NTGR - NETGEAR: Deterioration Continues

2023-11-24 08:54:46 ET

Summary

- Revenues have been decreasing for many years and the negative trend continued throughout 2023.

- Profit margins are currently depressed due to declining volumes, strong inflationary pressures, and higher freight costs.

- Some improvements are expected in 2024 as headwinds ease.

- The balance sheet is very strong thanks to zero debt, very high cash and equivalents, inventories, and short-term investments.

- Despite significant medium-term upside potential, I recommend staying away from NETGEAR as the long-term trend is negative.

Investment thesis

NETGEAR (NTGR) has tested the patience of investors in recent years, and the share price already accumulated a 73% decline from all-time highs reached in 2018. Revenues have been falling for a decade, and although it seemed that the trend had reversed in 2020, the current macroeconomic landscape marked by weaker demand and high customer inventory, along with the lift of the restrictions derived from the coronavirus pandemic, have caused two consecutive declines in 2021 and 2022. In addition, the declining trend has continued during 2023, and by 2024, a very limited recovery is expected.

Although the company has a debt-free balance sheet and very high cash and equivalents, inventories, and short-term investments, the trailing twelve months EBITDA margin has been in negative territory for more than a year, and although it returned to positive territory in the third quarter of 2023, profit margins are expected to suffer a further contraction in the fourth quarter. Lower volumes are significantly impacting profit margins, something that the management has not been able to reverse even through a significant reduction in the headcount, and trailing twelve months' cash from operations has been negative since Q4 2021.

In order to offset the impact that declining volumes are having on operations, the company is making great efforts to expand the number of subscribers in its paid subscriber services, which is certainly paying off as the number of subscribers is increasing at a significant rate. The Armor Cybersecurity service is the company's most demanded service, and the company's current strategy is to continue expanding the number of subscribers by offering more features, which is expected to deliver some long-term growth and improved margins.

But despite this, the company appears to be suffering the long-term consequences of a lack of significant innovation (beyond updating its products to adapt them to the changing needs of customers and consumers) and acquisitions, and nothing suggests that this is going to change as revenues for 2024 are expected to show a very slight recovery after three years of consecutive significant declines.

For this reason, I consider that the company's risk of continuing to suffer a long-term deterioration in its operations outweighs potential short and medium-term capital returns as no turnaround is expected in the foreseeable future and time has played against the company for many years, and nothing suggests this will change anytime soon as R&D expenses remained flat for a very long time.

A brief overview of the company

NETGEAR is a global manufacturer of networking products for consumers, power businesses, and service providers. The company was founded in 1996 and its market cap currently stands at ~$380 million as it employs over 600 workers.

NETGEAR (Q4 2022 Earnings Presentation)

{kind=link}

The company operates under two business segments: Connected Home, and Small and Medium Business (SMB). Under the Connected Home segment, which generated 60% of revenues in 2022, the company manufactures WiFi internet networking solutions, routers, 4G and 5G mobile products, and smart devices, and also offers subscription services for value-added performance, security, privacy, and premium support. Under the SMB segment , which generated 40% of revenues in 2022, the company provides solutions for business networking, wireless local area networks (LAN), audio and video over Ethernet for Pro AV applications, security, and remote management providing enterprise-class functionality.

Currently, shares are trading at $12.87, which represents a 71.55% decline from recent highs of $45.23 in 2021, and a 73.31% decline from all-time highs of $48.22 in 2018. This reflects growing pessimism among investors as revenues have been decreasing for years and, more recently, significant volume declines, strong inflationary pressures, and higher freight costs have pushed the EBITDA margin into negative territory despite significant headcount reductions.

2023 will mark a new bottom in revenues, and no significant recovery is expected in 2024

