NYC - New York City REIT: A Dangerous Dip To Buy

Summary

- The REIT's conviction on office properties could be a significant cause for concern.

- Although the fund's debt gearing is well arranged. Its core funds from operations are receding.

- Historical price action implies that New York City REIT is disliked during risk-off environments.

- REITs could pivot soon. However, New York City REIT's prospects are questionable.

REITs have not experienced the best of times during 2022's bear market. One of the REITs that has ended up on the wrong side of things this year is New York City REIT ( NYC ). Despite its near 70% year-to-date losses, we believe the REIT could shed even more value as its key influencing variables paint a blurry picture.

Operational Analysis

Work-From-Home Exposure

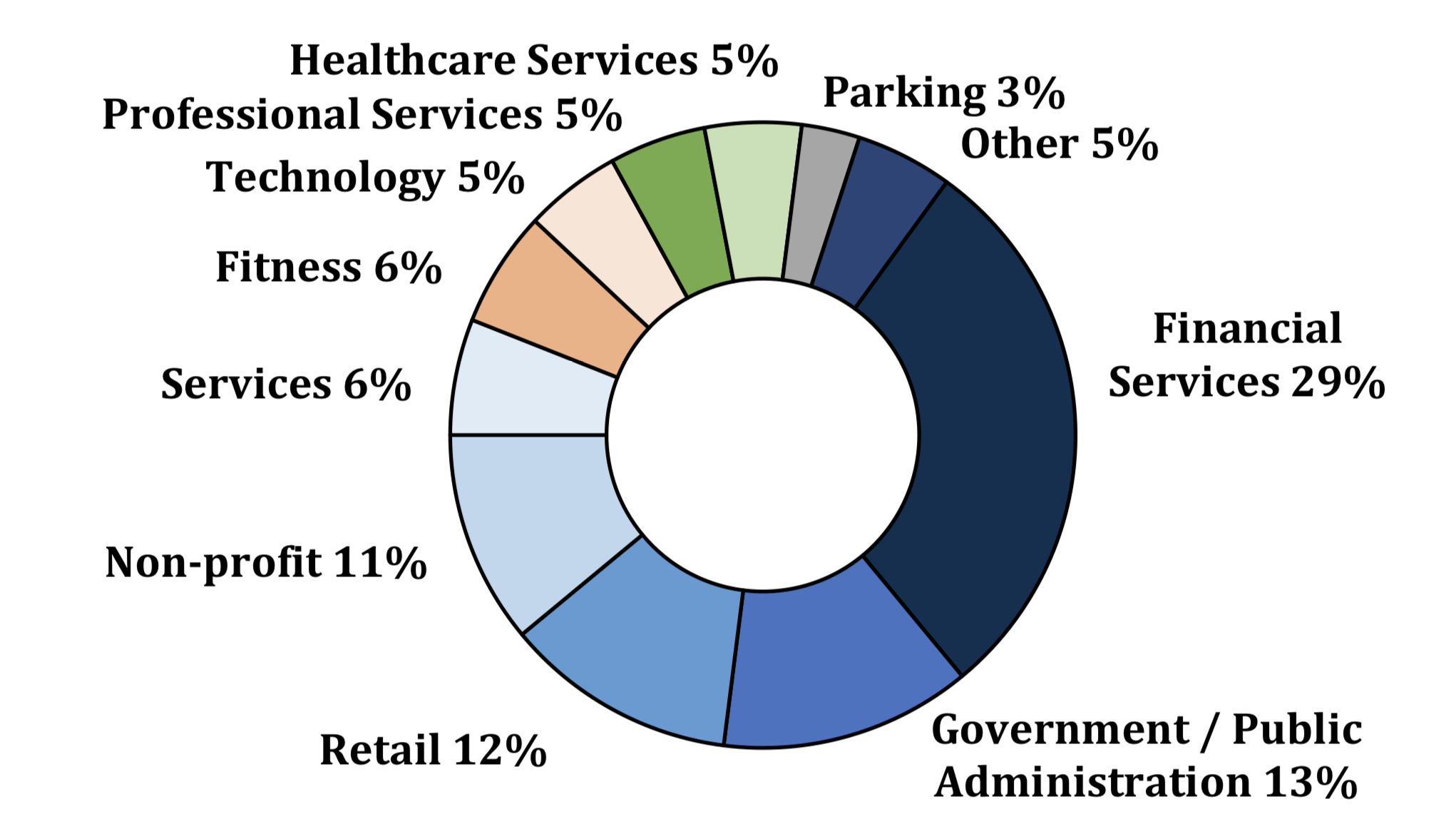

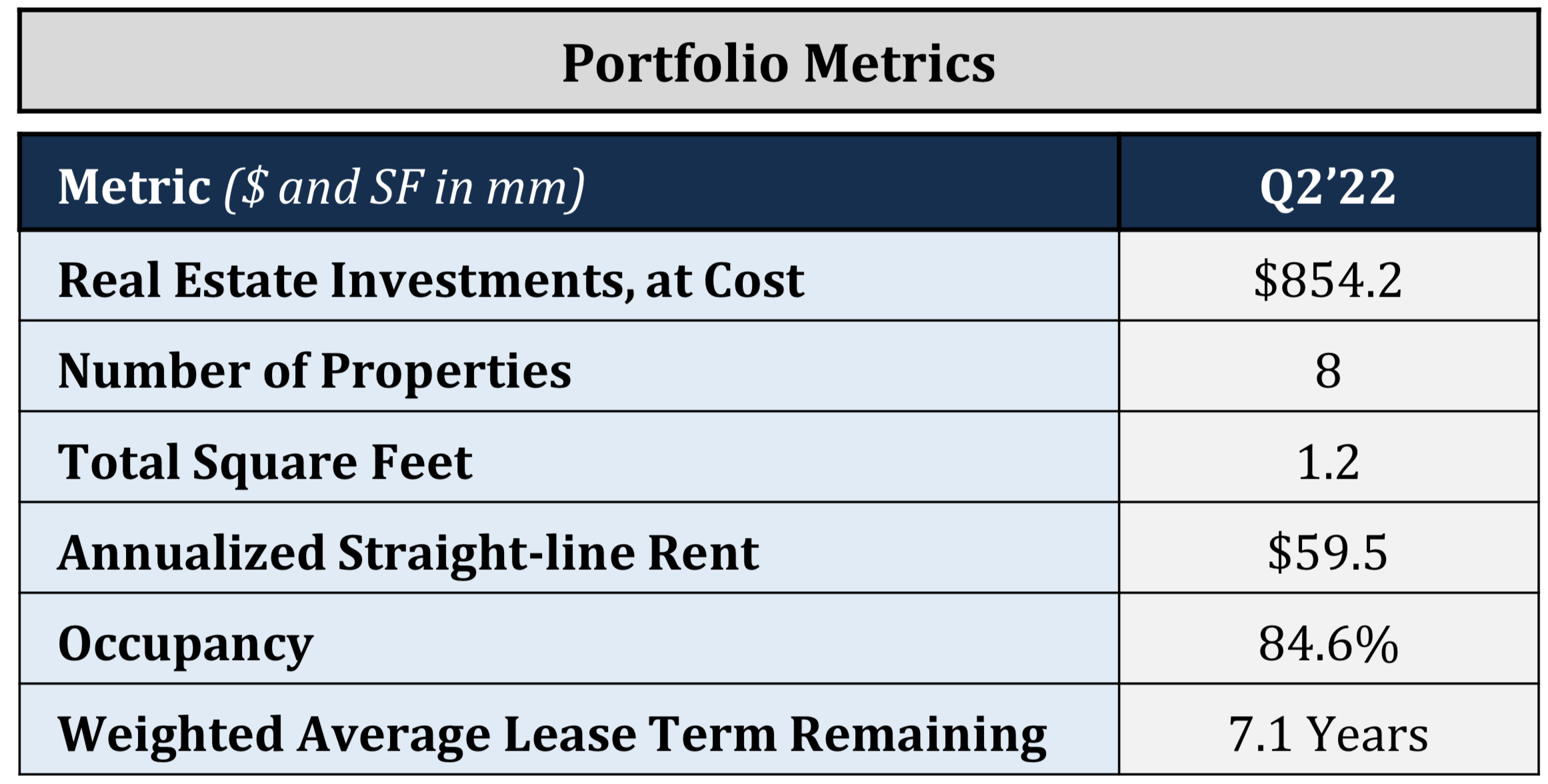

New York City REIT operates commercial properties with a few notable tenants, such as Citi National Bank, Equinox, CVS ( CVS ), and Cornell University. Despite the REITs respectable portfolio, it has struggled with the post-pandemic zeitgeist, which has been very much anti-office real estate. Moreover, the fund's 84.6% occupancy rate and questionable portfolio diversification sound alarm bells.

Much of the REIT's capital is exposed to potential "work from home" sectors such as financial services and information technology. In addition, its retail exposure includes a non-credit-rated tenant called "I Love Gifts New York". Thus, we would sadly have to conclude that this REITs portfolio is unfavorable.

