SSNLF - Netlist: A Strong Sell Due To Weak Performance And Overvaluation

2024-01-15 02:13:41 ET

Summary

- Netlist is a U.S. semiconductor company that manufactures and sells memory chips.

- NLST stock has underperformed the S&P 500 since its IPO in 2006, with weak financials and inefficient resource allocation.

- Legal battles with large corporations and lack of growth prospects despite sector tailwinds further support a Strong Sell rating for the stock.

Business Overview

Netlist Inc. (NLST) is a U.S. semiconductor company founded by a former LG Corporation employee, Hong Chun-ki. The company manufactures, designs, and sells a wide range of semiconductor products, in particular, memory products for cloud, datacenter, storage, and other types of B2B customers.

Taiwan, a semiconductor superpower, had important elections with the incumbent (and pro-US) Democratic Progressive Party having won a third time in a row. This status quo could result in further escalation by China. Therefore it is likely that semiconductor stocks will have increased volatility in 2024 - and there is room for profit making, both on the long and short sides of the sector. I will discuss a stock that, in my opinion, one can short to benefit from the volatility.

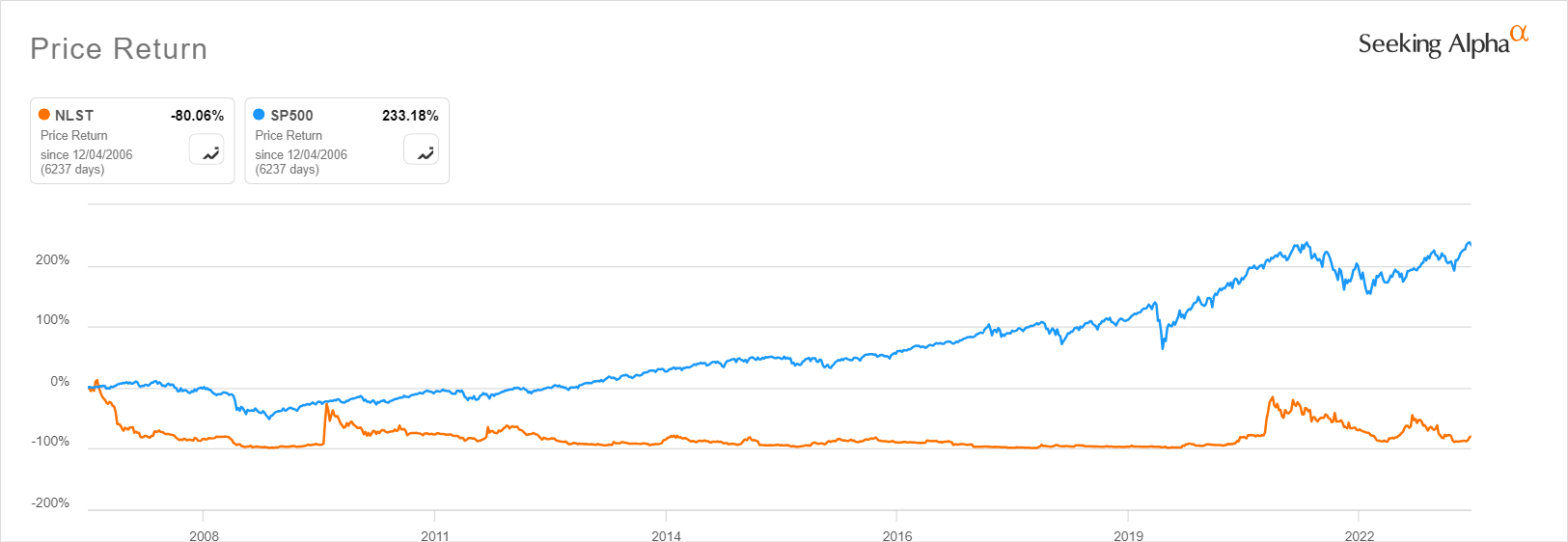

Poor Stock Performance & Investment Thesis

Since its IPO in 2006, the stock has been underperforming the S&P 500 by a wide margin. Indeed, since 2006, the stock is down -80% while the U.S. index is up more than +230%. If you went long on the stock, you would have painfully underperformed the overall U.S. market. But we know that past performance is not indicative of future performance, and therefore we will look now if anything has changed since.

