NGD - New Gold: Another Solid Quarter In Q2 - Assessing The Ideal Buy Zone

2023-07-16 04:57:20 ET

Summary

- New Gold posted solid Q2 results with ~102,400 gold-equivalent ounces produced vs. ~70,500 in the year-ago period.

- The strong production was helped by higher grades at both mines, and combined with a higher gold price, we should see much better Q2 results with easy comps vs. Q2-2022.

- Just as importantly, C-Zone development is progressing well after a slower Q1, with the company reaffirming first ore production by year-end.

- Given New Gold's improving margin profile and a path to meaningful free cash flow generation in 2025 after what's been a multi-year turnaround, I would view any pullbacks below US$1.02 as buying opportunities.

The Q2 Earnings Season for the VanEck Gold Miners ETF ( GDX ) begins later this month, and we've already seen multiple production reports from small-cap and mid-cap producers. Fortunately, New Gold ( NGD ) was one of those names that released a strong Q2 report in line with several of its peers, reporting Q2 production of ~102,400 gold-equivalent ounces [GEOs], leaving the company tracking ahead of its FY2023 guidance midpoint with its stronger half of the year still on deck. Just as importantly, the gold price has worked in the company's favor, with the metal spending a record 18 consecutive weeks above the $1,900/oz level despite its recent correction. In this update, we'll look at its Q2 2023 production and where the ideal buy zone sits for the stock:

Rainy River Operations (Company Presentation)

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q2 Production

Just over two months ago, I wrote on New Gold , noting that while margins improved materially in Q1 and stronger results were expected as the year progressed, there was no way to justify chasing the stock at US$1.45. This is because the stock was already up over 130% from its Q3 2022 lows and was no longer offering any real margin of safety, with it trading in line with its 5-year cash flow multiple. Since then and despite another solid quarterly report in Q2, New Gold has found itself down over 18% from its highs even after its recent rally, suffering a 32% drawdown from its highs. However, with a strong H2 on deck, the gold price continuing to cooperate, and New Gold being just a year away from consistent positive free cash flow, the probabilities have increased that the floor is in for the stock in the US$1.00 area.

