VNO - New York State Of Mind: Who Wants A Bite Of The Big Apple?

2023-03-24 07:00:00 ET

Summary

- I'm always fascinated with NYC, and I even dreamed about working on Wall Street and perhaps that’s why I’m now a Wall Street writer.

- What’s not to love about this iconic city?

- Well, let me tell you about three office REITs that aren't getting any love.

I recently spent a few days in New York City meeting with my ETF Index partner and touring the New York Stock Exchange with my son. As I mentioned in my weekend blog, " I ran into Peter Tuchman, aka, the Einstein on Wall Street ."

Source: Twitter

As a kid, I was always fascinated with New York City and I even dreamed about working on Wall Street, and perhaps that's why I'm now a Wall Street writer.

What's not to love about this iconic city?

But wait, it seems a lot different now after Covid-19, especially in the office sector.

The pandemic accelerated the migration of people out of high-density, high-cost cities to mid-sized markets offering more space, lower taxes and a lower cost of living.

At the same time, advances in remote-work technology have improved employees' flexibility and job mobility, and this appears to be a trend that will continue to drive office-using job growth in lower-cost, lower-density cities such as those in the Sunbelt.

Also, de-densification is taking place within offices as employers reverse the long-term trend of maximizing the number of employees per square foot. This, too, has become an important factor in understanding long-term growth prospects for landlords.

That said, employees may not end up with more desk space as many landlords are seeking more common space such as conference rooms and open meeting areas, and this trend could help offset the demand destruction from WFH and lower utilization.

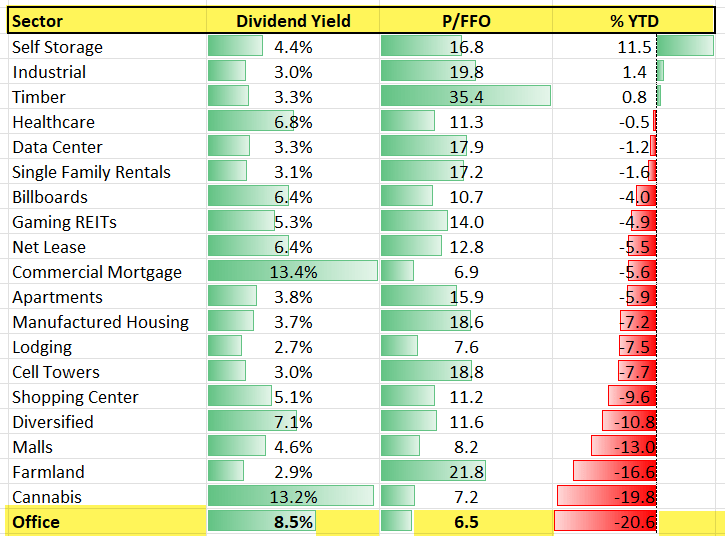

As seen below, the office REIT sector is the worst-performing sector year-to-date:

{kind=link}

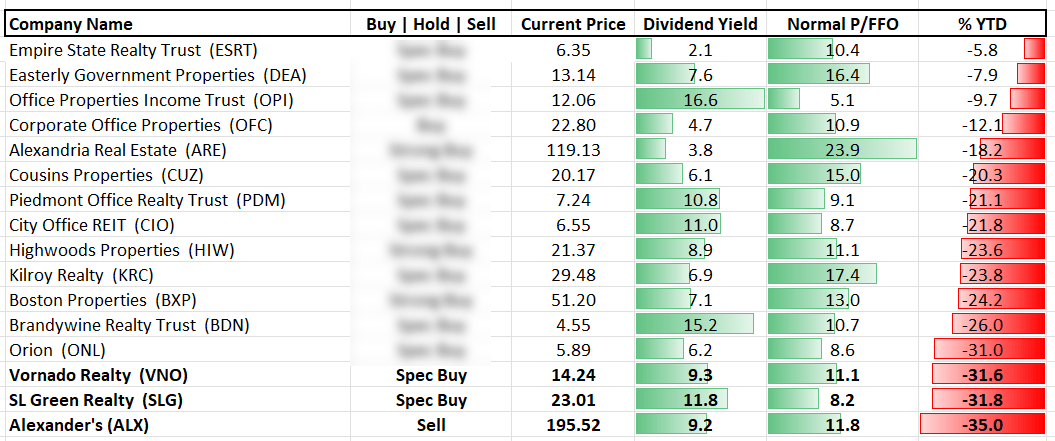

Today I wanted to focus on REITs that have New York City office exposure - Vornado Realty ( VNO ), SL Green ( SLG ), and Alexander's ( ALX ). In a few days I will write on the Sunbelt-focused office REITs, followed by the specialty office REITs.

{kind=link}

Vornado Realty Trust: 10.4% Dividend Yield

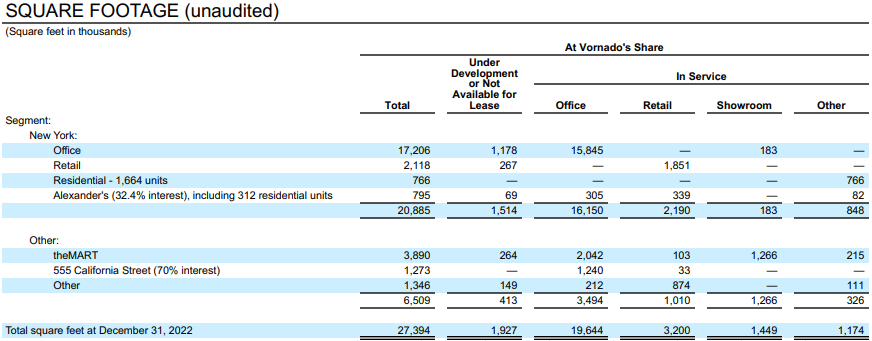

Vornado Realty Trust is a real estate investment trust ("REIT") that specializes in office properties but has additional property types including retail and residential. Their portfolio is concentrated in New York City with 20,885,000 square feet located in New York. In addition to New York, VNO has other properties located in Chicago and San Francisco.

