NVRO - Nevro: Potentially Better Than Traditional SCS Treatment For Pain And Undervalued

2023-05-09 22:13:10 ET

Summary

- Nevro is a company dedicated to the design and manufacture of medical devices.

- I believe that further news about the efficacy of the product, sufficient marketing, and internationalization efforts could bring significant FCF growth and stock price appreciation.

- In the last quarterly report, management made a comment about the work in the Costa Rica facility. In my view, further integration could bring significant FCF margin expansion.

- Further publications about the SENZA-NSRBP studies will likely bring more attention from market participants. For instance, the company promised full manuscripts for the year 2023.

Nevro Corp. ( NVRO ) reports a significant amount of cash for further research and marketing efforts, and the SENZA product line appears more efficient than traditional SCS treatment for patients with chronic pain. I believe that further vertical integration, new investments in the Costa Rica facility, and successful internationalization could bring significant FCF generation. Even taking into account risks from regulators, competitors, or lack of adequate financing, in my view, NVRO stock appears undervalued.

Nevro: Useful Product And Developing Vertical Integration

Nevro is a company dedicated to the design and manufacture of medical devices , focused on generating improvements in people's quality of life and changing the standard of treatment for patients with chronic pain.

The products that the company sells include platforms for the stimulation of the spinal cord or devices of a high and complex technological development in order to relieve pain in specific areas of the body. Senza, sold by Nevro, arrived in the United States in 2015, and it had already been present since 2011 in some parts of Europe and Australia.

The percentage of sales in the United States is not much higher than sales in the rest of the world. 2022 sales in the US stood at $348.2 million nationally and only $58.2 million in the rest of the world. With slight variations, this statistic has remained similar for at least the last 5 years. Considering net sales growth in 2018, 2019, 2020, 2021, and 2022, I believe that Nevro is a must-follow stock .

{kind=link}

Right now, the company's developments aim to perfect the SENZA product line, intended mainly for the treatment of back or leg pain, postoperative back pain due to highly complex surgeries, or diabetic neuropathy. I believe that further news about the efficacy of the product, sufficient marketing, and internationalization efforts could bring significant FCF growth and stock price appreciation.

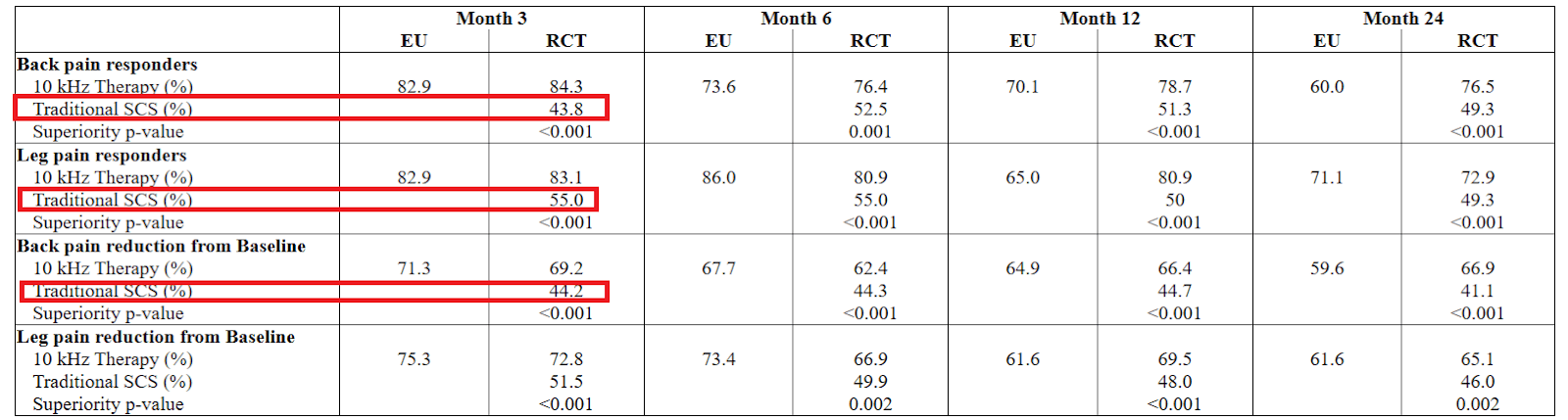

The company designed a number of trials in the United States and Europe. Without going into very specific details about the trials, in my view, it is worth noting that the 10 kHz therapy proposed by Nevro is way more efficient than the traditional SCS treatment.

