NGD - New Gold: A Turnaround Story At A Reasonable Price

2023-08-17 05:53:23 ET

Summary

- New Gold reported solid Q2 results with a 45% improvement in quarterly production and a 60% increase in revenue.

- The company's costs and margins improved, with all-in-sustaining costs dropping and all-in-sustaining cost margins improving.

- In this update, we'll look at whether NGD stock is nearing a low-risk buy zone yet, and why it's one of the better turnaround stories sector-wide.

We're nearly through the Q2 Earnings Season for the Gold Miners Index ( GDX ) and it was a mediocre reporting period overall, with one-time headwinds (severe weather, power outages, ongoing strike) affecting production levels at some mines and rising operating costs, even if inflationary pressures have eased a little from the double-digit inflation experienced last year. Unfortunately, this resulted in limited benefit from record gold prices from a margin standpoint, with names like Coeur Mining ( CDE ), First Majestic Silver ( AG ) and Iamgold ( IAG ) reporting razor-thin margins. However, New Gold ( NGD ) was one company that reported solid operating results which I covered one month ago , noting that while the stock was reasonably valued, it was difficult to justify paying up for the stock above US$1.20 per share.

Since that time, we've seen a 20% drawdown in NGD which is partially due to the sector-wide correction. That said, the stock remains a turnaround story, with an even better 2024 on deck with commercial production from the C Zone barely 12 months away, and a shift to being free cash flow positive. Let's take a closer look at its Q2 2023 financial results below:

All figures in United States Dollars unless otherwise noted.

