NGD - New Gold: Tracking Well Against 2023 Guidance

2023-10-08 08:23:41 ET

Summary

- New Gold had a solid Q3 performance, tracking well against its FY2023 guidance with a sharp increase in production.

- Meanwhile, Rainy River and New Afton continue to make solid progress on their growth plans, setting these assets up to grow materially post-2024.

- In this update, we'll look at how the company is tracking against its FY2023 guidance, its recent production results and if the stock has dropped into a low-risk buy zone.

The Q3 Earnings Season for the Gold Miners Index (GDX) will begin later this month, and one of the first companies to report its preliminary results was New Gold ( NGD ). Overall, the company had another solid quarter under its new leadership and is tracking well against its FY2023 guidance midpoint of 395,000 gold-equivalent ounces [GEOs] and looks set deliver into its cost guidance as well. For those new to the story, delivering into a guidance range of $1,505/oz to $1,605/oz might not seem all that impressive when the sector average is sitting below $1,350/oz. However, it's important to remember that New Gold is turning the corner on what's been a slow multi-year turnaround, with company-wide all-in sustaining costs [AISC] to decline below $1,250/oz in 2025 at the same time as capex rolls off, allowing for material free cash flow generation. Let's dig into the recent quarter below:

All figures are in United States Dollars unless otherwise noted.

