collaborations with more major studios or their game developments. With what I consider to be quite conservative estimates for the company’s revenue growth, the company is a good buy at these prices with a lot of potential from the mobile gaming industry for many years to come.

Outlook

I know that Activision Blizzard ( ATVI ) would be raking in the most from Diablo Immortal, but this showed me that NetEase is very capable of making a decent-looking mobile game, although plagued with predatory microtransactions, however, for a casual mobile gamer like me, who would only play mobile games when there is no other substitute and I'm not home, I got a lot of enjoyment from Diablo Immortal without the need of spending thousands of dollars, and there are many people like me. So, let’s take a look at what is in store for the company.

The company is going the right route to make money. The mobile gaming industry is bigger than PC and Console gaming combined and is projected to grow strongly in the future. Casual games are where the money is at. Casual gamers are dominating the industry because these types of games are very accessible. I know so many people in their late 40s who are on the 1120 th level of Candy Crush or are popping some colorful bubbles. Mobile gaming is addictive, easy to get into, and fun enough to keep a person entertained while commuting, waiting for an appointment, or just plain bored.

I am not home currently so my gaming is limited to mobile for now or the occasional remote play, but I found myself enjoying Diablo Immortal quite a bit even if I don't spend money on it. That game, although universally hated, was a hit for Activision and NetEase and is very profitable for both parties. Unfortunately, the contract between the two companies could not be renegotiated, so the 14-year partnership was concluded in January of 2023, however, Diablo Immortal is under a separate agreement so that is still on the table. The company said that the end of the agreement is not material to the company, so let’s look at what looks promising in my opinion.

The company seems to have nailed mobile gaming, and that is why it is making around 72% of total revenues from mobile games. Eggy Party seems to me to be the most promising game out of the bunch. It is colorful, vibrant, and very easy to get into. Of course, it has a lot of microtransactions, but I don't think it's going to affect a casual gamer too much. The company saw a lot of engagement in the game, with people creating their maps to play on and teaming up with a few other friends to play team games. It is very similar in style to Fall Guys and that is a good thing. On release, it became the No. 1 downloaded application in China on iOS, so it seems that it is resonating with the casual gamer quite a bit. If the company can keep updating the game for a long time, I can see this becoming huge in the future and retaining a decent audience.

What caught my attention in the presentation is that Justice MMO mobile is going to be using machine learning to develop and enhance the game in the future. I'm a little skeptical of this idea, as I think the end product will not have much soul. I also think that MMO games are not as casual as Eggy Party, and I believe that it will be harder to obtain a large, consistent audience. I do have to say that the game looks really good on mobile and the MMO market size is expected to grow at 10.5% CAGR until ‘28 . That is still very impressive, however, I don’t know what kind of growth mobile MMO games will experience.

Another one I’m not too excited about but I’m sure it’s subjective, is Badlanders. I think battle royale games have overstayed their welcome. Call of Duty Mobile was a massive success in mobile gaming. Apex Legends Mobile not so much. Fortnite and PUBG mobile are also still very popular and are generating billions in revenue, so I don’t know how Badlanders will manage to take market share from these juggernauts of the industry.

I also think that Racing Master will do quite well in the genre as there aren’t many good ones out there besides Asphalt and some older titles, so a fresh racing game will do well in my opinion. Probably not as well as Mario Kart Tour but decent enough.

And how can we forget about the wizard kid and the associated games? There is a large following for the franchise and with the release of Hogwarts Legacy, the resurgence of fans was big. Naturally, a mobile game in my opinion will deliver results, and Harry Potter: Magic Awakened already made over $350m as of October ’22.

There will always be new things to release on mobile and NetEase has plenty of opportunity to cash in. If it can keep making quality games like Eggy Party and other engaging casual games, the revenue will never dry out.

The Risks

The games above might not live up to the expectations and the company would have to go back to the drawing board. Games always do well during the launch days or weeks, however, a lot of them see the player base plummet because the games are not engaging enough to keep the casual player interested. The company would need to find a good balance in what type of microtransactions to include in these games. Cosmetics are never an issue would, however, if the in-app purchases give a player an upper hand in the game then this may deter a lot of players.