{kind=link}

{kind=link}

Income Statement Woes

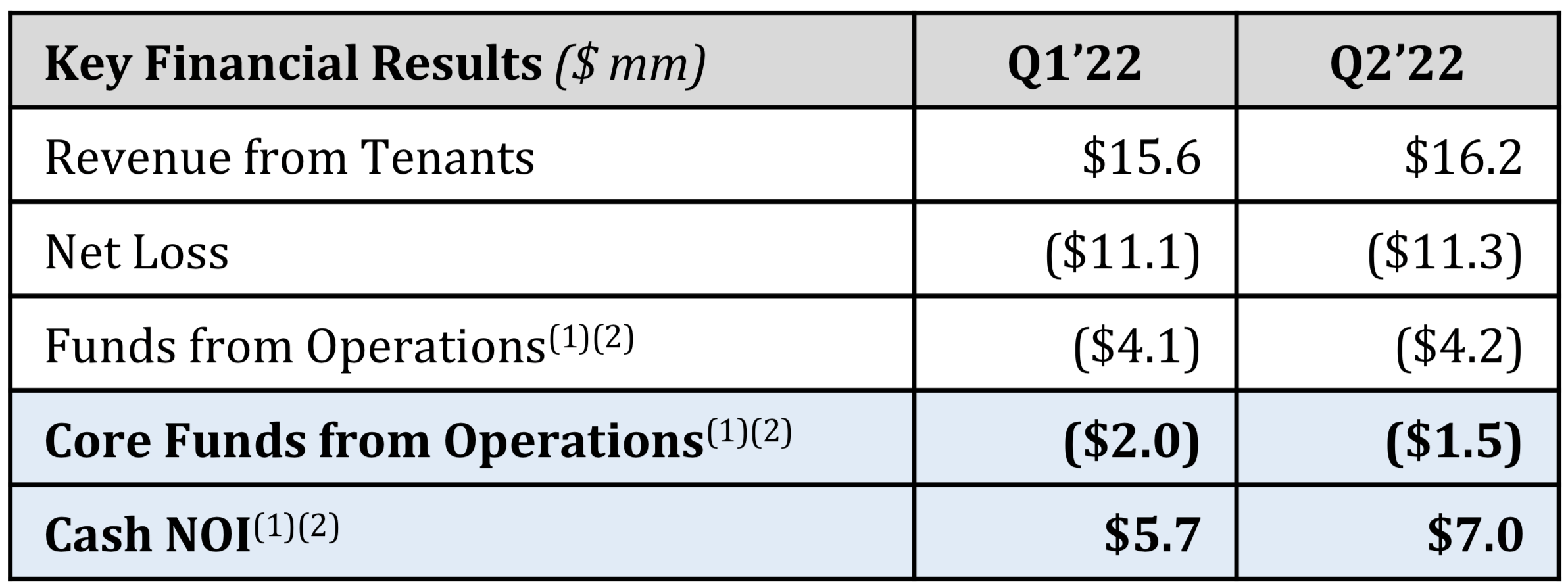

Furthermore, we believe New York City REIT's income statement is in poor health. The fund's revenue and cash net operating income have both increased since the same time last year. However, its funds from operations and income from core operations have both weakened severely. A REIT's income from core operations is a key feature of the fund's quality, and most REITs are valued by measuring the trajectory of their funds from operations. Thus, collectively, New York City REIT's income statement is worrisome.

{kind=link}

Increasing Borrowing Rates

An additional headwind to consider is the recent rise in commercial borrowing rates. Although rising rates might activate rental demand, they are mostly bound to contractionary economic policies.

Contractionary economic policies usually compress economic output, and real estate prices tend to trend lower as a consequence. Theoretically speaking, cyclicality is the main culprit. Furthermore, New York City REIT is exposed to commercial property. Thus, 'today's' receding GDP might work to the REIT's disadvantage.

