NJR - New Jersey Resources: Underperformance Since December Looking At 2023

2023-03-14 00:34:42 ET

Summary

- When I last wrote about NJR, I called the company a "HOLD" due to its valuation. The company, since that time, is in the red, validating the thesis.

- I'm updating my thesis for 2023 for New Jersey Resources - the company is a technically attractive compounder, especially in this environment.

- However, you'll want to "BUY" this compounder at the right sort of price - and you don't have that here yet.

- Read my thesis update for 2023 and find out why I'm still on the sidelines on NJR.

Dear readers/followers,

My last article on New Jersey Resources ( NJR ) garnered relatively low interest, but what interest there was seemed in agreement about my thesis. A good thing as well, because the company has actually been underperforming since that time.

Seeking Alpha NJR Article (Seeking Alpha)

We do have some new results to look at. Those are the 1Q23 results, which we'll digest in this article and see how it validates or changes my previous thesis on the company. Given the current state of the market, it's more important than ever to make sure that every dollar, euro, yen, or renminbi that you invest actually is invested at a relatively low valuation.

Looking at New Jersey Resources' 2023

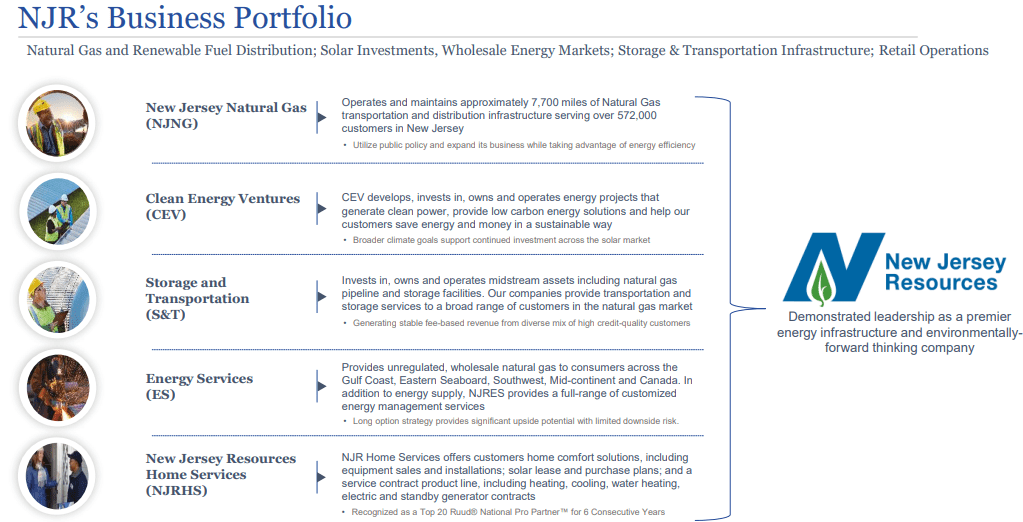

So, my first article describes this company's basic operations from a high level - essentially a holding company for various NJ-area utilities, and being a fortune of the Fortune 1000. It does retail operations, wholesale energy markets, natgas operations and distribution of Natural Gas, various clean energy ventures, storage operations, related services, and HVAC appliance repair.

An attractive mix, which adds potential growth sectors like repair segments and service segments to an otherwise conservative rate-base-oriented operating model.

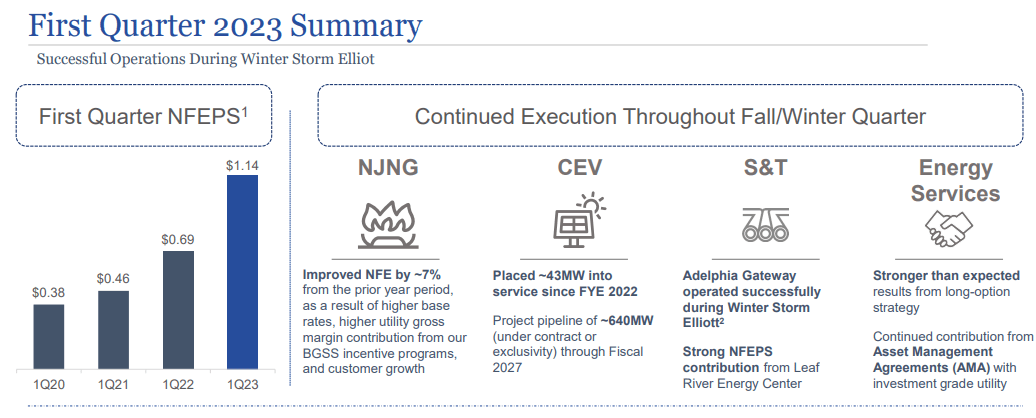

In 3Q21, we have some updates on how this company is doing - and the results are predictably boring. Net income is up a couple of millions YoY, up to around $116 for the first quarter, annualizing at about $450M+. The company increased guidance as of this quarterly report, despite some impacts from winter storm events in the NJ area during the end of 2022. Of course, such storm events also increase demand for what the company offers and does. The company is also raising its overall guidance to a higher-end range of $2.72, due to superb results from energy services, its natgas operating segments, and storage and transportation operations.

