NGD - New Gold: A Better Year Ahead

Summary

- New Gold was one of the worst-performing gold miners last year for a second year running, down 34% for the year, which followed a 31% decline in the prior year.

- Unfortunately, 2023 hasn't been much better from a share-price performance standpoint, with the stock down 6% year-to-date, underperforming the GDX.

- The good news is that NGD has a better year ahead at both operations after a tough 2022, with output set to increase to 395,000 gold-equivalent ounces at the mid-point.

- At a share price of $0.90, NGD remains reasonably valued at less than 3.0x cash flow, but with costs well above the industry average and a volatile gold price, I continue to see much better bets elsewhere in the sector.

It has been a rough Q4 earnings season for the Gold Juniors Index ( GDXJ ) and while New Gold's ( NGD ) Q4 results weren't terrible, they certainly left a lot to be desired, as did its annual results. The company reported annual production of ~347,100 gold-equivalent ounces [GEOs] at all-in-sustaining costs [AISC] of $1,818/oz, translating to a negative AISC margin for the year. Although the Q4 results were a little better at Rainy River after unfavorable weather in Q4, weaker output at New Afton offset this, with just ~26,600 GEOs produced. Given the softer results, it's no surprise that New Gold reported negative free cash flow of $148.0 million, down from [+] $35.1 million in FY2021. Let's dig into the results a little deeper below.

Rainy River Mine (Company Website)