{kind=link}

Netlist Inc. has essentially been marooned in legal battles, and their outcomes could dictate either a decline of the company or it could renew its hope to gain the long-awaited competitive edge against its much larger competitors. I lean towards the decline of the company and I will present my case for shorting the stock, but also some key risks to watch that would invalidate my Strong Sell rating on the stock.

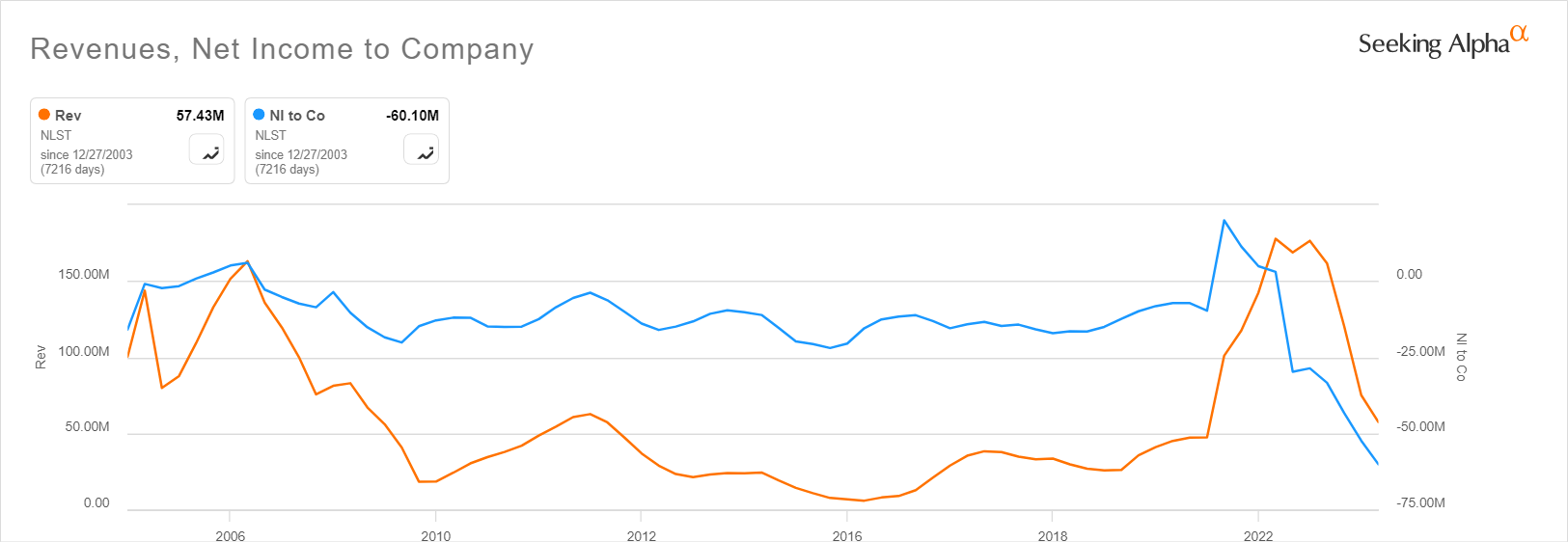

Fundamentally Weak Financials

Looking at the financials, the chart is not more attractive than its stock performance.