Among the 198 chronic pain patients who were randomized for treatments, 171 had a successful therapy evaluation phase, or trial phase, and were implanted with an SCS system. The study was designed as a non-inferiority trial and met its primary and secondary endpoints. Statistical analysis also demonstrated the superior efficacy of 10 kHz Therapy over traditional SCS therapy for all primary and secondary endpoints. Source: Quarterly Report

{kind=link}

It is also worth noting that Nevro is trying to vertically integrate the assembly of IPG’s, peripherals, and other manufacturing related activities to reduce its dependence on third-party manufacturers. In the last quarterly report, management made a comment about the work in the Costa Rica facility. In my view, further integration could bring significant FCF margin expansion.

We plan on conducting these manufacturing activities in a facility in Costa Rica. The integration process was completed in mid-2022, and we received approval from the FDA for the manufacture of our Senza system in the Costa Rica facility. Source: Quarterly Report

We have incurred and may continue to incur significant capital expenditures and implementation costs to initiate the manufacturing activities in our Costa Rica facility. Source: Quarterly Report

Balance Sheet

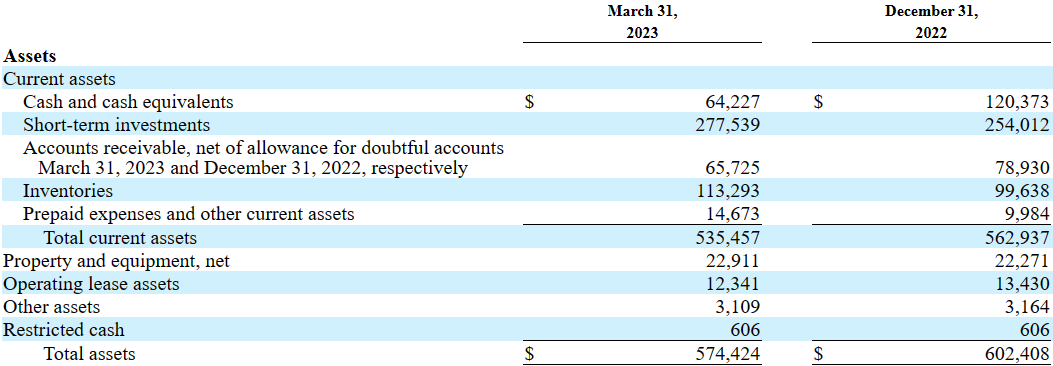

As of March 31, 2023, Nevro reported cash and cash equivalents worth $64 million, short-term investments of $277 million, and accounts receivable close to $65 million. In my view, further study of the short-term investments revealed that we can use them for deduction from the enterprise value.

{kind=link}

Management also reported inventories of $113 million, 13% more than what the company reported in 2022. Prepaid expenses and other current assets were equal to $14 million, 46% more than that in December 2022. In sum, total current assets are equal to $535 million, much more than the total amount of current liabilities.

Finally, with property and equipment worth $22 million and operating lease assets of $12 million, total assets stood at $574 million, implying an asset/liability ratio of 2x.

{kind=link}

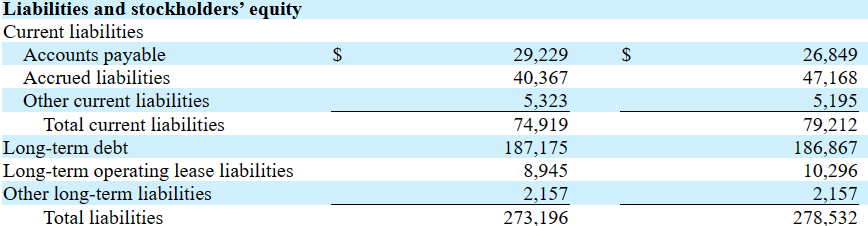

With accounts payable worth $26 million, 16% less than that in December 2022, accrued liabilities stood at $47 million. Besides, with long-term debt of $186 million, long-term operating lease liabilities were close to $10 million, -33% less than that in 2022. Finally, total liabilities were equal to $278 million.