VNO has two categories in which it details its property types, New York and Other. The New York category is broken down by office, retail, residential, and Alexander's (32.4% interest).

While the majority of their properties are in New York, they have additional properties under their Other segment that include "theMart" which has properties in Chicago that include design rooms, office, retail, and restaurants. Also included in the other category is "555 California Street" which is a 52-story office building in San Francisco that's currently leased to Bank of America.

{kind=link}

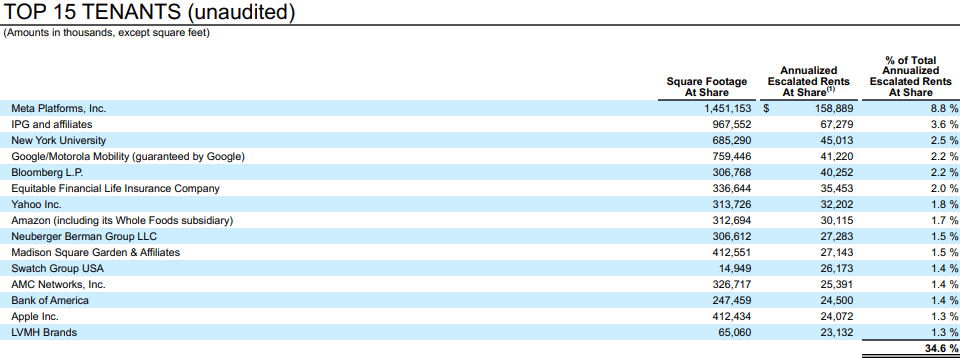

VNO has good tenant diversity with their top 15 tenants making up 34.6% of total annualized escalated rents. They're somewhat concentrated in their top tenant, Meta Platforms, with 8.8% of total annualized escalated rents contributed by Meta.

{kind=link}

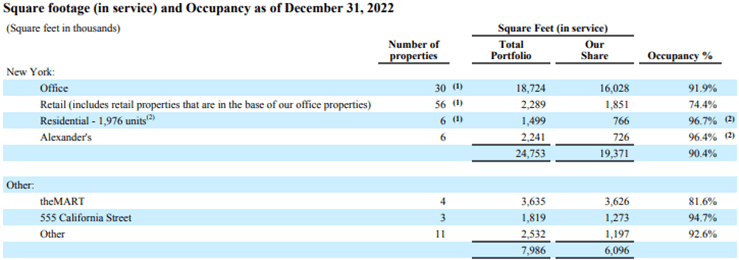

VNO's occupancy rates as of Dec. 31, 2022, stood at 90.4% for their New York properties, 81.6% for "theMart" properties, and 94.7% for their "555 California Street" property.

{kind=link}

A further breakdown on occupancy is listed below. Within the New York segment, office had an occupancy rate of 91.9%, retail occupancy was 74.74%, residential occupancy was 96.7% and their share of Alexander's had an occupancy rate of 96.4%. Within the Other segment, theMart had an occupancy rate of 81.6%, and 555 California Street had an occupancy rate of 94.7%.

{kind=link}

In their latest earnings release, VNO detailed leasing activity For the Year Ended Dec. 31, 2022. They leased 894,000 square feet of New York Office space with a weighted average lease term of 8.9 years.

111,000 square feet of New York Retail space with a weighted average lease term of 11.6 years. 299,000 square feet at theMART with a weighted average lease term of 7.2 years, and 210,000 square feet at 555 California Street with a weighted average lease term of 5.9 years.

9.4% of VNO leases expire in 2023 and 7.0% expire in 2024. Lease expirations are under 10% up until 2032. Almost 30% of their leases don't expire until after 2032.

VNO - Supplemental

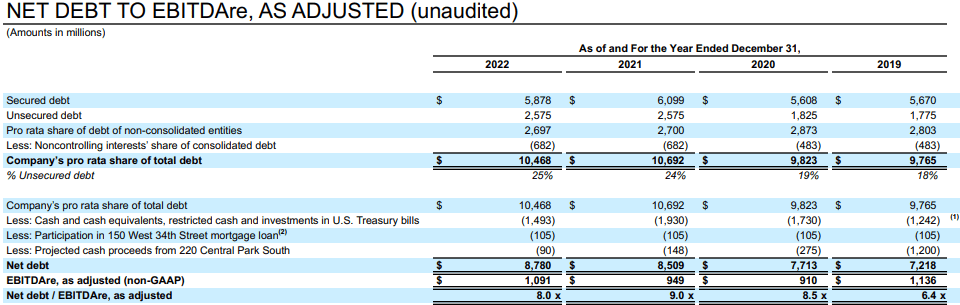

VNO has a net debt to adjusted EBITDAre of 8.0x, which is a bit higher than I'd like to see, and their interest coverage ratio is a bit lower than I'd like to see at 2.29x. Their total debt to total assets comes in at 48% and their long-term debt to capital is 58.54%.