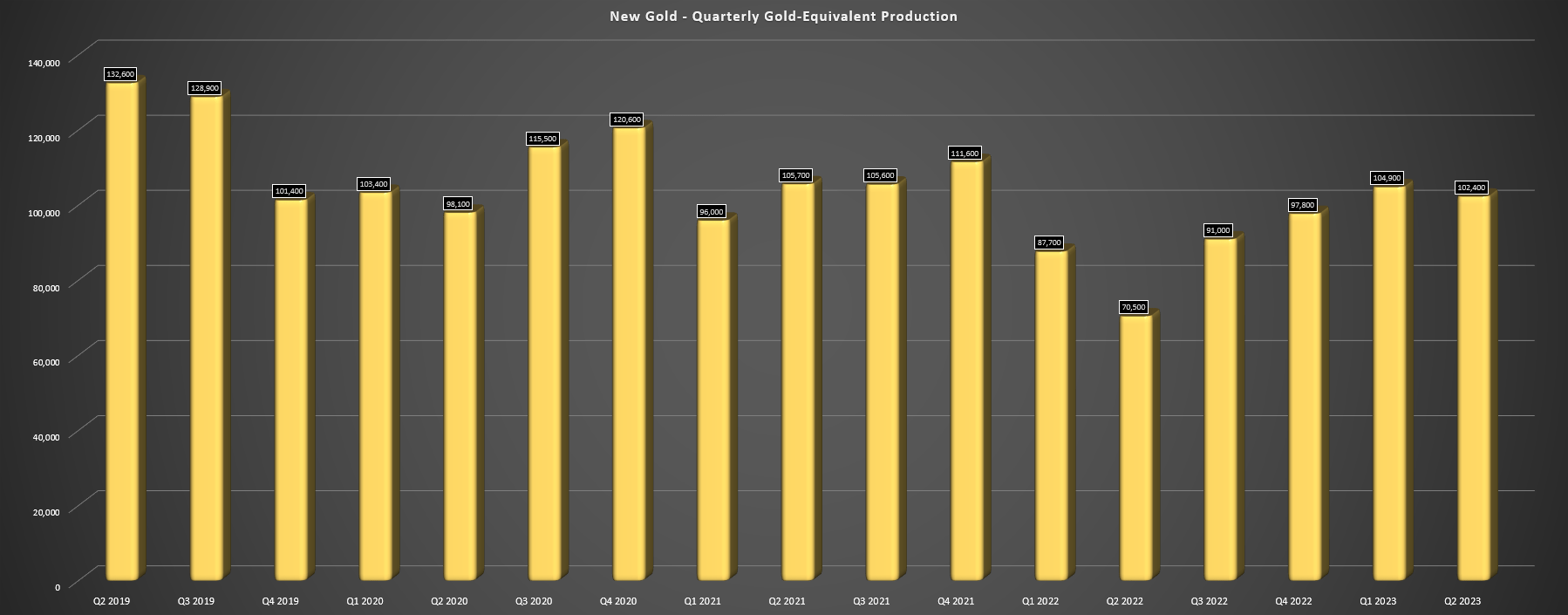

Looking at New Gold's preliminary Q2 results below, the company reported production of ~102,400 GEOs, a significant improvement from the year-ago period, with output up 45% year-over-year. This was mostly because of being up against easy year-over-year comps with heavy rainfall and flooding affecting Rainy River's Q2 2022 production, combined with the completion of Lift 1 mining at New Afton. Still, the results were still impressive and are tracking ahead of planned levels, with New Gold ending H1 2023 with total GEO production (helped by ~3,500 ounces from ore purchase agreements) of ~207,200 ounces, leaving the company at ~52.4% of its FY2023 guidance midpoint (395,000 GEOs) despite guiding for a 45/55 split for its H1/H2 production, with H2 expected to stronger.

New Gold - Quarterly GEO Production (Company Filings, Author's Chart)

