NFLX - Netflix: On An Incrementally Accelerating Growth Trajectory

2023-09-08 14:55:48 ET

Summary

- Netflix's advertising venture shows potential for additional revenue streams and reshaping the advertising industry.

- Management promises to expand the advertising business and contribute more than 10% of total revenues.

- Netflix's Q2 results were mixed, but management expects robust growth in the fourth quarter and raised their FCF guidance.

- Stock should trade around $510 per share. (Providing investors ~15% upside from current trading price).

Netflix's (NFLX) recent results and management's outlook present a mixed but evolving scenario. While subscriber growth remains strong and management anticipates growth acceleration, the revenue figures have been slightly underwhelming. However, with the potential for robust growth in the fourth quarter and an upward revision in company FCF estimates, there are positive signs for the company's future performance and financial outlook.

Investment Thesis: Netflix's strategic initiatives, including paid sharing, ad-supported content, and the removal of the Basic tier, position Netflix for the best growth ever.

Let's delve deeper into management promises and how they shape the overall long-term story of Netflix.

Management bets on Lucrative Advertising Venture

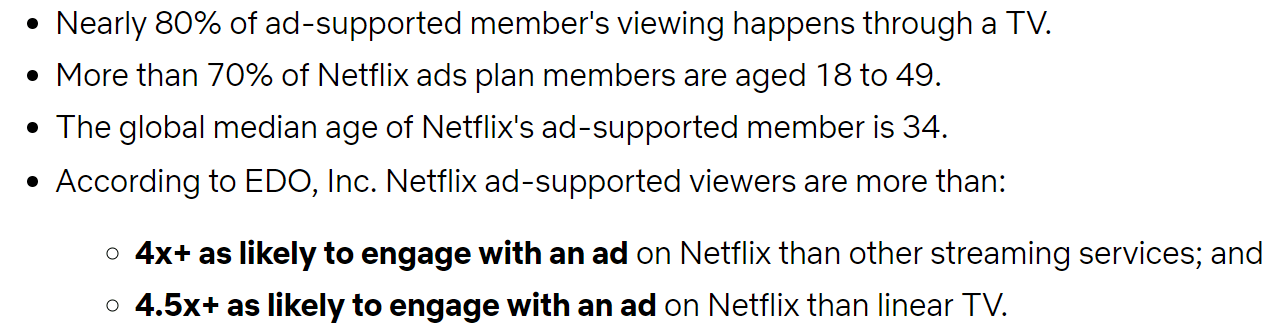

Netflix stands out with its unparalleled viewer engagement , leaving its closest competitor trailing by a staggering fivefold margin, capturing a commanding 80% of television viewership. Moreover, Netflix boasts a prime demographic, with approximately 70% of its members falling into the coveted 18-49 age bracket.

{kind=link}

Netflix's current advertising approach is marked by a light ad load, typically ranging from 4 to 5 minutes. This presents significant untapped potential for advertisers and additional revenue streams. However, Netflix adamantly rejects a one-size-fits-all approach and is diligently exploring varying ad loads, recognizing the distinct dynamics between films, episodic content, new releases, and library content.

In addition to traditional ads, Netflix is delving into sponsorships, offering innovative branding opportunities within its platform. It aims to be a driving force in reshaping the advertising industry, leveraging its vast user base and data resources.

Netflix is also actively expanding its targeting capabilities to enable precise ad placement, maximizing the impact of each ad impression. To enhance accountability and transparency, it has embraced Nielsen digital ad ratings, a trusted industry standard.

In a nutshell, Netflix's advertising strategy prioritizes viewer experience, acknowledges content diversity, and aims to redefine advertising's future. With its extraordinary engagement metrics, extensive user base, and commitment to innovation, Netflix is poised to make a substantial impact in the advertising landscape while optimizing revenue through meticulous management of ad-related variables.

