NJR - New Jersey Resources: Unfortunately The Underperformance Continues

2023-05-29 10:09:27 ET

Summary

- When I last wrote about NJR, or New Jersey Resources, I called the company an unattractive "HOLD" due to fundamentals and valuation. The company had underperformed prior.

- It once again underperformed for another half-year, validating once again my thesis and stance for this business. We're now almost 5% lower inclusive of dividends.

- How about now? Is the company attractive enough at this time to constitute an attractive investment for you? That's the question I aim to answer here.

Dear readers/followers,

On the surface of it, New Jersey Resources ( NJR ) isn't a bad company at all. The company has some of the best RoE you can find in the regulated utilities sector. It also has impressive profitability records for the past decade, putting it past most of the others in its segment. Most other margin numbers are either on par, meaning average, or slightly above/slightly below average. The company is no standout in any one sector - not positively, but not negatively either.

In fact, looking at ROIC, NJR has proven that it can drive profitable investments even as WACC increases, for the company has avoided ROIC/WACC negative numbers for over 7 years at this time. There also hasn't been any significant change in SE or other metrics that would justify or signify any sort of fundamental issue. Perhaps this is why this company has been slow in moving, and why some people are still positive on it.

Let's review the latest results and let me show you why I believe there are substantially more attractive options out there if you want a regulated utility company.

New Jersey Resources - Some things to like, some things not to

The company has the structure you'd be used to if you spent any amount of time looking at regulated utility businesses, especially US-based ones. It's structured as a holding company for a number of utilities and services throughout various regions in the NJ area, hence the name of the business.

Retail operations are the focus, specifically energy, natgas operations and distribution, a growing number of clean energy projects and ambitions, storage, but also a growing services and HVAC segment.

If you follow my articles, you know that I often look at companies that offer complimentary service segments, which come with a vastly different growth profile and potential, next to their "guaranteed"-earnings segments of regulated utility operations. It's not an unattractive model, and it's proven over time that it can deliver good earnings.

For those of you of my readership focused on clean energy above all, the company is the first east-coast utility to mix clean hydrogen into its stream. It also happens to be one of the largest owner-operators of solar assets in all of New Jersey. So plenty of appeals there from a renewables standpoint, and it's likely to grow going forward.

The recent number of years has put pressure on utilities. Usually, these companies argue with their income - attractive, bond-like yields with guaranteed payouts with very little volatility. The problem for many of them with the rising interest rate is that their 2-4% yields are no longer as appealing when every mom 'n' pop can get 3.5-4% from their local bank in a savings account - or similar, safety-equivalent investment opportunity. We're not there yet, but we may be soon. This flecks the appeal of investments such as these, even with an A- from Fitch, and a 20-year history of growing its EPS by around 6.2% on an adjusted basis every year. Anyone who invested long term into NJR stock has done well, with a 9.5% annually until now. But that may no longer be the case going forward.

Between increased OpEx and investment spending, the company's ability to grow its earnings has been slowing down. That's not even including inflation, which of course is pressing down on this company from every direction. What I see based on these trends is clear as crystal - to me, anyway. I see the declining rate of earnings growth, from high single digits to either low single digits or at most, mid-single digits.

The company recently reported 2Q23, and the company's results for the quarter were good. Increased net earnings, increased NFE, re-affirmation of its growth rate, and it does maintain that 7-9% - for the time being, at least. Though it's important to note that this is the measure NFEPS, which is non-GAAP. And I also, obviously, want to show you that decline on a quarterly basis, even though it's currently relatively stable compared to the periods going back to 2021.

