NVRO - Nevro: Economic Realities Too Deep To Ignore Downgrade To Hold

2023-09-01 15:54:03 ET

Summary

- Nevro Corp. shares have significantly underperformed, selling 57% lower than in 2021.

- The company's top-line momentum continues, but it faces economic challenges and lacks value creation for shareholders.

- As a positive, NVRO's Q2 FY'23 showed significant growth in painful diabetic neuropathy revenues.

- Net-net, revise to hold.

Investment updates

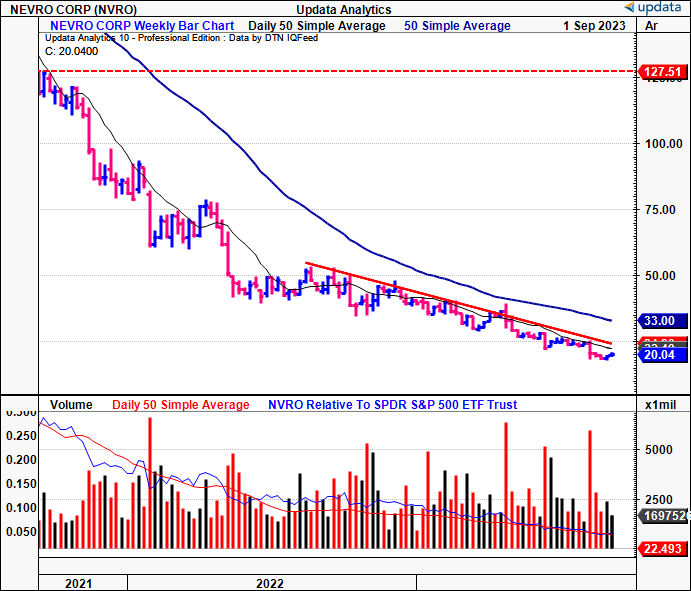

Shares of Nevro Corp. ( NVRO ) have underperformed by a significant margin since my December '22 publication recommending a Buy, and now sell 57% lower. As seen in Figure 1, NVRO has eroded an enormous sum of capital for investors since 2021, when it sold at $127/share. It now sells around the $26/share mark, at ~1.7x forward sales. Unfortunately, this price looks fair when reflected against the capital employed by NVRO and the earnings produced on said capital.

This report will deconstruct the latest investment updates for NVRO, and link this back to why I've revised the rating to a hold. Critically, top-line momentum continues for the company, and there are potential regulatory tailwinds via CMS' code changes in its proposed '24 rulings. However, these do not overcome the economic realities faced by NVRO's operations, notwithstanding the lack of value creation for shareholders. By all measures presented here, the historical trends look set to continue for some time, corroborating a revised rating to hold.

Figure 1. NVRO value erosion from highs of $127 to $26/share

{kind=link}

Critical updates to investment facts

NVRO Q2 FY'23 Insights

1. Operating walkthrough

NVRO put up $108.8mm in Q2 sales, reflecting a 4% YoY growth rate (including all FX adjustments). The company's U.S. revenues were up 4% to $92.9mm, with a significant contribution from its painful diabetic neuropathy ("PDN") segment. PDN sales were up 73% YoY - the main revenue growth driver - and clipped $19mm for the quarter. This was also ~18% of the company's permanent implant volumes. It pulled this to another operating loss of $25.8mm and a net loss of $0.69/share, flat on Q2 FY'22.

In terms of geographical distribution, U.S. permanent procedural growth was up 8% as compared to last year (driven by its PDN momentum). Whereas, it booked ex-U.S. revenues of $15.8mm, a growth of 5% (excluding ~100bps of FX headwind). Given the H1 FY'23 performance, management now projects a modest 1%-2% increase in global sales for the entire year. It looks to adj. EBITDA to range between negative $25mm and negative $28mm on this, a deeper loss than the $23.8mm clipped in FY'22.