There total debt is approximately $10.5 billion, with 72.5% at a fixed rate and 27.5% at a variable rate. Combined, their total weighted average interest rate is 4.23%.

They are investment-grade rated with a credit rating of BBB- by S&P and have $3.4 billion of liquidity which consist of $1.0 billion in cash and cash equivalents, $472 million invested in treasury bills and $1.9 billion available to them under their revolving credit facility.

VNO - Supplemental

{kind=link}

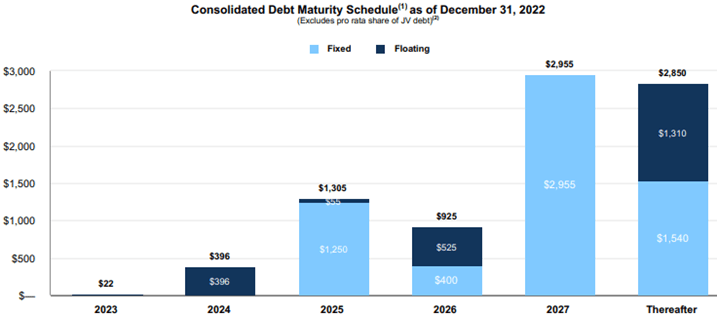

VNO does not have any major maturity due until 2025 with $1.3 billion due that year. Most of their maturities don't come due until 2027 or after and only $22 million is due in 2023.