Q2 Production & Sales

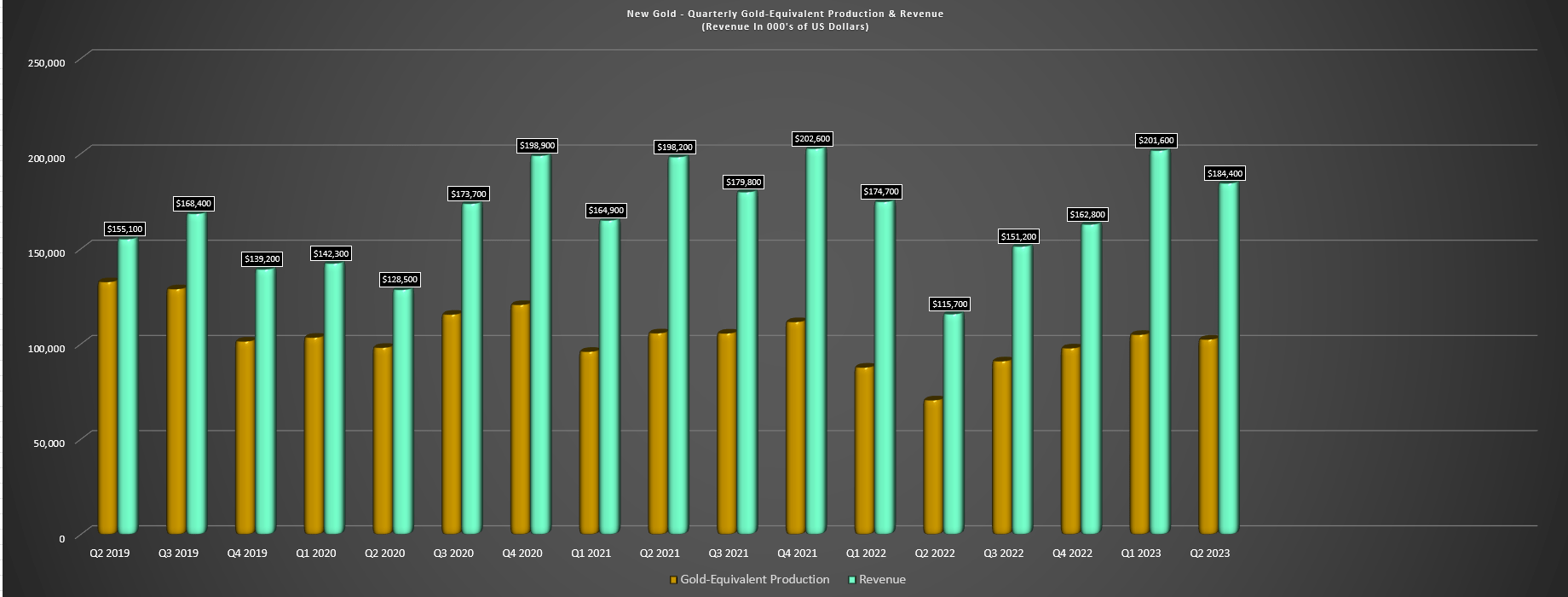

New Gold released its Q2 results last month, reporting quarterly production of ~102,400 gold-equivalent ounces [GEOs], a 45% improvement from the year-ago period. The significant increase in quarterly production can be attributed to easy year-over-year comparisons with heavy rainfall and flooding affecting Rainy River's production in Q2 2022 and the completion of Lift 1 mining at its New Afton Mine in British Columbia. The good news is that these results are here to stay and production should rise over 10% vs. its FY2023 guidance midpoint looking out to 2025. This is because New Gold will benefit from much higher grades at its C-Zone (New Afton) as well as higher grades from now on at Rainy River, with the asset expected to become a consistent ~350,000 ounce gold producer (2024-2028) at much lower costs. And this combination of margin expansion and higher production supports a compelling turnaround story here.

New Gold - Quarterly GEO Production & Revenue (Company Filings, Author's Chart)

{kind=link}

Digging into the production results a little closer, we can see that New Gold's production improved materially on a year-over-year, and the higher gold price in the period contributed to much better sales performance as well. In fact, revenue was up ~60% year-over-year to $184.4 million, with the increase in the gold price ($1,970/oz) and higher sales volumes more than offsetting the softer copper price in the period ($3.61/lb vs. $3.97/lb). At Rainy River, the higher production was driven by improved grades and recoveries, with an average feed grade of 0.97 grams per tonne of gold (Q2 2022: 0.69 grams per tonne of gold) and a 100 basis point improvement in recoveries. This contributed to lower costs year-over-year when combined with reduced sustaining capital, with all-in sustaining costs of $1,725/oz, down from $1,925/oz in Q2 2022.

New Gold Operations (Company Website)