Collaborations might dry out in the future, which may impact revenues if the games were very successful. I'm sure the loss of Blizzard Entertainment has put a damper on revenue potential. If the company breaches agreements with other licensing partners like Marvel or Warner Bros this could impact their revenues significantly.

Financials

The following graphs will be as of FY22 and all in US dollars. Figures may differ slightly from the company’s financial reports because I took the information from a third-party website that compiles annual data, so the FX rate used might be slightly different but in the ballpark.

As of FY22, the company had around $3.5B in cash and $13B in short-term investments, which brings the company’s total liquidity to a whopping $16.5B against $524m in long-term debt and 3.4B in short-term debt. That is a great position to be in. So little debt means that annual interest expense on debt is negligible because the interest the company gets from its short-term investments is much higher. The company has a lot of freedom to keep expanding and experimenting to see what they can come up with for the next big hit.

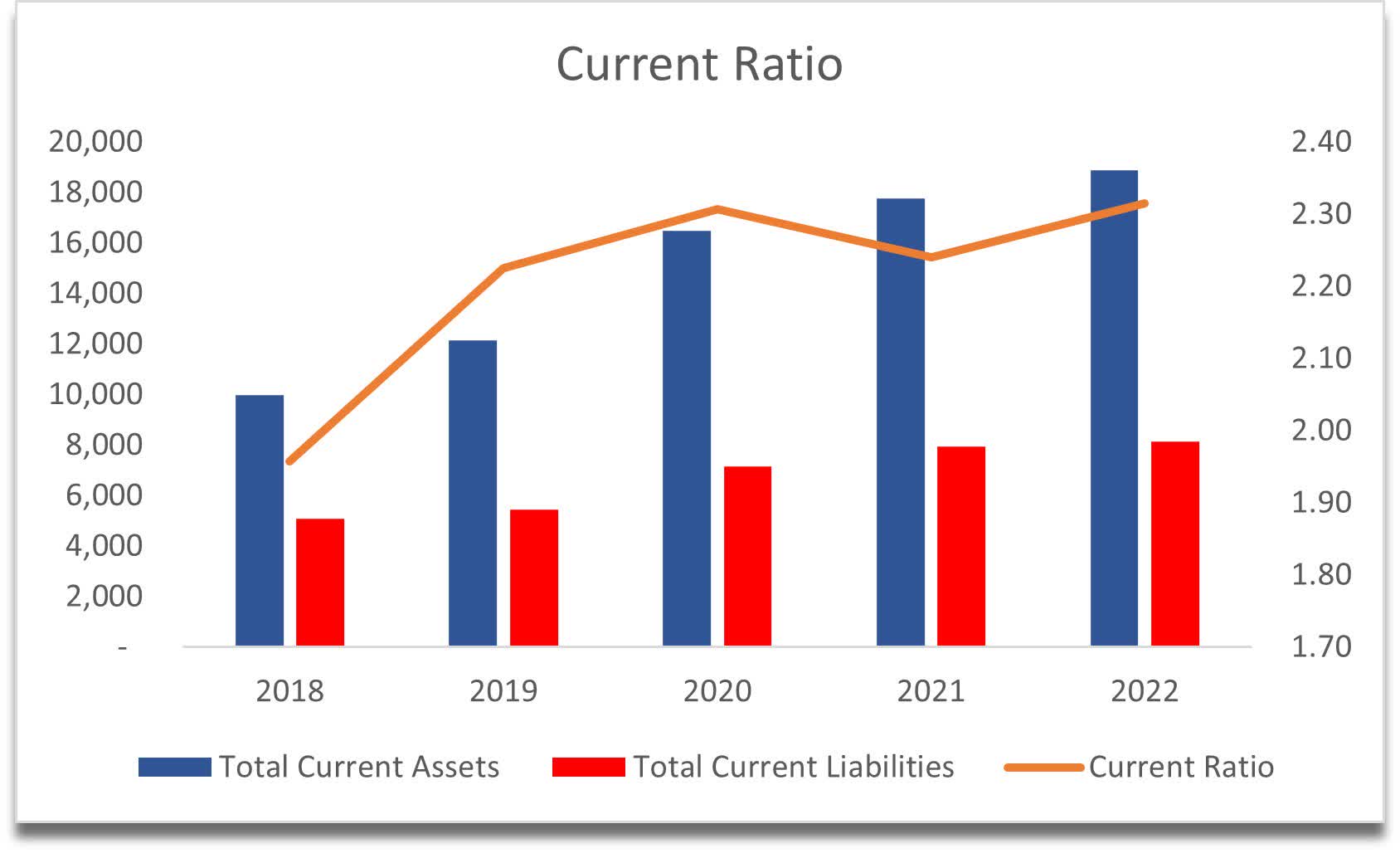

The company’s current ratio is also very strong, standing at around 2 for at least the last 5 years, meaning that if the company had to pay off all its short-term obligations at the same time, it would be able to with no problem. NetEase has no liquidity issues at all.