{kind=link}

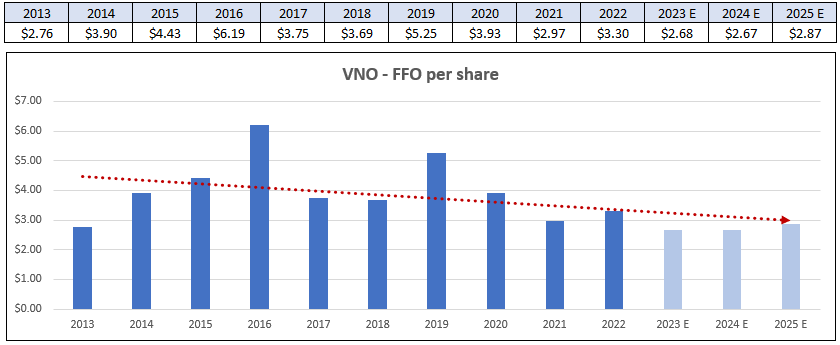

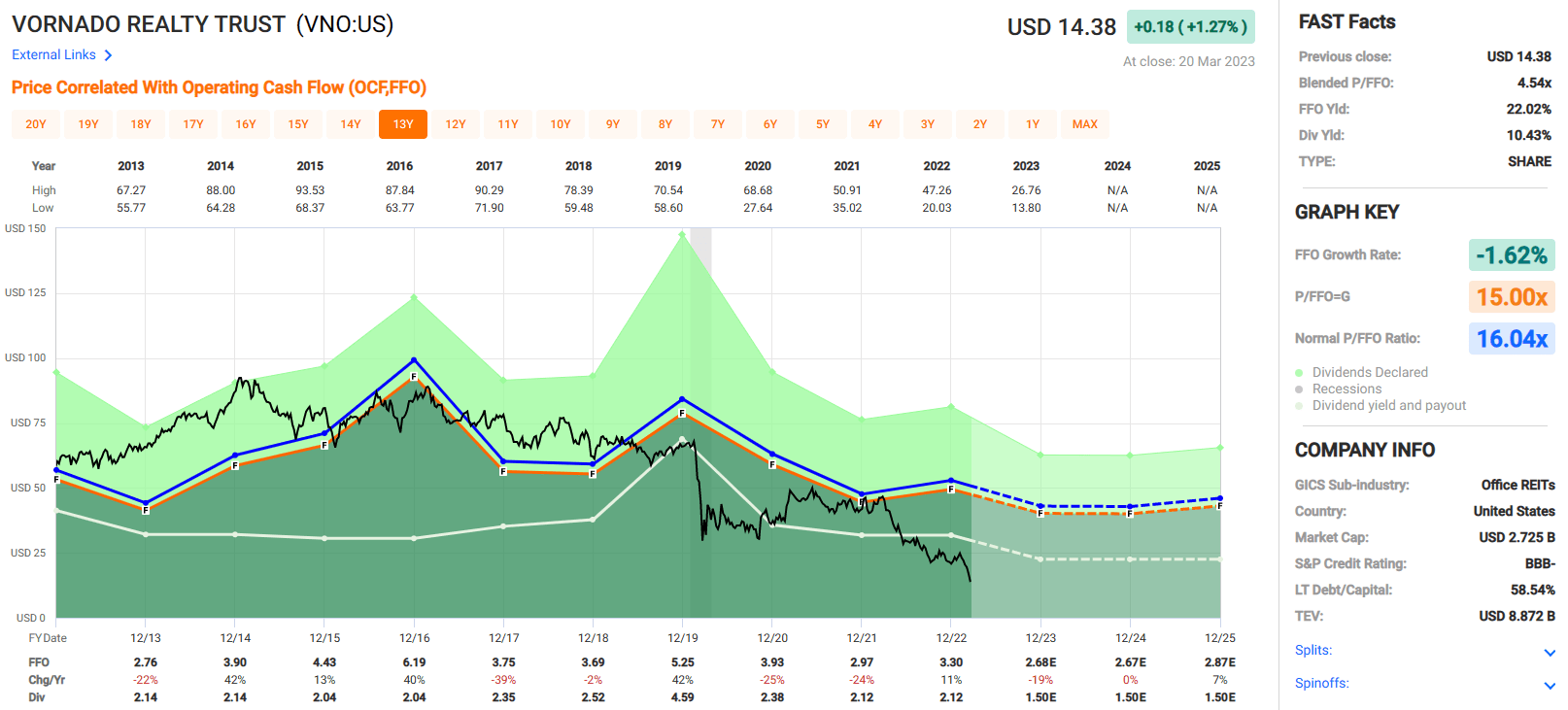

Since 2013, VNO has had a negative growth rate of -1.62% for its funds from operations ("FFO") per share. Earnings increased steadily from 2013 until 2016, but then dropped significantly in 2017 (-39% decline).

Earnings dropped again slightly in 2018 but then rebounded in 2019 with an increase of 42% in FFO per share. Their FFO dropped back down in 2020, as one might expect, and have not fully recovered since that time. Analysts expect FFO to drop by -19% in 2023.

{kind=link}

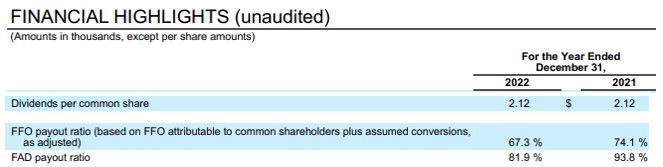

VNO pays a 10.43% dividend yield that's well covered by its FFO with an FFO payout ratio of 67.3% in 2022. When the payout ratio is based on funds available for distribution ("FAD") the payout ratio increases to 81.9%.

While the current dividend is covered, its historical growth rate leaves some to be desired. Over the last 10 years they have an average dividend growth rate of 1.86% or a compound growth rate of -2.58%.

{kind=link}

{kind=link}

VNO is trading at a major discount right now when compared to its normal multiple. Currently it trades for a P/FFO of 4.54x compared to its normal P/FFO of 16.04x. There's no doubt that the office sector as a whole has headwinds facing it, and some of the fundamentals could be better with VNO, in particular the debt levels, earnings consistency and growth, and dividend growth.

But with that said, at its current price it seems that these issues are priced in to a large extent and if the office sector reverts to its pre-pandemic levels, especially in New York, then there could be significant upside. We rate Vornado Realty Trust a Spec BUY.

{kind=link}

SL Green Realty: 13.5% Dividend Yield

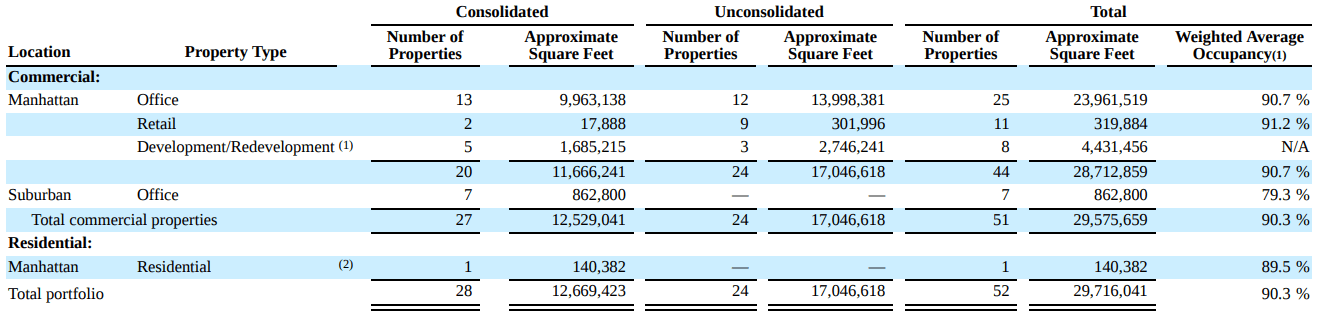

SL Green Realty Corp is a REIT in the office sector that's the largest office landlord in Manhattan. They're primarily focused on acquiring and maximizing value of commercial properties in the New York area. At the end of 2022, SLG held interests in 52 properties covering 29.7 million square feet. It breaks its properties down by property type and location.

In Manhattan they have both commercial and residential real estate. Their commercial real estate includes office and retail and as previously mentioned they hold residential real estate in Manhattan as well. Additionally, they hold office properties in suburban locations, which is defined as properties outside of Manhattan.

{kind=link}

As seen above, the majority of properties SLG has an interest in are office properties located in Manhattan. Office properties in Manhattan make up 23,961,519 square feet out of the total portfolios square feet of 29,716,041, or roughly 80%. Their next largest category is suburban office with 862,800 square feet, followed by Manhattan retail and residential at 319,884 and 140,382 square feet, respectively.