{kind=link}

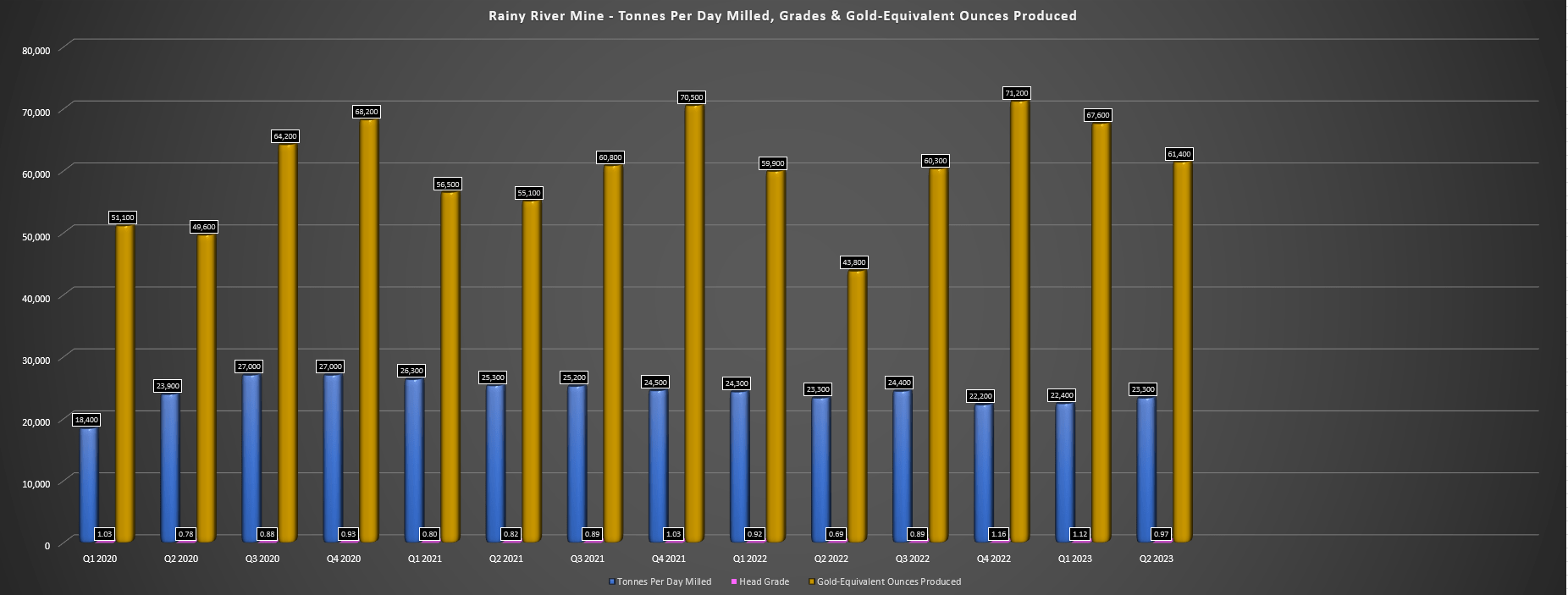

Looking at its Rainy River Mine in Ontario, production fell for the second consecutive quarter sequentially to ~61,400 GEOs, but was up sharply year-over-year, with increased ore tonnes mined, similar mill throughput, and a much higher average grade of 0.97 grams per tonne of gold (Q2 2022: 0.69 grams per tonne of gold). The quarter also benefited from a lower strip ratio and ore production from the higher-grade Intrepid Zone at Rainy River Underground, and New Gold called out higher mill availability as contributing to the outperformance during its planned maintenance. This solid H1 performance (~129,000 GEOs) despite planned maintenance has left the mine on track to deliver into guidance of 235,000 to 265,000 GEOs at much lower costs on a year-over-year basis (estimated costs of ~$1,550/oz vs. $1,605/oz in FY2022).

Rainy River - Tonnes Per Day Milled, Grades & GEO Production (Company Filings, Author's Chart)

{kind=link}

Moving over to New Afton, the British Columbia mine also had a solid quarter, with production of ~41,000 GEOs easily beating the ~26,800 GEOs produced in the year-ago period. The increased production was driven by much higher gold and copper grades of 0.72 and 0.78%, respectively, as well as higher recovery rates for both metals. Lower throughput of ~8,300 tonnes per day offset new Afton's higher grades and recoveries in the period, as well as less contribution from ore purchase agreements, but the mine is still tracking well against FY2023 guidance of 130,000 to 160,000 ounces based on ~78,200 GEOs produced year-to-date. And just as importantly, New Gold has reaffirmed that the C-Zone is on track for first ore production in Q4 of this year despite falling behind on development in Q1.