The divisional highlights of NVRO's Q2 top-line is as follows:

- Its HFX iQ spinal cord stimulation ("SCS") platform (that includes the Senza SCS system) accounted for ~30% of permanent implant procedures, up from the 11% share it held in Q1 this year. Whilst NVRO didn't disclose specific sales for this segment, at 30% of procedural volume, this gets me to ~$89.8mm in Q2 revenues using the math provided on its PDN segment. Management expects this trend in procedural share to persist throughout H2. I'd remind investors the Senza system has been approved in Europe since 2010, in Australia since 2011, and received FDA approval in 2015, 8 years ago now.

- As mentioned, the PDN business was the headline for NVRO in Q2. PDN trials contributed to ~23% of total U.S. trial volume, up from 14% YoY. It also made up 18% of permanent implant procedures as mentioned earlier, getting to the ~$19mm in PDN in sales (up 73%).

- As a positive, recent efforts to broaden its PDN coverage have started to bear fruit. In June, Florida Blue , one of the largest commercial payers in Florida, extended its coverage of PDN. It now impacts 4.6mm insured lives. Additionally , Novitas and First Coast Service Options , 2 Medicare administrative contractors ("MACs"), have decided to retire their SCS local coverage determination ("LCD") to start providing coverage for both PDN and non-surgical back pain using Medicare National Coverage Determination ("NCD") as of July.

- This move will improve accessibility, 1) to SCS therapy for PDN, and 2) to NSBP patients with Medicare or Medicare Advantage health plans. Critically, this extended coverage affects c.24mm covered lives and expands health plan coverage of PDN to >205mm covered lives. This could absolutely be a tailwind for NVRO moving forward, especially given its recent growth in PDN sales, and percentage of revenue share. I'd be watching this very closely going forward, to see what potential impact the expanded coverage will have on its top-line.

Moving down the P&L, it pulled the $108mm to 68.4% gross, ~140bps compression on last year. In fact, it's further down the P&L and cash flow statements that the challenges to rating NVRO as an investment-grade company start to appear, as discussed below.

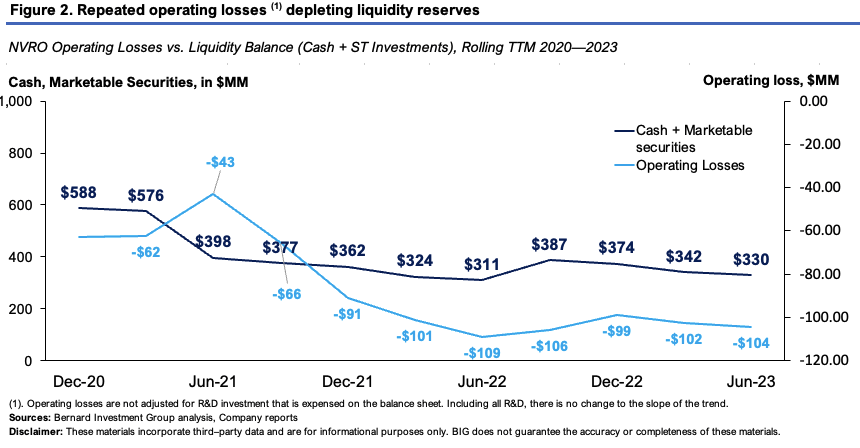

2. Economic leverage on capital employed

The company has produced a series of operating losses over the last 2.5 years, despite having its core products approved for around 10 years across all markets. This is proving to be a significant drag on liquidity, as shown in Figure 2. The rolling TTM operating loss is shown against the company's cash on hand plus marketable securities. Granted, the marketable securities are recorded at mark-to-market and are thus susceptible to changes in market value.

Nonetheless, cash on hand has tightened from $109mm in Q2 last year to $65mm in Q2 FY'23. Ultimately, I'd need to see this improve and see it start to produce some form of profitability to align with the core tenets of our equity holdings, that call for 1) high operating profits off capital employed, and 2) a return on capital investments of >12%. This supports a hold rating in my view.