{kind=link}

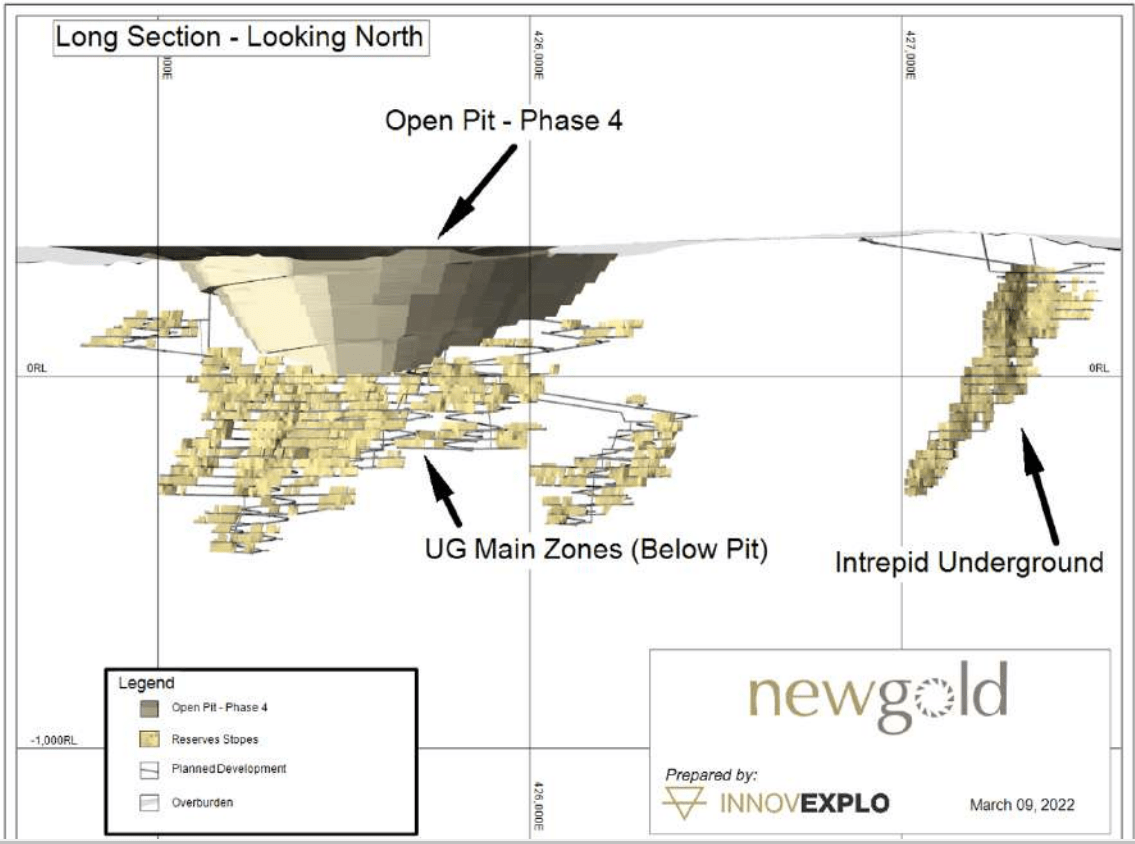

Besides the better operating performance at Rainy River with ~61,400 ounces produced in the period, the mine was free cash flow positive, with $16.6 million in mine-site free cash flow year-to-date. New Gold noted that its mining sequence was optimized to allow for a more consistent production profile and that it benefited from lower diesel prices, which helped to contributed to reduced mining costs in the period ($3.16/tonne vs. $4.01/tonne). Unfortunately, this was partially offset by higher processing costs of $11.00/tonne with higher costs related to mill maintenance. Finally, the company noted that after internal evaluations; it plans to defer the in-pit portal for the Main Zone and access from the underground Intrepid Zone. This is expected to be more efficient and reduce haulage distance, and it's also encouraging to know that underground grades and tonnes are reconciling well at Rainy River UG to date.

Rainy River 2022 TR - Company Filings

{kind=link}

Moving over to New Afton, it was a solid quarter here as well, with ~41,000 GEOs produced, up 52% from the year-ago period. This was driven by higher copper and gold grades 0.72 grams per tonne and 0.78%, respectively, and much better recoveries for both metals. And while the lower copper price was a slight drag in the period, this was more than offset by the higher sales volumes and lower sustaining capital with New Afton's AISC improving to $1,299/oz vs. ~$3,222/oz in Q2 2022. Just as important for the bigger picture, the C-Zone advanced 1,415 meters in Q2, up from 1,172 meters in Q2, benefiting from the completion of the vent raise, which contributed to higher development rates. So, assuming New Gold remains on schedule, investors can look forward to first ore from the C-Zone in Q4 with commercial production in H2-2024.