{kind=link}

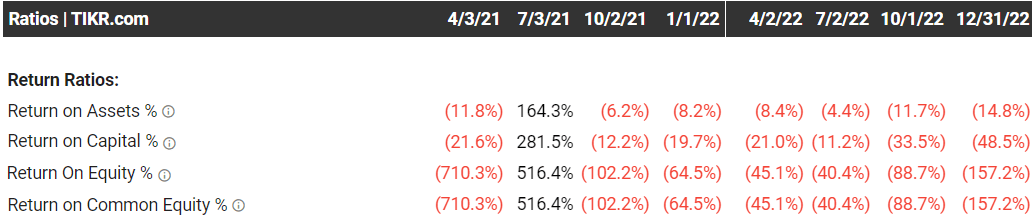

Indeed, despite rather steady revenue and net income levels over the years, we can see a sharp decline in both in the recent years. Revenue and net income have reached some of the worst figures since IPO, showing the company struggles to sell more while spending more. This means the company is inefficient, probably due to a wrong allocation of resources in my opinion. We will come to it later, but it is likely that management's focus is more on winning legal battles against potential large long-term customers (harming growth prospects) than on making the company more cost-effective and reaching higher growth levels. Indeed, when we zoom into 2021 and 2022, the years where revenue exceeded $100m, we observe negative and deteriorating ratios, indicating the company struggles to turn profitable over time.

{kind=link}

The exception is the 2nd quarter of 2021 when we saw a spike in revenue, in part due to the execution of a comprehensive licensing agreement with SK Hynix. Interestingly, SK Hynix Inc. is one additional company that made it in the list of lawsuits from Netlist, accused of also violating patents (more on that later).

In my opinion, the company falls under the Strong Sell rating because it failed to capitalise on the revenue spike and remain profitable. Looking at the valuation side, my Strong Sell rating is further confirmed.

Indeed, the valuation metrics available on Seeking Alpha show that the stock is trading at a 2.5x premium in relation to the sector medians of 2.94x EV/Sales ((TTM)) and 2.88x ((FWD)).

Seeking Alpha

In my opinion, as described above, the lack of corporate efficiency and sustained financial growth do not justify a valuation at such a high premium. Looking ahead, it does not seem that the company has sufficient focus on improving its internal situation and continues allocating resources to legal battles with potentially large customers.

Legal Battles Affecting The Business' Long-Term Viability

Indeed, the already poor prospects of Netlist brand continue to take further hits as the management continues to sue large corporations such as Samsung Electronics, Alphabet and Micron Technology. Netlist's biggest good news in years was when a Texas court, the Eastern Federal District Court, ruled that Samsung must pay $300 million (equating to 5x TTM revenue of Netlist!) to the plaintiff for patents' infringement. Samsung appealed and the US Court of Appeals for the Ninth Circuit ruled in favor of Samsung last October.

These legal battles against large corporations could end in a short-term boost (in case of unlikely new favorable rulings) but the reputational damage suffered by Netlist could exclude it in the long run from new business opportunities to turn around the company.

Therefore Netlist's poor prospects comfort further my case for a Strong Sell.

Main Aspects That Could Invalidate my Strong Sell

The main risks to my stock shorting case are actually not from within the company, but external. Indeed, with the tensions between Taiwan and China, and the scarcity of chips, the U.S. CHIPS Act is looking to provide support, regulatory and financial, to chip manufacturers based in the U.S. Should Netlist receive support from the U.S. government, investors could pivot and enter the long trade of the stock. I see this as a minor risk still, as the U.S. government through the Commerce Department only participates up to 15% of project capital expenditures , unlikely to significantly provide a competitive edge to Netlist in relation to the larger U.S. chip manufacturers.

Another key risk could be the company winning its lawsuits against the corporations it is suing, as it would both boost its cash reserves but also open the door to a potential acquisition of the company by a larger chip manufacturer, eventually a foreign company aiming at gaining a foot in the U.S. market through Netlist, which would have both significantly improved its cash position and secured its patents through the lawsuits. This is of course possible, but it is unlikely that an acquirer would pay a 150% premium in relation to the sector median as discussed in the valuation section.

Bottom Line: The Stock is a Strong Sell

Netlist is a good candidate to open a short, with sufficient reasons to support the Strong Sell rating. Weak financial performance, unjustified valuation and lawsuits with former large clients altogether are a poor combination to justify fresh capital entering the long side of the stock trade.

Increased volatility due to the geopolitical situation around semiconductor chips and the U.S. CHIPS Act could invalidate the Strong Sell rating in the short term, but the fundamentals of the company since its IPO, persistent underperformance, and improper resource allocation in the company's business plan make this stock a Strong Sell.

For further details see:

Netlist: A Strong Sell Due To Weak Performance And Overvaluation