WLY - New York Times: A Robust And Anti-Fragile Digital Media Empire

2023-04-03 11:05:02 ET

Summary

- Despite significant disruption in the media industry, NYT has proven its adaptability and ability.

- With optionality, debt-free status, and subscriber growth, NYT is poised for continued growth and success in the future.

- The New York Times aims to reach 15 million subscribers by the end of 2027.

- Overall, based on my analysis, I am increasing my The New York Times position.

Editor's note: Seeking Alpha is proud to welcome Renato Neves as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

As a value investor, I am bullish on The New York Times ( NYT ) stock. In my opinion, the Times has shown its resilience as a digital media powerhouse, successfully transitioning into the digital age while maintaining its mission of seeking the truth and helping people understand the world around them. This, coupled with the company's optionality, debt-free status, and subscriber growth, leads me to believe that the company is poised for continued growth and success in the future.

Over the past decade, the media industry has experienced significant disruption, yet NYT has proven its adaptability and ability to thrive in this changing landscape. As such, I am optimistic about its prospects and I walk you through the evidence supporting my investment thesis.

NYT's Winning Business Model

Despite being 172 years old, the company has emerged as a leader in the media industry, with a strong subscription-based business model and significant investments in product and engineering.

Although there may be challenges ahead, I believe in the long-term potential of The New York Times. Despite initial concerns in 2014 and 2015 that it would be overtaken by newer media companies like BuzzFeed ( BZFD ), Vice, and Vox, the Times has undergone a transformation and is now comparable to subscription-based businesses like Netflix ( NFLX ) or Spotify ( SPOT ).

The NYT has successfully adapted to the digital age and evolved into a modern media empire. While it still offers daily home delivery of the newspaper for those who prefer physical paper, the company's business model has been a key factor in its success.

In 2022, the NYT added over a million digital subscribers, bringing the total number to 9.6 million. This impressive growth has been driven by a combination of organic expansion and strategic acquisitions. The acquisition of The Athletic has expanded the NYT's options within the industry to sports. While some may prefer organic growth like me, the NYT has shown that it can grow both organically and through acquisitions.

In addition to its core news offering, the NYT operates several other digital properties that require a subscription. NYT Cooking offers access to a vast library of recipes, while Audm lets users listen to articles from a variety of media organizations, including NYT. The Wirecutter, a website that publishes reviews of products, is another key component of the company's digital portfolio.

The NYT also generates revenue from seminars and conferences, where it partners with advertisers and sponsors. Importantly, the company has been able to increase its moat without raising any debt, a testament to the strength of its business model. For example, the acquisition of The Athletic was completed entirely with cash, totaling $550 million in February 2022.

New York Times Segments (New York Times)

