HBAN - New York Community Bank Delivered Solid Earnings And Came Out Of The Financial Debacle Stronger

2023-05-01 09:00:00 ET

Summary

- NYCB delivered a strong Q1 earnings report, and shares have appreciated 66.25% since my last article on 3/15/23.

- NYCB strengthened its balance sheet, its earnings potential and drove its book and tangible book value higher in Q1 after the asset acquisition from Signature Bank.

- NYCB trades at a discount of -24.88% to its book value, and despite the recent appreciation, I believe shares are going higher.

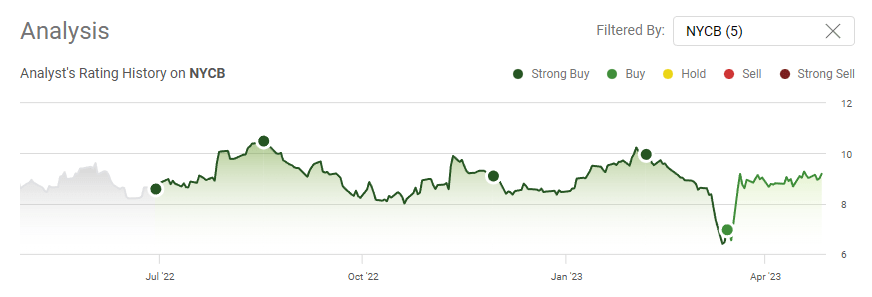

Thomas Cangemi should have started New York Community Bank's ( NYCB ) Q1 2023 conference call off with a big Ric Flair WOOOOHHHHHH. Silicon Valley Bank (SIVB) fiasco caused considerable amounts of concern throughout the banking industry as fears that the run on SIVB would spill over into the regional sector. Talking heads were discussing the likelihood of consolidation occurring into the large money centers and smaller banks having less relevancy in 2023 than they did a decade prior. On 3/15/23, at the height of the banking debacle, I wrote an article ( can be read here ) explaining why NYCB looked like a value play when shares traded for $6.43. It's a month and a half later, and NYCB is up 66.25% since that article was published and delivering a Q1 earnings beat. I don't have a crystal ball, but looking at the numbers, NYCB looks stronger than before, and I feel there is still value left to be unlocked. NYCB still yields just over 6%, and I think shares are headed higher.

{kind=link}

NYCB comes out of the gate swinging in Q1 2023 and delivers a blow to anyone who speculated they would be impacted by the recent financial debacle