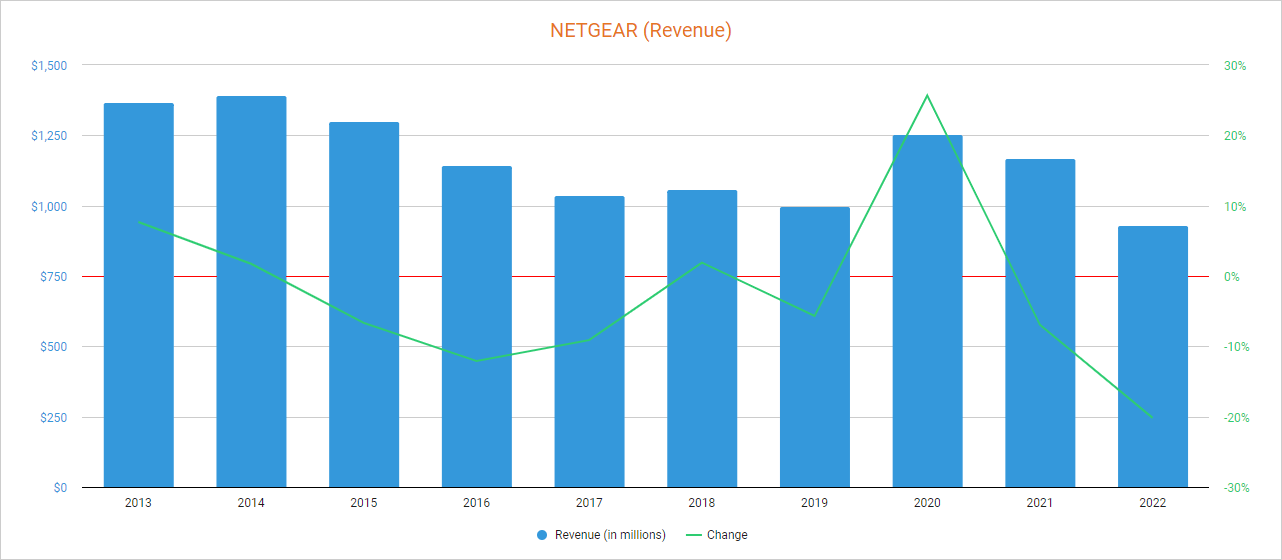

In the last 10 years, revenues have suffered a worrying negative trend as they experienced a 26.77% decline from $1.27 billion in 2012 to $0.93 billion in 2022. It seemed that the trend was going to be broken in 2020 boosted by growing connectivity needs due to the coronavirus pandemic as revenues increased by 25.68%, but they continued their negative trend soon after as they decreased by 6.94% in 2021 and by a further 20.17% in 2022.

NETGEAR Revenue (Seeking Alpha)

{kind=link}

Nothing has improved in 2023 as revenues declined by 14.08% year over year during the first quarter, by 22.31% year over year during the second quarter, and by 20.73% year over year during the third quarter (but increased by 14.1% sequentially), despite a 25% increase year over year in service revenue, as unit volumes declined by 25% year over year, and the trailing twelve months' revenues declined to $801.3 million as a consequence (vs. $932.5 million reported in 2022). Furthermore, 2023 is expected to close with very weak revenues of $737.29 million, which would represent a 20.93% decline compared to 2022, although some improvement is expected in 2024 as revenues are expected to increase by 4.75% to $772.30 million.

During Q3 2023, the number of paid service subscribers increased to 844,000 (compared to 666,000 during the same quarter of 2022), but the impact caused by weaker demand and customer inventory destocking has not allowed this to translate into an increase in overall revenues. Still, the management expects this number to reach 875,000 in Q4 and keep growing in the future, so now much of the hope is focused on the possibility of NETGEAR becoming a large digital services company in the long run.

The company enjoys a wide geographic diversification. Using 2022 as a reference, 66% of the company's revenues are generated in the Americas, whereas 19% are generated in Europe, the Middle East, and Africa, and 15% in Asia-Pacific, and despite the recent decline in revenues, an even steeper decline in the share price has caused a significant drop in the P/S ratio to 0.469, meaning the company currently generates $2.13 in revenues for each dollar held in shares by investors, annually.

This ratio is 40.71% lower than the average of the past 10 years and represents a 73.34% decline from 10-year highs of 1.759, which essentially reflects a prevailing pessimism among investors. For shareholders, this means that significant capital returns could be obtained by having enough patience to wait for the macroeconomic outlook, and especially the company's situation, to improve as the upside potential is very high, but I consider that if we add depressed margins that did not allow the company stay profitable in the past quarters to the systematic lack of growth, we have a company only for investors willing to invest in high-risks/high-reward turnaround plays.

Margins remain depressed despite recent improvement

In recent years, the company has managed to maintain a fairly healthy gross profit margin above 25% and an EBITDA margin that has typically hovered around 8%, which has allowed for steady share buybacks with which to reward long-term shareholders, but the trailing twelve months' EBITDA margin entered negative territory in 2022 and currently stands at -4.22% as a consequence of lower volumes, strong inflationary pressures, and higher freight costs, albeit the gross profit margin currently stands at 30.62%.

Still, some margin improvement was achieved in Q3 2023 as the EBITDA margin improved to 1.04%, and the same for the gross profit margin, which increased to 34.84%. This was boosted by a stronger mix of higher-margin products, lower freight costs, a 12% headcount reduction year over year, and increased service revenue. In the long term, growing paid service subscribers is expected to continue having a positive impact on profit margins. Still, the management expects a 150 basis point decline in gross margins in Q4 2023 compared to Q3 as it expects to sell older lower-margin inventory, and expects the margin recovery to start in Q1 2024 and accelerate in Q2.

If, as the management predicts, profit margins change towards a positive trend in 2024, the impact on investor sentiment will likely be positive. Although not guaranteed, some margin improvement is actually very likely because revenues are expected to stabilize, which should allow the decreased headcount to be positively reflected in operations. Still, for this to be reflected in the share price, investors will also need to see that revenues do not continue their long-term negative trend, and for this to happen, the strategy carried out in recent years would have to drastically change, which does not seem to be happening as R&D expenses have remained static.