{kind=link}

Q4 & FY2022 Production

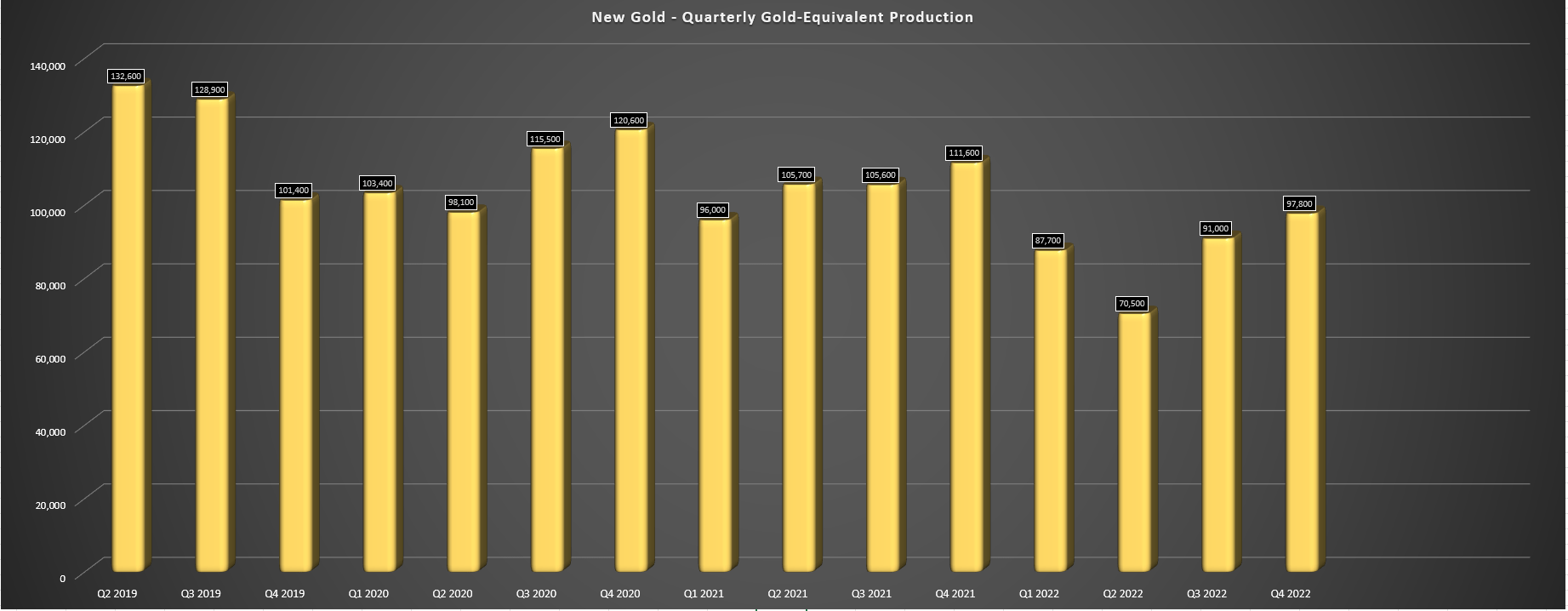

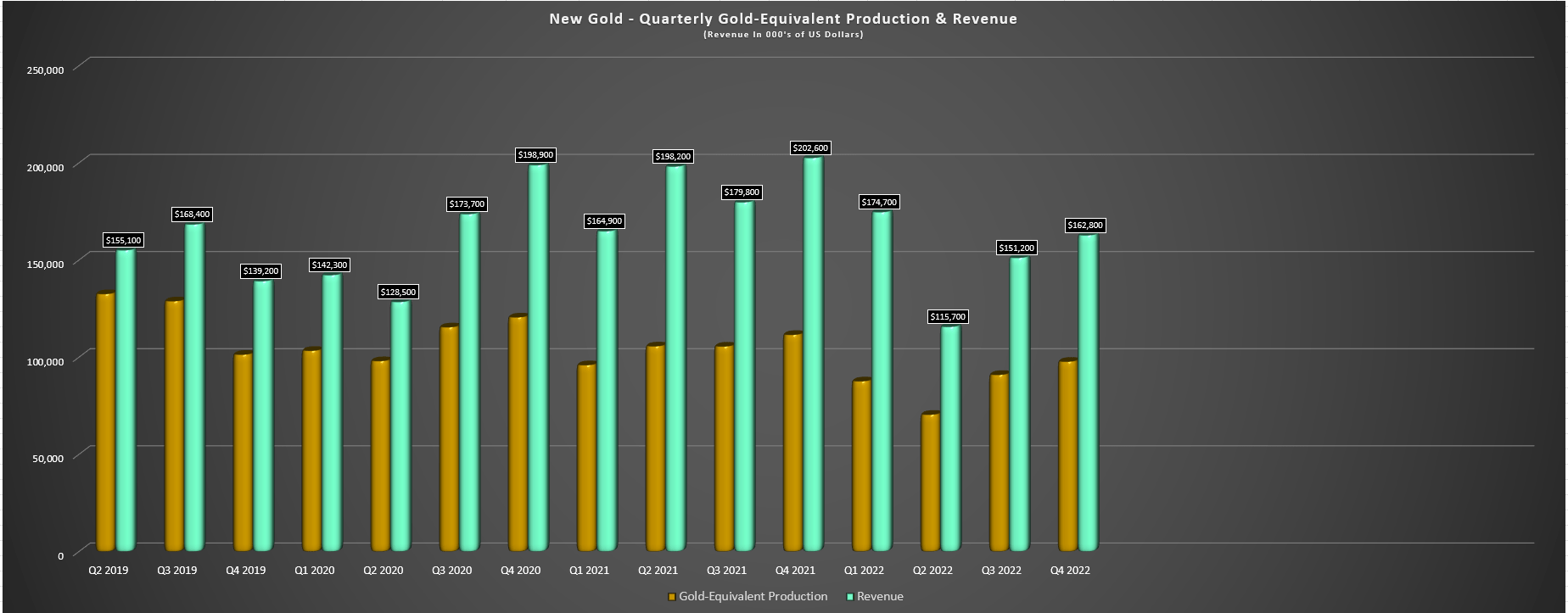

New Gold released its Q4 and FY2022 results last month, reporting quarterly production of ~97,800 GEOs, a 12% decline from the year-ago period. The company noted that lower output relates to fewer tonnes mined and processed at New Afton plus much lower copper grades (0.57% vs. 0.67%), partially offset by much better recovery rates in the period. New Gold's relatively weak consolidated Q4 production could not make up the shortfall from earlier in the year (flooding in the Rainy River open pit), and the result was that annual production came in 15% short of the company's initial FY2022 guidance midpoint of 410,000 ounces. This severely affected unit costs, which also missed by a mile.