Q3 Production

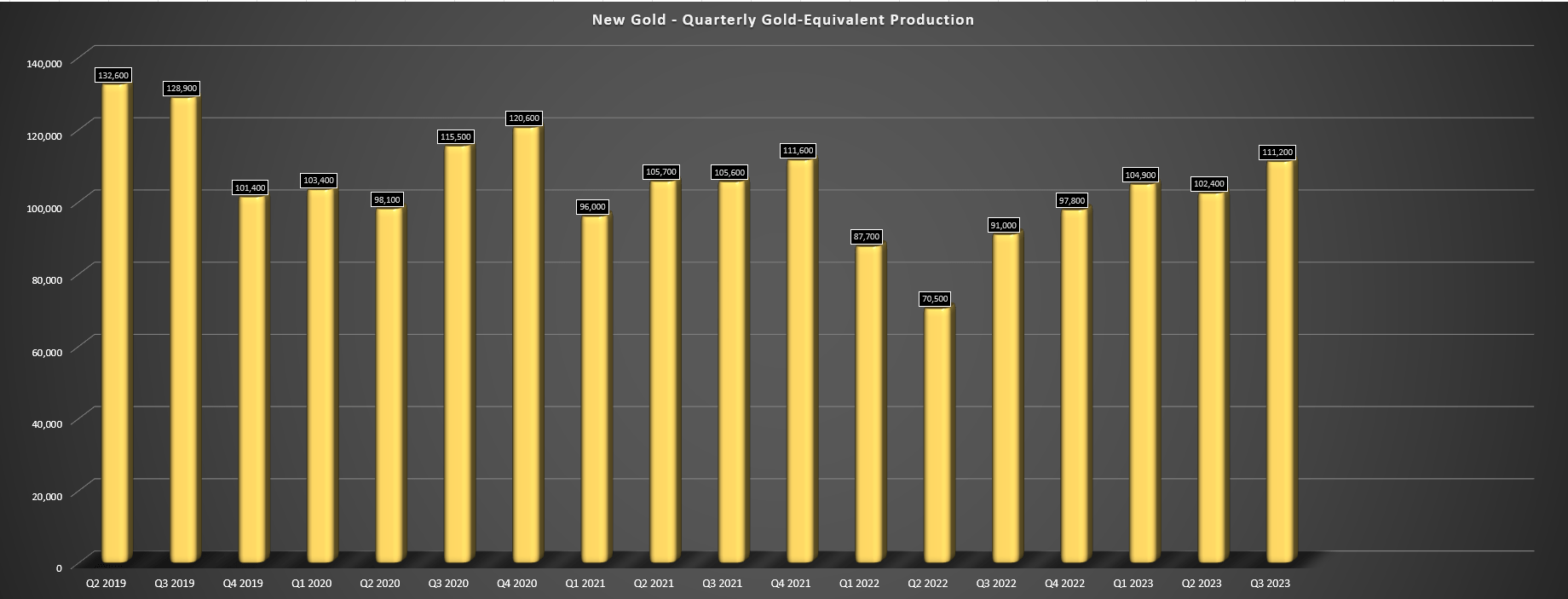

New Gold released its Q3 results last week, reporting quarterly production of ~111,200 GEOs, the company's best Q3 performance since 2020, and a significant improvement from the year-ago period. The increase in production was driven by higher throughput and grades at its Rainy River Mine offset by a minor dip in recoveries combined with a much stronger quarter at its New Afton Mine, with gold and copper production up ~58% and ~55% year-over-year, also driven by increased throughput at better grades. And while the company was up against relatively easy comps because of lower grades at both mines in the year-ago period, this has placed New Gold in a solid position to deliver at or above its production guidance mid-point, with the company currently sitting at ~318,000 ounces year-to-date and needing just ~77,000 ounces to deliver at its guidance midpoint, suggesting a high probability of a beat assuming no major hiccups.