NJR IR (NJR IR)

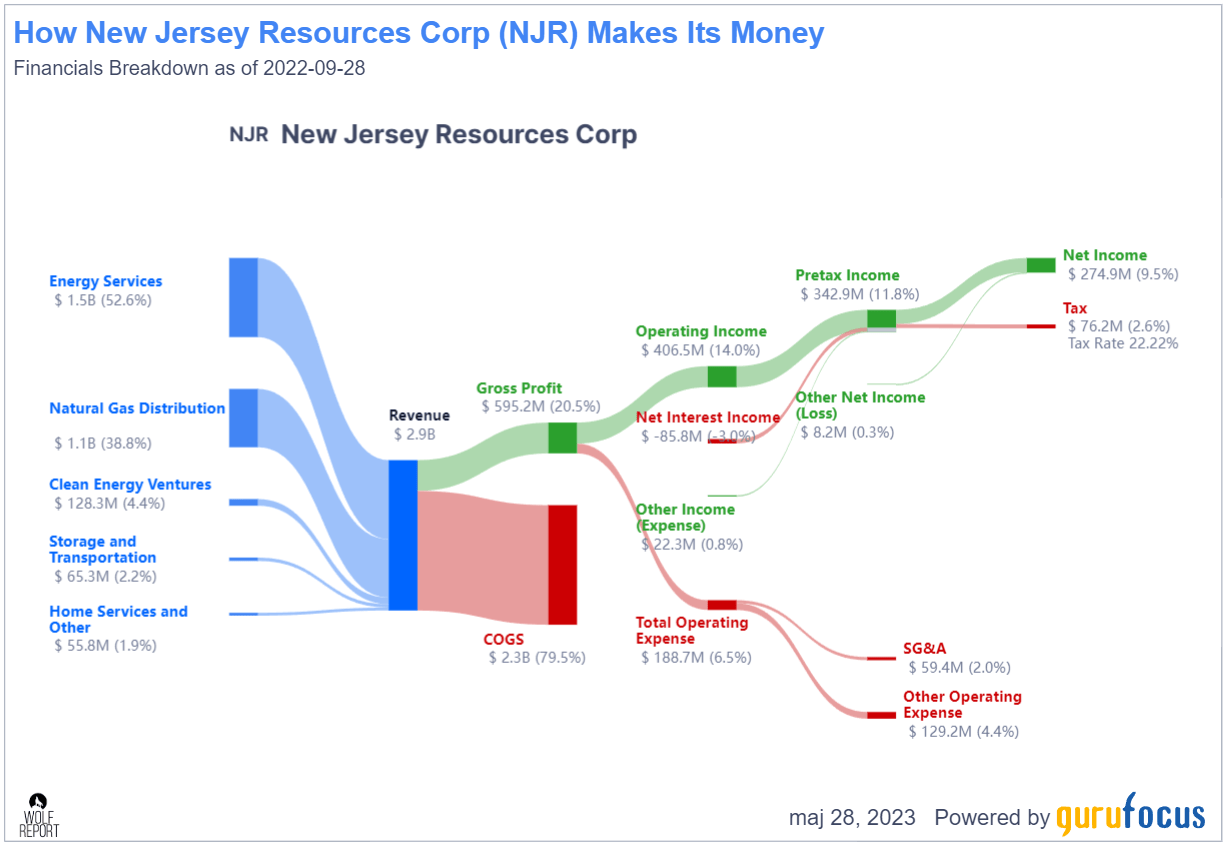

The company did manage solid results, and good gross margins, and continued to place new renewable assets into operation - 53 MW since FY22, with a project pipeline of 0.74 GW under construction until fiscal 2027. The recent positivity in both 1Q23 and 2Q23 has made the guidance affirmation clear, and at least for the 2023 period, the company expects net financial EPS of 7-9% growth, based on both its utility segments and non-utility segments. Take a look at the current mix.