New Gold - Quarterly GEO Production (Company Filings, Author's Chart)

{kind=link}

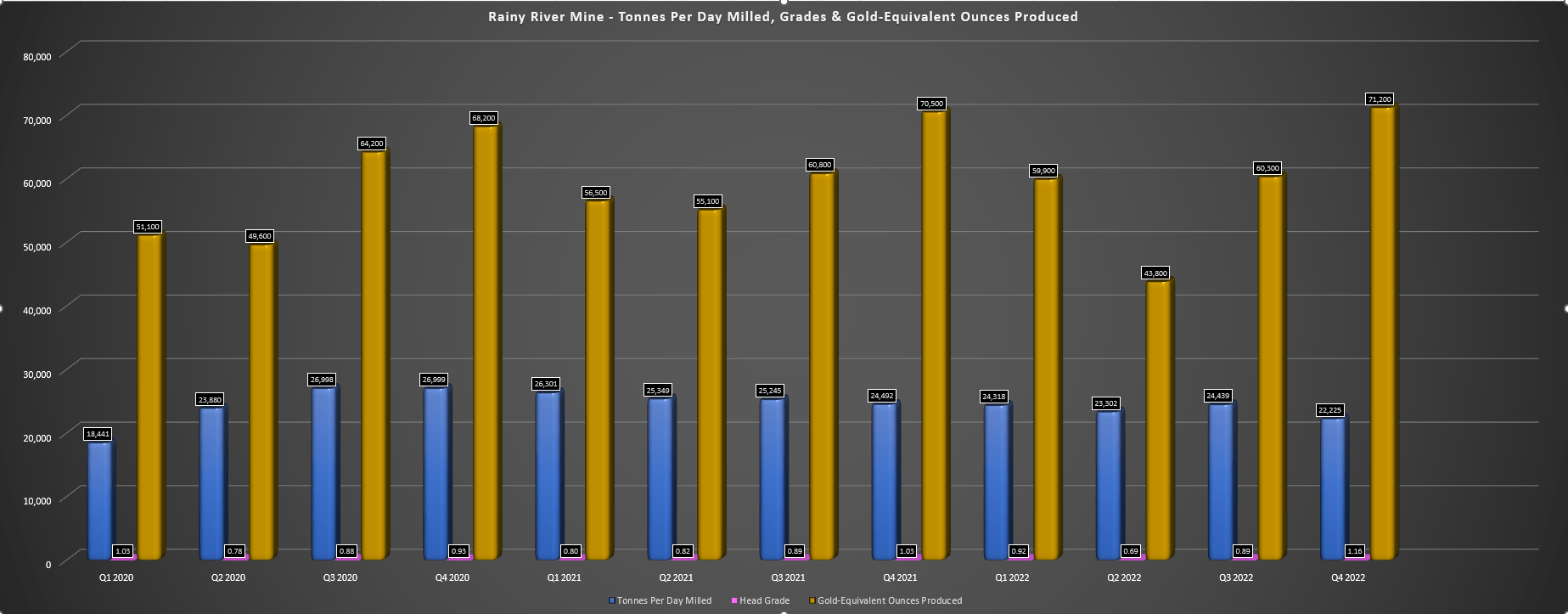

Beginning with Rainy River, the Ontario mine had a disappointing year overall with annual production of ~235,200 ounces at $1,605/oz, a clear miss vs. its initial guidance midpoint of 280,000 ounces at $1,320/oz. Although the annual performance doesn't inspire much confidence, it's important to note that this was mostly weather-related, with the heavy rainfall causing in-pit flooding that limited access to ore zones. Additionally, tonnes processed came in below expectations in Q2 because of having to process harder ore from North Lobe. That said, Q4 was much better with ~71,200 GEOs produced, the mine's best performance in years on the back of improved head grades with some early contribution from higher-grade underground ore (Intrepid Zone).

