DT - New Relic: The Impact Of Revenue Growth Deceleration (Rating Downgrade)

2023-06-27 18:11:46 ET

Summary

- Limited growth, high valuation, and strong competition make paying a premium for New Relic, Inc. stock less appealing.

- Concerns about profitability: while there was improvement, future non-GAAP operating margins are not expected to be significantly higher, affecting underlying profits.

- I turn neutral on this stock.

Investment Thesis

Back in February, I made a bad call. I issued a buy rating New Relic, Inc. ( NEWR ) stock, where I went on to state,

It's difficult to say that this is the ''best'' observability company. But there's clearly much to be excited about from this quarterly earnings result.

It turns out that my statement above was only partially accurate. I was right to say that New Relic is perhaps not the best observability company. But also, I was too eager to give the company the benefit of the doubt for its improving profitability.

With the passage of time, not only have its revenue growth rates meaningfully slowed down, but New Relic's valuation remains rich for what it offers, at 26x forward free cash flow. Consequently, I'm now neutral on this stock.

Why New Relic?

New Relic is similar to Dynatrace ( DT ), in that they both provide application performance monitoring and observability solutions.

The key difference between the two is that New Relic is more customizable and requires more integrations for comprehensive coverage. While Dynatrace emphasizes full-stack observability capabilities.

However, to be clear, there's a lot more that makes them similar than makes them different. Case in point, they are both focused on allowing businesses to identify, monitor, and resolve the performance of applications and infrastructure in real time.

In fact, as you can see above, the share prices of both companies in the past 3 years are practically indistinguishable.

However, I submit that from this point forward, we are likely to see a divergence between these two names. Why?

Because New Relic's revenue growth rates are decelerating, while its valuation remains high.

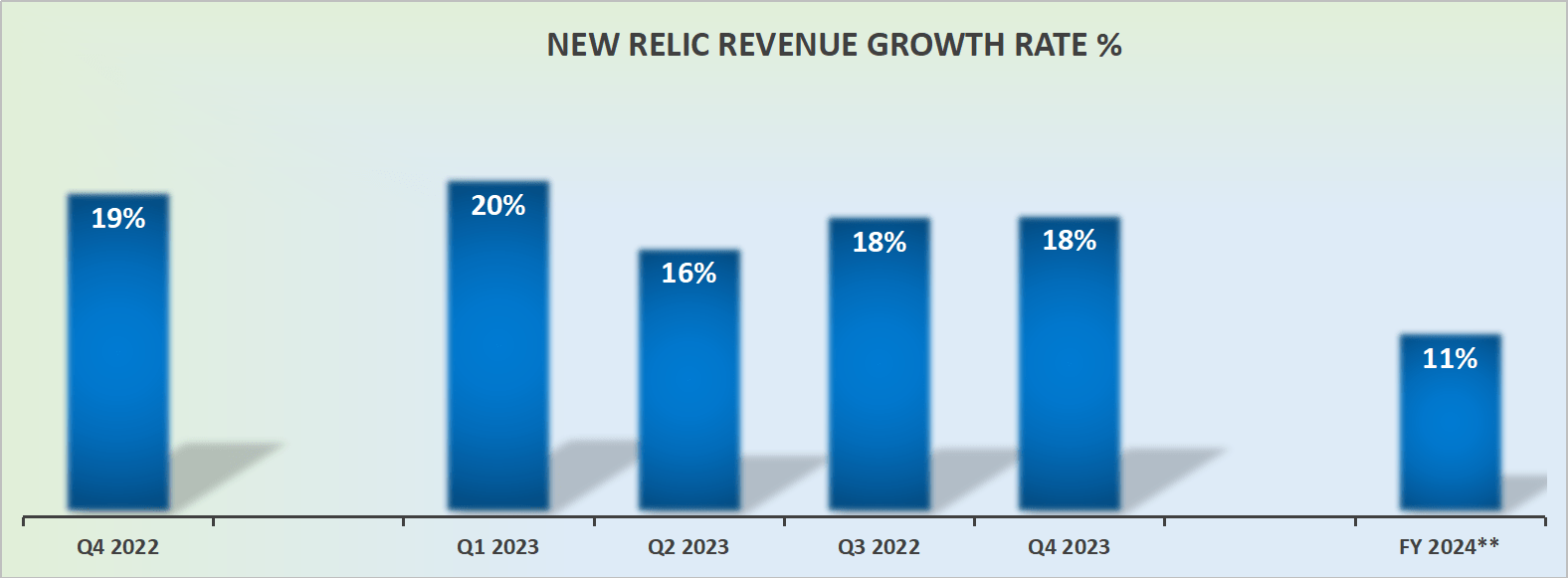

Revenue Growth Rates Hit A Speed Bump

{kind=link}

As touched on already, New Relic's revenue growth rates are slowing down. Simply put, New Relic can no longer be counted on as a sustainably fast-growing business.

And if it cannot be counted on as a fast-growing business, that means that investors will be increasingly looking towards its bottom line to support its valuation. And therein lies the problem, which we'll discuss next.

Profitability Profile Leaves Much To Be Desired

As I alluded to at the start of this analysis, the one thing that got me bullish on New Relic had been its rapid progression in improving its underlying profitability.

Recall, from fiscal 2022 into fiscal 2023, New Relic's underlying profitability jumped by just over 18%. More specifically, there was a terrific improvement to go from negative 8% of non-GAAP operating margins to positive 11%.

The problem now is that looking ahead to New Relic's fiscal 2024, its current fiscal year, at the high end of New Relic's guidance , New Relic points to around 15% non-GAAP operating margins.

Even if we presume that New Relic ends up delivering slightly higher than non-GAAP operating margins, and reaching around 16% non-GAAP operating margins, this means that its underlying non-GAAP operating profits are unlikely to be much higher than $170 million of non-GAAP operating profits.

Altogether, this leaves a stock that is barely growing on the top line by more than 11% CAGR priced at about 26x forward free cash flows. This is not the most shocking valuation in tech-land. However, for a business with only a limited moat around its operations, and plenty of competitors that are growing much faster, I am not overly enthused to pay such a high premium for this stock.

The Bottom Line

In my analysis, I revisited my previous buy rating on New Relic and adjusted my stance to neutral.

While I had initially been hopeful about New Relic, Inc.'s potential to improve profitability, I'm now uncertain this is the case. Or at least not enough to support its valuation.

Furthermore, New Relic's revenue growth rates have slowed down, and its valuation remains high at 26x forward free cash flow.

Going forward, on the back of its slowing growth revenue growth rates, I believe that New Relic, Inc. investors will be increasingly focused on its free cash flows and questioning whether the stock is really cheap enough to provide a margin of error. And I'm not sure it is cheap enough.

For further details see:

New Relic: The Impact Of Revenue Growth Deceleration (Rating Downgrade)