NCMGF - Newcrest: A Stronger H2 Ahead

2023-03-06 01:13:50 ET

Summary

- Newcrest has been one of the best-performing gold producers since last summer, up ~25% since June vs. a negative performance for the Gold Miners Index.

- I attribute the outperformance to lapping easier comps than some of its peers and its unique benefit of copper by-product credits that have helped to keep costs below $1,200/oz.

- Unfortunately, fiscal Q2 2023 was a softer quarter due to a tragic fatality (Brucejack) and drought conditions (Lihir), but the stock was buoyed by a failed takeover offer by Newmont.

- While I see Newcrest as one of the better majors, I see limited upside for the stock following its material outperformance, and I would only get interested in the stock below US$13.10 from an investment standpoint.

Just over six months ago, I wrote on Newcrest ( NCMGF ), noting that the stock was entering a low-risk buy zone near US$13.00 per share. This is because the stock was down substantially from its highs despite being more insulated than peers from inflationary pressures, benefiting from copper by-product credits at multiple operations (Cadia, Telfer, Red Chris) and the addition of a lower-cost mine in Brucejack (Pretium acquisition). Since then, the stock is up over 25%, has received a takeover offer from the world's largest gold producer (since rejected) and has outperformed the Gold Miners Index ( GDX ) by more than 2500 basis points in the period. Let's take a closer look at its fiscal H1 2023 results below:

{kind=link}

While North American gold producers recently released their Q4 2022 results, the Australian producers released their fiscal Q2 2023 results, which are the same as calendar year Q4 2022 results, to avoid confusion. All figures are in United States Dollars unless otherwise noted.

Q2 Production

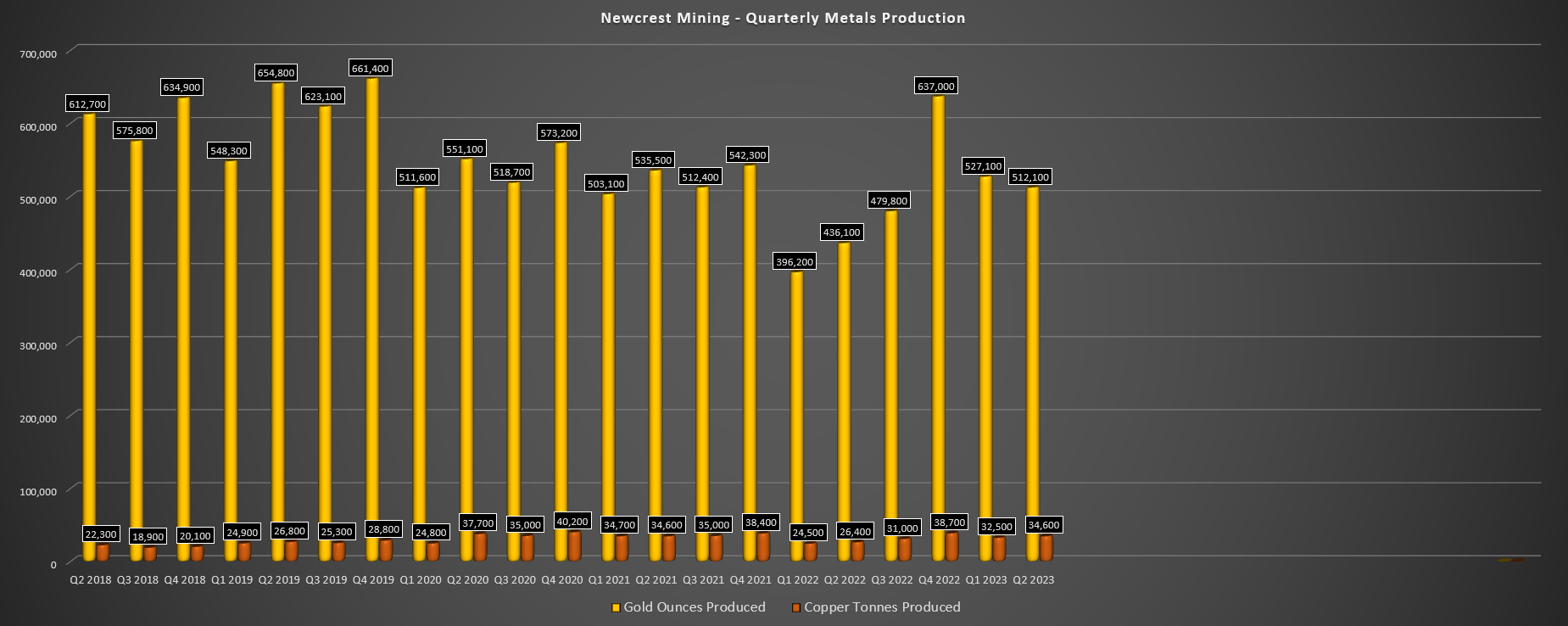

Newcrest released its fiscal Q2 2023 (calendar year Q4) results last month, reporting quarterly production of ~512,000 ounces of gold and ~34,600 tonnes of copper. This represented a 17% increase in gold production and a 31% increase in copper production vs. the year-ago period. Unfortunately, this was not due to broad-based strength with two assets heavily underperforming in fiscal Q2, but the company's flagship Cadia Mine pulled its weight and then some in the quarter, producing ~169,300 ounces of gold and ~27,100 tonnes of copper, representing one of the best quarters for the mine from an output standpoint since fiscal Q3 2021.