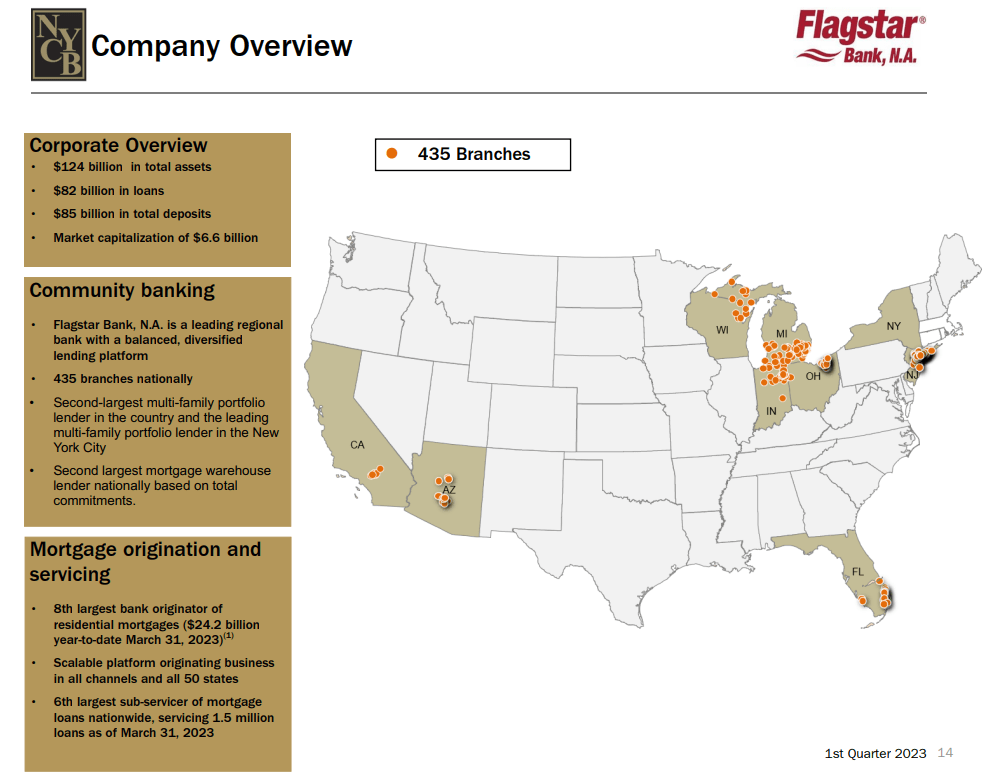

NYCB has set the stage for an interesting 2023 after generating $2.65 billion in revenue and driving $0.23 on non-GAAP EPS, a $0.02 beat compared to the consensus estimates. Going into the year, NYCB acquired Flagstar, and coming out of the SIVB crisis, NYCB's subsidiary Flagstar purchased certain assets and assumed certain liabilities of Signature Bridge Bank from the Federal Deposit Insurance Corporation ((FDIC)). Included in this transaction was the purchase of $25 billion in cash and $12 billion in mostly commercial and industrial loans. They also acquired approximately $34 billion of deposits, all of legacy Signature's core deposit relationships, including both the New York and West Coast private client teams, its wealth management and broker-dealer business, and Signature's specialty finance lending team. All of Signature's branches have been re-branded to Flagstar Bank, N.A. NYCB granted the FDIC equity appreciation rights in common stock in connection with the acquisition. On March 31, 2023, the FDIC exercised its equity appreciation rights, and NYCB issued 39,032,006 shares in, which the FDIC will use all reasonable efforts to sell these shares over a 40-day period beginning April 28, 2023.

