NTES - NetEase: A Worthy Buy Despite Regulatory Risks

2024-01-19 03:29:43 ET

Summary

- NetEase Inc is recommended as a buy with estimated per share values of $86.39, $98.15, and $104.17 in different scenarios.

- The recent drop in NetEase's share price due to new gaming regulations may be an overreaction from the market.

- The company's gaming division has historically shown decent revenue growth rates and operates with similar cost structures as peer companies.

Editor's note: Seeking Alpha is proud to welcome ERIC JIAQING WU as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Executive Summary:

- Buy recommendation issued for NetEase Inc (NTES). Per share value estimated to be $86.39, $98.15, and $ 104.17 in the pessimistic, base, and optimistic case respectively.

- At a market price of USD $90.42 per share, this implies an overvaluation of 4.66% in the pessimistic outlook, undervaluation of 7.87% in the base case and an undervaluation of 13.20% in the most optimistic scenario.

Introduction:

On 22nd December 2023, National Press and Publication Administration (NPPA) released the draft of new online gaming regulations to solicit public feedback ( English translation: here ). Two articles from the draft attracted much attention as they aim at regulating the revenue business models of online games.

In particular, Article 17 of the draft states that the prohibition of involuntary Player vs Player combat system in games while Article 18 of the draft outlined steps to limit excessive in-game spending. Following the announcement, shares of Chinese gaming companies plummeted. With NetEase's share price dropping from USD $104.43 to USD $86.55 overnight, a 17.12% plummet. This article aims to assess the possibility of overreaction from the market.

Company Overview:

Founded in 1997, NetEase has evolved over the years from being a software development company offering free web-based e-mail services to an internet conglomerate with four major business divisions: Games and related value-added services, Youdao (DAO), Cloud Music ( HKG:9899 ), and Innovative businesses and others. Of which Youdao and Cloud Music were separately publicly listed in the years 2019 and 2021. Each of the divisions respectively accounted for 78.41%, 5,27%, 8.12% and 8.19% of revenues in the past TTM. With the gaming division stably accounting for close to 80% of the total net revenue over the years. Note that Cloud Music was reported under Innovative businesses and others in years prior to 2020.

NetEase Revenue Breakdown (NetEase Annual Report)

{kind=link}

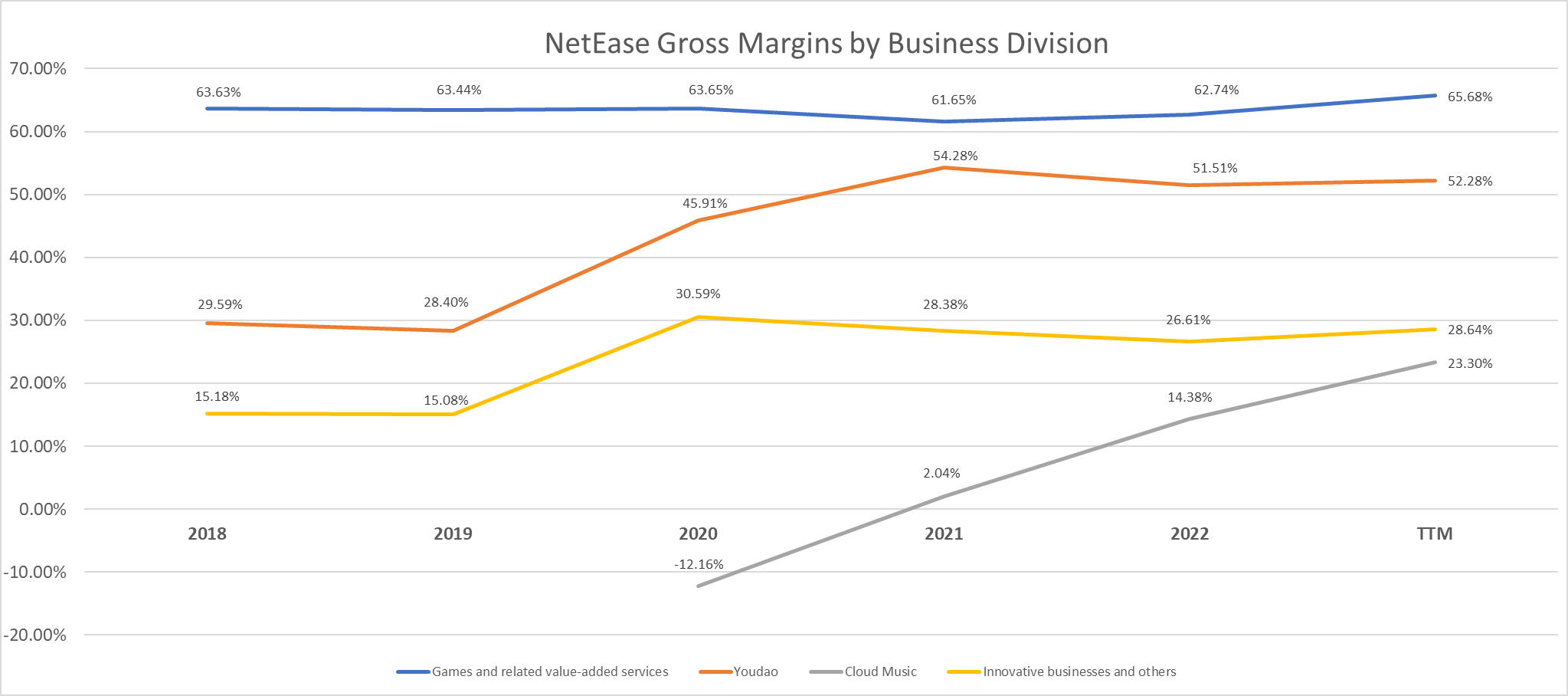

A quick break down of the gross margins of the various business divisions suggests that the various business lines operate in industries of varying cost structures, with the highest gross margin belonging to Games and related value-added services at 65.68% and the lowest gross margin belonging to the Cloud Music business at 23.30% for the trailing 12 months.