{kind=link}

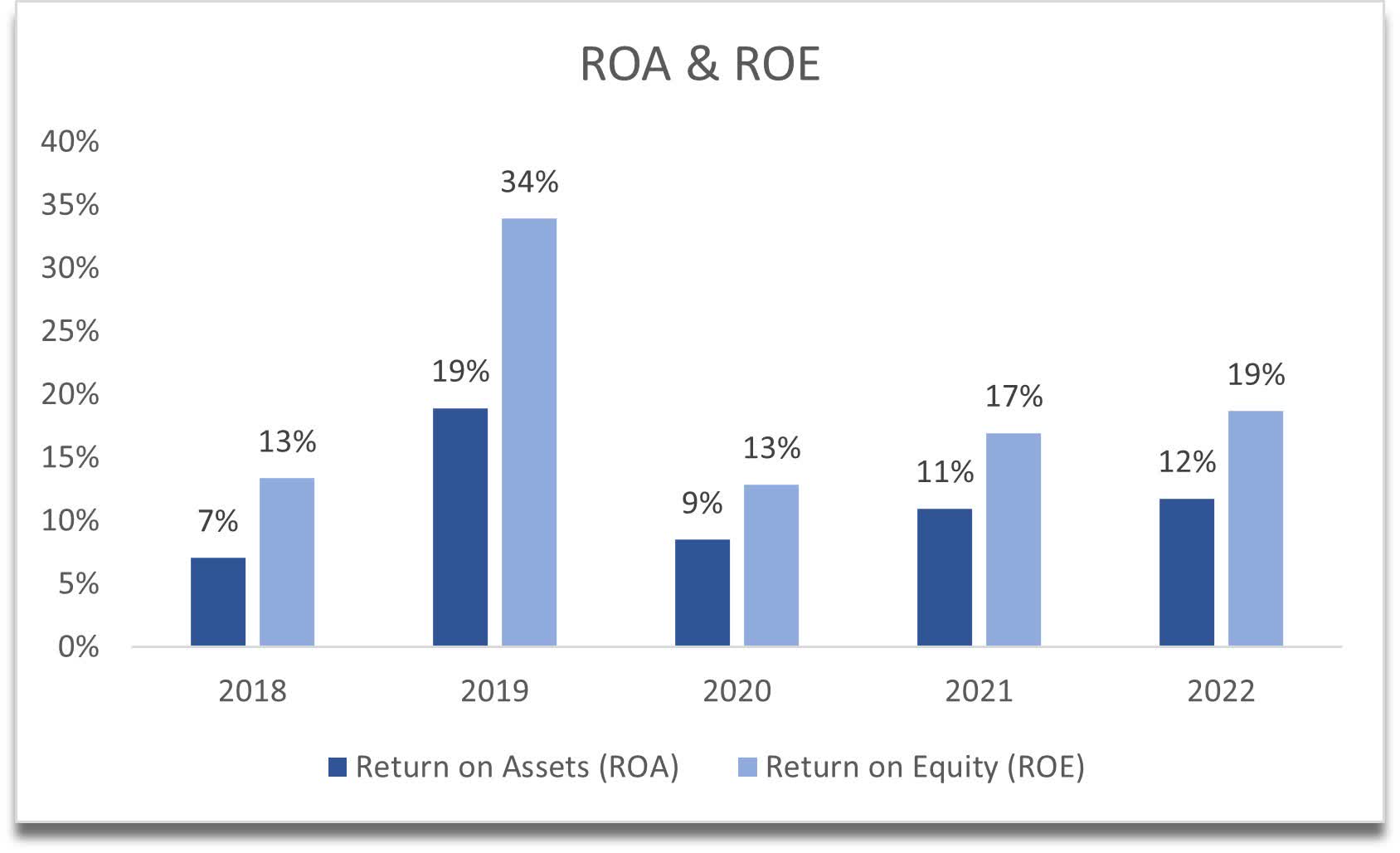

Let’s have a look at some efficiency and profitability metrics. The company’s ROA and ROE are and have been pretty decent over the years and well above my minimum of 5% for ROA and 10% for ROE, which is great. This tells us that the management can utilize the company's assets and shareholder capital efficiently.