{kind=link}

Expectations From Market Analysts Include 2025 EBITDA Growth And Sales Growth

I believe that investors will appreciate receiving some information about the expectations of other market analysts. Under market estimates, Nevro would deliver sales growth in 2023, 2024, and 2025. Besides, 2025 EBITDA would stand at $42 million, which means that shareholders may enjoy triple digit EBITDA growth. 2025 net sales would be $533 million, and the EBITDA margin would be close to 7.9%.

{kind=link}

Assumptions Under My DCF Model Would Imply A Valuation Of $34 Per Share

Under my financial model, I assumed that management will be able to maximize its market share in what refers to the treatment of back pain, and improve the operating margin of the Senza platform. I also believe that Nevro will successfully develop an effective communication strategy to present the performance levels and benefits of 10 kHz therapies to patients.

Considering that the company received significant product approvals in 2021 and 2022, I assumed that many doctors and potential clients do not know a lot about the Senza systems. Under these circumstances, successful marketing strategies could bring significant revenue growth.

{kind=link}

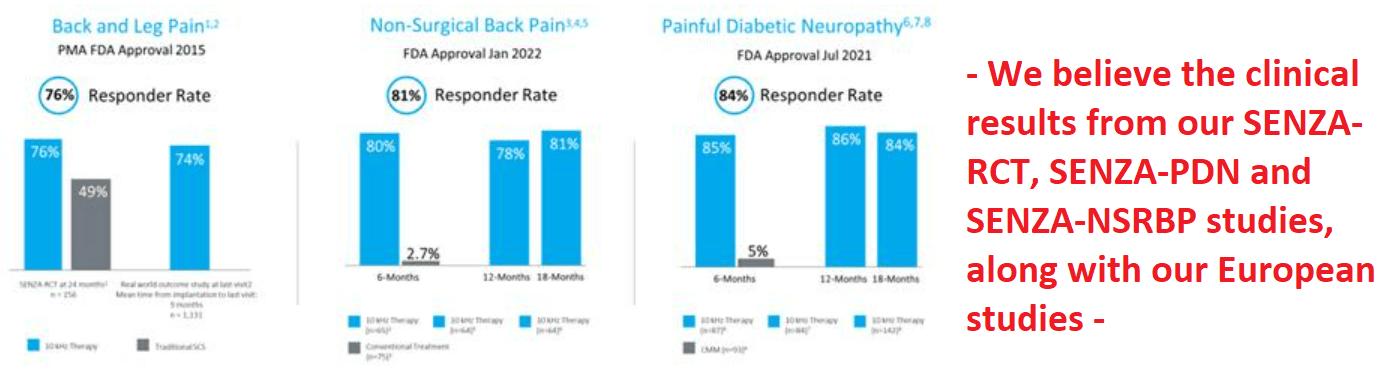

In my view, as soon as potential patients and medical professionals learn about the responder rate reported in clinical trials, net revenue may trend up. We are talking about responder rates ranging from 76% in back and leg pain, 81% in non-surgical back pain, and 84% in painful diabetic neuropathy.

{kind=link}

It is also worth noting that the company is targeting a market of more than $2 billion, and currently net revenue is close to $401-$500 million. Thus, I believe that the potential for revenue growth is significant.

The 2022 global market for SCS therapy was estimated to be approximately $2.3 billion. We believe, however, that the superiority of 10 kHz Therapy over traditional SCS therapies will allow us to continue to capitalize on the addressable trunk and limb chronic pain market, which is estimated to be approximately 14% penetrated in the United States, as well as expand the SCS market by treating other pain-related indications, such as PDN and NSBP, among others. Source: 10-K

I also believe that further publications about the SENZA-NSRBP studies will likely bring more attention from market participants. For instance, the company promised full manuscripts for the year 2023.