NetEase Gross Margins by Divisions (NetEase Annual Report)

{kind=link}

Furthermore, revenue growth rates of the various business lines differ too. With the Cloud Music line suffering from an 8.17% contraction in net revenue in the past TTM, while the other business division managed to achieve varying revenues growth rates between 5.15% to 6.97%.

NetEase Business Divisions Revenue Growth Rate (NetEase Annual Reports)

{kind=link}

Given the disparate growth rates and distinct cost structures evident in the various business segments, it is inappropriate to value the entire company as a singular entity. Therefore, we propose adopting a sum-of-the-parts (SOTP) valuation approach to account for the unique characteristics of each segment and provide a more accurate representation of the company's overall value.

Games and Related Value-Added Services:

The gaming division currently boasts a diverse portfolio of over 100 games, developed either in-house or through licensing arrangements, catering to both mobile and PC platforms. Among the notable titles in their repertoire are Eggy Party, Harry Potter: Magic Awakened, Diablo Immortal, Naraka: Bladepoint, and Fantasy Westward Journey Online.

Most of the games offered by NetEase currently utilize the item-based revenue model. Under this revenue model, in order to attract a larger pool of players, the games are free to play but offers sales of virtual items in the games for better gaming experiences. As such, if the draft of new online gaming regulations released on 22nd December 2023 were to become effective, in-app purchases by consumers will be restricted, placing considerable downward pressure on NetEase gaming revenue's future growth.

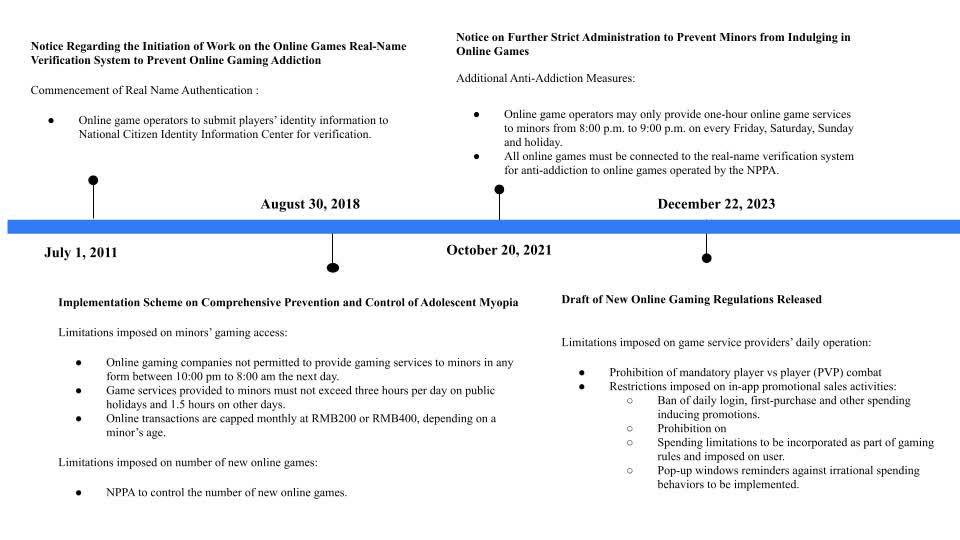

Timeline of China's Gaming Regulations (NetEase Annual Report)

{kind=link}

A brief examination of China's gaming regulations history reveals that the authorities have consistently imposed regulations. While previous regulations primarily aimed at preventing addiction among minors, they had minimal impact on the gaming market, as minors were not the main customers. However, the newly released draft marks the first instance of regulations aimed at directly curbing gamers spending of all age groups and restricting in-game promotional sales activities, serving as a signal of further regulatory actions down the line. To smooth the market's fear, shortly after the announcement of the draft, the National Press and Publication Administration (NPPA) approved 105 new online games for the gaming industry. Furthermore, the head of publishing unit of NPPA, Feng Shixin, was allegedly removed from his position due to the stock market rout caused by the earlier draft.

Such efforts by the Chinese authorities suggest the receptiveness of the authorities to market opinions. As such, the I believe that while there may be further regulations down the line, the regulatory acts would be catered more towards addiction prevention and prevention of excessive in-game spending instead of direct curbs on all fronts. Placing a modest downward pressure on NetEase gaming departments' future revenue growth.