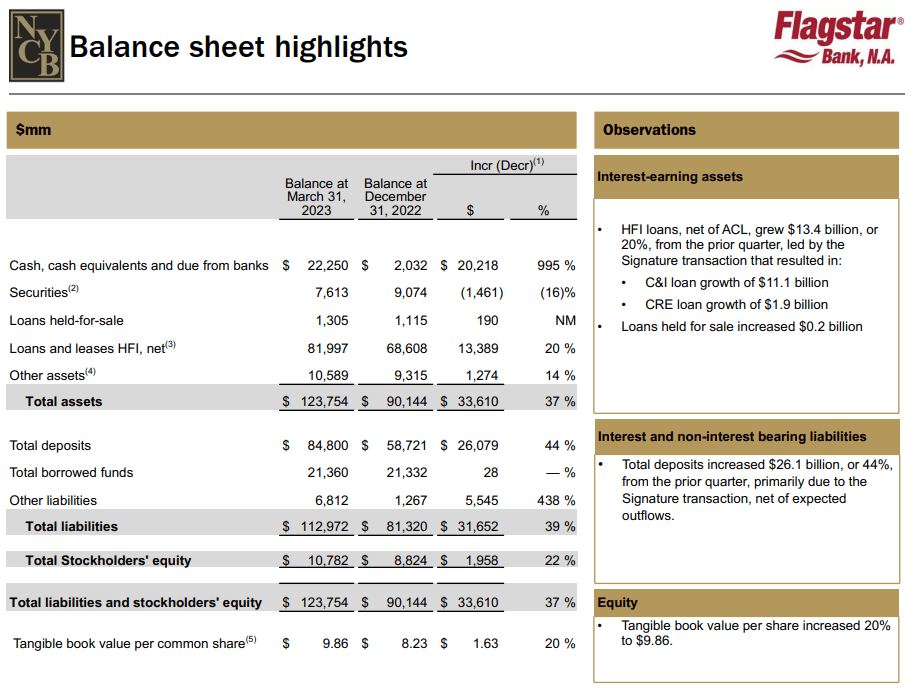

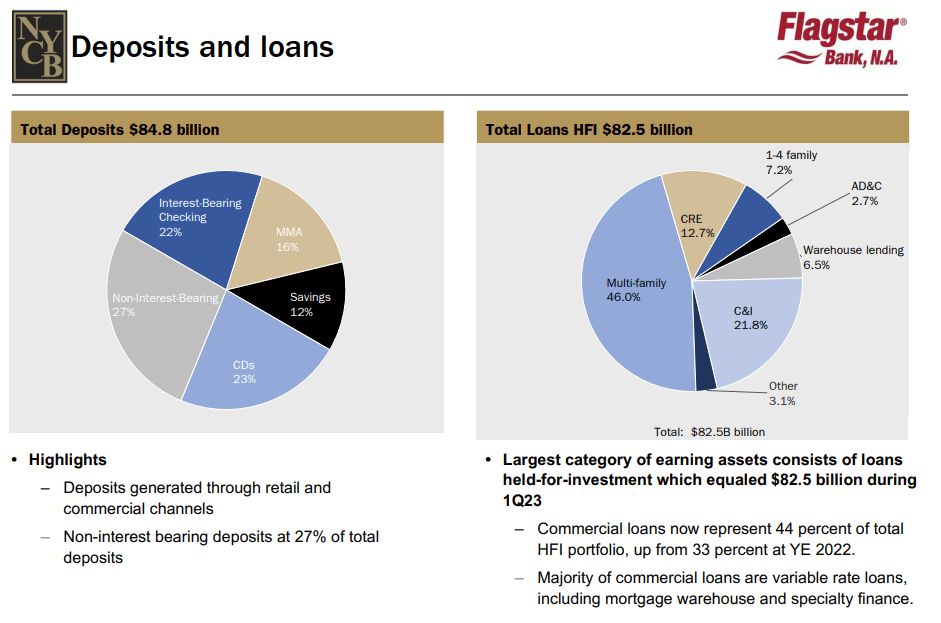

NYCB's balance sheet further improved due to its recent activity. NYCB used a portion of the $25 billion of cash to pay down a portion of its wholesale borrowings. At the end of Q1, NYCB ended with $123.8 billion in total assets, a 37% QoQ increase from the $90.12 billion on the books at the end of 2022. NYCB's total net loans and leases held for investment were $82 billion, up 20% from $68.61 billion. NYCB's total deposits increased by 44% QoQ to $84.8 billion, and total shareholder equity increased 22% to $10.78 billion. The tangible book value of NYCB grew 20% QoQ to $9.86. There is still more than $4 billion in additional equity on the balance sheet than NYCB's market cap today.

{kind=link}

In addition to driving shareholder equity and book value, I was looking forward to seeing how the loans and deposits matured in Q1. Prior to the results, NYCB had $68.61 billion in loans and $58.72 billion in deposits on the books. This was a bit concerning because it created a loan-to-deposit ratio ((LDR)) of 1.17x. This isn't great for banks which was clearly demonstrated in March. While no 2 portfolios are the same, having an LDR of under 1x gives me peace of mind. NYCB's total deposits increased to $84.8 billion, while its total loans increased to $82.55 billion, placing its LDR ratio at 0.97x. NYCB no longer has more loans than deposits on its balance sheet, which helps deleverage the company and makes me much happier.

{kind=link}

In Q1, NYCB delivered $2 billion in net income, which was mainly derived from a bargain purchase gain from the Signature transaction. The adjusted net income available to common shareholders was $159 million, up $20 million QoQ. Q1's net interest margin ((NIM)) of 2.60%, was up 32 basis points QoQ and its net interest income ((NII)) increased 46% QoQ to $555 million. In Q2 of 2023, NYCB sees its NIM expanding to 2.7 - 2.8%. NYCB also declared its Q2 dividend of $0.17, in line with its previous dividend payable on 5/18, as it goes ex-dividend on 5/5. NYCB is in a stronger position now than it was in Q4 2022, and the dividend continues to be paid regardless of what the bears have speculated. I am excited for 2023 as I see more value to be unlocked in shares of NYCB.