In February 2022, the SENZA-NSRBP 12-month results were published online in the Journal of Neurosurgery: Spine. We expect that this 12-month publication will be used to seek expanded payor coverage for this patient cohort. Finally, in January 2023, we presented the full 24-month results from the SENZA-NSRBP study at the 2023 NANS conference, and publication of the full manuscript is planned in 2023. Source: 10-K

Finally, I assumed that investors and investment professionals will continue to help Nevro finance future research and development of its products, and scalability will likely lower the cost of production. To these key points we must add the possibility of developing into new markets in the treatment of other chronic pain, mainly non-operative back pain and painful neuropathies.

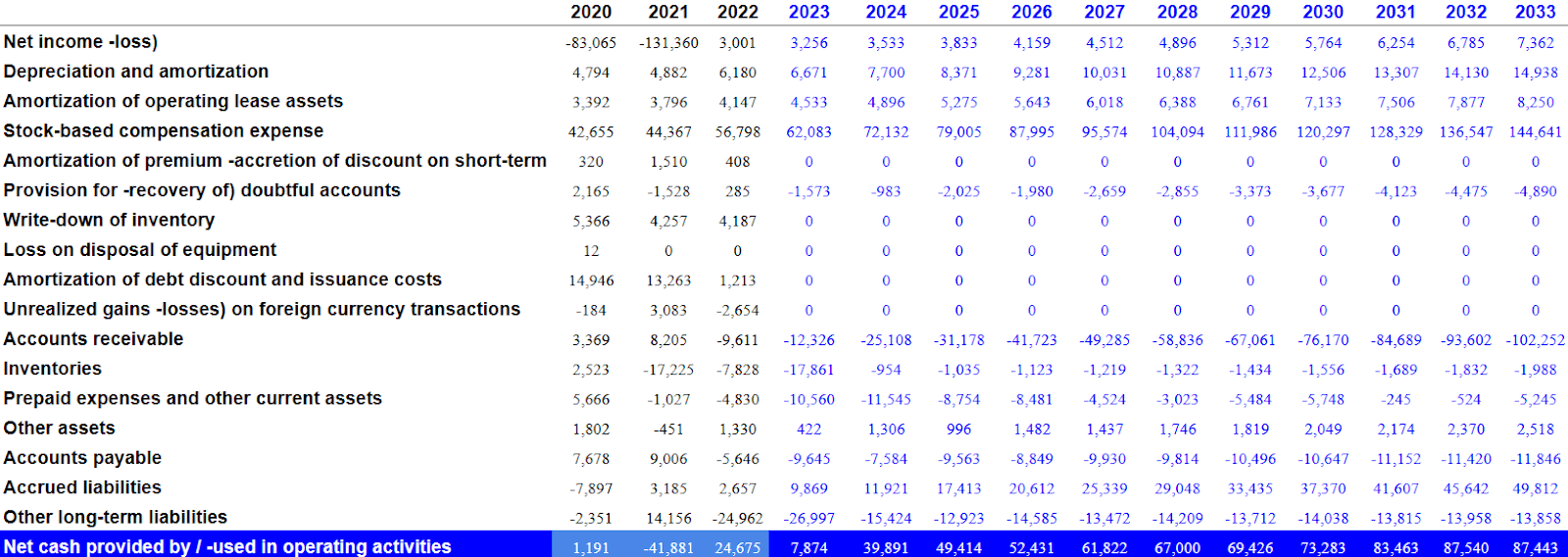

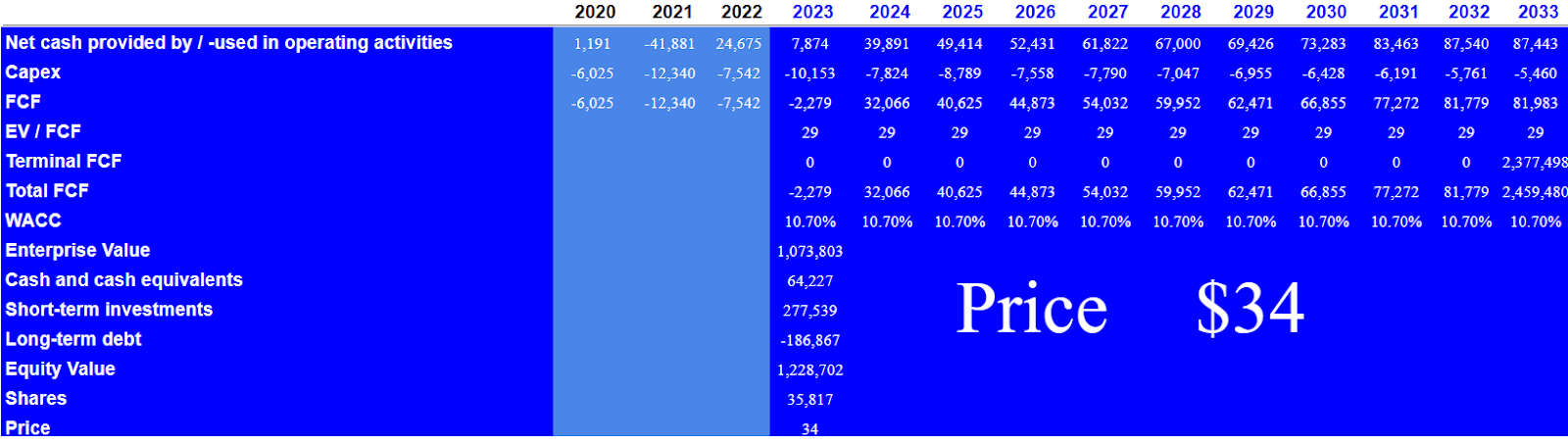

My cash flow model included 2033 net income of $7 million, depreciation and amortization close to $14 million, amortization of operating lease assets of $8 million, and stock-based compensation expense close to $144 million.

Also, with accounts receivable of around -$103 million, changes due to inventories of -$2 million, prepaid expenses and other current assets close to -$6 million, changes due to accounts payable of -$12 million, and accrued liabilities of around $49 million, CFO would be close to $87 million. Finally, with 2033 capex of -$6 million, 2033 FCF would be close to $81 million.

{kind=link}

I also assumed EV/FCF of 29.55x, which appears a conservative valuation for a company that traded at more than 51.55x in the past.

{kind=link}

By assuming a WACC of 10.755%, I obtained an enterprise value of $1.073 billion. Also, adding cash and cash equivalents of $64 million and short-term investments worth $277 million, and subtracting long-term debt of -$187 million, I obtained an equity valuation of $1.228 million, which implied a fair price of $34 per share.

{kind=link}

Large Competitors