Rainy River - Quarterly Key Operating Metrics (Company Filings, Author's Chart)

{kind=link}

At New Afton, the softer annual performance (~26,600 GEOs vs. ~41,100 GEOs) can be attributed to having to supplement the mill with lower-grade surface stockpiles due to lower mining rates, and much lower throughput. Fortunately, 2023 is expected to be much better as the company ramps up to consistent 8,000 tonne per day mining rates at B3 and we see the first contribution from the higher-grade C Zone (~0.70 grams per tonne of gold and ~0.75% copper). This is expected to result in a dramatic improvement in unit costs vs. AISC of $1,870/oz and $2,044/oz, respectively (Q4-22/FY2022).

Costs & Margins

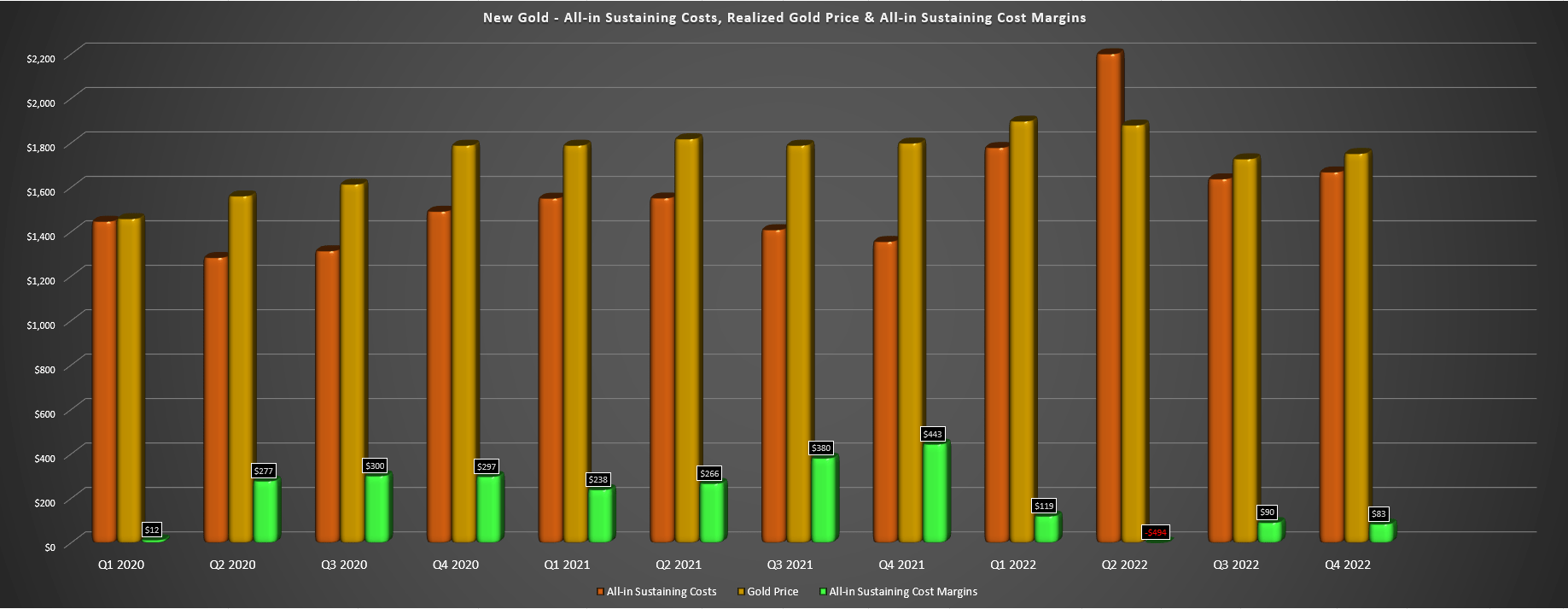

Moving over to costs and margins, the results didn't come anywhere near meeting investors' expectations, with consolidated FY2022 AISC of $1,668/oz. This represented ~28% higher costs relative to the industry average of ~$1,300/oz. It also represented a nearly 10% miss vs. the guidance midpoint of $1,520/oz. Although this wasn't entirely company-specific as the sector suffered from inflationary pressures (New Gold called out grinding media and fuel), the mid-year set back at Rainy River certainly didn't help, with much lower gold sales than planned leading to a lower denominator.

NGD - Quarterly AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

Looking at Rainy River in more detail, the mine's AISC came in $1,605/oz for the year, a disappointing result given that we were supposed to see a marked improvement in costs this year. The higher costs aren't overly surprising given that it's a relatively high-volume operation (~24,000 tonnes per day). However, Q4 AISC came in at a much more respectable cost of $1,467/oz with the asset starting to benefit from higher-grade ore from the Intrepid Zone. The other good news is that diesel prices have pulled back from their 2022 highs, suggesting a minor tailwind as well headed into 2023.

Rainy River - Actual & Forward AISC Estimates (Company Filings, Author's Chart)

{kind=link}

Unfortunately, given the much higher costs and limited cooperation from the gold price, AISC margins fell sharply year-over-year, from $382/oz to $202/oz for the year. While Q4 2022 wasn't much better with AISC margins of $281/oz, we should see a slightly better Q1 2023 report with an average realized price of ~$1,850/oz, with a further boost to revenue from a copper price just shy of $4.00/lb. Plus, industry-wide commentary suggests we may be past peak inflation, and the worst is in the rearview mirror. One example is Peter Hardie, CFO of Equinox Gold ( EQX ).

"On costs, our views that inflation is peaked. But the cost will stay elevated through the year. And you can see that reflected in both our cash and sustaining costs."

- Equinox Gold, Q4-22 Conference Call

In addition, Ryan Gurner of Northern Star (NESRF) stated the following in its fiscal Q2-23 (CYQ4-22) Call:

"We're not seeing significant cost reductions, albeit we are seeing some reduction. So, for instance, we're seeing it on our energy prices, particularly diesel. And also some of our input costs that are indexed around steel prices."

- Northern Star Resources, Fiscal Q2-23 Conference Call

Let's look at New Gold's FY2023 outlook below:

2023 Outlook

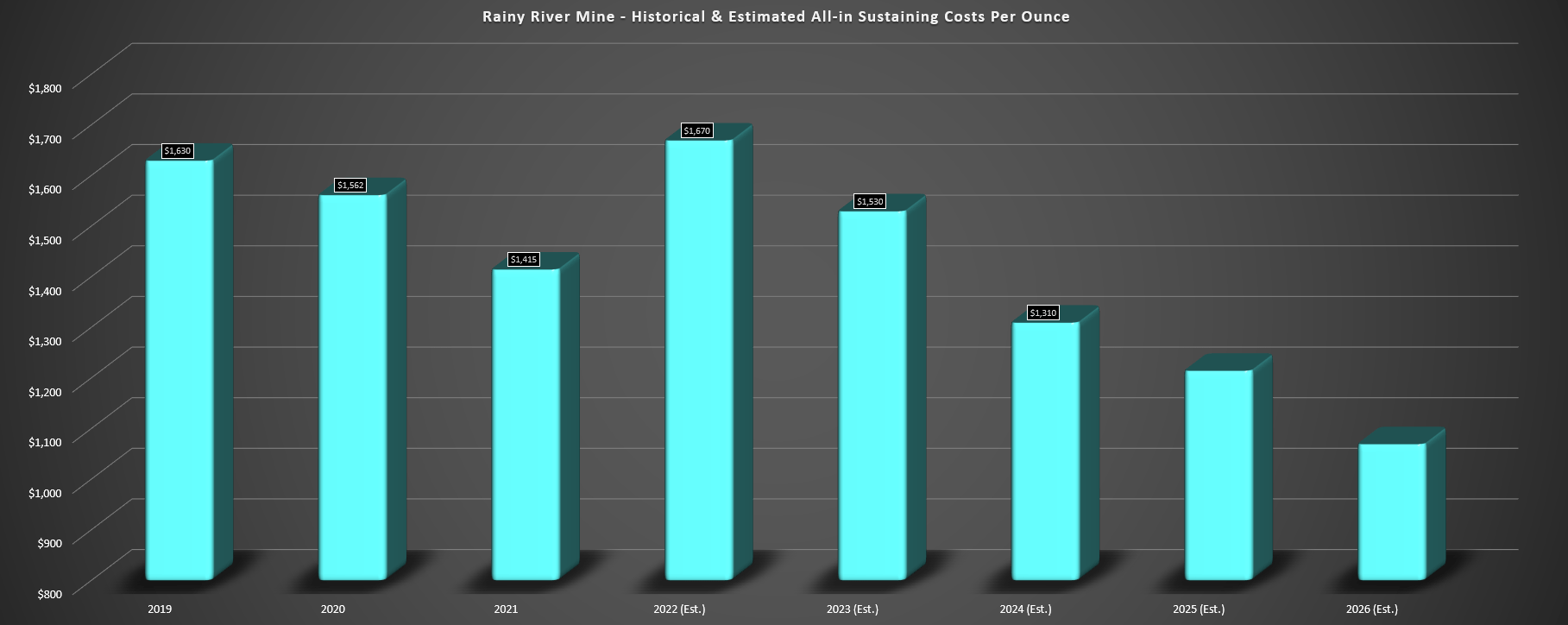

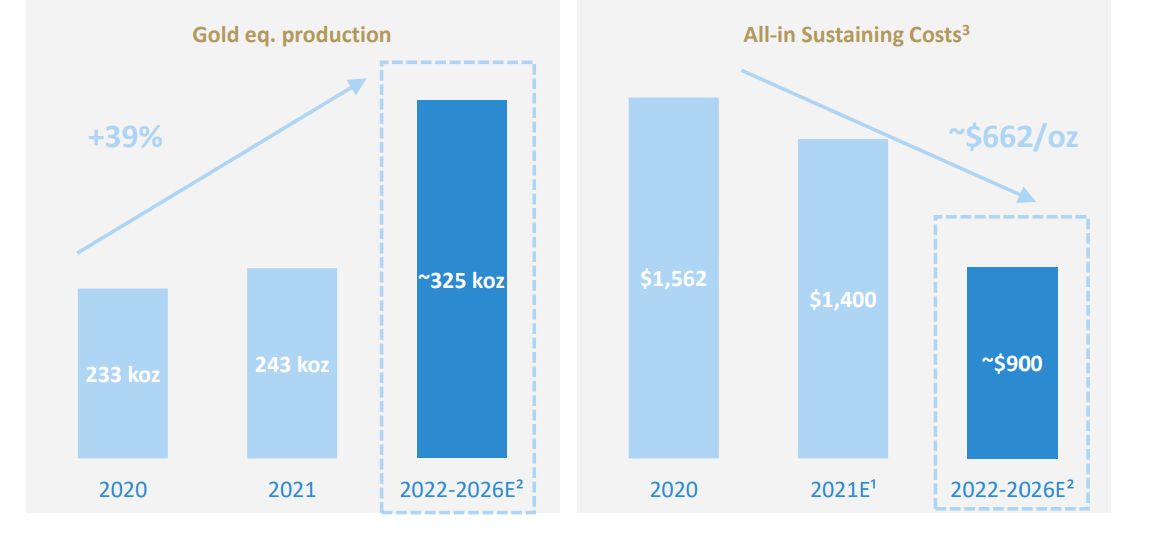

Assuming we don't see any hiccups this year, New Gold expects to produce 395,000 GEOs, helped by a stronger year at both operations. At Rainy River, the mine will benefit from a full year of production from the high-grade Intrepid Zone, and all-in sustaining costs are expected to dip to $1,525/oz at the mid-point (FY2022: $1,647/oz). Unfortunately, the 2023 cost guidance at Rainy River is significantly higher than the expected 2022 costs of $1,320/oz even though the mine will benefit from much higher grades hitting the mill. So, while investors can look forward to a steady downtrend in AISC at Rainy River, the previous AISC estimates (~$900/oz from 2022 to 2026) are looking far too ambitious.

New Gold - Quarterly Revenue (Company Filings, Author's Chart) Rainy River - Previous AISC Estimates (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Regarding revenue and cash flow, FY2023 is shaping up to be a better year (FY2022 revenue: ~$605 million), but it will be second-half weighted and New Gold will not report positive free cash flow this year with significant capital spending of $290-$350 million. However, we should see an improvement from FY2022 (cash outflow of $138.0 million), with a less than $100 million outflow if both metals prices cooperate. As for 2024, we should see a dramatic improvement and a return to positive free cash flow with the C-Zone and Intrepid both in production for the full year. This is because both operations will enjoy much higher margins, combined with reduced sustaining capital. In summary, there is a light at the end of what's been a long and winding tunnel for New Gold shareholders.

Valuation & Technical Picture

Based on ~687 million fully diluted shares and a share price of US$0.94, New Gold trades at a market cap of ~$650 million, but has ~$400 million in long-term debt. As the chart below shows, the stock has traded at a historical cash flow multiple of ~4.8 (10-year average), and it's currently trading at ~2.6x FY2023 cash flow estimates. Although this is a very reasonable valuation, it's not surprising that the stock trades at a discount to the peer average with industry-lagging margins and sub-par execution over the past couple of years, even if it has been a challenging operating environment.