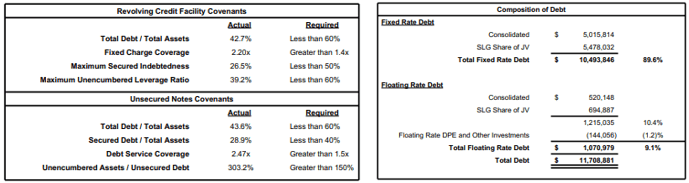

SLG has reasonable debt metrics with total debt to total assets of 42.7%, a fixed charge coverage ratio of 2.20x, and a long-term debt to capital of 55.37%. They're junk rated with a credit rating of BB+ by S&P. For the fourth quarter of 2022, SLG had a weighted average interest rate of 4.16% and 89.6% of their debt is fixed rate. At the end of 2022 SLG had $1.2 billion in total liquidity.

{kind=link}

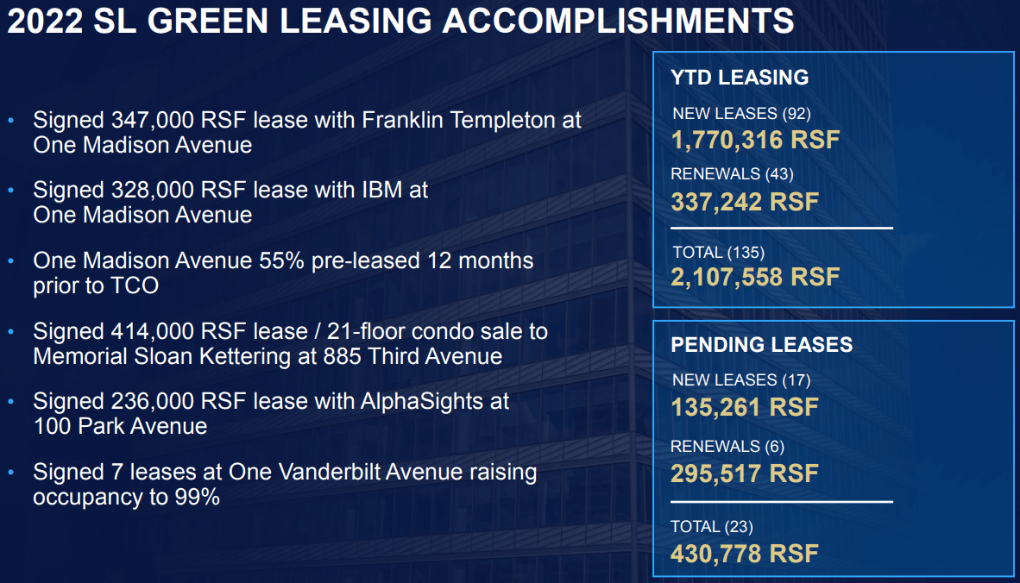

During 2022 SLG executed a 347,000 rentable square feet ("RSF") lease with Franklin Templeton, a 328,000 RSF lease with IBM, and a 414,000 RSF lease with AlphaSights. They signed 92 new leases for 1,770,316 RSF and 43 renewals covering 337,242 RSF. In total they had new or renewed leases covering 2,107,558 RSF in 2022.

{kind=link}

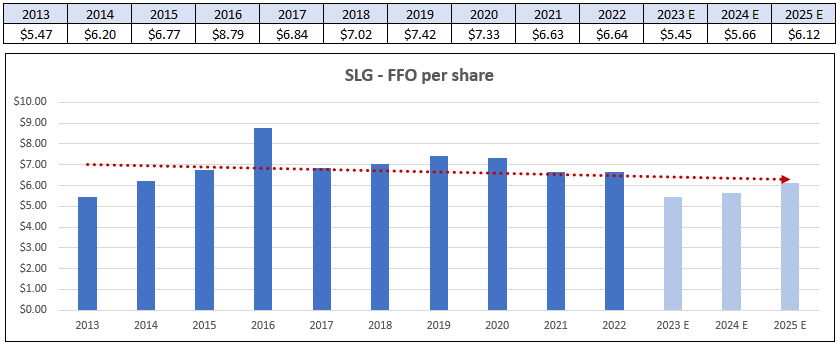

Since 2013, SLG has an average FFO growth rate of 0.68%. Much of this slow growth can be attributed to the pandemic and its current aftermath. When looking at SLG's FFO growth rates prior to the pandemic (2013-2019) the growth rate improves to 4.11%.

In 2020 their FFO per share fell by -1% and then fell by 10% in 2021. Analysts expect FFO to fall by 18% in 2023, but then to increase by 4% and 8% in the years 2024 and 2025, respectively.

{kind=link}

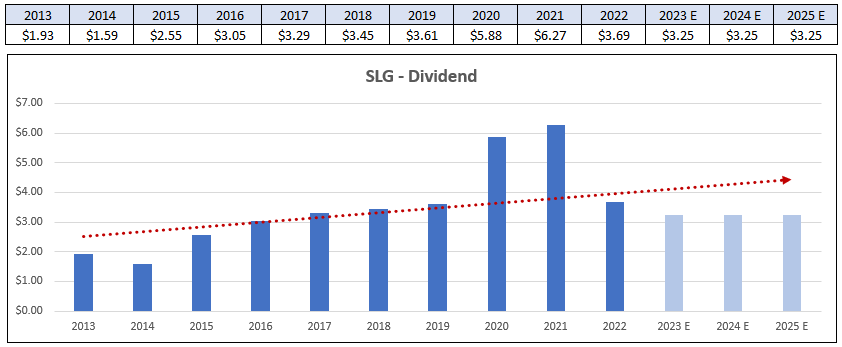

SLG pays a 13.50% dividend yield and makes monthly distributions. The dividend is well covered with an AFFO payout ratio of 81.23% in 2022. They have steadily increased their dividend since 2015, but analysts expect a dividend cut in 2023, likely due to their expectations on earnings.