{kind=link}

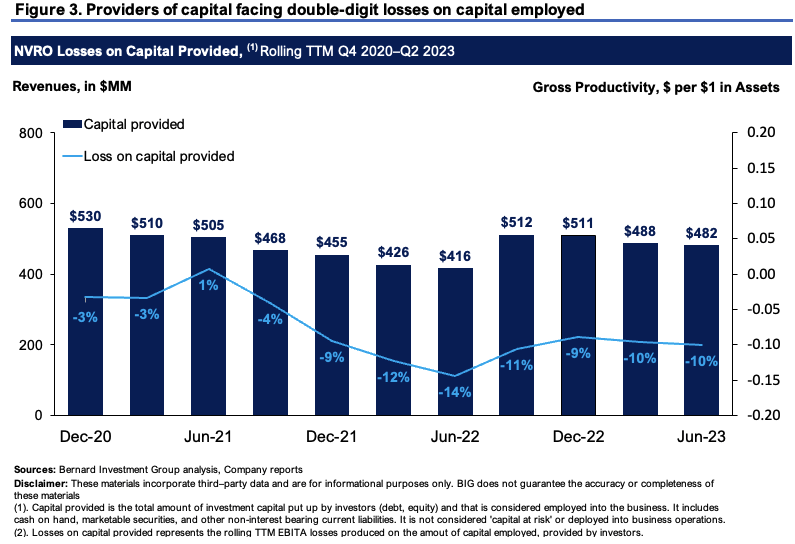

Figure 3 outlines the challenges of these figures with more granularity. NVRO's operating margins are persistently negative as a function of sales. However, the issues are deeper when checking the profits as a percentage of capital provided by investors.

Figure 3 outlines the pre-tax income produced on capital employed by investors (debt, equity) on a rolling TTM basis. It shows double-digit losses on investment since Q1 FY'22 and a loss on investment over the entire testing period. That is, $482mm of capital employed produced a 10% trailing loss in Q2, consistent across the last 4 rolling periods.

As far as value creation is concerned - this is not it. Instead, we have a situation where:

- Cash reserves are being depleted to finance steady-state (let alone growth) operations.

- Continued losses are produced on the capital employed in the business.

The company trades at compressed multiples (discussed later), and it would appear there is a valid reason why this is the case, based on this economic analysis.

{kind=link}

Valuation and conclusion

The stock sells at 1.7x sales , and this is a discount of 55% to the sector. It also sells at $2.62 in market value for every $1 in net asset value. The question is, is this discount fair in relation to 1) the assets, and 2) the earnings on such assets, NVRO is producing/can produce?

The data presented here today would suggest the 55% discount is, in fact, fair. How can we expect NVRO to trade at a premium when the capital it has been provided to deploy produces a series of economic losses on an ongoing basis?

If you were to invest a sum of cash into any form of capital - call it investment securities, tangible assets, business, fine art, wine, whatever - and it continued to produce double-digit losses every quarter for 2 years, would this be considered valuable? The answer is likely no, that is precisely why the market has rated NVRO at such a tight multiple to capital employed, in my opinion. At an EV of $600mm, the company sells at just 1.2x EV/Capital employed (600/482 = 1.2x), telling me that most of the company's growth prospects may already be priced in.

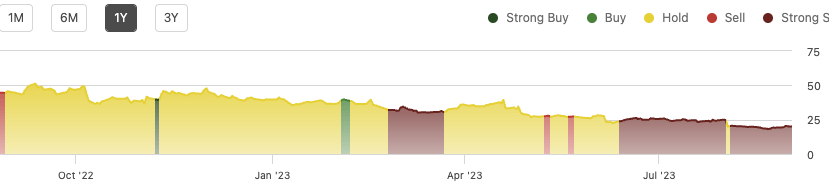

This supports a neutral view, and this sentiment is shared by the quant system which rates NVRO a 'strong sell', as seen below.

Figure 4

{kind=link}

In short, whilst there have been notable progressions in top-line growth, procedural volumes, and potential regulatory tailwinds, the economic realities for NVRO as an investment do not support a buy rating in my view. Looking at the post-tax numbers produced on the capital provided by investors, there is a lack of value creation, likely why the stock sells at such a breadth from its previous highs in 2021. Net-net, I revise NVRO a hold.

For further details see:

Nevro: Economic Realities Too Deep To Ignore, Downgrade To Hold