Select Commercial Funding LLC

{kind=link}

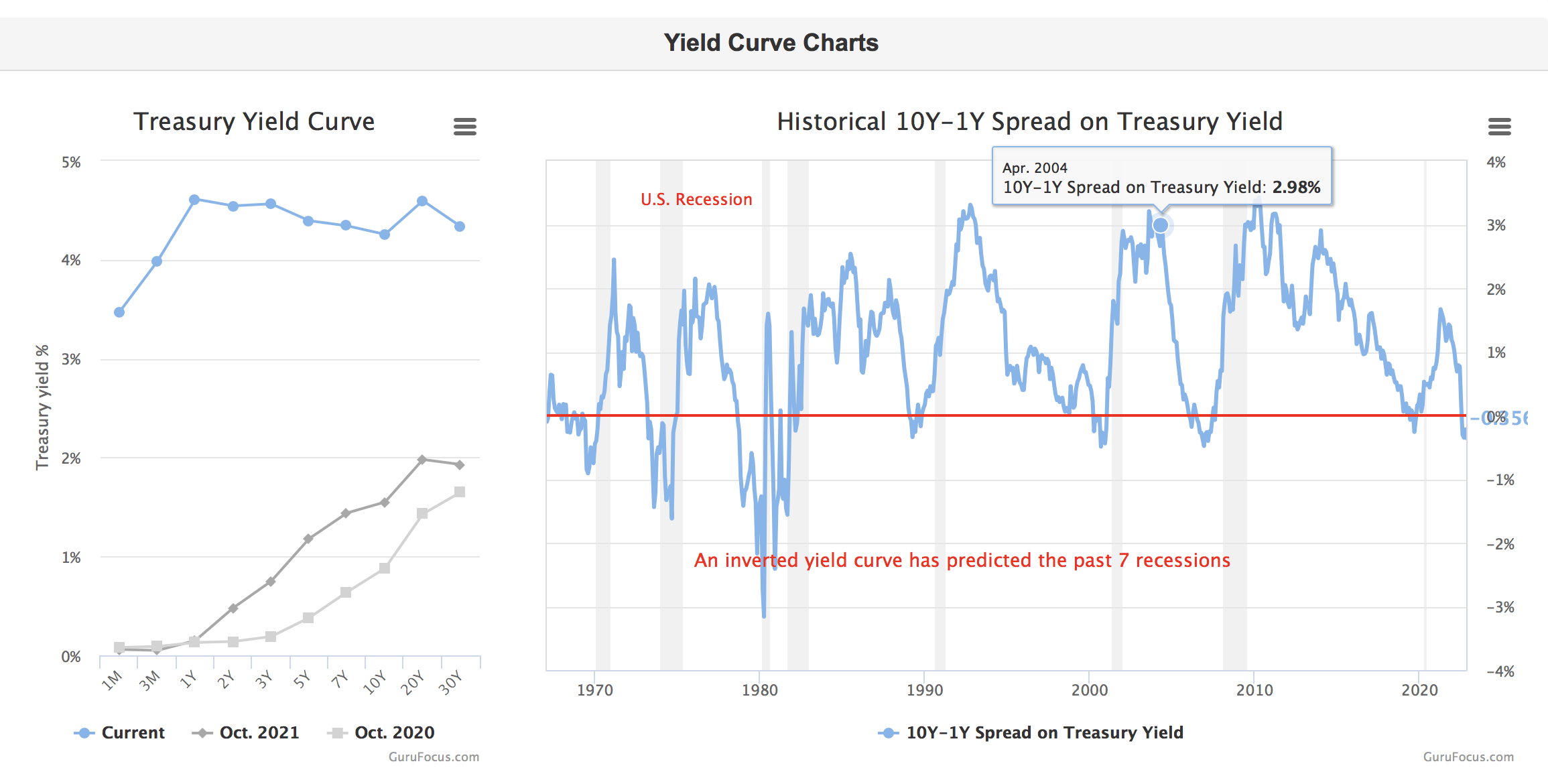

Lastly, the yield curve is a concern. A receding yield curve usually indicates an impending recession. Therefore, real estate could crumble if future interest rates follow the yield curve's trajectory.

{kind=link}

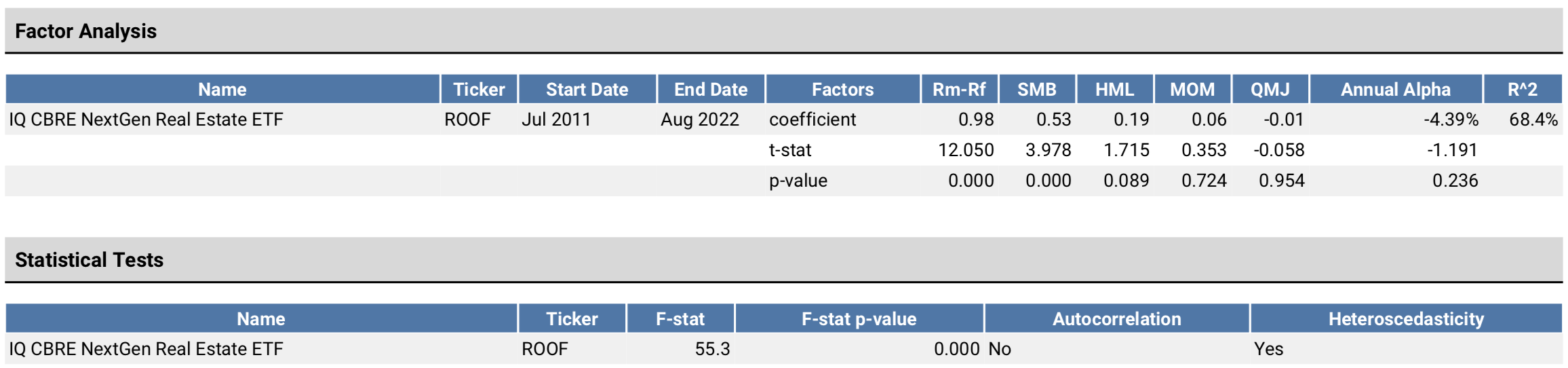

Price Action - Factor Analysis

We ran a regression (diagram below) on the REIT's past returns relative to various market environments and discovered the following about New York City REIT.