Strong Financials

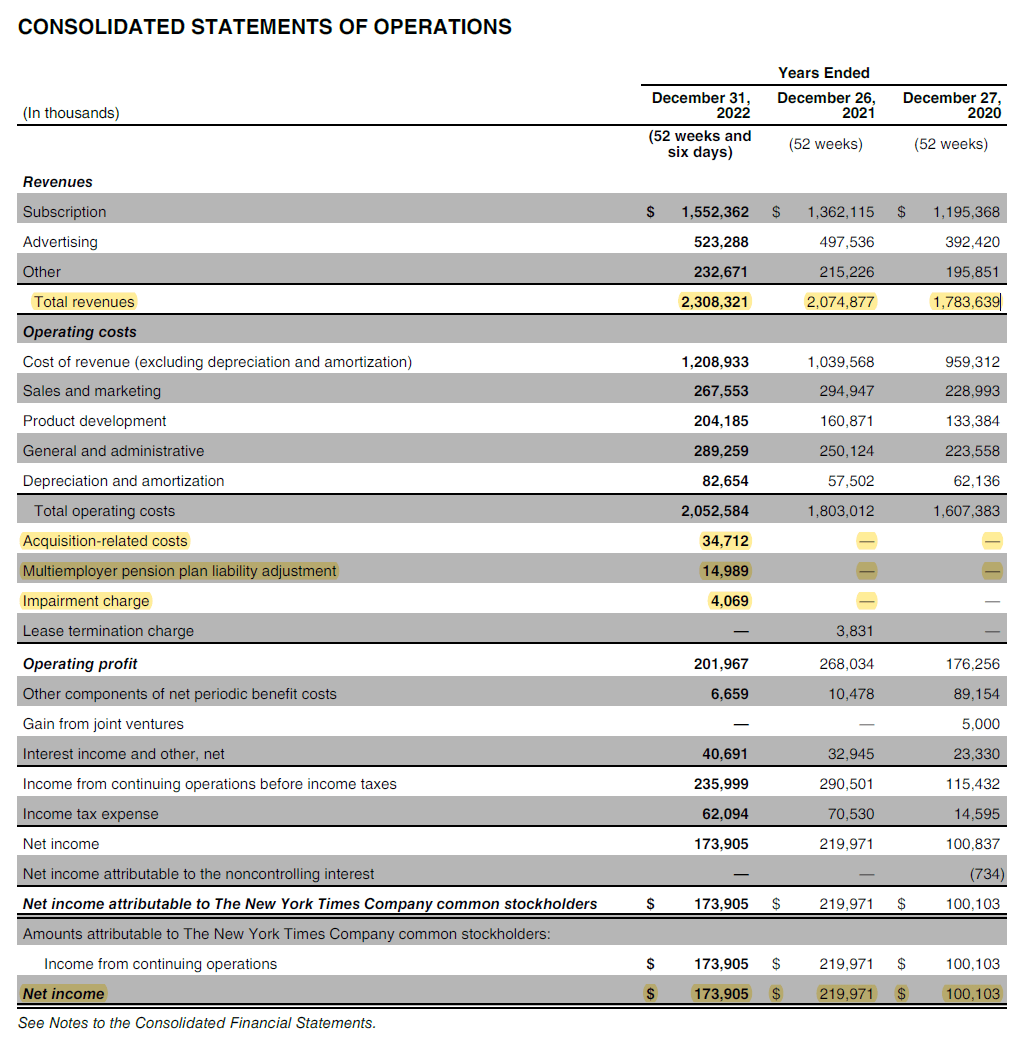

The NYT delivered strong financial results in the fourth quarter of 2022, beating Wall Street estimates and demonstrating the resilience of its business model. Adjusted earnings from continuing operations came in at 59 cents a share, surpassing the Wall Street estimate of 43 cents and representing a 37.2% increase from the prior-year figure. Total revenues of $667.5 million also exceeded expectations, coming in ahead of the Wall Street estimate of $647 million and improving by 12.3% year over year.

Statements of Operations (New York Times 10-K)

{kind=link}

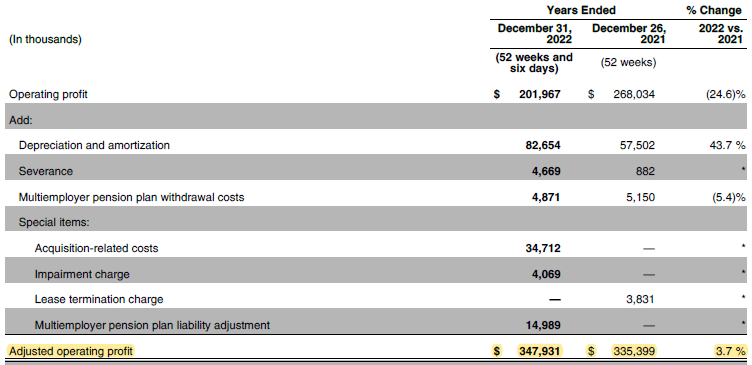

Subscription revenue was a major driver of NYT's revenue growth, increasing by 14% year over year to reach $1,552 million. Despite inflationary pressures in 2022, the company was able to maintain a healthy gross margin of 47%. However, the net income decreased by $0.46 million due to special items highlighted above, which is one of the reasons why the stock price has fallen. Nevertheless, when adjusting for operating profit, the NYT had an increase of 3.7% in its adjusted operating profit. As these items were a one-off, I do expect the net income to increase in the next year.

Adjusted Operating Profit (New York Times 10-K)

{kind=link}

The NYT's balance sheet remains in excellent shape, with no debt and cash and marketable securities of approximately $486.3 million. The company also repurchased $127 million worth of shares and paid out $42 million in dividends, reflecting its commitment to creating value for shareholders. In February 2023, the Board of Directors approved a $250 million share repurchase program in addition to the amount remaining under the 2022 authorization, as well as increasing the dividend to $0.11 per share, an increase of 22% per share from the previous quarter.