What appears to be a drastic cut in 2022 is not. In 2020 and 2021, SLG paid a special dividend due to extraordinary gains received from the disposal of assets, so what looks like a large decline in 2022 is just the regular dividend without any special dividend paid.

{kind=link}

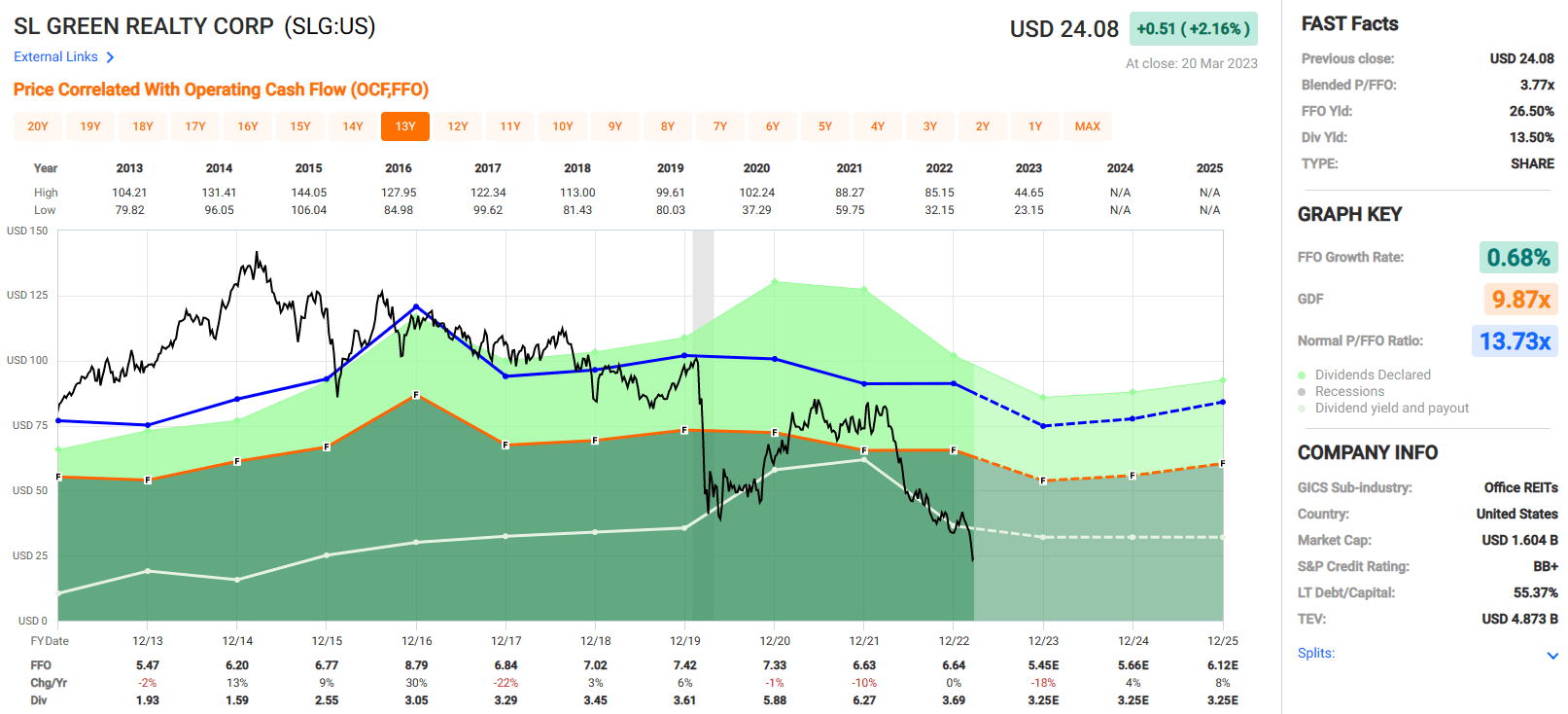

SL Green Realty is currently trading at a P/FFO multiple of 3.77x which gives it an FFO yield of 26.50%. It's trading at a significant discount to its normal P/FFO multiple of 13.73x and this discount has pushed the dividend yield up to 13.50%.

The low price multiple and high yield imply heightened risk, and there is given all the uncertainty in the office space with the stay at home movement, but we feel at this price, much of the risk has been accounted for and the selling has been overdone. Currently SL Green trades for less than it did at the depths of the pandemic and less than any time since 2009. We rate SLG a Spec BUY.

{kind=link}

Alexander's, Inc: 9.3% Dividend Yield

Alexander's is an externally managed REIT that is managed by Vornado Realty Trust which holds a 32.4% interest in ALX. Alexander's has six properties in the New York City metropolitan area which include:

- 731 Lexington Avenue: A multi-use property that covers 1,079,000 square feet. This property includes both office and retail space. Bloomberg L.P. occupies the office space while Home Depot is the primary retail tenant.

- Rego Park I: A shopping center located in Queens NY that covers 338,000 square feet and has anchor tenants Burlington, Bed Bath & Beyond, and Marshalls.

- Rego Park II: A 615,000 square foot shopping center in Queens NY. This center is anchored by Costco and Kohl's.

- The Alexander apartment tower: 312 apartment units totaling 255,000 square feet that is located above their Rego Park II shopping center.