- SMB - The REIT outperforms whenever investors are small-cap stock seeking. The market is usually conducive to small-cap stocks whenever the economy is in an early-stage expansion.

- HML - New York City REIT mostly outperforms whenever the broader market is value-seeking. Value investors are usually most active in early-stage bull markets.

- MOM - The REIT outperforms when the broader market is in a momentum trajectory. Momentum usually occurs in late bull markets as investors hold onto investments longer than they ideally should.

- QMJ - New York City REIT exhibits a negative correlation to quality stocks. Quality stocks are characterized by features such as high profitability, robust balance sheets, and strong business fundamentals. Quality stocks mainly tend to outperform whenever recession risk is high.

{kind=link}

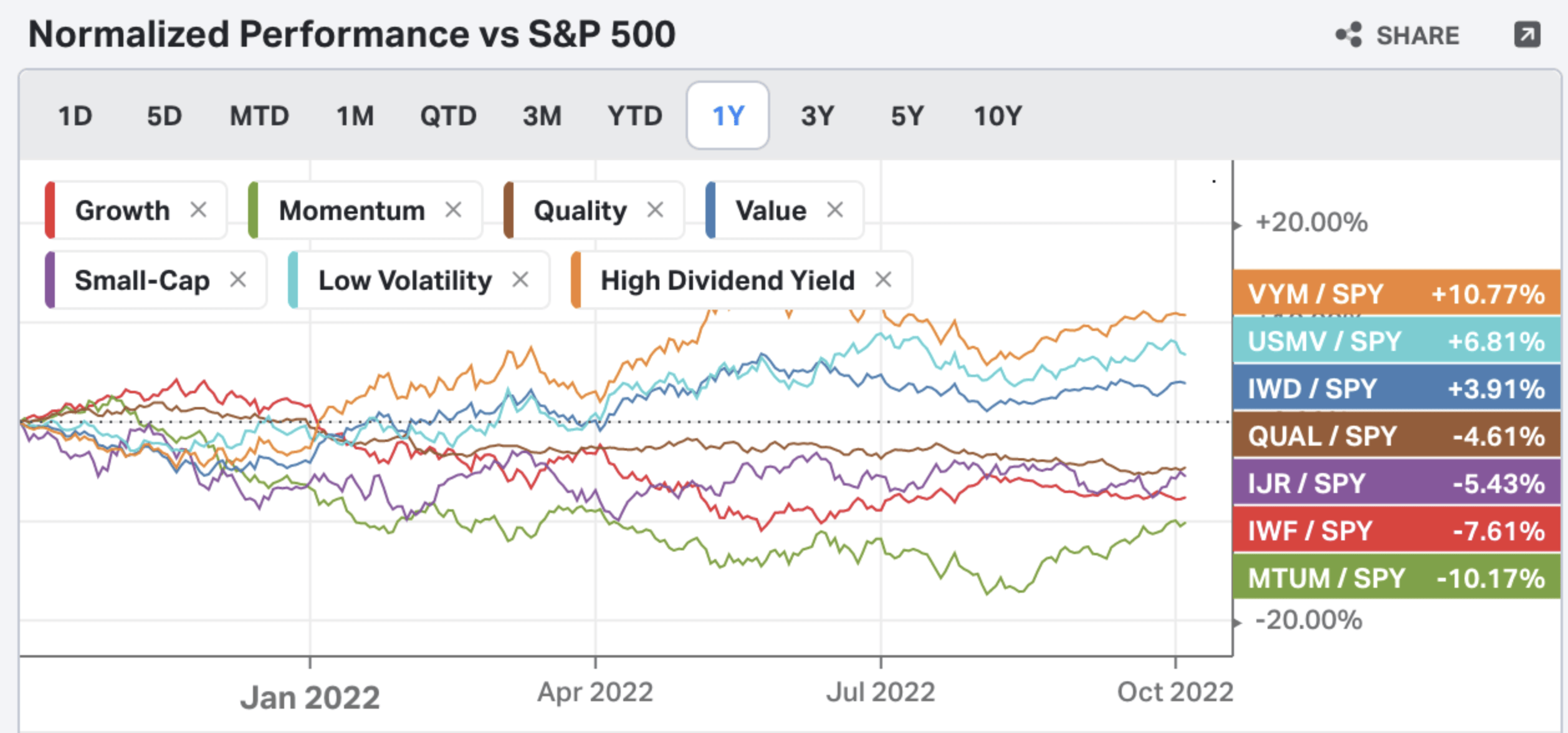

Based on the current market climate, it is unlikely that New York City REIT's positive correlation to small-cap and momentum stocks could yield benefits. Investors tend to drift towards risk-off market segments such as quality, low volatility, and high dividends whenever recession risk is high. Thus, the REIT could face further headwinds based on retrospective market performance and current economic indicators.