Costs & Margins

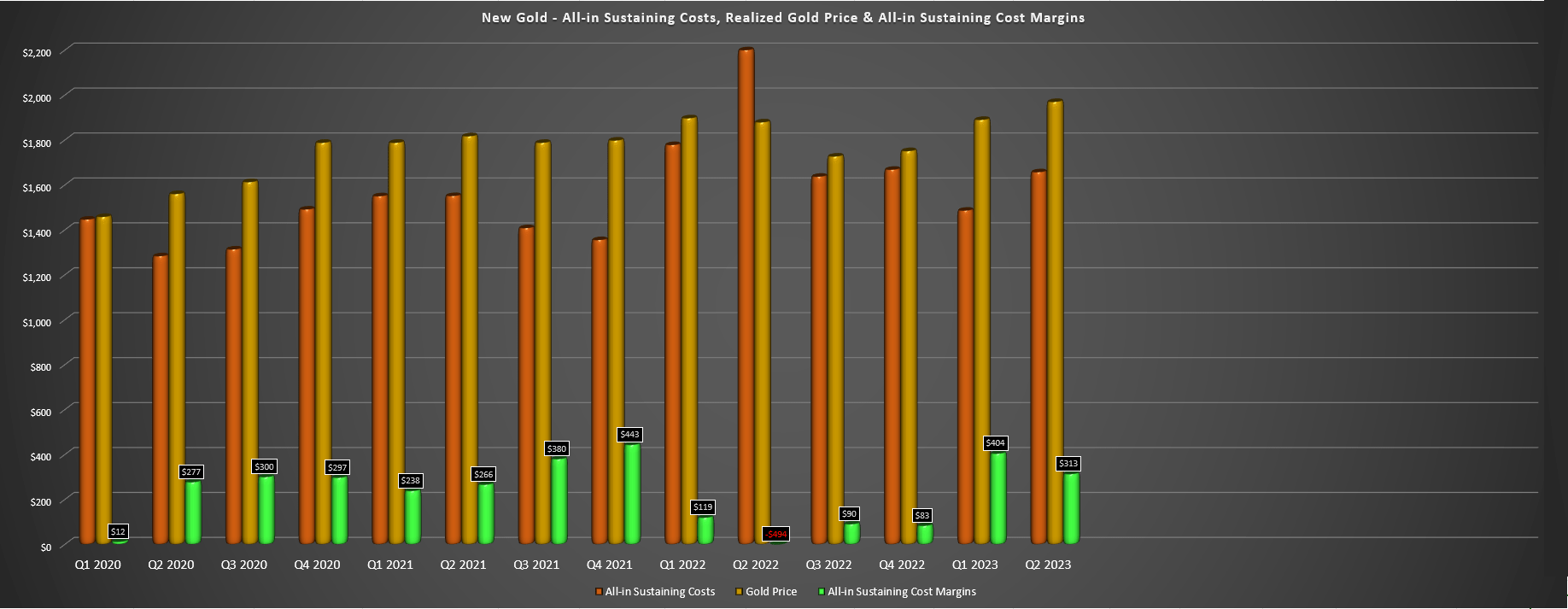

Moving over to costs and margins, New Gold's all-in sustaining costs [AISC] improved materially year-over-year, benefiting from higher sales volumes and more normalized sustaining capital spend vs. the $56.9 million spent in the same period last year. This resulted in AISC dropping from $2,373/oz to $1,657/oz, and AISC would have come in at even better levels at ~$1,556/oz if not for the ~6% difference in ounces produced vs. sold in the period (~96,200 vs. ~102,400). Given the higher average realized gold price combined with a more respectable AISC figure, all-in sustaining cost margins improved to $313/oz in Q2, up from [-] $494/oz in the year-ago period. And just as importantly, costs are tracking well against guidance of $1,555/oz at the mid-point, sitting at ~$1,566/oz year-to-date.

New Gold - AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

Unfortunately, despite the improved operating results, free cash flow was still negative in the period, with a cash outflow of $26.1 million. However, it's important to note that this can be attributed to elevated growth capital at New Afton, with its company-wide growth capital up ~90% year-over-year in Q2 to ~$36.0 million, offsetting most of the benefit from the lower sustaining capital in the period. However, with more relaxed capital spending in FY2024 (~$200 million vs. FY2023 guidance of $320 million), and assuming gold and copper prices can cooperate, we should see New Gold generate at least $60 million in free cash flow next year, with a significant increase in free cash flow in 2025 with a full year of commercial production from the high-grade C Zone. So, for patient investors, there is certainly room for a re-rating here with New Gold set to generate upwards of $180 million in free cash flow in FY2025.

Based on an enterprise value of ~$920 million, New Gold trades at barely 5x FY2025 free cash flow estimates, a very reasonable valuation for a Tier-1 jurisdiction producer.

Recent Developments

While the progress at the C Zone and Rainy River Underground is positive and investors can breathe a sigh of relief that the TSF worries were resolved immediately with less than two days of lost time, the lower gold and copper prices could affect its Q3 results, with copper sliding closer to its Q2 lows and gold also drifting towards its Q2 lows. This could pressure margins in the period assuming similar to slightly higher all-in sustaining costs in H2 (implied by guidance), putting a dent in margins sequentially (Q3 2023 vs. Q2 2023). That said, this is hardly relevant to the bigger picture outlined above, which is a ~450,000 ounce producer in 2025 with sub $1,250/oz AISC capable of generating over $180 million in free cash flow. And while this might not matter to the market today, it should help with a re-rating 18 months from now, suggesting that further weakness in the stock should present a buying opportunity.

Gold Price - Daily Chart - StockCharts.com

{kind=link}

Summary

New Gold had a much better quarter in Q2 with the benefit of being up against easy year-over-year comps and is tracking well against its FY2023 guidance midpoint of 395,000 ounces with ~207,200 GEOs produced year-to-date. Meanwhile, the stock is trading back near the attractive valuation levels it sat at in March of this year despite being just a year away from commercial production at the C Zone and already chewing through higher-grade ore from Rainy River Underground. That said, while New Gold is cheap, several of its peers have also found themselves on the sale rack despite having higher margins and higher-grade assets. So, while I see New Gold as a Speculative Buy at US$0.94 for its updated low-risk buy zone, my Neutral rating reflects the fact that I continue to see better opportunities elsewhere in the sector.

For further details see:

New Gold: A Turnaround Story At A Reasonable Price