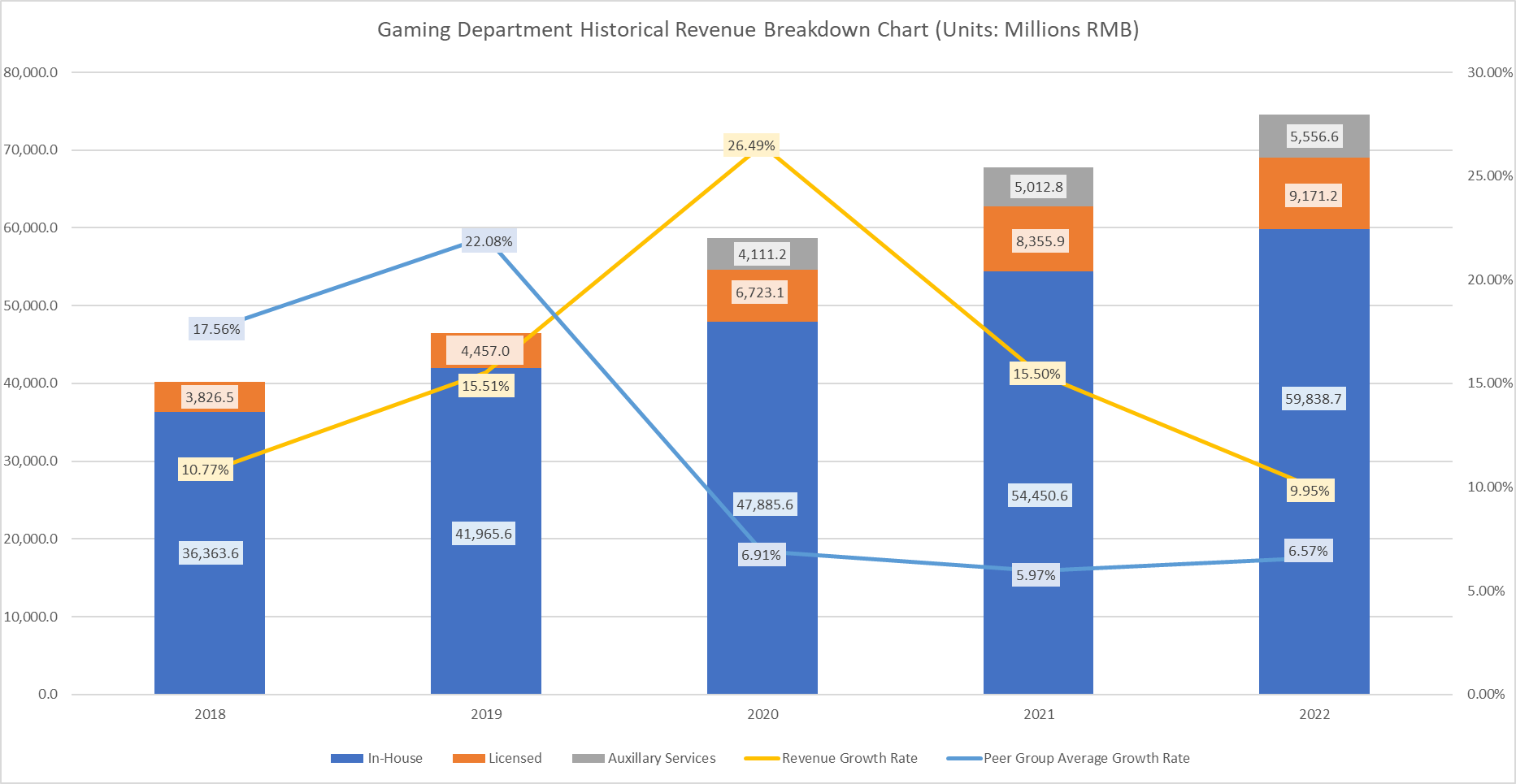

Looking at the past performance of the gaming department, we can see that the gaming department has traditionally enjoyed decent revenue growth rates of CAGR of 13.43% between 2018 and 2022 against a peer group average CAGR of 10.10%, with licensed games stably accounting for approximately 9% of net revenue. Note that ancillary business lines related to games like the NetEase CC live streaming service (a platform offering various live streaming content with a primary focus on game broadcasting) and other value-added services from "innovative businesses and others" were incorporated into "online game services" in 2022 to form "games and related value-added services". Detailed breakdown of TTM figures could not be achieved due to lack of available information as detailed full breakdown of Youdao and Cloud Music are revealed only once per year.

NetEase Gaming Revenue Breakdown (NetEase Annual Reports)

