NJR - New Jersey Resources: Waiting For That Valuation HOLD

2023-11-03 07:43:48 ET

Summary

- New Jersey Resources has underperformed and dropped in value despite being a fundamentally sound company.

- NJR has strong profitability records and impressive RoE in the regulated utilities sector.

- The company is focused on retail operations, including energy, natural gas, and clean energy projects, with plans for future growth.

Dear readers/followers,

The recent performance of New Jersey Resources (NJR), is not an especially pleasant read. The company, which I have gone on record calling "unattractive" and an overall "HOLD" due to valuation, has underperformed once again. I started reviewing this business after a request, and it has been an interesting business to keep an eye on, but one that's also underperformed (meaning following my stances correctly) in every one of my articles for the past year and more.

My last article on the company can be found here, making this an update on the company. I did not view the company as attractive then, and in this article, I'll show you if and why we can view the company as attractive at this time.

This underperformance is puzzling for some investors because, on the surface of it, New Jersey Resources ((NYSE:NJR)) isn't a bad company in any way. The company has some of the best overall RoE you can find in the regulated utilities sector. It also has impressive profitability records for the past decade, putting it past most of the others in its segment. Most other margin numbers are either on par, meaning average, or slightly above/slightly below average. The company is no standout in any one sector - not positively, but not negatively either.

So what makes this company drop like a stone, down double-digits since my last article ( which you can find here ), when the market is slightly better than flat?

Seeking Alpha NJR (Seeking Alpha)

That's what we'll look at here.

Updating on unattractive NJR and seeing if a "BUY" is now valid.

I don't like seeing qualitative companies underperform the market - and this is what NJR has been doing. NJR has proven that it can drive profitable investments even as WACC increases, for the company has avoided ROIC/WACC negative numbers for over 7 years at this time. (Source: GuruFocus)

There also hasn't been any significant change in SE or other metrics that would justify or signify any sort of fundamental issue. Perhaps this is why this company has been slow in moving, and why some people are still positive about it.

NJR has the sort of operating structure you'd expect from a regulated utility - it's a large holding company for a large number of regulated utility businesses. It has both the regulated retail you'd expect, and if you follow some west-coast operations you'll know that many of those have service and HVAC segments, and NJR has this as well. Retail operations are the focus, specifically energy, nat gas operations, and distribution, a growing number of clean energy projects and ambitions.

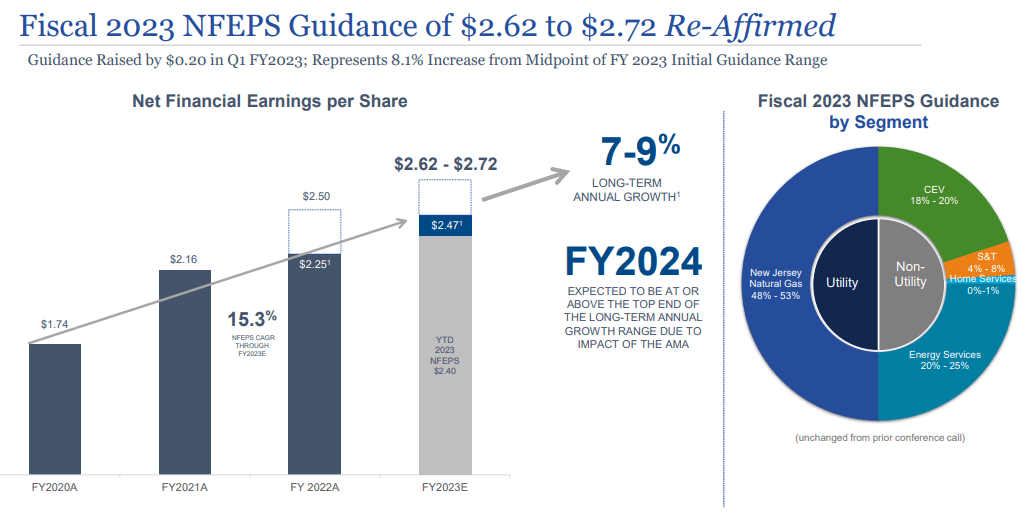

We have 3Q23 results to look at (Source: NJR IR, 3Q23 ), and these results are characteristically unexciting for this business. Company NFEPS is up to $0.10, with a YTD NFEPS of $2.4/share, which is actually up significantly due to strong customer growth, good capacity growth, revenue growth from the S&T services, and good contributions from the service segment. None of these developments are surprising to me, they were all forecasted, and the company reaffirmed its full-year target.

{kind=link}

The company managed a significant increase in Natgas customers, with almost 6,000 new customers added YTD alone, bringing it closer and closer to a 600,000 customer portfolio. The next rate case for the NJGas segment isn't expected until later, with the current filing for the next case expected next year. (Source: NJR IR, 3Q23)

The company is heavily pushing investment into the gas segment, with a good split of front-loaded returns - over 40% of the company's 2023E gas CaPex is earning near-tern returns

We've all read about how clean energy ventures are resulting in less and less returns, due to increased costs of capital. NJR operates only solar projects in its clean ventures, with over 460MW of current capacity, with 1.2 GW of planned capacity in 2027E and beyond. The current pipeline means the capacity will more than double, both under contract or in exclusivity. This is a small point, as I see it, to the company's forward plans for growth.