Koyfin

{kind=link}

Potential Counterargument

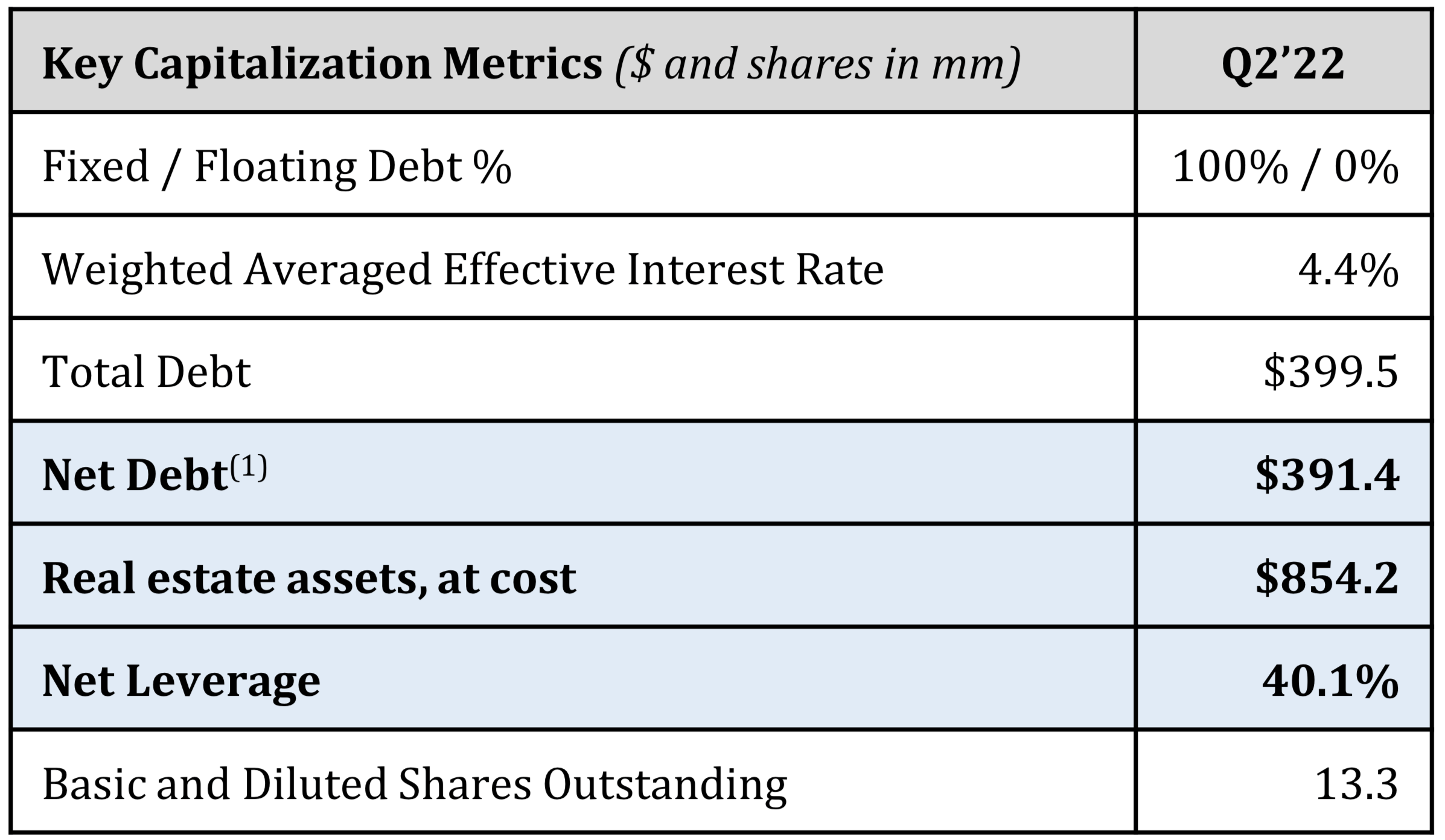

Impressive Debt Utilization

Despite all of its negatives, we realize that New York City REIT has done a phenomenal job with its debt structuring. The fund does not have any variable debt, meaning its exposure to interest rate risk is probably low. Moreover, the REIT's 40.1% net leverage suggests a likely ability to pass much of its value through to its shareholders.