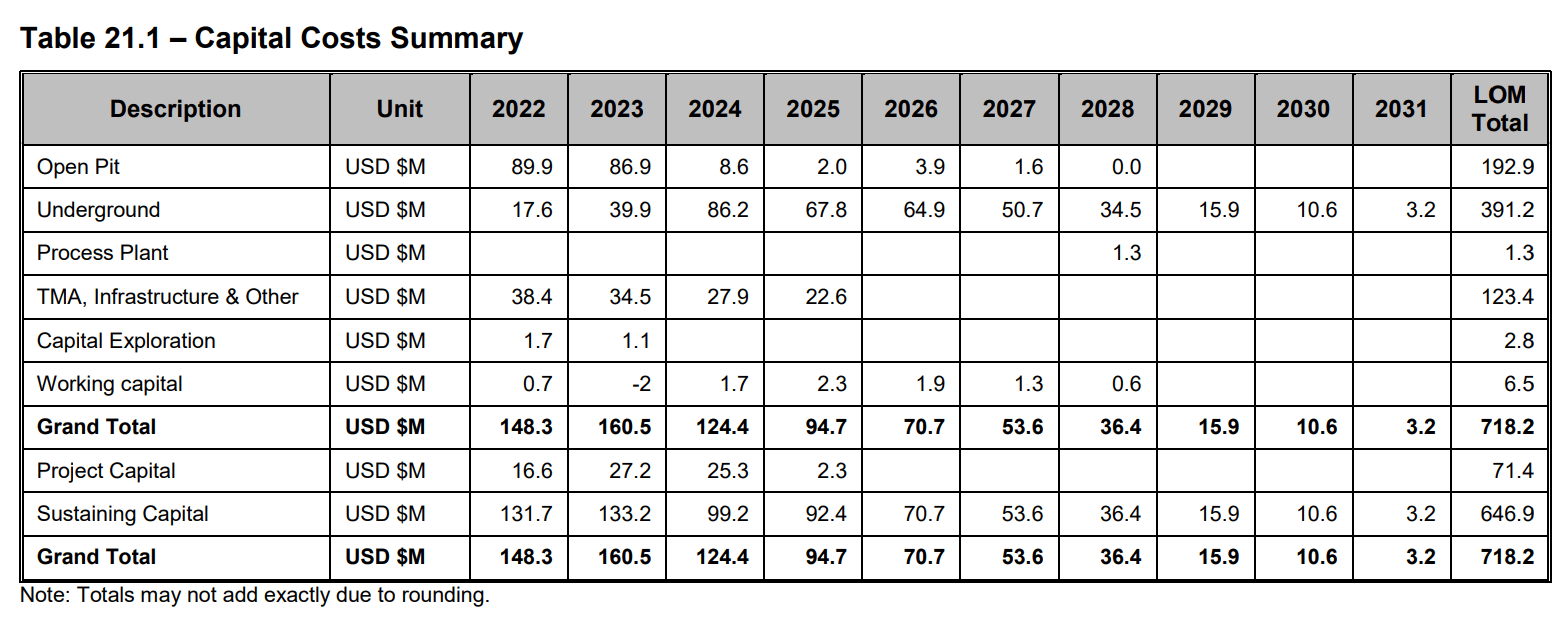

Overall, the combination of higher production and a stronger gold price year-over-year has set up New Gold to deliver strong Q2 results when it reports on July 27th, and it's certainly nice to see the company on track to beat its annual output guidance midpoint after what's been a spottier track record of meeting guidance in previous years. And while the company will not see positive free cash flow this year as it invests heavily in growth with C-Zone development, these investments will pay dividends in future years, with C-Zone set to transform New Afton into a much lower-cost mine with significantly higher gold and copper production. Plus, the best years at its Rainy River Mine are on deck as well, with much lower sustaining capital expected in FY2024 through FY2030 vs. ~$130 million in FY2022 and FY2023, which should help to pull costs below $1,450/oz (consolidated basis) in FY2024.

Rainy River Capital Costs (Rainy River 2022 TR)

{kind=link}

Recent Developments

As for recent developments, New Gold continues to benefit from a stronger gold price than many producers might have expected when they entered 2023, with the metal logging an impressive 18 consecutive weeks above the psychological $1,900/oz level. And while this is a welcome development for all producers, it's even more significant for a high-cost producer like New Gold, where the gold price can make or break their year given their lower margins. So, with New Gold lapping a rough Q2 2022 with ~70,500 GEOs produced at $2,373/oz all-in sustaining costs [AISC] or deeply negative AISC margins, Q2 2023 should be a much better quarter, with an average realized gold price closer to $1,950/oz, ~40% higher sales volumes, and lower all-in sustaining costs given the lift in grades at both assets.

Gold Futures Price (TC2000.com)