In addition, the NYT remains free cash flow positive year over year, highlighting its ability to generate cash from operations and invest in growth opportunities.

What I Like

There are several reasons why I like The New York Times. Consumers and companies have seen their disposable income shrink. Despite macroeconomic headwinds such as the Fed raising rates at an unprecedented pace, inflation, and layoffs, the company has been able to generate significant revenue from subscriptions, which now account for three times as much revenue as advertising.

In fact, while advertising revenue has decreased from $558 million in 2018 to $523 million in 2022, representing a decline from 30% to 20% of total revenue, subscription revenue has increased by 50% over the same period. This demonstrates that there is still a strong demand for high-quality journalism, even in a challenging economic environment.

Subscribers growth (New York Times 10-K)

One factor that contributes to customer retention and engagement is games like Wordle, which The New York Times has successfully leveraged to attract and retain tens of millions of players each week. This free and accessible game introduces users to other NYT products and games, helping to drive subscriptions and increase revenue.

Nonetheless, the company has proven its strong management in terms of implementing successful strategies to increase revenue and manage costs, as evidenced by the fact that it has not laid off employees despite challenges in the subscription and advertising business and has seen in other companies in the same sector.

Potential/Valuation

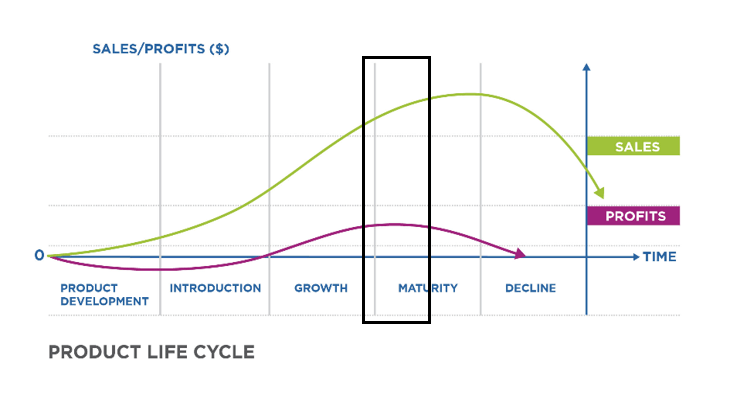

Before making any investment, I like to look at the valuation of a company that passes my quality checklist. I believe NYT is a quality business with long-term upside potential. The company is 172 years old and has only recently become a dominant player on the internet. Its balance sheet is sound, and both its top-line and bottom-line income statement figures have been increasing year-over-year. Therefore, I have included this stock in my quality checklist, and now it's time to find out which stage of growth the company is in.

Product Life Cycle (Lumen Introduction to Business)

{kind=link}

Overall, it seems that NYT is ending its growth stage for revenue growth, but in terms of free cash flow, it's actually in the maturity stage, which means that it is optimized for gross profit. This means that I have some metrics to look at and compare to its peers. The company does not provide guidance for earnings per share, but Wall Street expects $1.27 (higher than my expectation of $1.23), which equates to a forward earnings multiple of 29x. For context, the S&P 500 is currently trading at 17.36 . NYT is trading at high levels on an absolute basis, but low compared to where the company has been trading at.

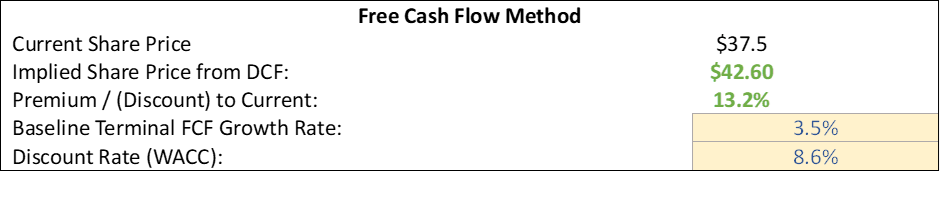

I also use a discounted cash flow model to value the stock, and with this, I put the weighted average cost of capital at about 8.6% (this assumption was based on a risk-free rate of 3.56% , a beta of 0.98 and a market risk premium of 4.78% ) and the terminal growth rate at about 3.5%, which gives me an implied share price of about $42.60. The implied growth rate here is about 13%. Is that reasonable for me? I am basically saying that NYT can grow at about 13% over the next decade, which is a high bar, but it's a bar that's certainly possible. Is that an expensive price tag? Sure, but is it one that NYT could meet? I believe so.

