WY - New REIT Acquisition Target... Themselves

2023-11-08 16:46:25 ET

Summary

- REITs are increasingly buying back their own shares as the best real estate investment.

- Share buybacks are the focus of the third quarter earnings season for REITs.

- Factors such as strong financial conditions, weak property acquisition spreads, and high implied cap rates make buybacks attractive.

REITs are increasingly realizing that the best real estate they can buy is their own shares.

Share buybacks are the clear theme of the third quarter earnings season. It does not seem to be a question of whether to buy back shares or not, but rather how aggressively they should buy back.

This article will discuss the factors that are making share buybacks so attractive for REITs as well as the top opportunities of this nature.

4 factors making buybacks particularly strong right now

- Strong financial conditions and cash flows finance buybacks.

- External property acquisition spreads are weak.

- Discount to NAV and high implied cap rates.

- Private to public arbitrage.

Capital allocation is all about opportunity cost. Free cash flow can be invested in a variety of ways and it is up to the companies to decide which allocation will translate the best to AFFO/share.

Depending on the environment each property acquisition, debt paydown, or share buyback can be the best use of capital, but right now buybacks are the clear winner for a large portion of the REIT universe.

Strong financial conditions supporting buybacks

Since about mid-way through 2013 REITs have been bracing themselves for rising interest rates. While the Fed Funds rate increases were rapid, they were telegraphed since May 21, 2013, which marked the initial taper tantrum.

Because of how well telegraphed the change in interest rates was, REITs had a long window of time during which interest rates were still low yet they knew higher rates were coming. This meant a combination of reducing overall debt levels, terming out debt with long-dated unsecured notes, and making sure most of their debt was fixed rate.

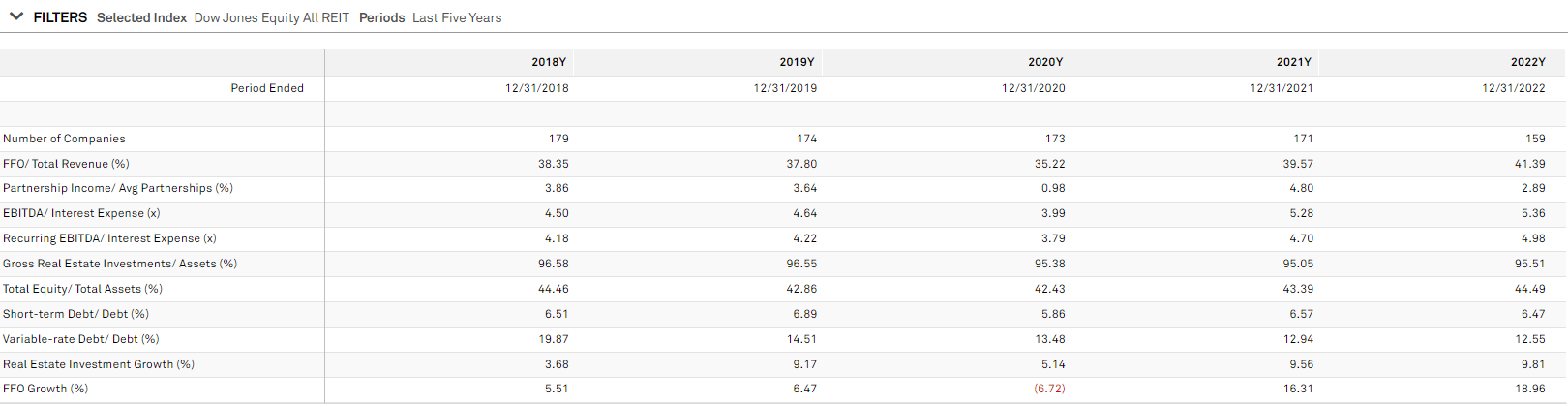

Note in the table below that EBITDA/Interest expense has risen from 4.5X in 2018 to 5.36X in 2022. Short-term debt is just 6.47% of overall debt and variable rate debt has dropped from 19.9% to 12.6%.

{kind=link}

With balance sheets in order, most REITs are in a position where they can buy back shares. The question then becomes whether they want to as opposed to buying properties to grow the business.

Property acquisition spreads are low

There is no doubt that the cost of capital has increased in the last couple of years. In addition to debt financing going up roughly in parallel with prevailing interest rates, equity capital has gotten more expensive due to plummeting share prices.

While the weighted average cost of capital ((WACC)) for REITs used to range from 3.5%-6% depending on the REIT, it is now closer to 5%-8%. Acquisition cap rates depending on the property type a few years ago ranged from 4%-8% which resulted in a nice spread over WACC. Today, however, despite the interest rate environment, cap rates have not risen very much. There has been maybe 50 to 100 basis points of increase to cap rates. Thus, we are looking at cap rates ranging from 4.5%-9% against WACC of 5%-8%.