{kind=link}

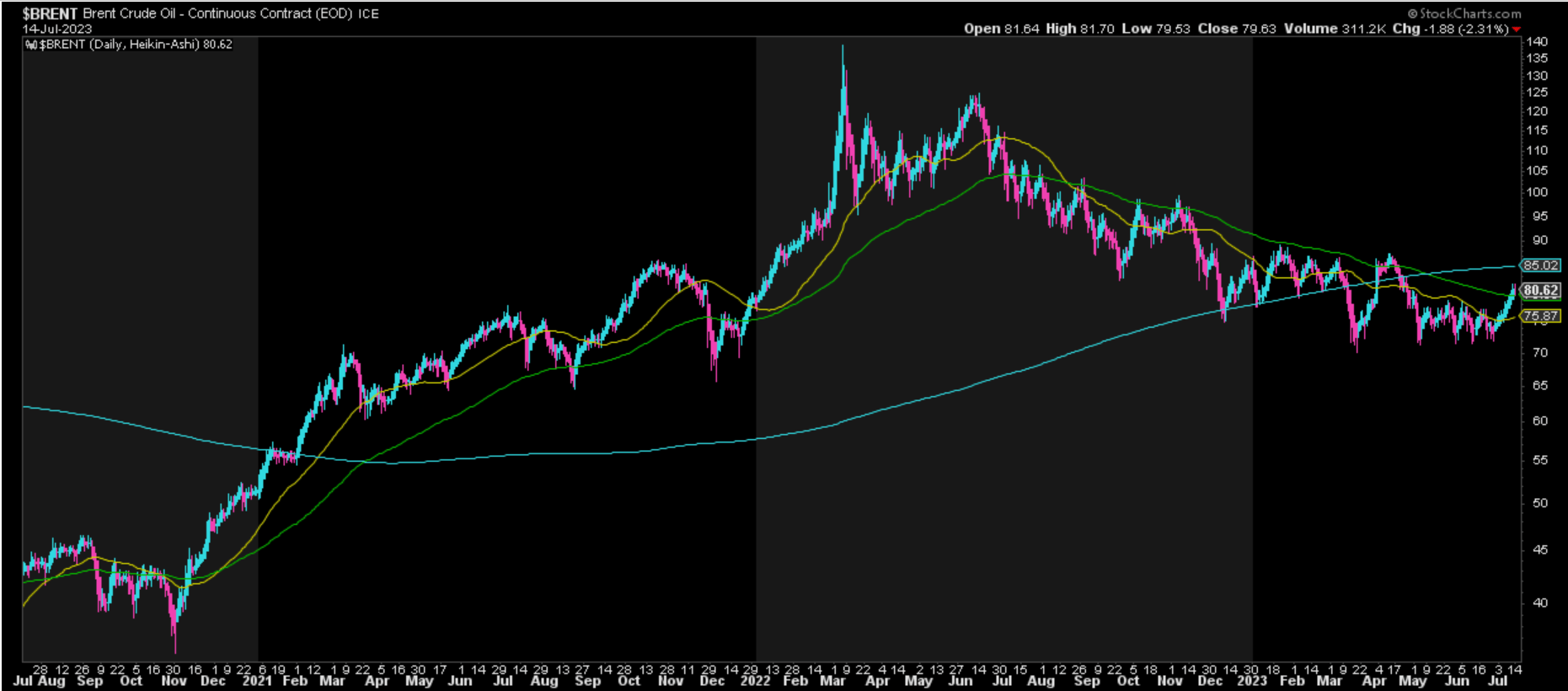

The second positive development for New Gold is the pullback in oil prices over the past year, which especially benefits its Rainy River Mine, a higher-volume operation. And while this isn't as significant for New Gold as some other open-pit producers given that it has 75% of fuel consumption hedged for Q2, it will benefit Q3 production where its hedges as a portion of fuel consumption drop to 50%. Meanwhile, although the Canadian Dollar has been stronger recently which can impact costs for Canadian producers, New Gold has hedges in place for 75% of all-in sustaining costs in Q2 and Q3, suggesting that we should see much better margin performance in Q2/Q3 2023 vs. Q2/Q3 2022, especially if the copper price can also maintain its upward trajectory. In summary, even if this is a high-cost year for New Gold ahead of positive free cash flow in FY2024, it's shaping up better than expected due to oil price softness and a stronger gold price.

Brent Crude Oil - 3-Year Chart (StockCharts.com)

{kind=link}

Valuation

Based on ~689 million fully diluted shares and a share price of US$1.21, New Gold trades at a market cap of ~US$830 million and an enterprise value of ~$1.04 billion, making it one of the lower-valued multi-asset producers operating solely in Tier-1 ranked jurisdictions. And while the stock's lower multiple can be attributed to its higher cost mines and the fact that it's still not generating positive free cash flow and has struggled to do so, these two points should change dramatically by FY2025. This is because its Rainy River Mine will benefit from lower costs related to a lower strip ratio and higher feed grades from the Rainy River Underground Mine. Plus, New Afton will benefit immensely from commercial production at the C Zone, with higher grades and much lower sustaining capital contributing to significant free cash flow generation.