{kind=link}

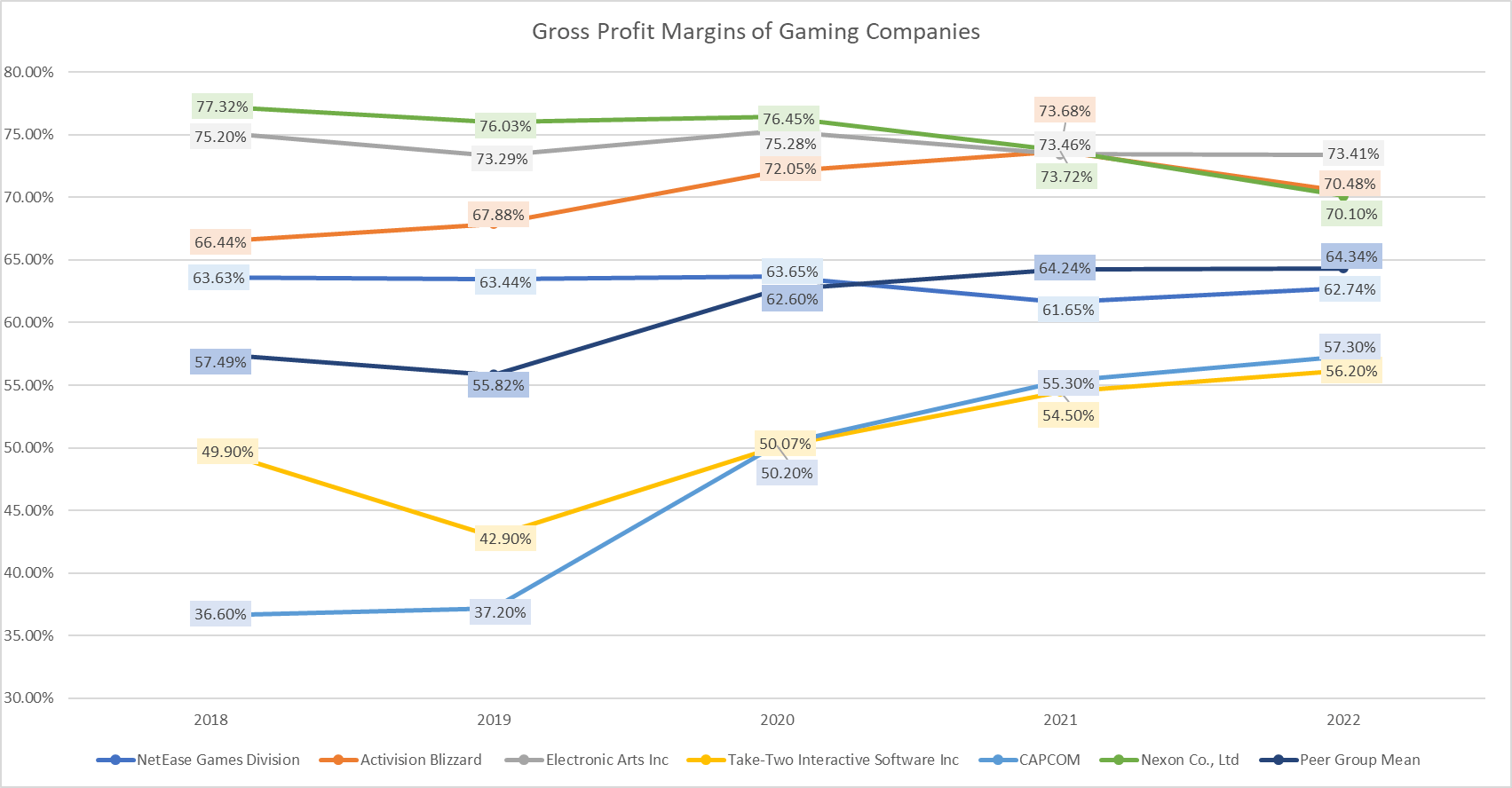

Comparison of gross profit margins against similar companies reveals that NetEase Games faces similar cost structures as pee groups with the average gross margin of 63.02% between 2018 and 2022 compared to the peer group average of 60.9%. Note that Tencent (TCEHY) was not included in in the peer groups as the operating figures of Tencent's gaming division is consolidated under its Value-Added Services segment, hence the exact figures of its gaming division could not be determined.

Gross Margins of Various Gaming Companies (Annual Reports of Various Companies)

{kind=link}

Operating Margins Estimation:

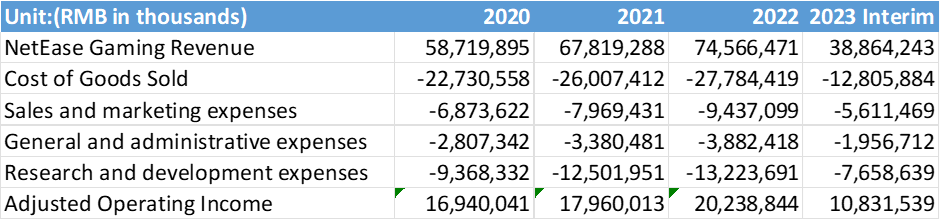

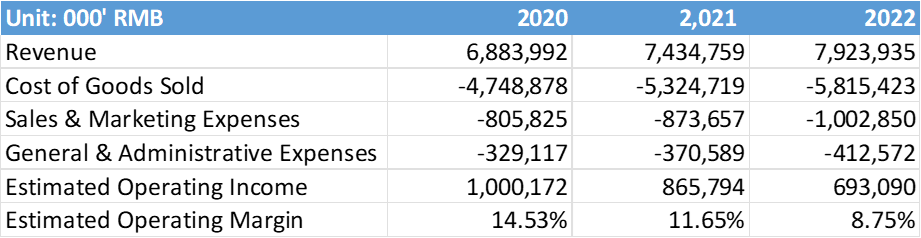

As the operating expenses of NetEase are only reported as consolidated figures of all four divisions, no direct figures on operating expenses belonging to the gaming division are available. Since Youdao and Cloud Music are publicly listed with their operating expenses separately reported in their annual reports, we can subtract their operating expenses from the consolidated figures of NetEase to derive the combined operating expenses of the Gaming division and Other Innovative Businesses division. Following of which we pro-rated the Sales & Marketing expenses and General & Administrative expenses between the gaming division and other innovative businesses by revenue. Research & Development expenses were allocated to the gaming division since the other innovation businesses division is not research intensive.