Using what I believe to be a more conservative multiple of 3.5x cash flow and current cash flow per share estimates ($0.37), I see a fair value for the stock of US$1.30. Although this represents a 38% upside from current levels, I require a minimum 40% discount to fair value to justify starting new positions in small-cap miners, and especially those with razor-thin AISC margins. If we apply this discount to NGD's fair value of US$1.30, this means that the stock would need to decline below US$0.78 to move into a low-risk buy zone. Obviously, the stock doesn't need to decline this far, and there's no guarantee that it pulls back this far. However, this is what I would need to become more interested given that it's a high-risk name that isn't paying me to hold it (regular dividends), unlike other miners.

Finally, regarding the technical picture, NGD has resistance at US$1.04 and no strong support until US$0.67. This corroborates the view that the stock is not in a low-risk buy zone currently, with just $0.10 in potential upside to resistance and $0.27 in potential downside to support, translating to a reward/risk ratio of 0.37 to 1.0. Based on the technical picture and a minimum reward/risk ratio of 6.0 to 1.0 to justify starting new positions, the ideal buy zone for NGD is below US$0.75, so I have little interest in the stock at current levels, even if it is well off its highs.

Summary

While 2023 will be a better year with New Gold up against easy year-over-year comps and the copper price is certainly helping it, this has turned into a 2024 cash flow story vs. a 2023 story, and I'm not sure that the stock will be able to outperform the index with another year of negative free cash flow. Plus, other names sector-wide with lower-risk profiles continue to trade at very attractive valuations, with one example being Osisko Gold Royalties (OR) that continues to put up record numbers and trades at just 1.0x P/NAV, and trades 30% below what I believe to be fair value (US$18.50). So, for investors anxious to buy the dip, I think one can do better than NGD, and I see i-80 Gold (IAUX) and Osisko GR as more attractive bets.

For further details see:

New Gold: A Better Year Ahead