Is that reasonable for you? Do you agree with my assumptions? Let me know in the comments below.

Discounted Free Cash Flow Method (Author)

{kind=link}

Here's a table that shows a comparison of some key financial metrics for NYT and its peers:

| Company Name |

| EPS |

| P/E |

| Price to Operating Cash Flow |

| P/B |

| ROIC |

| New York Times |

| 1.05 |

| 35.8 |

| 41.77 |

| 3.875 |

| 11.27% |

| News Corp ( NWSA ) |

| 0.52 |

| 31.67 |

| 8.896 |

| 1.169 |

| 2.51% |

| John Wiley & Sons ( WLY ) |

| -0.17 |

| 25.71 |

| 8.786 |

| 1.982 |

| -0.40% |

| Gannett Co ( GCI ) |

| -0.63 |

| N/A |

| 6.043 |

| 0.89 |

| -4.77% |

| BuzzFeed Inc ( BZFD ) |

| -1.44 |

| N/A |

| 870.11 |

| 0.72 |

| -44.51% |

Although NYT's share price has dropped more than 20% from its 52-week high, it is not the cheapest stock among the five companies presented. However, quality comes at a price. Among these five companies, NYT has the highest price-to-earning (P/E) ratio of 36x, the highest price-to-book value (P/B) ratio of 3.9x, and the second-highest price-to-operating cash flow ratio of 42x, which may seem unattractive to value investors. But these high ratios reflect the company's quality. NYT's earnings per share are over a dollar, and its return on invested capital is 11.3%.

What should I watch moving forward?

Looking ahead, the company anticipates that its average revenue per user will continue to grow in 2023 as more subscribers transition to paying higher prices. However, it is important to note that the NYT's retention rate is only 67.34%, indicating the need for continued investment in customer retention efforts. If the company fails to transition these users from promotional subscriptions to higher subscriptions and increase the retention rate, it could be a cause for concern.

The company has set a goal to reach 15 million subscribers by the end of 2027, representing a compound annual growth rate of 10%. This milestone will be closely monitored, and any unexplained slowdown in annual growth could raise doubts about the company's future prospects.

While the gross margin has decreased slightly, it is hoped that this is due to the acquisition of The Athletics, which has yet to reach scale. However, it is also possible that the company is discounting its prices, and this possibility will need to be closely watched.

Lastly, labor tensions at The New York Times will also be monitored, as they have the potential to impact the stock performance in the near term.

My Final Thoughts

In my opinion, The New York Times is a solid business with a robust model that belongs in any well-diversified portfolio. Over the last 10 years, it has outperformed the market by 100%, and I foresee that the NYT could do it again.

I believe that the stock offers downside protection in bear markets due to its financial quality and provides upside potential in a bull market due to its ability to grow subscriptions even in a downturn. Although the shares of the company aren't cheap, I maintain my bullish view.

What should I watch moving forward? The company set a goal to reach 15 million subscribers by the end of 2027, which represents a compound annual growth rate of 10%. I will keep an eye on this milestone. The gross margin is down a little bit, and I'm hoping that has to do with the acquisition of The Athletics which hasn't reached scale yet, but it could be a sign that the company is discounting its prices. We'll have to watch that moving forward. The last thing I'm going to watch is labor tensions at The New York Times, which could affect the stock performance in the near term.

After evaluating the competitive landscape, it is evident that great businesses face significant competition. The media industry has undergone significant disruption, but The New York Times has adapted to the digital age and emerged as a leader. In today's market environment, I seek companies that are robust and anti-fragile, meaning companies in which we can have a lot of confidence to navigate difficult economic conditions. With its iconic global brand, huge addressable market, and strategic investments, The New York Times is poised for growth. The company has consistently exceeded expectations and surprised Wall Street each quarter in the past year. In my opinion, the moat is definitely widening, and the thesis is very much on track for owning this company.

For further details see:

New York Times: A Robust And Anti-Fragile Digital Media Empire