Therefore, I consider that despite margin improvement expectations in 2024, a recovery in revenues of only 4.75% boosted by easing headwinds will not change current investors' pessimism significantly as the risk of long-term revenue deterioration is, in my opinion, high.

A very strong balance sheet should allow the company to navigate current and potential headwinds

By maintaining a good profitability profile in recent years (excluding recent quarters), the company has managed to maintain a robust balance sheet, which means that the company is prepared to navigate current headwinds and even a potential recession for a very long time. In this regard, inventories currently stand at $281 million, cash and equivalents at $131 million, and short-term investments at $97 million, which together are 25% higher than market capitalization.

This has allowed positive cash from operations of $26.1 million in Q3 2023 as the company managed to reduce its inventories by $43.6 million compared to Q2 to $280.9 million, and the management expects to continue reducing them in Q4 2023 and Q1 2024, which means trailing twelve months' cash from operations should enter positive territory as soon as in Q4 2023 as the company reported negative cash from operations of -$4.9 million in Q4 2022. Currently, trailing twelve months' capital expenditures are at the lowest level of the past 10 years at $5.23 million, so inventory destocking should allow the company to amply cover it while generating excess cash.

Certainly, the company keeps regularly launching new products on the market as revenues from products launched in the last 12 months accounted for 11% of revenues in the third quarter of 2023, but this fact should not confuse investors as NETGEAR is a company that operates in a very changing technological sector due to advances in technology as the products launched eventually become obsolete when replaced by others.

Therefore, I consider that despite the company having a very robust balance sheet, it could deteriorate in the long run if profit margins do not recover much of the recently lost ground and if revenues do not change their trend to a positive one once and for all.

Share buybacks are paused

In recent years, the management has allocated significant amounts of cash to buy back the company's shares as the total number of shares outstanding has declined by 19.63% in the last 10 years. This practice allows the company to improve per-share metrics as its results are divided among fewer shares, and is much more flexible compared to dividends as the management has no need to stick with it during weaker years.

In the long term, investors can expect further share buybacks as long as cash from operations allows, but they stopped in early 2022 and I would not expect buybacks as significant as in the past in the foreseeable future due to weaker performance. On the other hand, I actually believe share buybacks have not been the best use of cash in the case of NETGEAR as the company has spent $703.13 million in share repurchases since 2013 while the market cap is currently at $381 million as a result of the lack of growth. If the company had allocated all that cash to growing initiatives and acquiring other businesses, I am highly convinced that the situation would be better than the current one.

Risks worth mentioning

Given the situation the company has gone through in recent years and the current complex macroeconomic landscape, I consider that the risk of investing in NETGEAR, despite the recent drop in the share price and a very robust balance sheet, is significant. Below, I would like to highlight those risks that I believe potential investors should take especially into account.

- If the company fails to increase its innovative efforts focused on high-growth markets, revenues could continue their downward trend in the coming years.

- Recent interest rate hikes could cause a global recession, which would have a significant impact on the company's operations. Lower volumes caused by a potential recession would cause a significant decline in revenues, as well as further margin contraction due to unused workforce.

- The growth rate of paid subscribers could slow down significantly if the macroeconomic landscape continues deteriorating or if the company fails to adapt offered services to consumer needs. It is also important to keep in mind that the number of subscribers could decline if new customers are not satisfied with the service and the company fails to retain them.

- The balance sheet could steadily deteriorate if profit margins do not improve significantly from 2024 onwards, which would ultimately increase pessimism among investors.

Conclusion

Although I usually look for opportunities in companies that are going through a bad moment in order to find reasonable prices to invest, whether they are dividend-paying companies or if the potential capital return is significant, a promising long-term outlook has always been a must for me.

It is true that the current pessimism towards NETGEAR is very strong among investors and that this could represent a good opportunity for those potential investors with enough risk appetite and patience to wait for the current macroeconomic landscape, as well as the specific situation of the company, to improve. But despite this, I consider that a long-term negative revenue trend in a highly competitive and constantly changing industry is a very bad sign that suggests that, despite potentially high medium-term capital returns, time is against the company as the negative trend could continue if it fails to find niches for growth.

Capital expenditures are at very low levels compared to recent years and R&D expenses have remained flat, which suggests that there are not really great efforts to grow, but rather that the company is more focused on continuing updating its products while expanding the number of paid subscribers in the services business as its growth strategy. Certainly, this could work in the long term, but so far, not even high growth rates have made it possible to compensate for the loss of volumes in the rest of the products manufactured by the company. Therefore, I consider the risks of further operational deterioration in the long term to be significant and I believe there are better investments than NETGEAR.

For further details see:

NETGEAR: Deterioration Continues