{kind=link}

How NYCB is stacking up to its peers and why I see value after the recent appreciation

Based on NYCB's Q1 presentation I am changing up its peer group to reflect what they consider their peer group to be:

- Western Alliance Bancorporation ( WAL )

- Valley National Bancorp ( VLY )

- Citizens Financial Group ( CFG )

- KeyCorp ( KEY )

- M&T Bank Corporation ( MTB )

- Huntington Bancshares Incorporated ( HBAN )

Steven Fiorillo, Seeking Alpha

{kind=link}

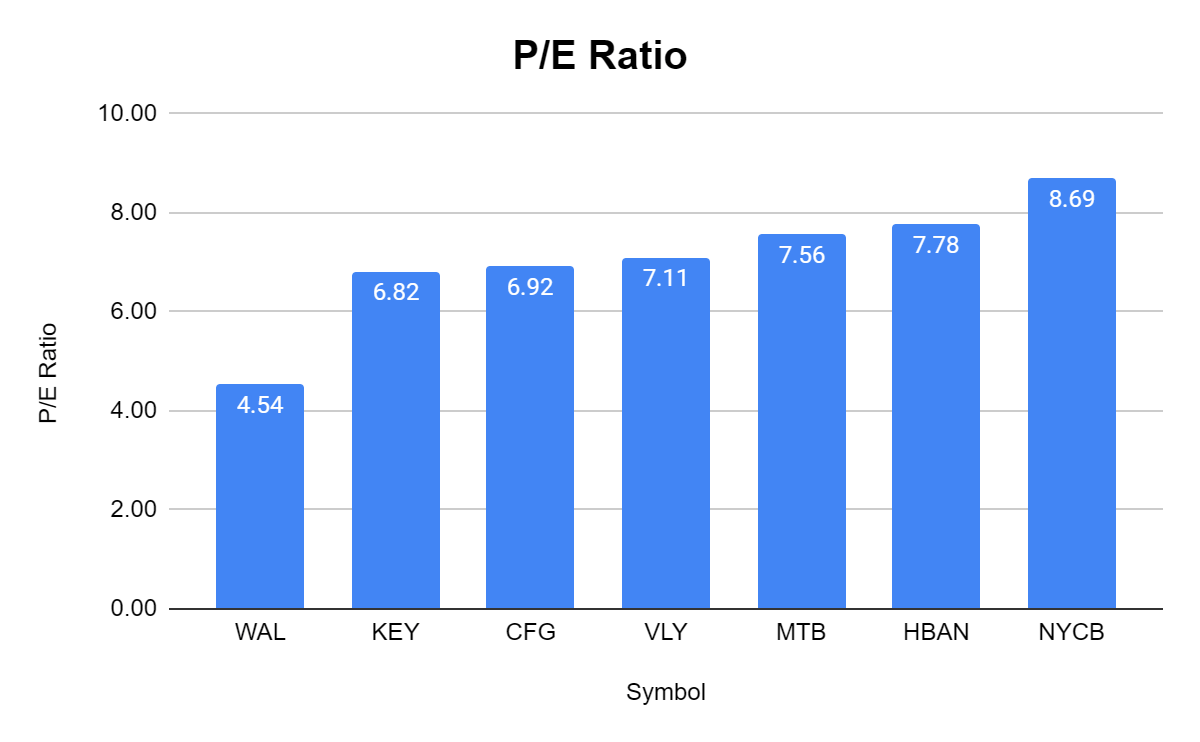

The recent appreciation in share price has pushed NYCB's P/E ratio significantly higher. Last time I wrote an article, its P/E was 5.93, and it was trading at the lowest position in the group. Now the roles are reversed, and NYCB has a P/E of 8.69 and trades above the peer group average of 7.06. I am fine with this, as I think anything under 10 is undervalued for NYCB.