Overall, it was a quarter that highlighted the strength of a diversified portfolio that includes services I would characterize as almost VAP.

The company, as I said early on, has an excellent history of growing earnings, but also has an appealing dividend stability which really makes this utility a solid and practicable sort of income investment. From a segment or industry split, the company's EPS comes to 60% from natgas, and 20% from energy services, with the remaining services being a bit mixed from 6-18%. So the fact that energy services did so well, and with natgas also doing very well, provides a good explanation to the positive results, and why the company is likely to generate more earnings than expected only 1-2 months ago when I wrote my last piece.

I was clear in that piece, that NJR is in no way a bad company - it's a very solid company with a good upside, averaging 4-5% growth going forward in a very attractive geography.

The issue is the price we're paying because it's beyond the typically premiumized levels that the company trades at.

While the company expects its 7-9% annual long-term growth to continue, and even recently bumped expectations for its net earnings, this doesn't change the fact that there is no way I'm paying a 20x P/E multiple for a 3.14% yield in this environment, when we have a company with very clear ups and downs, no matter how attractive its trends can show the company being.

The company also has impressive ESG records, for those who care a whole lot about this.

{kind=link}

Me, I obviously care more about the solid trends, like EPS and execution - and NJR has excelled here in 1Q23.

{kind=link}

Elliot, as in winter storm Elliot, was a good indicator of the resilience of the company's network and operations. The event caused no interruptions, and due to a significant uptick in Natgas prices at the time, the company also recorded impressive income trends.

The company's capital allocation plan is intact, and 2023E is expected to see about the same level as 2022 in terms of overall investments - with the year of -24 being sort of the year where potentially another $100M might be put into investments.

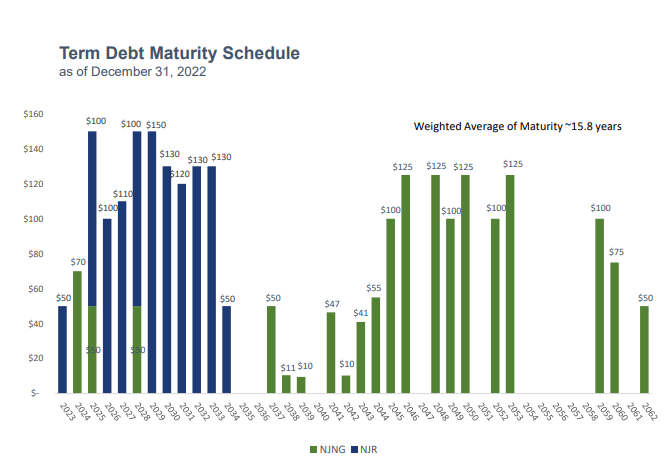

The company has some exposure to the rising interest rates in the current environment, with plenty of refinancings incoming for the NJR debt maturities.

{kind=link}

However, with almost $1B in facilities through 2027, I foresee only an uptick in costs and no major issues. Keep in mind that NJR is A-rated by Fitch, so they're at the upper range of the totem pole when it comes to financing costs.

As always, an investment into a utility company like NJR is done for the combination of growth and safety, with a lesser overall emphasis on growth, and more on safety. The dividend here is actually starting to look fairly meager given the yield available is essentially risk-free. Even for me, in Sweden, the spread is less than 70 bps.

Couple this with a high valuation - more on that in a little while - and I have a hard time seeing an appealing entry here, even with what the company is planning in terms of infrastructure.

The company's fundamentals aren't the problem. The company itself is targeting a TSR of 10-12% with a net-zero ambition in 2050 for NJ operations. The company also has one of the more fundamentally attractive portfolios in the entire segment and area.

{kind=link}

But all the advantages in the world won't make up for what I'm about to show you here - so let's get it out of the way.

New Jersey Resources is unfortunately still too pricey going into 2023

Now, despite having seen some decline in the company's share price since my last piece, there's not enough to like about this valuation. In fact, there's a lot to dislike about where the company currently is compared to where it has been and where it might go from here.