{kind=link}

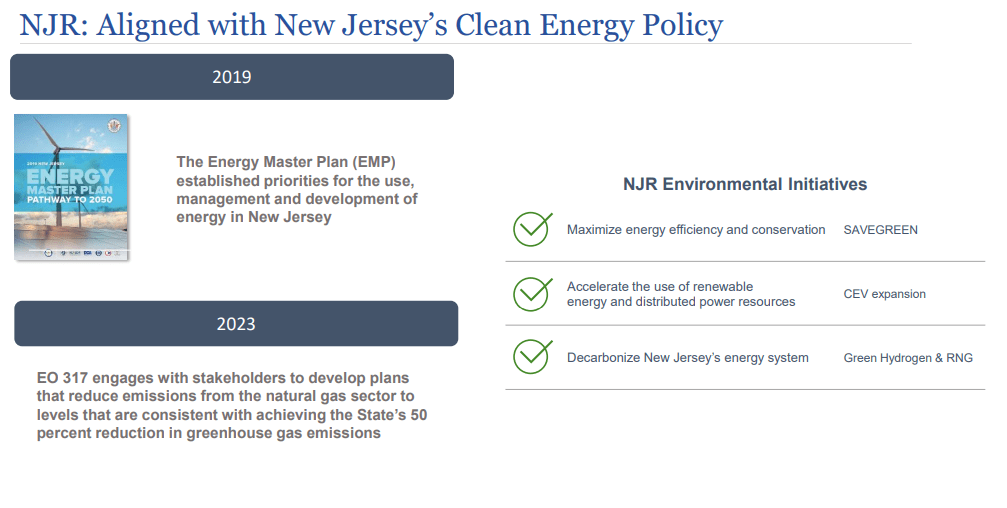

My issue has never been with NJR's business. They're a very capable operator, and they're both efficient and with good management, managing what you see above. The company's capital plan is robust, and on paper supports the company's growth targets, though it demands annual investments of at least $520-$782 going forward until 2024E. Its goals are also aligned with what is called the Clean energy policy of New Jersey, according to the EMP delivered in 2019.

{kind=link}

So for the time being, I find very little support for my assumptions that EPS growth rates are going to be slowing down in the next few years. NJR has a solid balance sheet, good inflation protection, and good debt with a staggered profile in terms of maturities. It's ESG-compliant on a state level, and it has recently reiterated relatively strong guidance. This guidance is also in line with what analysts are expecting for 2023 - and I could get on board, at least for 2023, with a 5-8% EPS growth rate on an adjusted basis. The issues, I believe, will come in the later years of 2024-2026, when I expect this growth rate to start to taper off. A few reasons for this.

The company has yet to see the effects of interest rates due to its debt schedule. When this hits home and it refis, we'll see NIC pressures come bearing down. Utilities have large debt loads , which makes this an inevitability, as I see it. NJR, as an example, is leveraged to 54.22% of debt/cap, has almost no cash at a cash/debt of 0.01x, equity to asset of less than 0.33x, debt/EBITDA of 5.1x, and interest coverage of less than 4.5x. And that is on current numbers. It's not worrying at this time, but I do think this will be of greater importance going forward, and this will eat into otherwise excellent margins and return numbers.

Aside from this, I don't believe we've seen the full impact of utility input cost, rising customer rates, and other macro-level trends. This has resulted in very low overall dividend growth from the entire [[XLU]] ETF, which is a good benchmark for the entire sector. I believe this strain will continue as the pressure on the entire utility market grows. The reason I believe it will grow is that the entire market is regulated , and regulators are, in my Swedish welfare-oriented experience, the first to start tamping down on the companies where they can. Why? Because they have the ability to do so, and they actually have the obligation to protect consumers from what in their mind is unfair pricing.

In times of trouble, these trends can really ratchet things up, and that's not something you want to see.

And that's really the reason why I won't be paying significant money or multiples for NJR at this time.

Let's look at company's valuation.

NJR Valuation - Still not that compelling

So, this is a qualitative company. Why not go ahead and buy it?

The company is currently trading at 18.66x, offering less than 3.2% yield compared to EU telcos with better credit quality and yield where I can get not only payments but significant upside. Comparatively speaking, this utility has very little to offer when viewed contextually as a component of the global regulated utility landscape.