{kind=link}

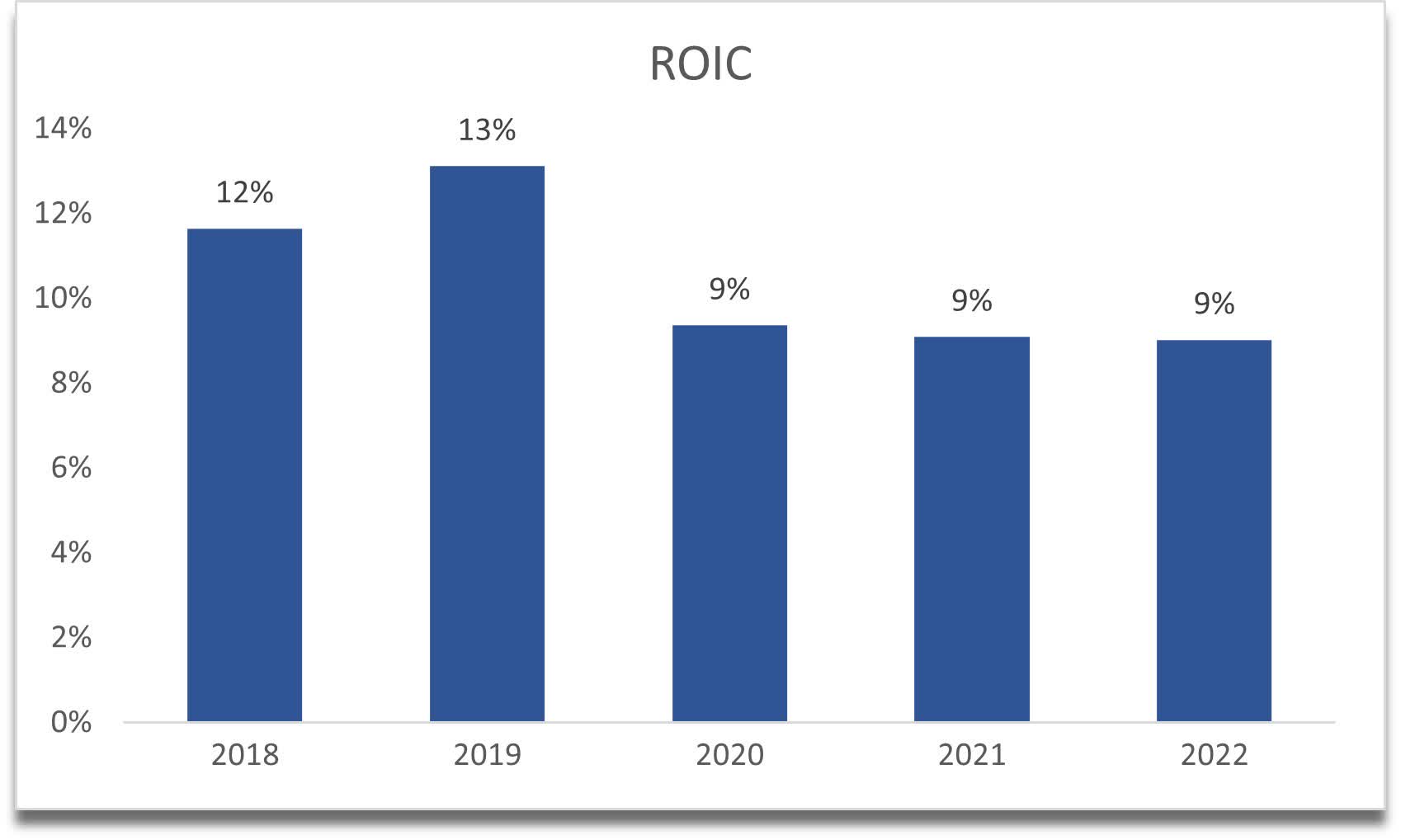

The return on invested capital is alright in my opinion, however, looking at FY19, it was over the minimum of 10% that I look for, so I would like to see this improving going forward. This tells us that the company does have some sort of competitive advantage and a moat, however, it has deteriorated slightly in recent years. It's a tough industry, so I am not surprised.