New Gold - Quarterly GEO Production - Company Filings, Author's Chart

{kind=link}

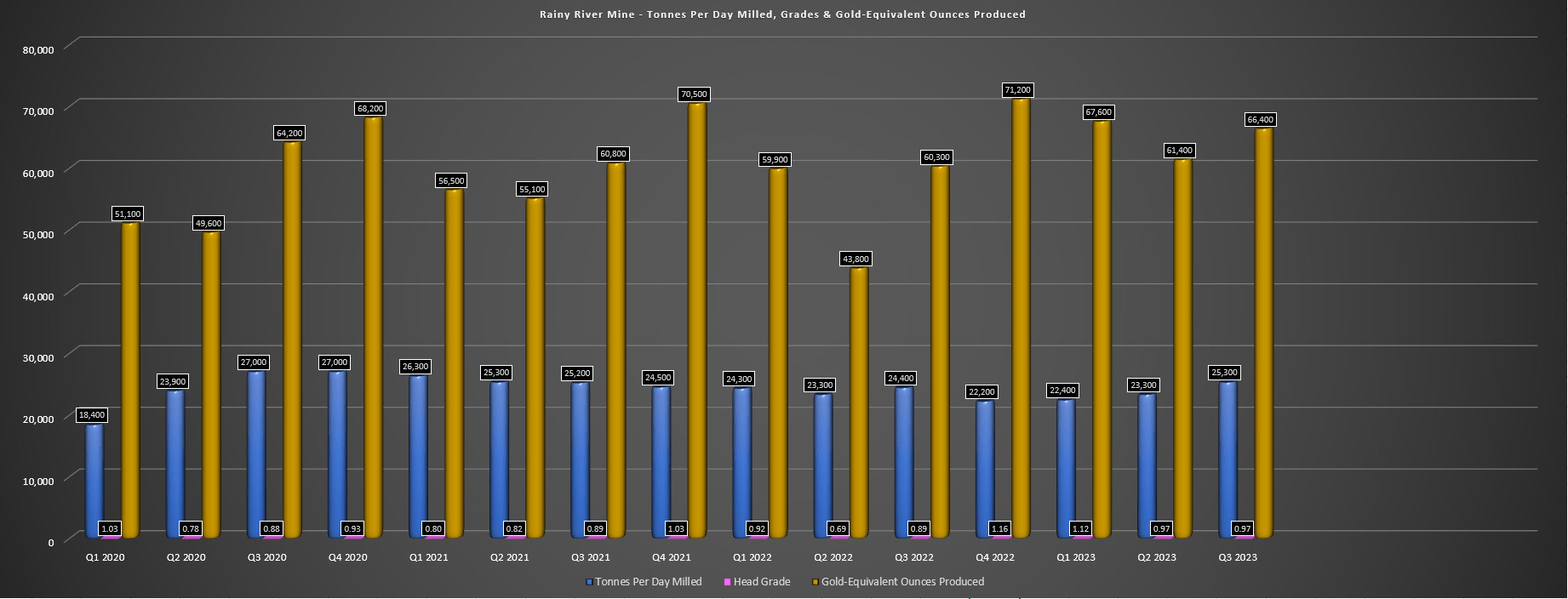

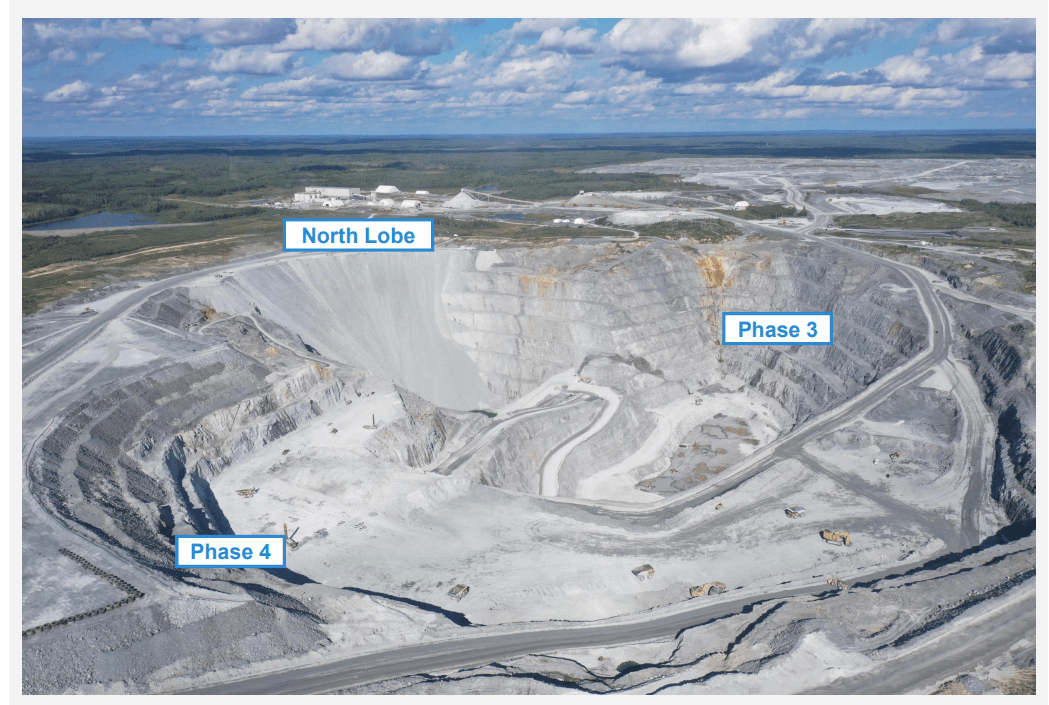

Digging into the production results a little closer, we can see that Rainy River had a solid quarter from a grade and throughput standpoint, with ~25,300 tonnes per day processed at an average grade of 0.97 grams per tonne of gold. This was up significantly from the year-ago period at better grades, benefiting from higher grade ore available from Rainy River Underground where tonnes and grade are reconciling well to date. Meanwhile, from a mining standpoint, ~36,200 tonnes per day were mined at a lower strip in the period, and the company will benefit from shorter haul distances in the future based on its decision to use North Lobe as an in-pit waste storage facility. And regarding optimizing the underground, the company will deploy Modified Avoca vs. Long-hole Stoping with cemented rockfill and is putting a connection ramp in place between Main Zone and Intrepid. This will reduce labor/material costs and allow for more effective exploration in the gap between Intrepid/Main.

Rainy River - Operating Metrics - Company Filings, Author's Chart Rainy River Mine - Company Website

{kind=link}

{kind=link}

As for the company's New Afton Mine, it was a solid quarter here as well, with ~44,800 GEOs produced, up from ~30,700 GEOs in the year-ago period. The strong quarterly performance has left New Afton tracking to deliver on its guidance midpoint of 145,000 GEOs, with ~123,000 GEOs produced year-to-date. Just as importantly, the company has made solid progress from a development standpoint, with it completing its first draw bell at the C-Zone while also commissioning the final two dewatering wells at the New Afton TSF. This has set New Gold up to begin commercial production by year-end from the much higher-margin C-Zone where costs will be materially low because of a much higher throughput rate (15,000+ tonnes per day).