How Management Promises are impacting the overall growth story

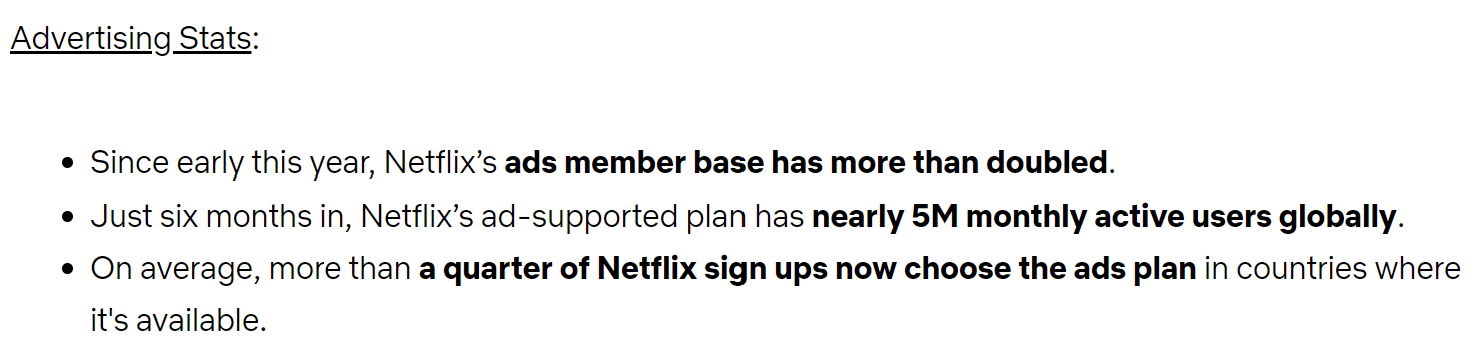

While management consistently emphasizes that it's still in the early stages of its advertising venture, it has recently disclosed some noteworthy statistics. The company now boasts approximately 5 million Monthly Active Users (MAUs) on the ad tier, with over 25% of gross additions opting for ads in the 12 markets where this feature is available.

{kind=link}

Management is confident that the advertising business will continue to expand and eventually contribute more than 10% of the total revenues. However, they are hesitant to commit to growing ad revenue per member beyond the current range of $8-9. This caution stems from the potential challenges posed by increasing inventory leading to pressure on Cost Per Mille (CPM) rates.

The presentation emphasizes the significant societal impact the platform has, driven by its extensive customer base and high engagement levels. This impact extends to various aspects, including music popularity (artists like Kate Bush and Metallica), sports (such as Formula 1), and consumer products (like chess sets). Management believes that it can replicate this influence for brands advertising on the platform, highlighting the platform's potential as a powerful marketing tool.

Long-term Strategy underpinned on both subscribers and ARM

The primary challenge I saw when analyzing the Q2 2023 results is the 1% decline in ARM (Adjusted Revenue Metrics) excluding foreign exchange impacts. This decline was not uniform across regions, with UCAN (United States and Canada) showing a modest 1% increase, while EMEA (Europe, Middle East, and Africa) experienced a 1% decline, LatAM (Latin America) achieved an impressive 8% growth, and APAC (Asia-Pacific) encountered a substantial 7% decrease.

Looking forward to the third quarter, management commentary indicates an expectation of ARM remaining flat or experiencing a slight decline. Management attributes these challenges to several key factors:

Lapping Price Increases: Temporarily halted price increases in anticipation of the launch of our paid sharing feature. This decision affected our ARM figures.

Shift in Subscriber Mix : Observed a shift in the subscriber base, with a higher proportion coming from countries with lower ARM. This mix change contributed to the overall ARM decline.

Gradual Contribution from Advertising: Gradually building revenue streams through advertising, with a significant increase in ad-supported subscribers compared to the previous quarter. Importantly, our Ad Average Revenue Per User (ARPU) remained unchanged during this transition.

Paid Sharing Expansion: Paid sharing was successfully rolled out in more than 100 countries in May, with revenue in each region surpassing pre-launch expectations and sign-ups outpacing cancellations. They are set to extend this feature to most remaining countries, paving the way for new price increases in 2024.

In conjunction with these strategic initiatives, management made the decision to eliminate the Basic ad-free tier, a move that has been implemented in the U.S., UK, and Canada to date. This, combined with the rollout of paid sharing and our advertising strategy, is expected to create a substantial revenue growth opportunity, particularly targeting a teenage demographic, as we progress into 2024.