Steven Fiorillo, Seeking Alpha

{kind=link}

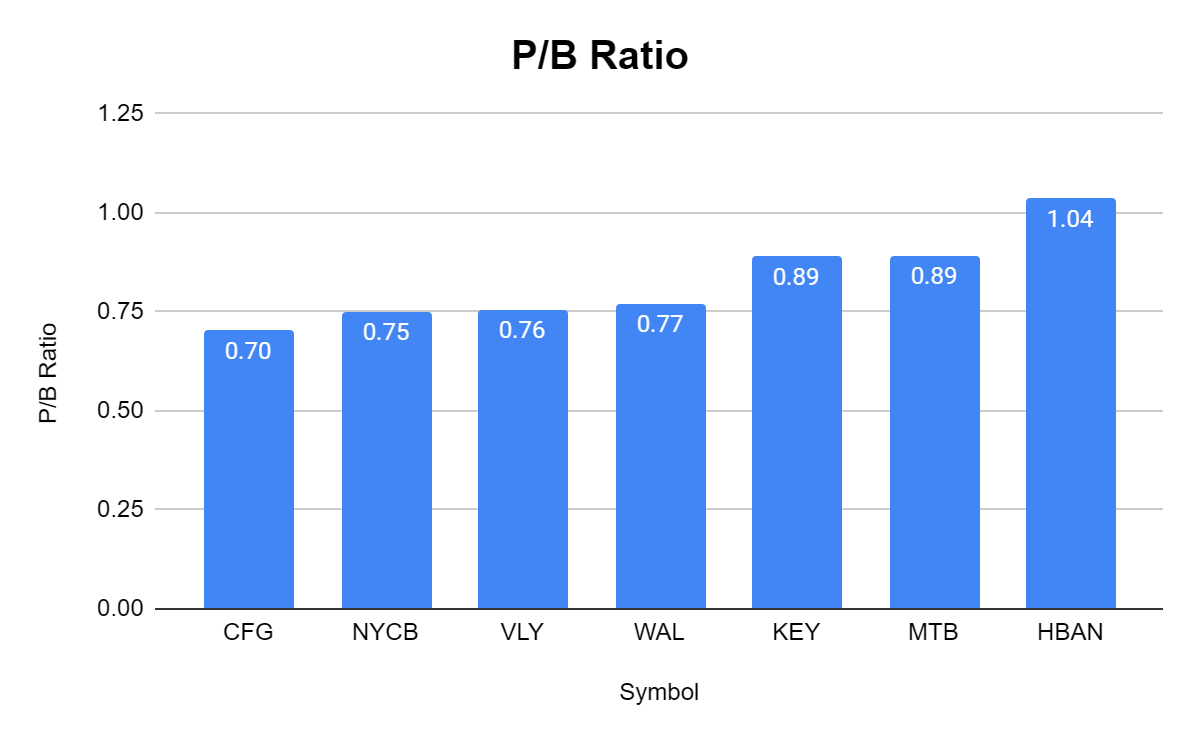

NYCB increased its book value to $14.23 and has a price-to-book of 0.75 which is the 2 nd lowest in the group. The peer group average is 0.83, placing NYCB slightly under where its peers collectively trade at.