Due to the recent operating authorizations the company has received, the main competitors for Nevro are Medtronic ( MDT ), Boston Scientific ( BSX ), and Abbott Laboratories ( ABT ). Saluda and Biotronik are expected to join the competition in this market in 2023. Many of these competitors have greater resources than Nevro as well as a recognized track record and a historical relationship with large institutions and governments.

Risks

I believe that future acceptance of the 10kHz therapy partly depends on the communication capacity. A growing rejection of the therapy or the inability to demonstrate its benefits over the developments of its competitors may mean a major setback to the company's operations.

I also believe that the resources and market positioning of some of its competitors may complicate Nevro's presence in the market. If competitors deliver other products that are even less efficient than Senza, but they invest more in marketing, Nevro may even lose market share.

Besides the risks inherent to operating internationally, there are risks specific to this type of market, governed by a large number of laws in relation to the uses, distribution, and manufacture of products and devices in each region, which may mean delays or restrictions in the activities of the company.

Nevro may be in trouble if management cannot access capital to carry out new developments. As a result, without cash in hand, I believe that investors would most likely sell their shares, which may lead to stock price declines.

Conclusion

With a significant amount of cash in hand and a treatment that appears significantly better than traditional SCS treatment, I believe that Nevro will likely bring significant revenue growth in the next decade. If the vertical integration efforts continue, Nevro makes further successful marketing efforts, and internationalization works out, FCF will likely trend up. There are several risks from lack of financing, competition, and regulations; however, I believe that the stock price could be higher.

For further details see:

Nevro: Potentially Better Than Traditional SCS Treatment For Pain And Undervalued