Simultaneously, they are also committed to managing our high-speed operating expenses (HSD opex) efficiently. This approach is anticipated to drive a significant improvement of over 400 basis points (bps) in profit margins by the year 2024.

Q2 2023 results & outlook mixed; FCF guidance raised

The second-quarter (2Q) results and management's outlook for the third quarter (3Q) have presented a mixed picture for Netflix. While net additions and profits exceeded expectations, revenues and Adjusted Revenue Metrics ((ARM)) fell below projections.

In 2Q, Netflix managed to add 5.9 million subscribers, surpassing Street estimates of 3.6 million. However, revenue growth for the quarter was at 3% year-over-year, aligning with the company's guidance but falling short of Street's +4% expectations. Furthermore, this growth represented a slight deceleration from the previous quarter when Netflix reported an 8% increase in revenue.

Looking ahead to 3Q, management anticipates similar subscriber additions, implying around 6 million, which is slightly above the street consensus of 5 million. This robust subscriber growth is expected to support a revenue increase of 7.5%, although this figure falls short of the street's more optimistic projection of 10%. Meanwhile, operating income is forecasted to grow by over 20% to reach $1.89 billion, slightly exceeding the Street's estimate of $1.86 billion.

It's worth noting that while the 3Q revenue guidance reflects a modest acceleration, management hinted at more substantial growth in the fourth quarter. This growth is expected to be driven by the increasing contribution from paid sharing and advertising. These dynamics suggest that the business is on a trajectory for accelerating revenue and operating income growth into 2024, as per street estimates of 15% revenue growth and 44% operating income growth compared to approximately 7% in 2023.

In terms of cash flow, management now expects more than $5 billion of Free Cash Flow ((FCF)) in 2023, which is an improvement from the prior estimate of $3.5 billion. This increase is attributed in part to the timing of content spending and the impact of strikes. Assuming content spend of $15 billion and $18 billion in 2023 and 2024, respectively, it is anticipated that FCF will reach $5 billion and $6 billion in 2023 and 2024E.

Password sharing fix going as expected

Management is enthusiastically addressing the issue of password sharing and has rolled out a solution they are excited about. They have made it clear that the majority of subscribers will not notice any significant changes as a result of this solution.

Recent reports about cost-cutting efforts are in alignment with the company's ongoing commitment to operational efficiency. This emphasis on efficiency has been a key focus for the company in recent times, reflecting its dedication to maximizing resources and optimizing its operations.

Management has indicated a potential interest in mergers and acquisitions (M&A), particularly when it comes to acquiring intellectual property ((IP)) or content libraries. However, they have emphasized that any M&A activity would be carefully considered and weighed against the option of investing in organic content creation. Management recognizes that acquisitions come with their own set of complexities, including the management of legacy assets, and these factors would be factored into any decision.

Netflix set to gain significantly rationalizing competition in DTC

Netflix stands to gain significantly as the direct-to-consumer ((DTC)) streaming landscape undergoes a process of consolidation and rationalization. This transformation is expected to encompass several key changes:

Content Spend Reduction : Many competitors may decrease their content spending as part of cost-cutting measures or strategic shifts. This would reduce the level of competition for content acquisition, potentially allowing Netflix to secure sought-after content at more favorable terms.

Localized Content Reduction : Some streaming platforms may reduce their investments in creating localized or region-specific content. Netflix, with its global reach, can continue to offer a wide range of content, potentially appealing to a broader international audience.

Market Exits : Market exits by certain DTC platforms could lead to a consolidation of viewership, with Netflix poised to capture a portion of the user base left without their preferred streaming service.

Price Increases : In response to market changes and the need to sustain profitability, streaming platforms may implement price increases. Netflix, with its established user base and a reputation for quality content, may have more room to adjust pricing upward without significant subscriber attrition.

Content Licensing : The rationalization of competition might lead to more opportunities for content licensing, enabling Netflix to supplement its original content with licensed titles, further enriching its content library.

These shifts in the DTC landscape are expected to work in Netflix's favor. They should support the company's ability to attract new subscribers and potentially implement price increases, possibly beginning in 2024. Importantly, these developments are anticipated to help Netflix maintain control over its content costs.