Steven Fiorillo, Seeking Alpha

{kind=link}

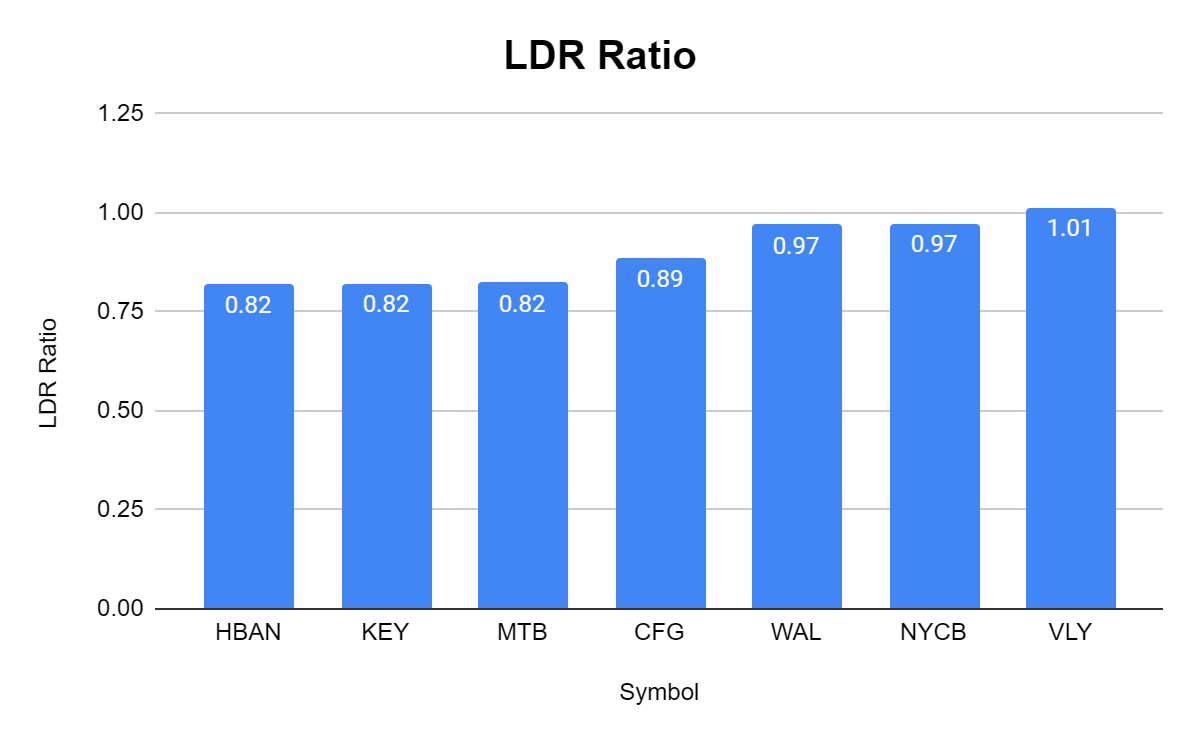

As I discussed earlier, I am very happy that NYCB no longer has an LDR over 1x. NYCB is still trading over the peer group average of .9x, but it's delivered its balance sheet and decreased its LDR from 1.17x to .97, which is a win. I would like to see this get a bit lower, but I am fairly happy at the moment.