{kind=link}

Potential Rental Market Growth

There's a contra argument concerning rising interest rates and property devaluation. The opposing view is that REITs could benefit from rising interest rates as more consumers will opt for rental properties instead of buying a property. As such, New York City REIT could benefit from a bidding war in the rental space and flow through more dividends to its investors.

Furthermore, New York City REIT's "quality lease" exposure stands out, with its 85% occupancy holding contracts of 7.1 years or longer . If given enough time, the REIT could attract additional long-term tenants while curbing its vacancy rates.

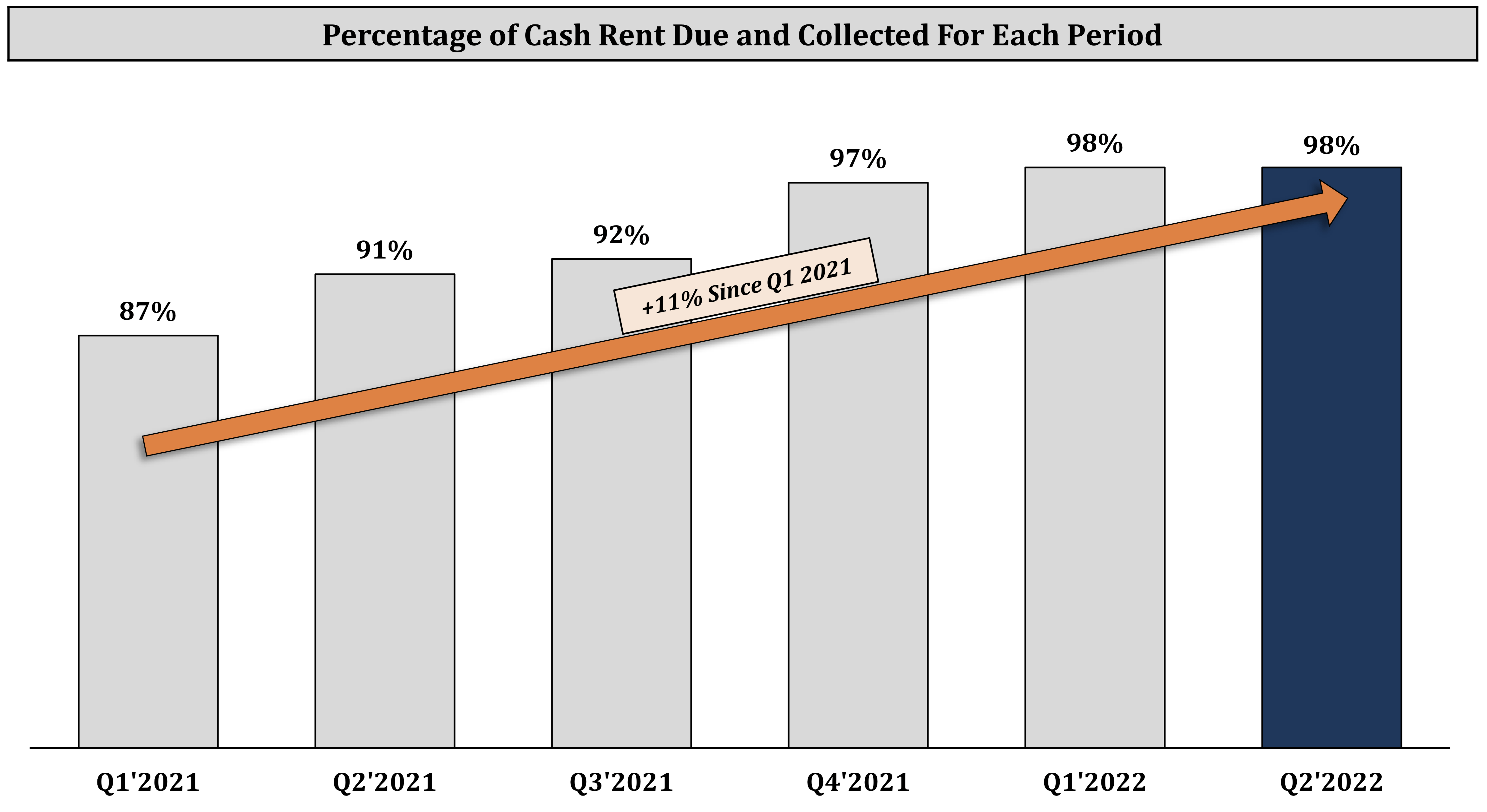

A final consideration regarding the REIT's rental attributes is its 11% increase in cash collections since its first quarter in 2021. If this trajectory continues, we might see much of the REIT's non-investment grade counterparty risk phased out.