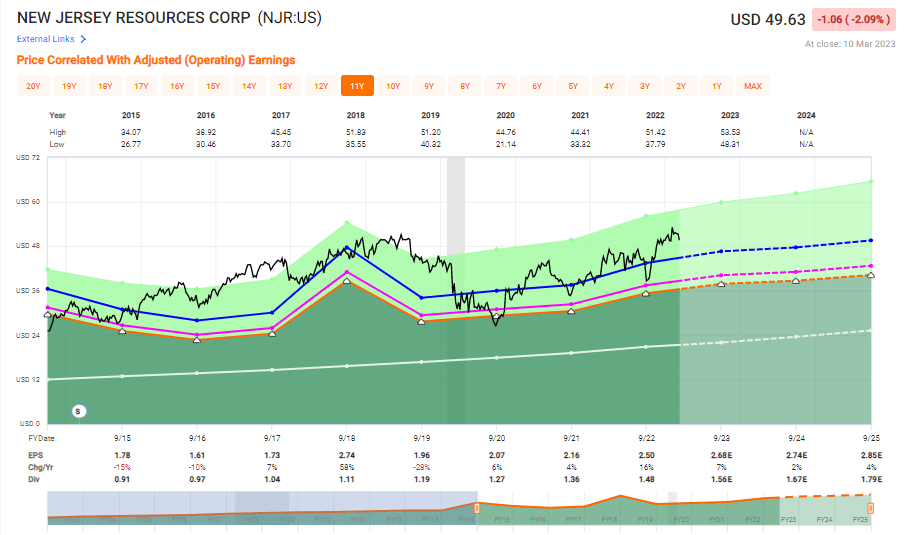

Take a look at this visual representation.

{kind=link}

Not particularly exciting, as undervaluation goes. Given the relative volatility over the past 10-11 years, you can clearly see where you might want to be buying this company, and it certainly isn't at close to 20x P/E, when the normalized P/E is closer to 17.4x. Even at 17.4x, I'd be somewhat careful here given the alternatives available on the market today. Frankly, at 3% yield, you can find bond alternatives maturing in 2024 that have better conservative return potential than this investment does.

I want an upside in this investment that is a combination of both yield and return. Given that isn't something we can expect here - at least not unless the premium continues to expand, that's not something I'm willing to do.

I would be able to see an upside if there was some instance or some part of the company's plan that somehow vastly increased its earnings potential, like a tack-on M&A, or a new project - but NJR is about to do the same thing they've always been doing for the next 5 years - and that means I don't expect massive changes here.

The realistic TSR on an annual basis until 2025 is a whopping 4.29% up to a total 3-year TSR of 11.36%. Back 6 months ago, you could have gotten more than twice that when the company, very briefly, was actually cheap. That is not the case at this time.

The 20-year perspective is even worse than the 10-year. The company's typical premium comes to around 16.65x over 20 years, which I would actually view as decent and attractive given the company's fundamentals - but it only goes to show you that the valuation has disconnected from the company's historical trends without any real reason for this happening.

I don't view NJR as an especially complex or difficult investment to evaluate or go for. It's incredibly stable, attractive, and operates with some of the best metrics and fundamentals I've seen in an American company in this sector - and its relationship with regulators is superb.

But the highest I'd be willing to pay is between 16-17x P/E.

S&P Global analysts would disagree with my conservative assessment, unsurprisingly. 9 analysts follow the company, and their range begins at $43, going all the way up to $59/share. That upper range valuation would imply that the analyst believes the company to be worth a 21x 2025E P/E , for a company yielding less than 3.2% in a rising interest rate environment where you can get over 4% from an MMF, or even I can get a 2.8% from a short-term fixed savings account with FED/equivalent insurance.

I'm going to go ahead and say "no" to that price target. The analyst average comes to $50.22/share here, which still implies a 1.2% upside here. Again I clearly say "No" to that particular price target.

Their recommendations are interestingly enough, disconnected from their own price targets. 7 out of 9 analysts are either at a "HOLD" or an "Underperform" here, which is something I see quite often - a high PT, but their ratings don't matching that positive PT.

This tells me all that I need to know - which is that the time is ripe to give New Jersey Resources a firm "HOLD" despite improved results.

The following is my thesis for NJR for the year of 2023 - at least for the time being.

Thesis

My current thesis for NJR is as follows:

- This is an above-average quality utility with a very attractive set of fundamentals and overall qualities. The yield is growing and well-covered, the stability and the relationships with regulators are solid, and the company operates a very attractive mix of assets in a very attractive geography.

- The company also has some very attractive side operations, giving the company growth potential and service potential beyond its legacy operations.

- At any appealing price below 16x-17x P/E, this becomes a "BUY" to me. But that is not where we currently are, and it seems unlikely that we'll go there anytime soon.

- For that reason, I am giving NJR a price target of a conservative normalized $42/share, unchanged from my last article, which would be where I would become interested in the stock. We're a far cry from this right now, at $49.63/share.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Because the company does not fulfill my valuation criteria - any of them - at this time, I'm forced to go with a "HOLD" here.

For further details see:

New Jersey Resources: Underperformance Since December, Looking At 2023