{kind=link}

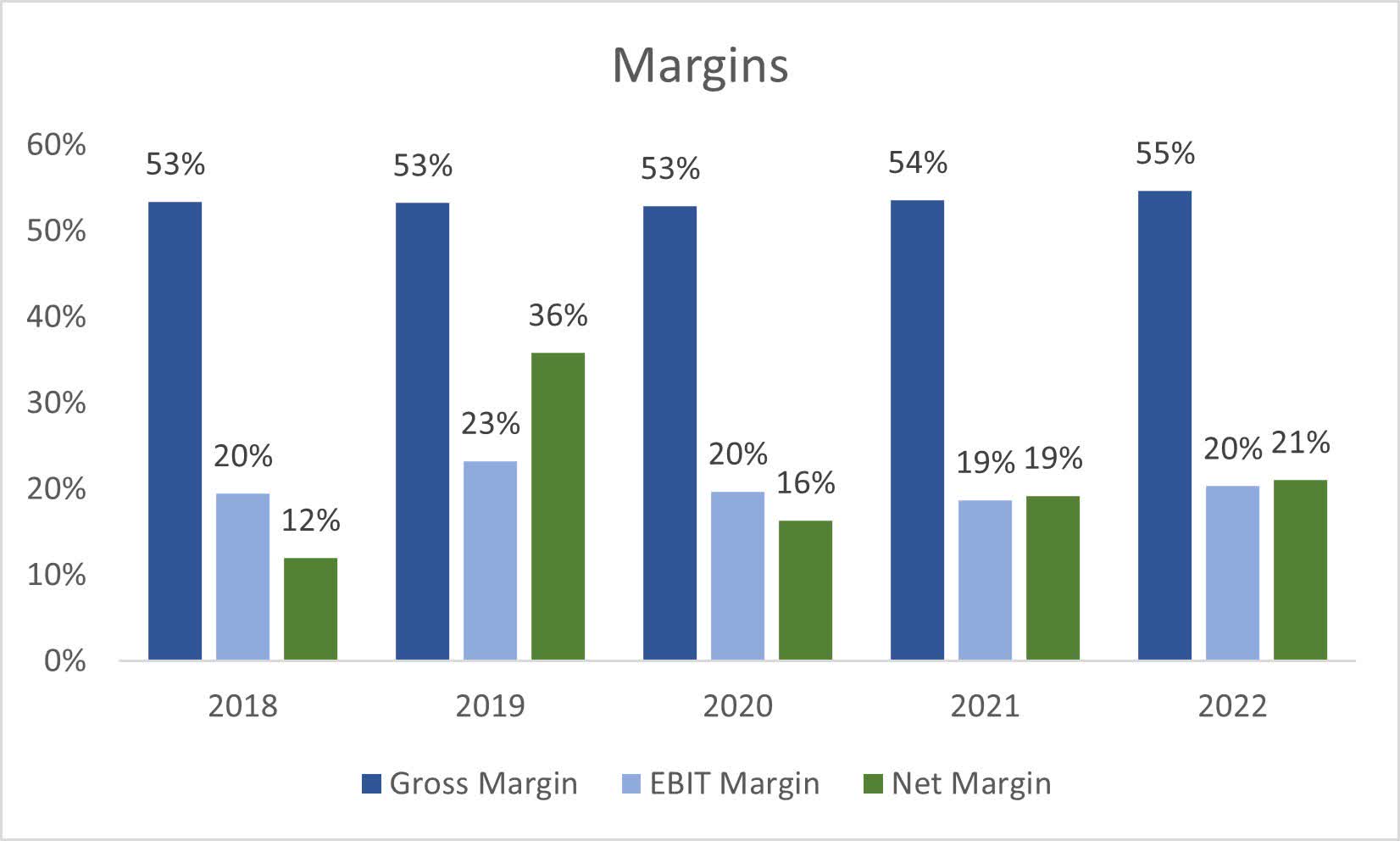

I also see that the company managed to improve its margins slightly from FY21 and during the Q1 23 announcement, the management said they managed to improve margins even further. I just hope the company can maintain its momentum.

{kind=link}

Overall, I can see a company that is very strong financially right now, with a lot of promise in the gaming industry and plenty of gunpowder to get something new and exciting going with all of that available liquidity. With the acquisition of Quantic Dream, the company is going further into the AAA console and PC space. I enjoyed Heavy Rain and Detroit: Become Human, so with Net Ease behind them, I could see another strong narrative-driven experience on the way.

Valuation

Looking back at the company’s previous 10 years, I was very surprised to see how strong the annual growth has been. It has averaged 20% annual growth in the last decade. I usually like to approach my calculations more conservatively, so I decided for my base case, revenue growth will be around 11% CAGR, for the optimistic case, I went with 14.7%, while for the conservative case, I went with around 9% CAGR until FY32.