{kind=link}

Price Reversion

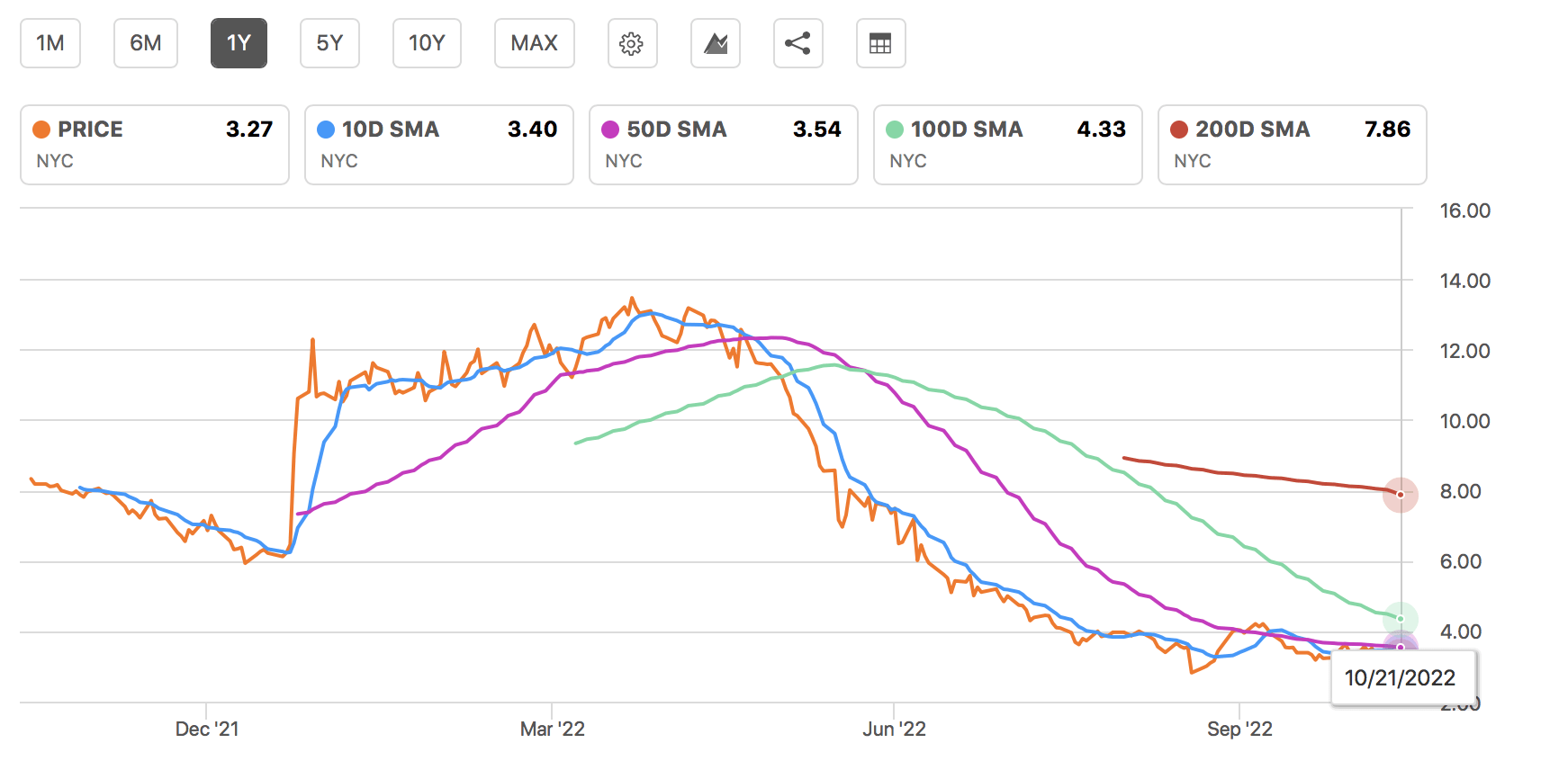

Lastly, New York City REIT is trading below its short and long-term moving averages. Thus, there is a possibility that a reversal might occur, which could send the REIT into recovery mode.

{kind=link}

Final Verdict

New York City REIT is suffering from receding funds from operations. Moreover, office properties' declining popularity will likely draw a draw on the REIT's prospects. Furthermore, the REIT's price action reveals risk-on characteristics, which are not necessarily favorable in today's market environment.

For further details see:

New York City REIT: A Dangerous Dip To Buy