Steven Fiorillo, Seeking Alpha

{kind=link}

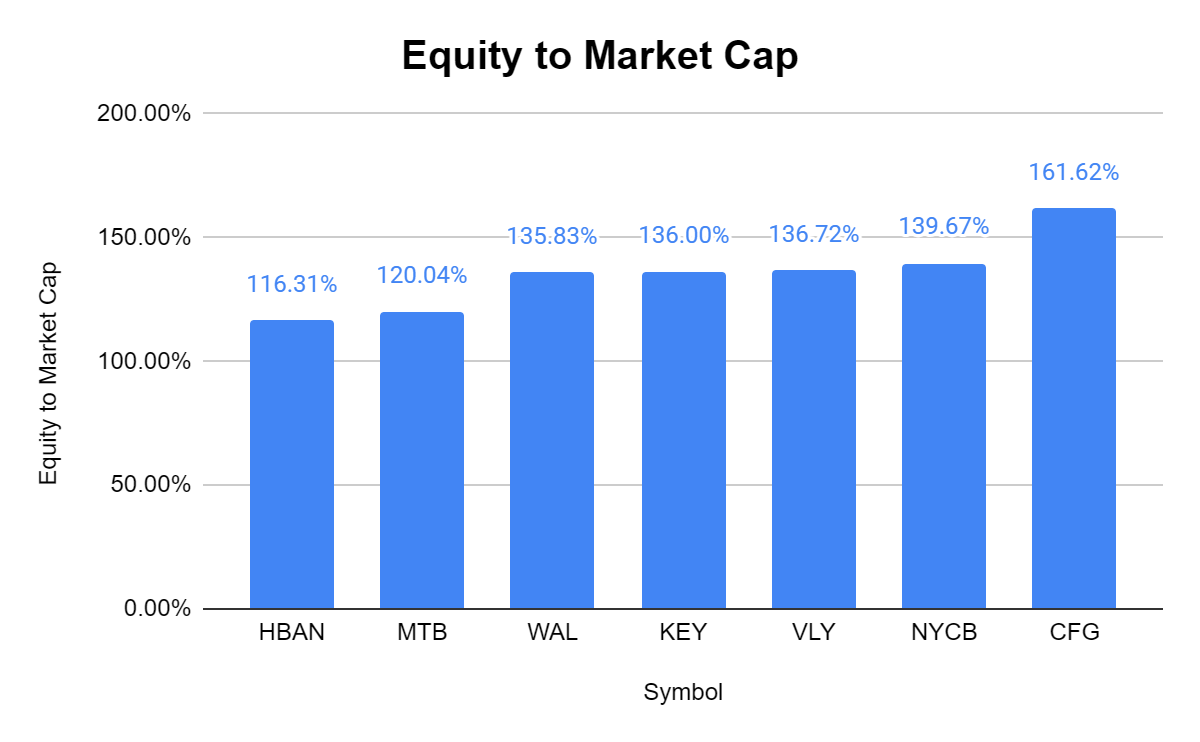

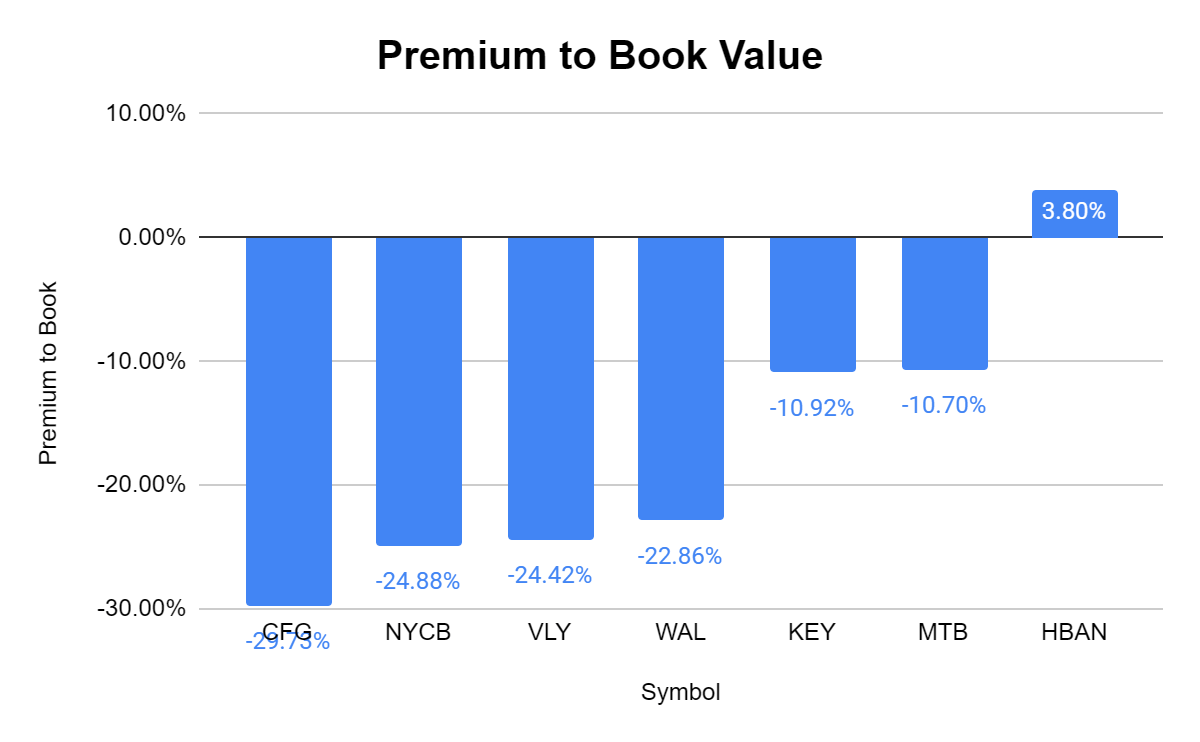

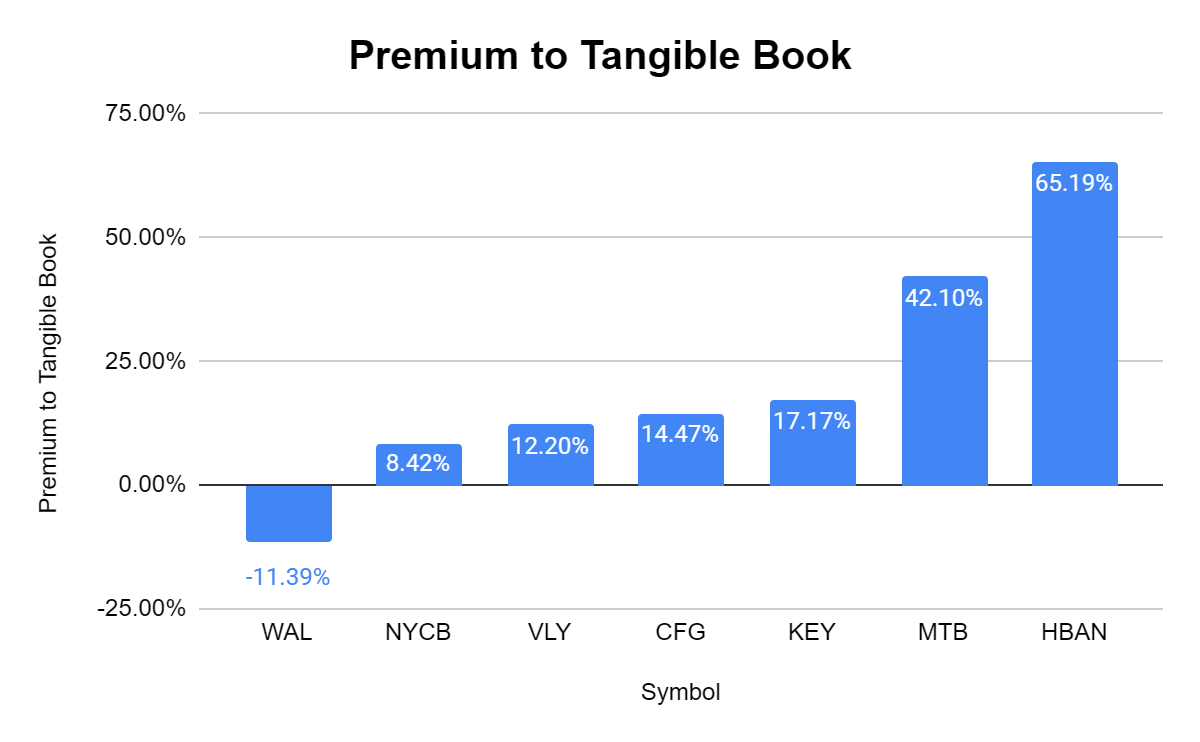

NYCB has 139.67% of its market cap in total equity on the balance sheet. NYCB equity to market cap ratio is slightly above the peer group average, and I am still shocked that its equity trades at this large of a discount to the market cap. NYCB is also still trading at a -24.88% discount to book value. The peer group trades at a -17.1% discount to book, and I am surprised that there is still this much of a gap between NYCB's share price and its book value. When looking at tangible book value, NYCB trades at an 8.42% premium, while the average premium is 21.17% for the peer group. Overall, NYCB looks undervalued after looking at these metrics.

Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha

{kind=link}

{kind=link}

{kind=link}

Conclusion

I am still long NYCB and believe shares are going higher regardless of the current appreciation. NYCB trades at a -24.88% discount to its book value, and at a discount to its equity while still producing a dividend yield that exceeds 6%. NYCB has made some strong moves, and the overall business looks very strong going forward. My prediction is that shares of NYCB will close the gap between its share price and book value throughout 2023, and we could see another 20-40% appreciation. I don't have a crystal ball, and this may not occur, but NYCB looks to have come out unscathed during the recent financial crisis and is positioned to do well in 2023. Regardless I will sit back, collect the dividends and reinvest them while waiting to capture additional appreciation.

For further details see:

New York Community Bank Delivered Solid Earnings And Came Out Of The Financial Debacle Stronger