That is a tiny spread. Some REITs can make it work and still grow through external acquisition, but it is certainly a less desirable capital allocation pathway than the historical norm. Acquisitions are the primary opportunity cost of share buybacks, which makes buybacks functionally cheaper.

Buybacks themselves are far more accretive than normal

The same market price moves that have made equity capital expensive make buybacks higher yield. If a REIT is trading at 20X AFFO, the AFFO yield of buybacks is only 5%. 20X AFFO has previously been a fairly normal multiple.

With all the REIT doom and gloom I think the market has assumed REIT earnings have crashed, but AFFO is actually up for a majority of REITs which combined with the market price declines on the stocks has resulted in extremely low AFFO multiples.

The median REIT now trades at 11.9X forward AFFO. That makes the AFFO yield of share buybacks 8.4%. For most REITs buybacks at this yield are accretive. Beyond AFFO/share accretion, buybacks are accretive to net asset value ((NAV)).

The median REIT is trading at 68.5% of NAV, so every dollar spent on buybacks is immediately accretive to NAV. Think of this as a billion dollars of assets offered on the market for $685 million. The REITs are aware of their asset value and if the market isn't going to give them credit for it they can just take that deal themselves.

Private to public arbitrage

While property acquisitions are often funded with a combination of debt and equity issuance, share buyback funding usually comes from retained cashflows and/or asset sales.

The retained cash flow situation is normal. Dividend payout ratios are slightly on the conservative side, but capex is also a bit higher than normal due to increased labor costs associated with property maintenance.

On a run rate, REITs should be able to buy back a modest amount of stock through retained cashflows. The bigger opportunity right now is selling properties to buy back stock. Quite a few REITs are having success selling properties at cap rates in the 4s and 5s. When those proceeds are used to buy back stock it is wildly accretive. Selling properties at NAV to buy stock at 68% of NAV and sale cap rates around 5% to buy stock at cap rates over 8%.

Reversing capital markets

Common wisdom is that REITs rely on capital markets to grow so at times like this when capital markets are not cooperating REITs have been a bit stifled in growth.

However, REITs are increasingly realizing that they can run the model in reverse. With buybacks, the cost of capital becomes the proceeds of property sales. They can and are growing AFFO/share by shrinking.

Thus far we have discussed why buybacks make sense in theory .

From theory to evidence

Third quarter earnings reports featured a slew of REITs putting this theory to action. Here is some commentary from the conference calls:

David Wold, CFO of Weyerhaeuser Company ( WY ):

"As of quarter end, we had completed $733 million of repurchase under our $1 billion authorization. Looking forward, we will continue to leverage our flexible cash return framework and look to repurchase shares opportunistically"

Paul Pittman, Chairman of Farmland Partners Inc . ( FPI )

"We will continue selling assets at good gains and using those funds to pay down debt and buy back stock as long as the significant discount exists. And it's important to recognize that our gains to date have been very strong, but we are not selling the assets we like the most. We are selling assets that probably have been laggards in terms of appreciation compared to the rest of our portfolio"

Luca Fabbri, CEO of Farmland Partners Inc.

"We have repurchased about 6.4 million shares at an average price of $10.98. So, of those $124 million of proceeds, so far, we used about $70 million in common stock repurchases. We've also paid down about $8 million of Series A preferred."

Ric Campo, CEO of Camden Property Trust ( CPT )

" And so for us, we were aggressive buyers of the stock when the stock was down substantially for a long period of time. And if we have the opportunity to do it, we probably will."

Dan Oberste, CEO of BSR Real Estate Investment Trust ( BSRTF )

"I think our NCIB is capped at around $35 million give or take of share repurchases. I believe it expires subject to renewal in October of this year. And to date, I believe in the last 10 or 11 months, we've acquired about 20 million. Leaves us about 15 million of availability with a REIT that just produced a NAV of $20.40 on 31 properties against a trading price on the TSX of $12.90. To me, 15 million is the amount that we're able to buy before the October renewal period. Doesn't seem unreasonable that we'd continue that pace. But price dependent and dependent on with an eye towards our liquidity. Right now, it's an incredible deal. We can't buy a property at a 6.7 cap, we certainly buy our stock at a 6.7 cap"

The Bottom Line

Valuation matters. AFFO multiples matter. NAV discounts matter. When the market isn't valuing a company properly, they can directly convert asset value into realized value through selling the property and buying back that stock. I think these buybacks are just the tip of the iceberg.

For further details see:

New REIT Acquisition Target... Themselves