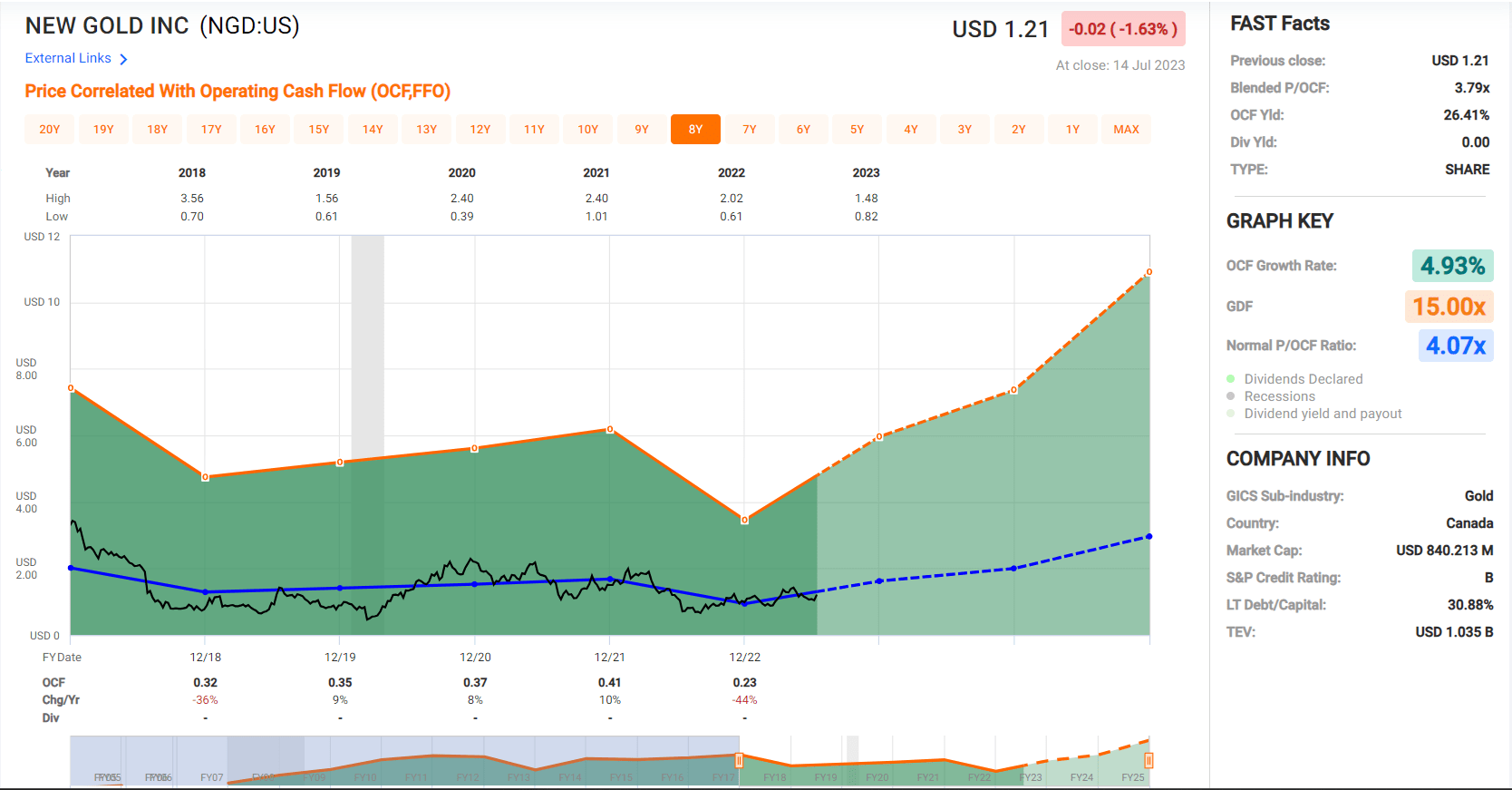

New Gold - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

Looking at the chart above, we can see that New Gold has historically traded at ~4.1x cash flow, which is one of the lower multiples sector-wide as New Gold had one of the weaker balance sheets among peers and costs well above the industry average (three-year average: ~$1,550/oz vs. ~$1,200/oz for the average gold producer). However, given the improvement in New Gold's balance sheet and path to positive free cash flow in 2024 with improved margins, I believe the stock could easily trade at 4.4x cash flow, a premium to its 5-year average. If we multiply this figure by estimated FY2023 operating cash flow of ~$260 million [$0.38 per share], this translates to an estimated fair value of US$1.67, pointing to a 37% upside from current levels.

Although this points to a meaningful upside from current levels if New Gold can execute successfully and gold prices continue to hover above $1,900/oz, I prefer to wait for a minimum 40% discount to fair value to justify buying small-cap producers given their high risk and volatility. This is especially true for high-cost producers, given that downside volatility in metals prices can have an outsized impact on their margins. So, if we apply this discount to New Gold's estimated fair value of US$1.67, the stock's low-risk buy zone comes in at US$1.00 per share or lower, suggesting the stock is no longer offering a low-risk buying opportunity after its 20% rally. Obviously, this doesn't mean that the stock can't go higher, but I prefer to pay the right or pass entirely and I see more attractively valued names elsewhere currently.

Summary

New Gold enjoyed another solid quarter in Q2, with year-to-date gold-equivalent production sitting at ~207,200 ounces, on track to beat its guidance midpoint of ~395,000 GEOs, especially considering that it expects a more productive second half of the year. That said, while the higher production at lower costs year-over-year will translate to a better year than FY2022, it is a capital-intensive year, meaning that investors will need to wait another year to see meaningful free cash flow generation. Given that New Gold trades at one of the lowest cash flow multiples sector-wide among Tier-1 jurisdiction producers with a significant improvement in margins on deck, I would expect the stock to continue to make higher highs and higher lows, with the potential for the stock to trade up to US$2.00 by 2025. That said, I see more attractive bets elsewhere currently, so I'd only become interested in buying on any pullbacks below US$1.02.

For further details see:

New Gold: Another Solid Quarter In Q2 - Assessing The Ideal Buy Zone