NetEase Gaming Operation Expense Allocation (Self-Computation)

{kind=link}

With the adjustments made, we can see that the gaming division of NetEase has achieved an estimated operating profit of RMB¥ 16.94 billion, RMB¥ 17.76 billion and RMB¥ 20.23 billion in 2020, 2021 and 2022 respectively. Note that minor non-core operating incomes and expenses were excluded in the calculation. The exclusion had little impact on the figures.

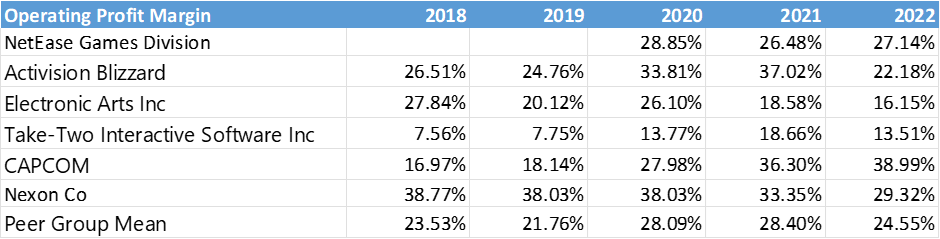

Operating Margins of Gaming Companies (Various Gaming Company Annual Reports)

{kind=link}

Comparing the operating margins against similar gaming companies, we can see that NetEase gaming has achieved an average operating margin of 27.49% in the past three years against a peer group three years average operating margin of 27.01%. Figures earlier than 2020 could not be computed due to lack of available data.

Future Revenue Growth Projection:

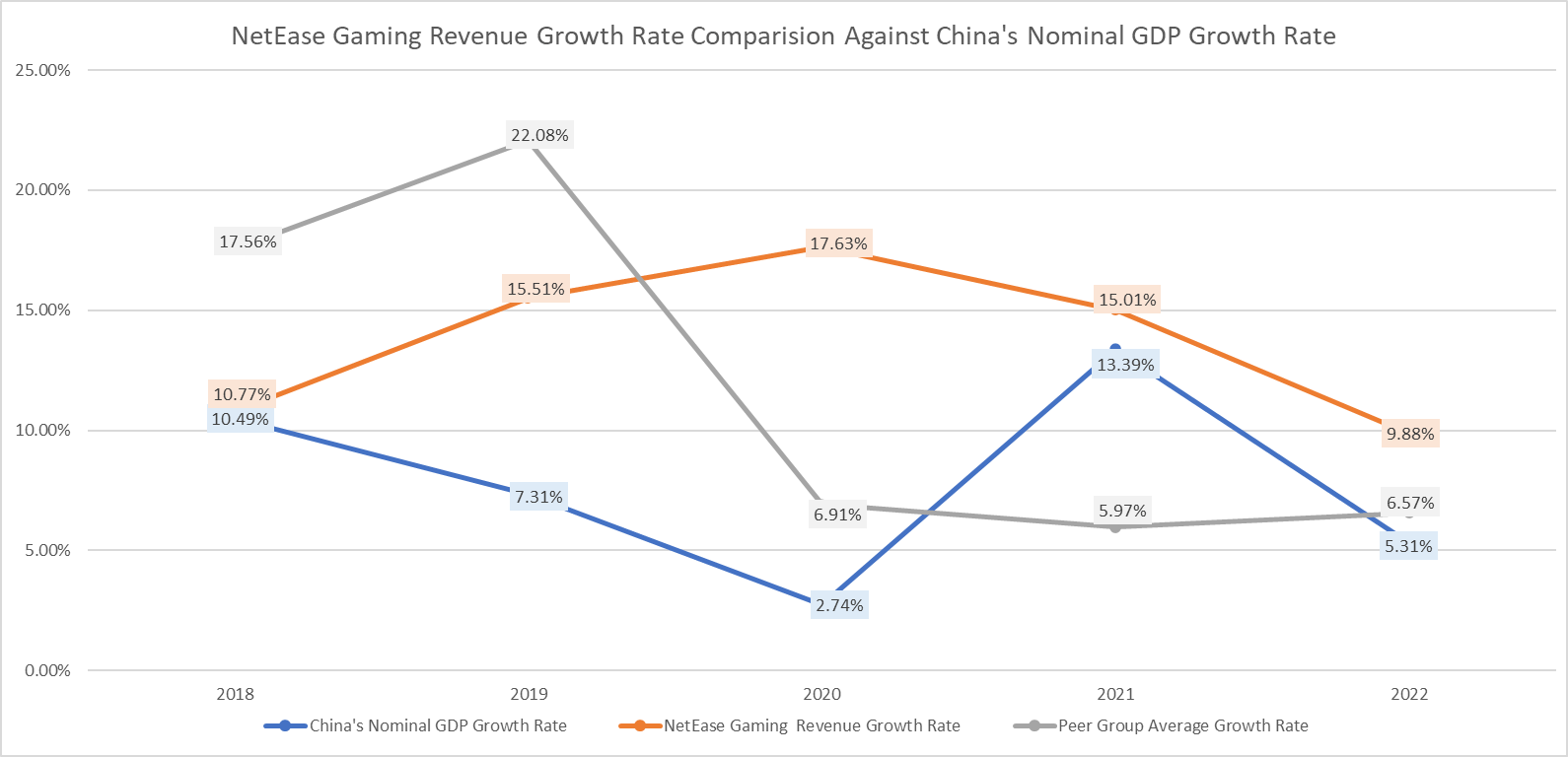

NetEase Gaming Revenue Growth Rate Comparison Against China's GDP Growth Rate (Various Sources)

{kind=link}

A review of the past revenue growth reveals that NetEase gaming revenue growth was 17.63% in 2020, 15.01% in 2021 and 9.88% in 2022, outpacing both China's GDP growth rate and the peer group average.