- Flushing: A 167,000 square foot building located in Queens NY that is sub-leased to New World Mall.

- *Rego Park III: a land parcel to be developed covering 140,000 square feet and is adjacent to Rego Park II.

For the five developed properties, ALX has strong occupancy rates. 731 Lexington Avenue has an occupancy rate of 100% for its office properties and 90.3% for its retail properties, Rego Park I has an occupancy rate of 100%, Rego Park II has an 87.3% occupancy rate, The Alexander apartment tower has a 98.7% occupancy rate, and Flushing has a 100% occupancy rate.

*On March 8th ALX disclosed it had entered into an agreement to sell its undeveloped land parcel (Rego Park III) for $71.0 million. The transaction is expected to recognize a financial statement gain of $54.0 million and should close in the second quarter of 2023.

{kind=link}

ALX is diversified by property type, holding office, retail, and residential, but is very geographically concentrated with all of its properties located in New York. Additionally, they're very concentrated in the amount of real estate they own, having only five developed properties in their portfolio. Most concerning though is their tenant concentration, namely their top tenant Bloomberg.

In their most recent 10-K filing they disclosed that Bloomberg accounted for approximately 56% of their revenue in 2022. Bloomberg made up approximately the same percentage of their revenue in 2021 and 2020 as well. Bloomberg leases office space at their 731 Lexington Avenue property and are the sole occupant of the office portion of the property.

If Bloomberg were to reduce their demand for office space, or even worse, move to a different location altogether, it could have a significant impact on ALX. 731 Lexington Avenue is a trophy property so it's likely ALX would find another tenant, but this is still a risk an investor should be aware of. The Bloomberg lease is set to expire in 2029 with an optional term to 2039.

{kind=link}

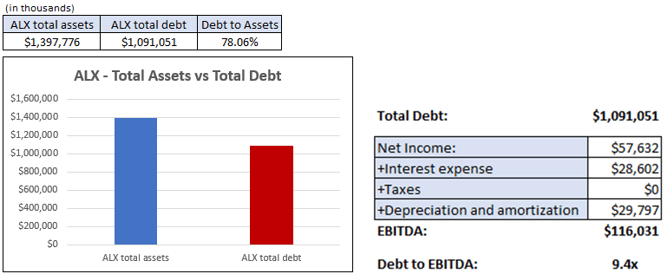

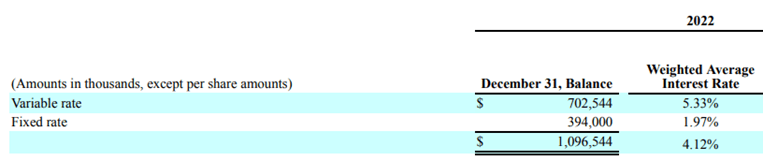

ALX has a large amount of debt. By my calculations they have a debt to EBITDA of 9.4x and debt to asset ratio of 78.06%. Additionally, they have 64.07% variable rate debt with a weighted average interest rate of 4.12% and a long-term debt to capital of 82.45%.

As of Dec. 31, 2022, ALX had $481.4 million in total liquidity consisting of $214.5 million in cash, cash equivalents, and restricted cash and $266.9 million of investments in US Treasury Bills.