Valuation:

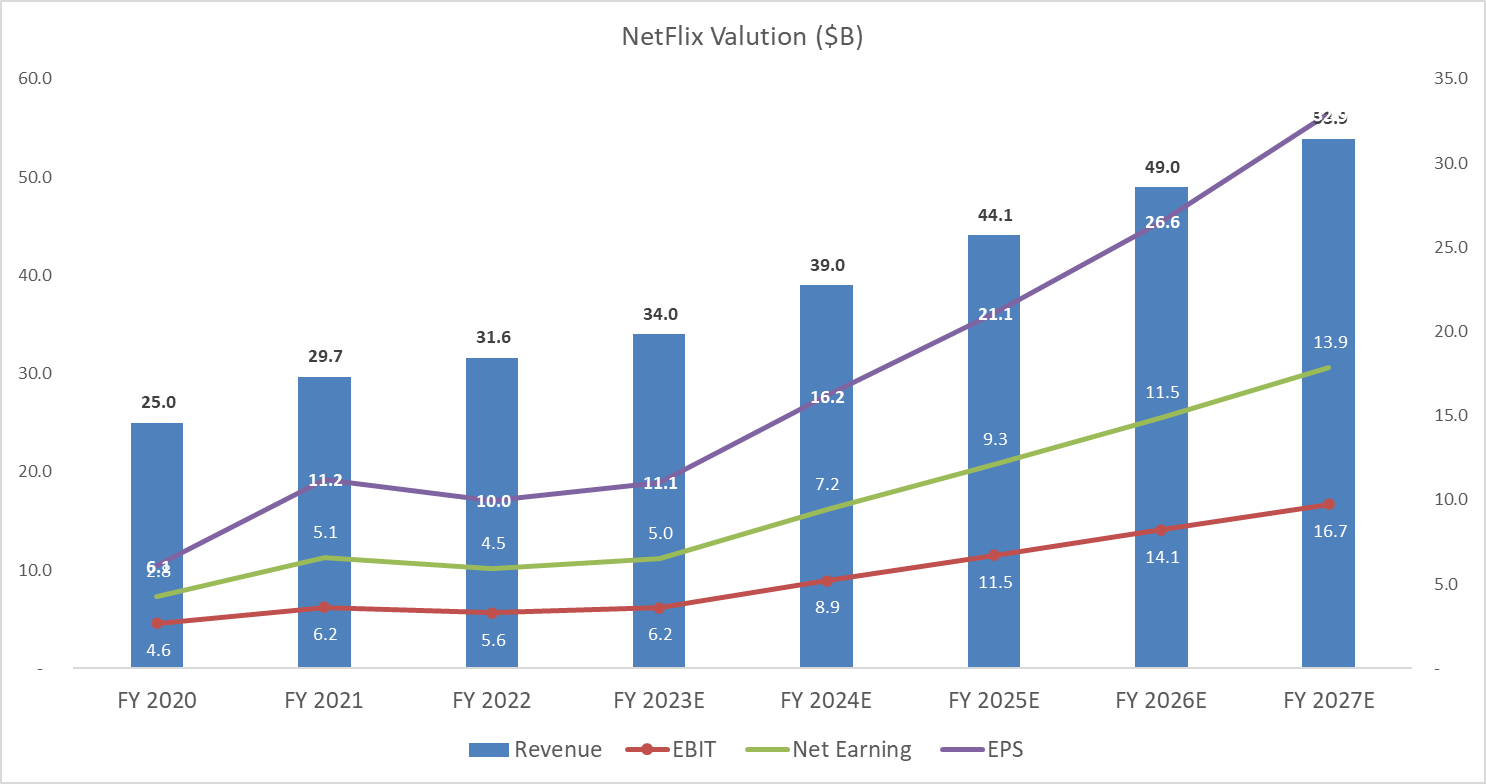

By applying a ~28X multiple, this stock should trade around $510 per share. (Providing investors ~15% upside from current trading price). My price target for Netflix is based on a multiple of 28 times the estimated Free Cash Flow ((FCF)) for the year 2025, discounted back to the present. This valuation approach reflects our confidence in Netflix's growth potential and the expectation that it will continue to adapt and thrive amid changing industry dynamics, equating to approximately one times its expected growth rate.