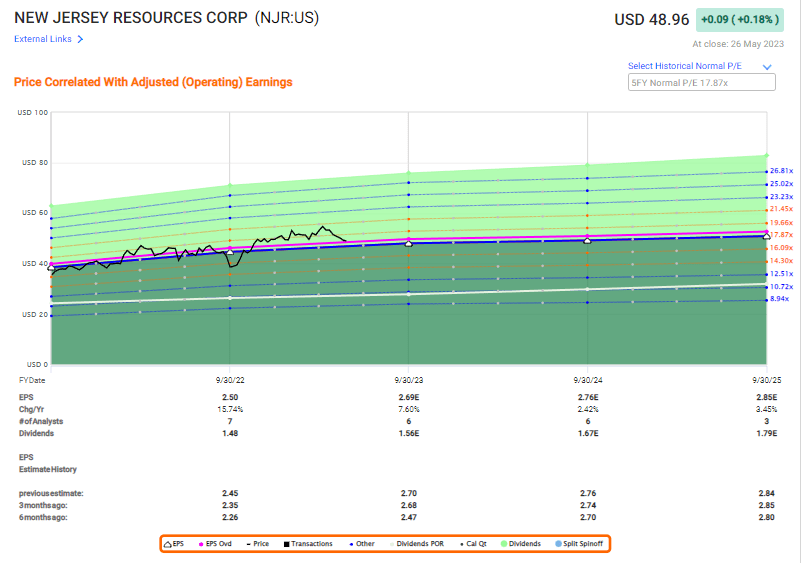

Add to that compared to a 5-year average of 17-18x P/E, this company offers very little in the way of conservative upside. At 17.87x, the upside based on current estimates is no higher than 5.22% per year, which is sub-par no matter how you slice it.

{kind=link}

If you see that small bout of undervaluation back a year ago, that's a time when I would be open to buying the company. But even at that time, because I happened to be in the market for more utilities at the time, I would have, and did compare it to other potential investments. And the company did not measure up as an investment compared to businesses like Enel ( ENLAY ) or Engie ( ENGIY ). One of the advantages of being an internationally-oriented investor with access to over 30 native markets and various currencies, is that I am not limited to the upside appeal of one market. At times, there is nothing to buy attractively in Sweden, at which time I go to Germany. Or France. Or Spain. Or Canada, or the USA. The markets are endless, and while market dynamics and attractions differ, the measurements used to look at companies, especially as a quad-lingual with fluency in many of the languages mentioned in the nations above, means I have an understanding of several markets.

Nonetheless, the comparative attractiveness for this company at this time, even after a good 2Q, remains muted, and I am not that interested in investing here. S&P Global analysts remain exuberant on this business, forecasting it at a $51/share average from a range of $45 to $60/share. But only 2 out of 9 analysts have an official "BUY" rating, which tells you about their conviction at this time when the company is trading at a price of $48.96/share.

I personally would not invest in NJR above $42/share. This was my price target in my previous article, and I see no reason, even based on these latest trends, to deviate from this. The reason is that this price target is based on trends that have not changed.

Because of that, this is my thesis.

Thesis

- This is an above-average quality utility with a very attractive set of fundamentals and overall qualities. The yield is growing and well-covered, the stability and the relationships with regulators are solid, and the company operates a very attractive mix of assets in a very attractive geography.

- The company also has some very attractive side operations, giving the company growth potential and service potential beyond its legacy operations.

- At any appealing price below 16x-17x P/E, this becomes a "BUY" to me. But that is not where we currently are, and it seems unlikely that we'll go there anytime soon.

- For that reason, I am maintaining my NJR price target of a conservative normalized $42/share at May 2023, unchanged from my last article, which would be where I would become interested in the stock.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Because the company does not fulfill my valuation criteria - any of them - at this time, I'm forced to go with a "HOLD" here.

For further details see:

New Jersey Resources: Unfortunately, The Underperformance Continues