In terms of margins, the company managed to improve gross margins in the latest quarter by around 500bps. I decided not to make such an improvement in my model to be on a safer, more conservative side. I decided to improve gross and operating margins by around 200bps or 2% in the next decade, which will keep net margins at an average of 21%.

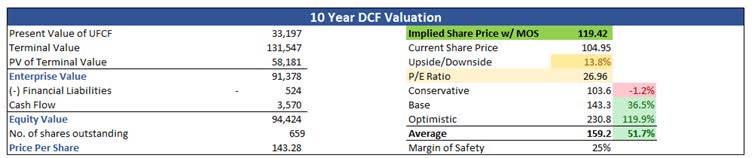

To stay even more conservative, I will add a 25% margin of safety to the calculation, which will bring NetEase’s intrinsic value to around $119.42 a share indicating around 14% undervaluation from the current price.

{kind=link}

Closing Comments

NetEase is one of the largest video game companies in China. I heard it often being compared to Tencent ( TCEHY ) and even though it's not that big, I can see it becoming very similar, especially if the company's other sectors will start to generate a lot more revenue to compete with the gaming segment, like the Cloud Music and Innovative Businesses segments.

What this calculation represents is that I like the risk/reward profile at current prices and with such a conservative growth assumption built in, I can see the company performing better in the long run and will continue to reward shareholders. I am going to wait until the next earnings release and continue to research further but it looks very promising in my opinion as a long-term play.

For further details see:

NetEase: A Good Deal At This Price Point