Given this solid progress, investors can look forward to a dramatic change in the company's production and cost profile starting in 2025, with Rainy River set to benefit from an average grade of ~1.17 grams per tonne of gold (2024-2028), up from ~1.0 grams per tonne of gold currently combined with much lower sustaining capital (~$71 million per annum vs. ~$130 million in 2022/2023). And even if we apply more conservative AISC estimates for the 2023-2027 period because of the impact of inflationary pressures (vs. the ~$1,100/oz AISC highlighted in 2022 TR), its Rainy River Mine should still operate at sub $1,250/oz AISC (2023-2027), benefiting from a change to the mining method, shorter haul distances in the pit, and a weaker Canadian dollar. At the same time, New Afton's costs will plunge due to ~70% higher gold/copper production, allowing NGD to transform from a high-cost producer ($1,550/oz+) to a low-cost producer (sub $1,300/oz).

Recent Developments

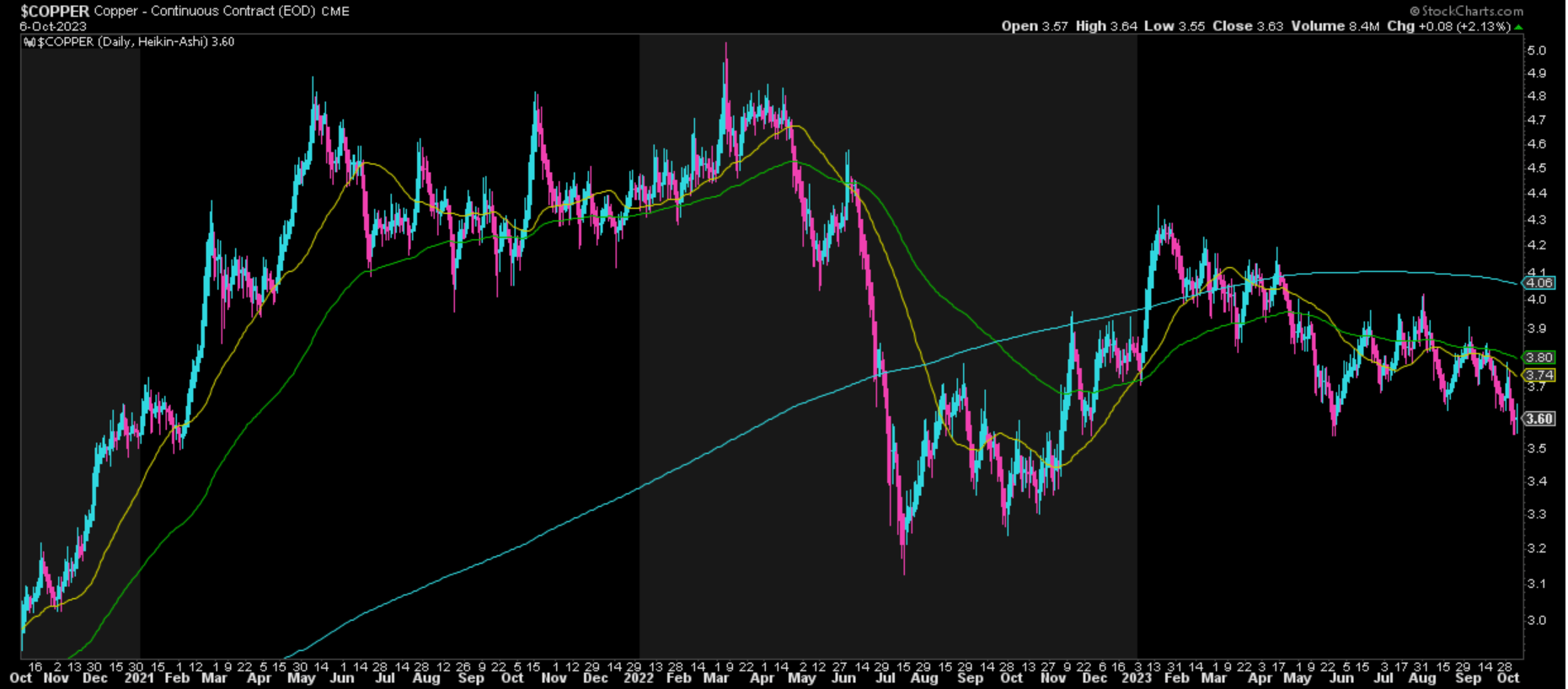

While this is very positive and leads to a brighter long-term outlook, the company certainly has got little help recently from commodities, with gold prices sliding below $1,850/oz, copper losing the $3.60/lb level, and oil soaring back towards $90.00/barrel. This is not ideal for a higher-cost producer, and this could lead to a much softer Q4 than some were anticipating, given the lower sales volumes from copper prices and a much weaker gold price at both assets combined with higher fuel costs. That said, the company will at least benefit from fuel hedges in Q3 to lighten some of the blow from a cost standpoint even if its top-line results will be weaker than many investors hoped in H2 2023.

Copper Price - StockCharts.com

{kind=link}

Although this is disappointing and further weakness in gold and copper prices could weigh on the stock and push it back below US$1.00, I don't see this as material to the story, especially with the company on the eve of a major transformation into a much lower-cost producer. And, while some companies may have weak balance sheets that could lead to share dilution if they have to do an equity raise to get through this choppy period for commodity prices, New Gold has over $170 million in cash and upwards of $500 million in liquidity, allowing it to get through this higher-capex period without any share dilution with significant credit available if it needs to tap its RCF where the company has ~$370 million available. Therefore, while the commodity price weakness is unfortunate, New Gold will have no problem weathering the storm due to its much improved balance sheet from a few years ago.

Valuation

Based on ~688 million fully diluted shares and a share price of US$1.06, New Gold trades at a market cap of ~US$730 million and an enterprise value of ~$950 million, giving it one of the lower capitalizations among the 400,000+ ounce producer space. In fact, this valuation pales compared to smaller and similar sized producers like Orla Mining ( ORLA ) at ~$1.20 billion market cap, Lundin Gold ( LUGDF ) at a ~$2.70 billion market cap, and Wesdome ( WDOFF ) at a market cap of ~$1.0 billion. Given New Gold's much higher costs, higher debt levels and inability to deliver on promises for most of the past decade, this discount has been justified. However, with a new team in Patrick Godin (President & CEO) from Pretium, Yohann Bouchard (EVP & COO) from Yamana, and VP Technical Services from Yamana, Luke Buchanan, the company is in much better shape to deliver on its goals and remains at an inflection point from a free cash flow standpoint.