Going forward, we shall project three possible revenue growth rate scenarios. In the most pessimistic case, we will assume tough regulatory measures in the future, dragging NetEase gaming department's future revenue growth rate to that of China's overall forecasted GDP growth rate. Which is predicted to be 4.0% in 2024 and 2025, and an average of 3.8% from 2026 to 2030 in accordance with Moody's latest outlook for China. For the base case, we will assume a CAGR of 7.63% between the year 2024 and 2029, in line with Mordor Intelligence's forecast for China's gaming market. In the most optimistic case, we will assume the NetEase gaming division to be able to invent new revenue growth models to circumvent the tightening restrictions placed by the Chinese authorities and expand overseas to match the forecasted global gaming industry CAGR of 9.32% between the year 2024 and 2029, in accordance with Mordor Intelligence's report .

Effective Tax Rate Estimation:

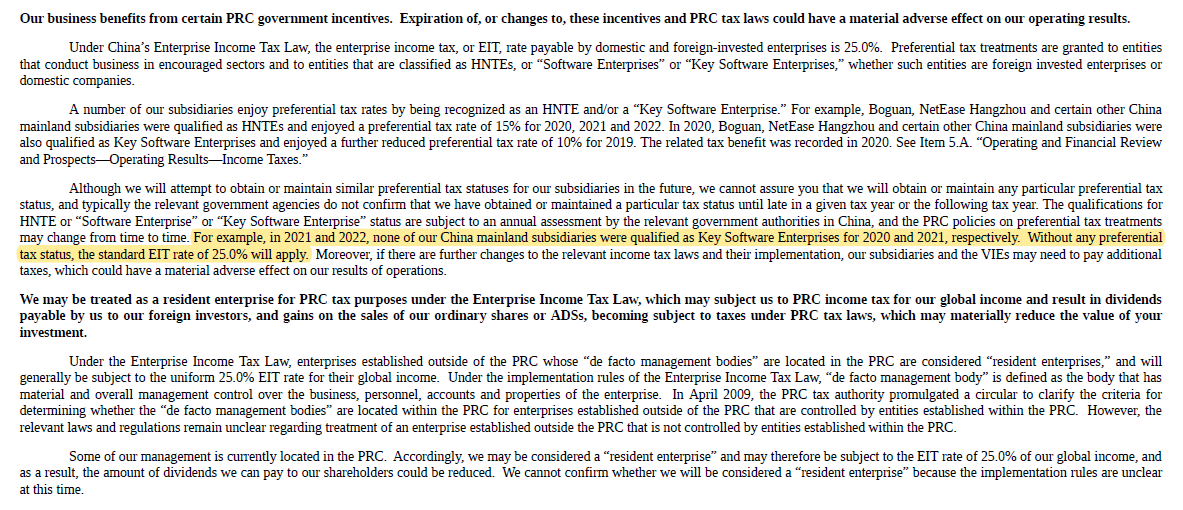

As both Youdao and Cloud Music experienced net losses in the past few years, effective tax rates reported on the consolidated income statements would not be reflective of real effective tax rates paid by the gaming division. Hence the operating figures of Youdao and Cloud Music needed to be stripped from the consolidated income statements. After the adjustments, we derived an effective tax rate of 15.89% in 2020, 17.10% in 2021 and 19.86% in 2022 respectively.

Effective Tax Rate Estimation (Self-Computation)

{kind=link}

For the purpose of the DCF valuation, we shall use China's corporate tax rate of 25% as the future effective tax rate as the company is no longer getting the tax subsidies like it used to in the past, as suggested by the following extract from the 2022 annual report and evident via the uptrend trend of effective tax rates in recent years.

NetEase Tax Rate Extract (NetEase Annual Report)

{kind=link}

Discount Rate Estimation:

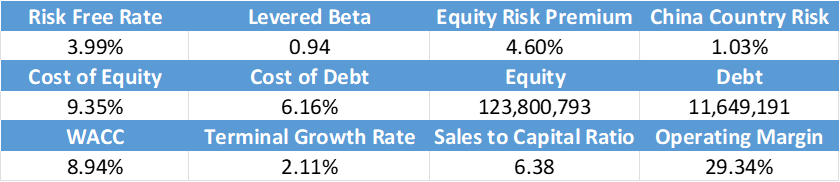

As the time of writing, the 7 years US treasure yield stands at 3.991% as of 11th January 2024. According to Professor Aswath Damodaran of NYU, equity risk premium and China's country risk premium currently stands at 4.60% and 1.03% respectively. We will use his figures for our valuation. Levered beta of 0.94 will be used.

Using the following formula:

{kind=link}

We derive a cost of equity of 9.345%.