The company's current capital allocation plan, which saw a peak CapEx in 2021, is being planned in accordance with the earnings growth target of 7-9%, which is above the average for these businesses. The company is projecting cash flows in excess of, or/and closing in on half a billion as early as next year. (Source: NJR IR, 3Q23)

I also remind you that the company's credit rating is one of the best in the entire sector - we're talking A1 stable from Moody's and A+ Stable from Fitch, even if the company does not use S&P Global for this. This is due to an adjusted FFO/adjusted debt of less than 20% - which is up from 14% in 2020 but is expected to go down to 17-18% during the next year. This is one of the least leveraged utilities I have come across - and this is very much in line with what I want to see from companies like this in this environment. This is not the same, of course, as having a good leverage metric based on all perspectives. The company here has a debt/EBITDA of over 5.3x, an interest coverage of 3.6x, and a debt-equity of above 1.55x. This is above the sector average and puts the company below the 50th percentile (Source: GuruFocus). So despite A+, this can be seen as a mixed bag.

The company is fully in line with the current policy landscape both for the state of NJ and overall with the US as well given its clean energy ventures. At worst, I would impact the company's expected earnings from the clean energy somewhat given what we're seeing on the macro side here, but even that is in excess of what I believe it should be doing - the company is simply too good at both hitting targets and within its operating specificities.

What do I mean by this?

I mean that NJR does not miss estimates. Ever. Or at least, not in over a decade, and not with a 10-20% margin of error. Choose what you will, the company beats or hits its targets with the accuracy of a a sniper. No, dear reader. Quality has never been a problem for this company.

The problem is, even though growing on average by 6.4% and seeking to up this to 7-9% per year (I would forecast at 7% to be conservative), the company usually trades at a non-trivial premium. That's where the clincher is.

Even with the company's rather significant decline in pricing that we've seen over the past few months, this does not necessarily equate to this business being "cheap". There are utilities that I would view as more qualitative and with a better upside than this one, but this would require you to be open to investing in European businesses.

Let's look at the valuation of the business here.

NJR - The valuation is actually favorable here

So, if we had any other environment, I might go positive on the stock here. At below $42/share, the company might actually be able to perform well and deliver a double-digit annualized RoR here.

However, since my article back in May, we've also seen a significant change in the risk-free rate, and the company's current 4% yield at this price is not exactly impressive.

In fact, I've judged that I have no choice as of this article but to actually lower my overall price target for NJR as a business - not by massive amounts, but still significant ones. The company would have been a "BUY" under my previous PT, if only barely. However, under the current set of estimates in terms of earnings and in this environment, we're seeing a potential annualized upside of only 8% per year - and that's to a 15x P/E assuming a 5-7% EPS growth rate.

You have to estimate the company at above 17.5x, which is above the company's 5-year average premium, in order to get above 15% annualized RoR. Because my target is over 15%, this is not good enough - especially not going into this environment.

This company does hold a flawless track record in terms of meeting forecasts and estimates - in that they either hit them or beat them - but this does not help when it comes to not beating the minimum target threshold I have here.

NJR, at this particular time, is not in a position where market-beating rates are possible from any conservative valuation. The company is being estimated at price targets ranging from $40/share on the low side to $57/share on the high side, with an average price target of $48/share from 9 analysts.

Only 2 analysts are currently at a "BUY" for this business. The rest are at "HOLD", and one is even at "SELL"/Underperform. (Source: S&P Global)

So while my lowering of my price target, in this case to $40/share, which is the lower end of the analyst range as well, might be extreme - I view it as justified in this environment. At $40/share, we can at least see a 15%+ annualized RoR at a 16-17x P/E, which is not possible today under the sort of earnings estimates that NJR has made a habit out of beating over the last decade or so.

Because of this, I cannot change my rating here - instead, I change my PT and maintain my "HOLD" in this post-3Q23 update.

Here is my updated thesis for NJR.

Thesis

- This is an above-average quality utility with a very attractive set of fundamentals and overall qualities. The yield is growing and well-covered, the stability and the relationships with regulators are solid, and the company operates a very attractive mix of assets in a very attractive geography.

- The company also has some very attractive side operations, giving the company growth potential and service potential beyond its legacy operations.

- At any appealing price below 16x-17x P/E, this becomes a "BUY" to me. But that is not where we currently are, and it seems unlikely that we'll go there anytime soon.

- For that reason, I am maintaining my NJR price target of a conservative normalized $40/share in November 2023, unchanged from my last article, which would be where I would become interested in the stock.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Because the company does not fulfill my valuation criteria - any of them - at this time, I'm forced to go with a "HOLD" here.

For further details see:

New Jersey Resources: Waiting For That Valuation "HOLD"