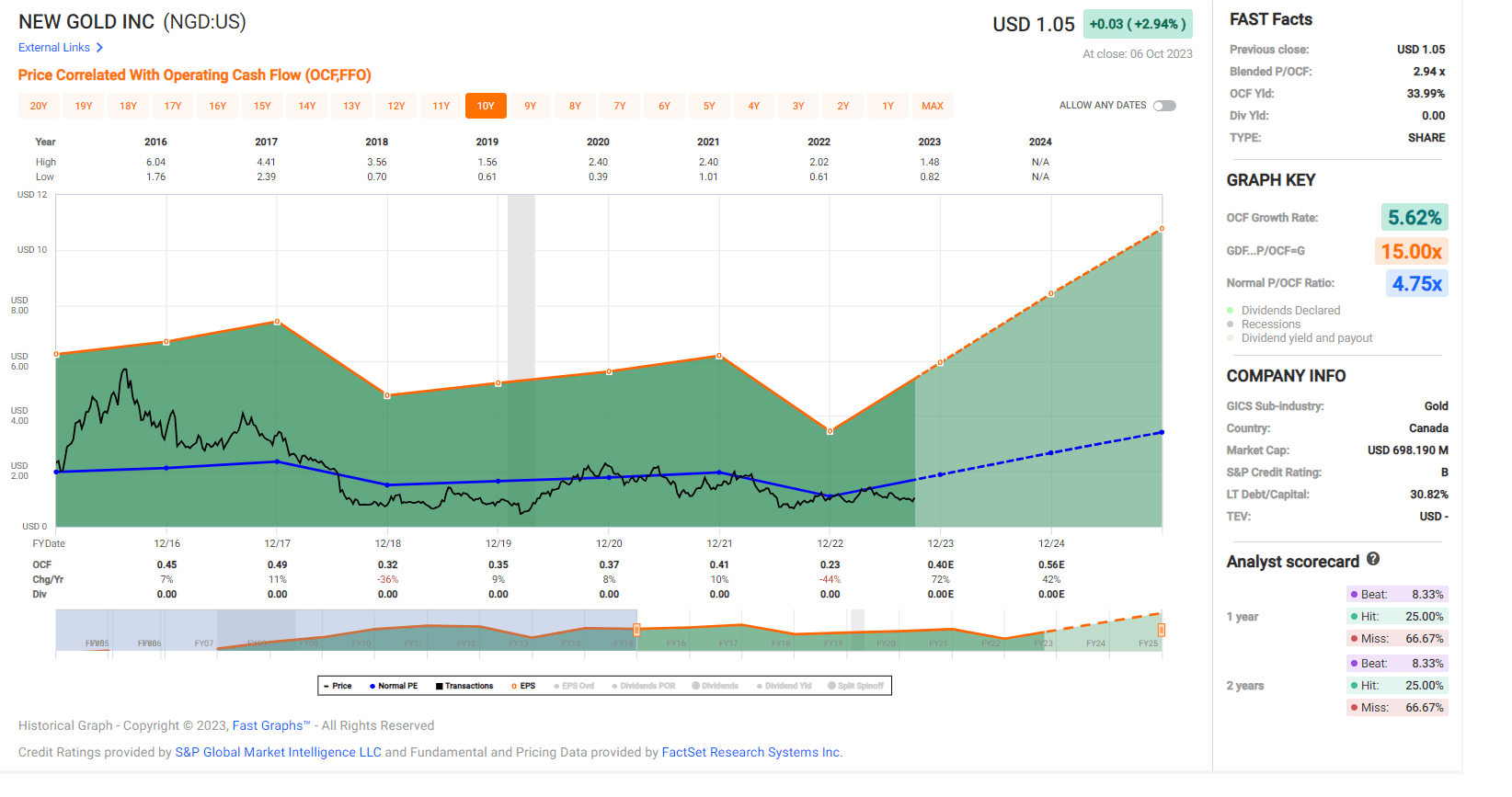

NGD - Historical Cash Flow Multiple - FASTGraphs.com

{kind=link}

This is because the company is on track to finally shift to free cash flow positive next year, benefiting from reduced growth capital and higher production at New Afton as production begins at the C-Zone, while also benefiting from higher-grade ounces from Rainy River UG and lower sustaining capital post-2023. And assuming gold and copper prices cooperate, the company could generate upwards of $195 million in free cash flow in FY2025 even assuming inflationary pressures persist, leaving the stock trading at just ~5.0x FY2025 free cash flow estimates based on its current enterprise value. And while there might be higher free cash flow yields available elsewhere if one prefers to venture into Tier-2 or Tier-3 ranked jurisdictions, this is certainly one of the highest among Tier-1 jurisdiction producers.

Given this improved valuation and a stronger technical team that's better equipped to achieve these goals, NGD is one of better buy-the-dip candidates sector-wide among the sub $1.0 billion market cap producers. That said, we're still 12-18 months away from free cash flow ramping up materially, with the major decline in capex and operating costs set to take place in FY2025. So, while the outlook has improved materially, I continue to see NGD as a name that's best to buy on sharp pullbacks vs. chasing rallies, and especially with copper under pressure, which affects New Afton. Hence, while I remain optimistic about NGD's ability to re-rate materially over the next 18 months and trade back above $1.60/share, I think this is a name to buy on sharp pullbacks vs. chasing as the quarterly results in the interim if gold/copper prices remain under pressure short-term.

Summary

New Gold remains one of the cheapest names in the sector from an EV to production per gold-equivalent ounce standpoint within Tier-1 jurisdictions, trading at just ~$230/oz, and closer to ~$200/oz on FY2025 production estimates. And while this might make sense at first glance given its $1,500/oz cost profile, this will change dramatically in 2025. So, for patient investors that are comfy owning lower market cap names and betting on turnarounds, NGD remains one of the more interesting reward/risk setups, especially with it trading ~40% off its year-to-date highs. To summarize, while I continue to see more attractive bets elsewhere in the sector, I would view any pullbacks on NGD below US$0.94 as buying opportunities.

For further details see:

New Gold: Tracking Well Against 2023 Guidance