NetEase Cost of Debt (NetEase Annual Report )

{kind=link}

Since interest income (expense) is reported as a net figure in the annual reports, one could not estimate the interest rate of NetEase loans. The best estimate found was the five-year loan facility reported in the annual report, that states a cost of borrowing at 85 basis points per annum over LIBOR. Since LIBOR is no longer used, SOFR will be used as substitute. As of 9th January 2024, the SOFR rate stands at 5.31%, yielding us an estimated cost of borrowing for NetEase of 6.16%.

With equity standing at RMB¥ 123.800 billion and debt standing at RMB¥ 12.98 billion, this yields us a an WACC of 8.9%. Reinvestment needs will be estimated by the average sales to capital ratio of the past few years, which stands at 6.38. Terminal growth rate of 2.11% will be used.

Here is a summary of the inputs for the valuation.

{kind=link}

Sales to capital ratio was computed by averaging the revenue to net invested capital ratio between 2020 and 2022 with figures belonging to Cloud Music and Youdao removed from the calculation. Terminal growth rate of 2.11% was arrived by taking the geometric mean under Moody's projection that China's GDP growth slows down to 3.5% in 2030 and to 1% in 2050.

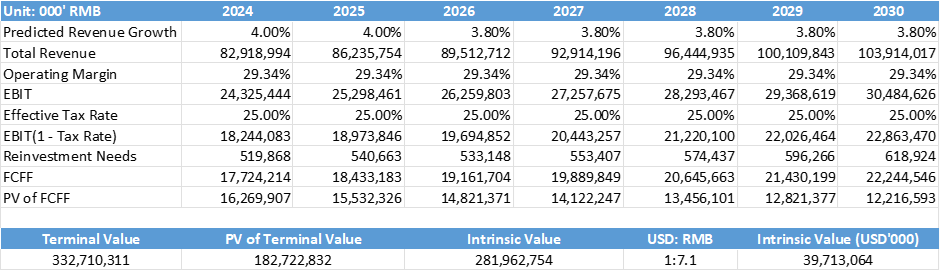

Pessimistic Case:

Pessimistic Case: NetEase Gaming Division DCF (Self-Computation)

{kind=link}

Under the pessimistic outlook, the revenue of NetEase gaming is projected to grow to RMB¥ 103.9 billion in 2030 with a terminal value of RMB¥ 332.7 billion. Yielding it a present value of RMB¥ 281.96 billion, which translates to USD $39.71 billion dollars with an USD:RMB exchange rate of 7.1:1.

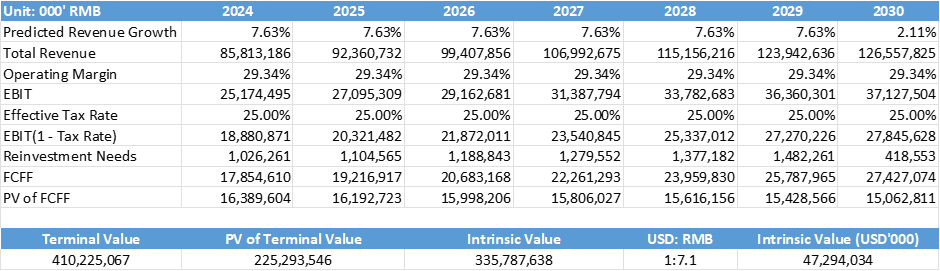

Base Case:

Base Case: NetEase Gaming Division DCF (Self-Computation)

{kind=link}

With the base case outlook, NetEase gaming is expected to deliver a free cash flow to firm of RMB¥ 15.06 billion in 2024, yielding the division a current intrinsic value of RMB ¥335 billion, which is equivalent to USD $47 billion.

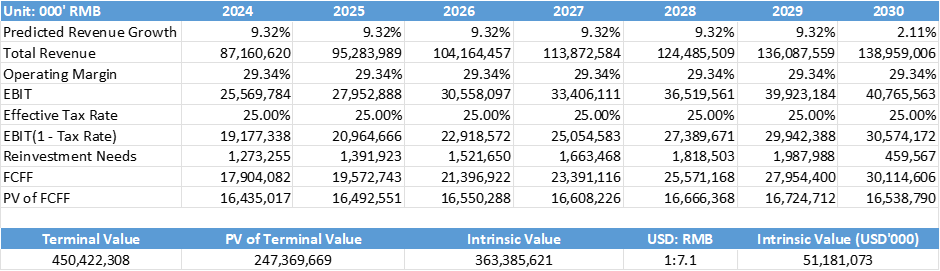

Optimistic Case:

Optimistic Case: NetEase Gaming Division DCF (Self-Computation)

{kind=link}

By assuming that NetEase gaming will circumvent the upcoming regulatory restrictions and grow on par with the global gaming market, we arrive at a projected revenue of RMB¥ 138 billion in 2030 and intrinsic value of RMB¥ 363 billion. Putting the estimated worth of the division at USD $51 billion dollars.

Youdao & Cloud Music

Youdao currently trades at USD $3.56 as of 11th January 2024, resulting in a market capitalization of USD $442.20 million. With a 55.0% holding in Youdao, this puts the shareholding worth at USD $243.21 million dollars. As of 11th January 2024, Cloud Music currently trades on the Hong Kong Stock Exchange for HKD $88.50 per share with a total market capitalization of HKD $18.96 billion dollars. With a 60.5% ownership in Cloud Music Inc, this put the value of the holding in Cloud Music Inc at HKD $11.47 billion dollars. Which translates to USD $1.47 billion dollars at an exchange rate of 1 USD to 7.82 HKD.