{kind=link}

{kind=link}

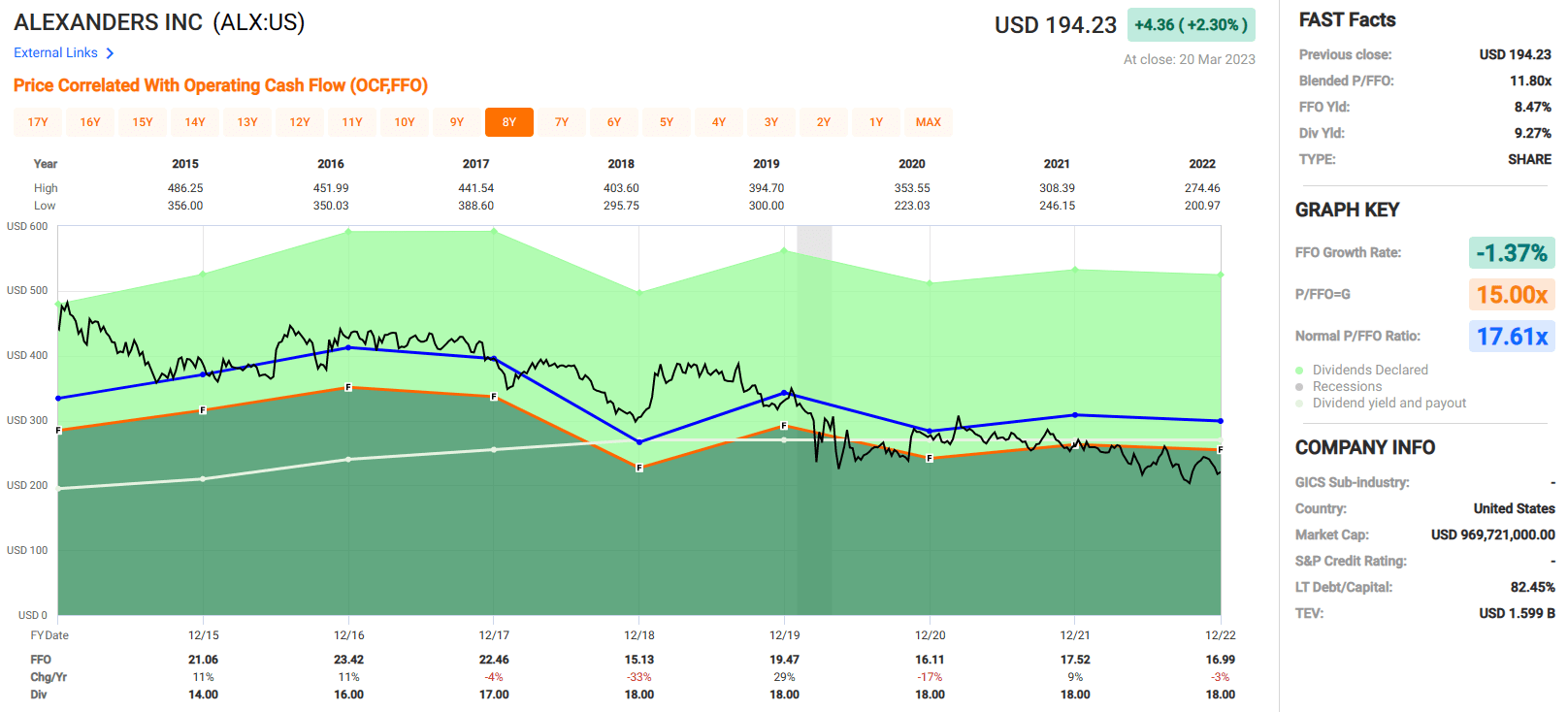

Since 2015 ALX has had a downward trajectory on its FFO per share. Their average FFO "growth" rate is negative -1.37% and their FFO per share in 2022 of $16.99 is well off their 2015 FFO levels. FFO per share increase from 2015 to 2017 but then fell sharply in 2018 and has not fully recovered since.

FAST Graphs (compiled by iREIT)

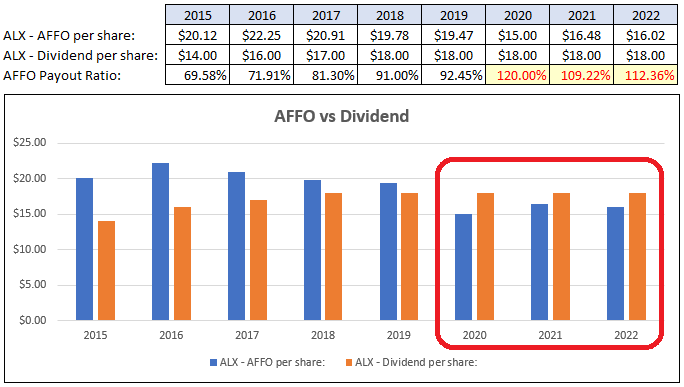

During this same time period Adjusted Funds from Operations ("AFFO") dropped from $20.12 in 2015 to $16.02 in 2022. What's more concerning is their AFFO has not covered the dividend over the past three years.

The payout ratio was getting into dangerous territory in 2018 and 2019 with payout ratios of 91.0% and 92.45% respectively, but in 2020 their payout ratio jumped to 120.0% and now sits at 112.36%.

{kind=link}

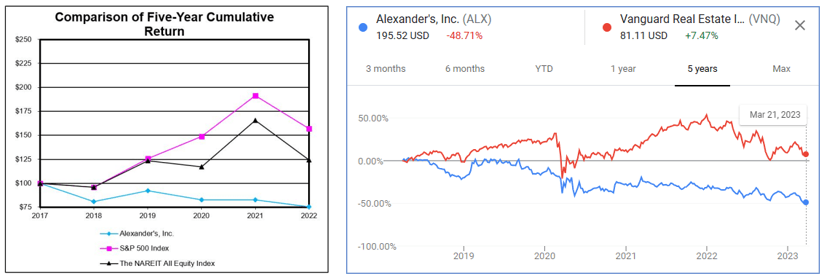

ALX stock performance hasn't done very well either. According to ALX's own graph it has significantly underperformed the S&P 500 index and the NAREIT All Equity Index since 2017.

Over the past five years ALX has lost 48.71% vs VNQ that has gained 7.47%. The cumulative return chart assumes all dividends were reinvested but the Google chart does not account for dividends. In either case, ALX has not performed well since 2017.

{kind=link}

Currently ALX is trading at a P/FFO of 11.80x which compares favorably to its normal P/FFO multiple of 17.61x. This is a speculative pick though. While the dividend yield is high at 9.27%, the payout ratio has exceeded 100% over the past three years and earnings have generally been declining since 2015.

If earnings recover to their past levels then this may be a good entry point, however if earnings continue to fall then a dividend cut could be on the horizon. We rate Alexander's a Sell.

{kind=link}

New York State of Mind

As I looked out the window of my friend's NYC apartment this week (see below), I began to ponder all the great bargains in the Big Apple, that includes a big bank known as First Republic ( FRC )…

Twitter: @rbradthomas

…or several really beaten-down office REITs (that I just wrote about).

I know there's a lot of politics I left out of this article intentionally (saved them for your comments below), and believe New York City will survive and thrive… because, as Billy Joel sang,

Some folks like to get away

Take a holiday from the neighborhood

Hop a flight to Miami Beach

Or to Hollywood

But I'm taking a Greyhound,

On the Hudson River Line

I'm in a New York state of mind.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

New York State Of Mind: Who Wants A Bite Of The Big Apple?