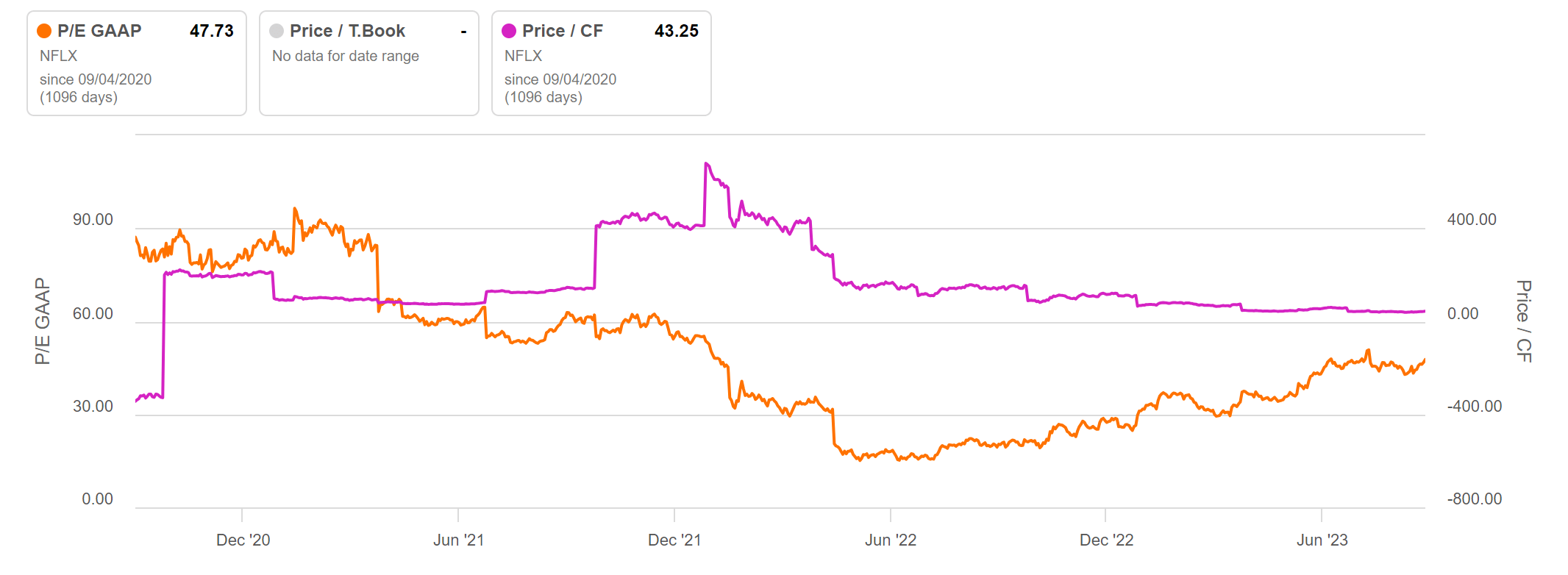

I am using a conservative multiple of 28X for valuation purposes. This is relatively lower compared to the historical trading range of the stock over the past 5 years, where the median P/E (Price-to-Earnings) ratio has been around 26-32X. Despite being on the lower end of historical valuations, I believe this lower multiple is justified due to anticipation that the market will begin compressing the multiple. This expectation is based on the substantial increase in earnings I foresee in the upcoming quarters.

Chart made by Author using company data and projections

{kind=link}

{kind=link}

Conclusion:

In conclusion, while recent ARM figures may have presented challenges, Netflix's strategic initiatives, including paid sharing, ad-supported content, and the removal of the Basic tier, position Netflix for promising revenue growth as we move forward. These efforts, coupled with prudent expense management, are expected to yield substantial margin improvements in the coming years.

Risk Statement:

My valuation for Netflix relies on a blended approach using various multiples. It's crucial to note that any shifts in growth expectations for the U.S. economy and consumer sentiment, whether positive or negative, have the potential to influence my projections, ratings, and price targets. Additionally, companies like Netflix, which operate internationally, are exposed to similar risks in the countries they serve. They also contend with the impacts of foreign currency fluctuations, all of which may have consequences for our overall perspective and investment strategy.

For further details see:

Netflix: On An Incrementally Accelerating Growth Trajectory