Innovative businesses and others

The 'Innovative businesses and others' division of NetEase encompasses 'Yanxuan' - a private label consumer lifestyle brand, 'Wangyi Xinwen' - a news website, 'NetEase Pay' - a payment service, 'NetEase Mail' - a free and fee-based email service along with other services.

Innovative Businesses Operation Expenses Allocation (Self-Computation)

{kind=link}

After allocation of operating expenses between the Gaming Division and Innovative Business division, the estimated operating income of the Innovative Businesses division stands at RMB¥ 1.00 billion, RMB¥ 865.79 million and RMB¥ 693.09 million in 2020, 2021 and 202 respectively. The average operating margin stands at 11.64%. Revenue growth rate was 8% in 2021, 6.58% in 2022 and 5.15% TTM. Operational data earlier than 2020 were excluded as Cloud Music was previously reported under the Innovative Business division.

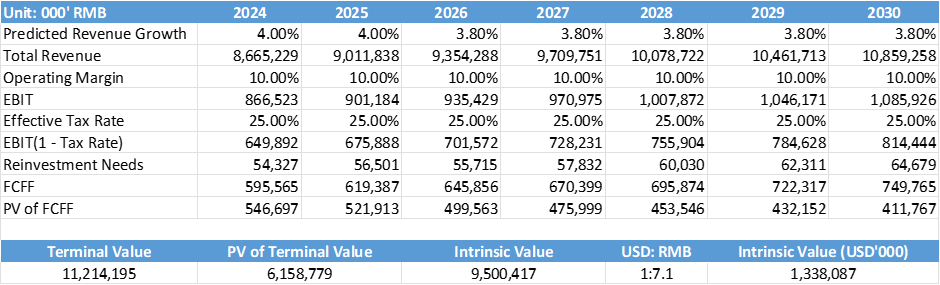

Due to the lack detail operational information on the Innovative business division and the similarity of its past revenue growth rate with that of China's overall GDP growth rate, we shall project the division's future revenue growth rate to be similar to Moody's forecasted GDP growth rate of China, which is 4% in 2024 and 2025 and an average of 3.8% between the years 2026 to 2030. The future operating margin used for valuation will be 10%, which is lower than the past average operating margin of 11.64% to account for its downward trend.

DCF of NetEase Innovative Businesses Division (Self-Computation)

{kind=link}

With the assumption above, we derive an intrinsic value of RMB 9.5 billion for the Innovative Business division, which translates to USD $1.338 billion dollars.

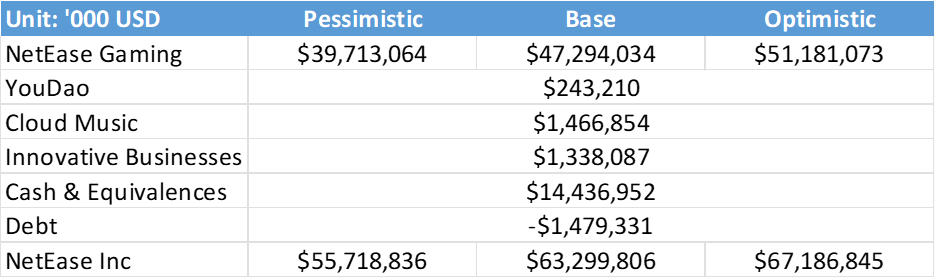

Summary:

Summary of NetEase Estimated Intrinsic Value (Self-Computation)

{kind=link}

After adjusting for cash & equivalents and subtracting off debt, we arrive at a valuation of USD $55.7 billion dollars under the pessimistic assumptions, USD $63.3 billion in the base case and USD $67.2 billion in the most optimistic scenario.

Estimation of Intrinsic Value Per Share (Self-Computation)

{kind=link}

Stated in per share basis, NetEase Inc has an estimate per share intrinsic value of $86.39, $98.15, and $104.17 in the pessimistic, base, and optimistic case respectively. Representing an overvaluation of 4.66% in the pessimistic outlook, undervaluation of 7.87% in the base case and an undervaluation of 13.20% in the most optimistic scenario.

Moving forward, potential investors should continuing monitoring the regulatory authority's attitude towards gaming regulation and avoid investing in NetEase in scenarios of hostility. At the same time investors should also keep a lookout for technological disruption risk. With the increasing maturity of Virtual Reality Technology and the introduction of consumer-ready headsets like Apple Vision Pro , the genre of VR games is becoming increasingly compelling. By offering a more immersive experience, consumers may start to prefer VR games over traditional PC and mobile games in the future. With a market size of USD $20.73 billion in 2022 and a forecasted CAGR of 22.7% between 2023 to 2030, the VR games genre poises itself as both a source of opportunity and threat to the current gaming companies. While NetEase has proved itself to be a formidable player in the PC and Mobile gaming segment, its ability to adapt to the of next wave of change in the gaming industry remains to be seen.

As of the present, with market price of USD $90.42 per share, the risks associated possible future regulatory restrictions are already sufficiently compensated by the lowered share price. With limited downside risk and higher upside reward potential at this price point, NetEase Inc deserves a buy recommendation.

For further details see:

NetEase: A Worthy Buy Despite Regulatory Risks