Newcrest - Quarterly Metals Production (Company Filings, Author's Chart)

{kind=link}

Starting with the largest of its top-3 operations, Cadia saw a 46% increase in gold production and a 49% increase in copper production vs. the year-ago period, with these increases largely due to being up against easy comparisons. The increased output was related to higher grades (0.84 grams per tonne of gold and 0.40% copper), and higher mill throughput with maintenance completed in the previous quarter and the commissioning of the two-stage plant expansion project. From a development standpoint, Newcrest has approved its PC1-2 Feasibility Study to the execution stage, with this being the next panel cave at Cadia after PC2-3, enabling the recovery of another 20% of Cadia's vast resources.

The recently released Feasibility Study highlighted average annual gold and copper production of 231,000 ounces and 42 million tonnes, respectively at negative all-in sustaining costs, with an After-Tax NPV (4.5%) of US$1.4 billion even using conservative metals prices.

{kind=link}

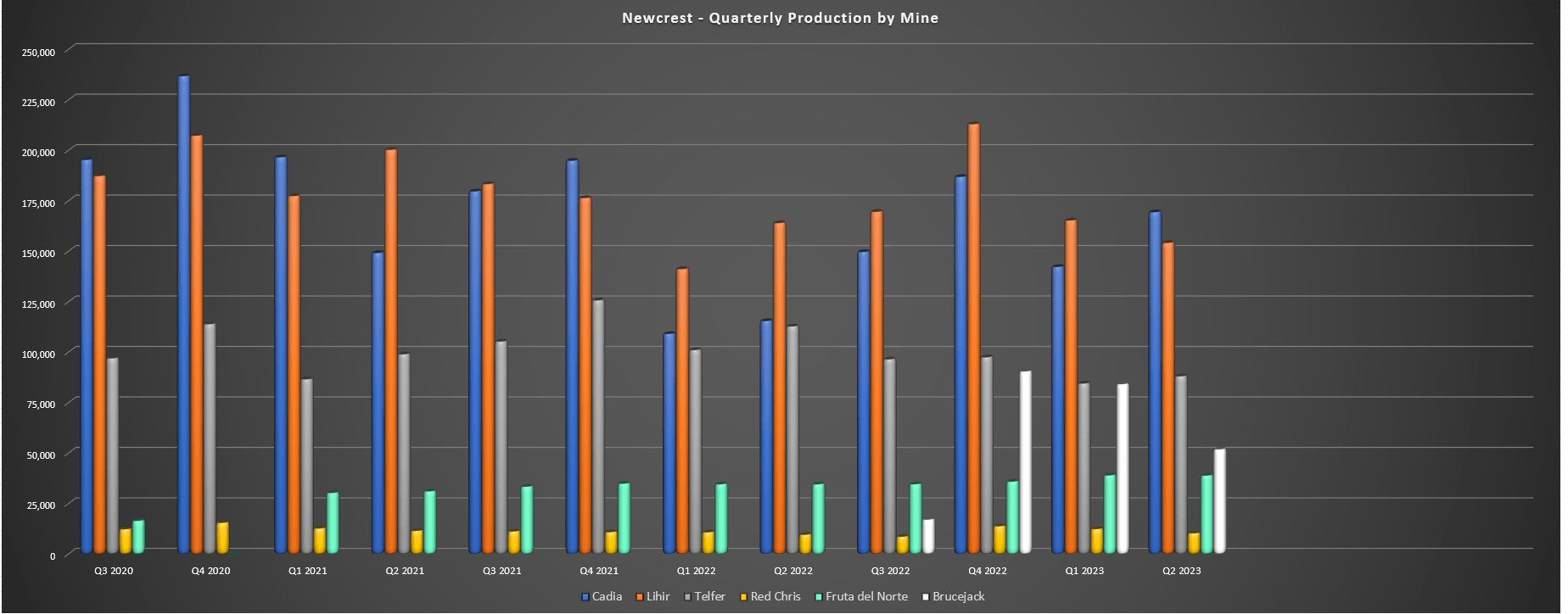

Moving over to its Lihir Mine in Papua New Guinea, fiscal Q2 production came in at ~154,100 ounces of gold, a 6% decline from the year-ago period. The decline in production was despite a slight improvement in head grades (2.20 grams per tonne of gold vs. 2.17 grams per tonne of gold) with this offset by lower throughput in the period due to drought conditions that limited the water supply to the plant. The result is that Lihir produced just ~319,400 ounces of gold year-to-date, tracking at just ~41% of the FY2023 guidance mid-point (780,000 ounces).

Fortunately, the company noted in its recent Conference Call that the situation is improving, with interim CEO Sherry Duhe stating the following:

I'm pleased to say that Craig [COO] and I went out to visit the site a few weeks ago and brought the rain with us."

- Newmont Interim CEO, Sherry Duhe

While this improved water situation for the second half won't allow the mine to close the gap between year-to-date production and the guidance mid-point unless we see two back-to-back 220,000-ounce quarters which I don't see happening (trailing-twelve-month average quarterly output ex-Q2 2023 = ~178,000 ounces), the company might be able to deliver into the low end of guidance at 720,000 ounces for the year. From a positive standpoint, the company is exploring an alternative seepage barrier (the Nearshore Soil Barrier) vs. the proposed Kapit Seepage Barrier, which would be simpler and more cost-effective, which I would see as quite positive in what's a capex heavy few years ahead.

Newcrest - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

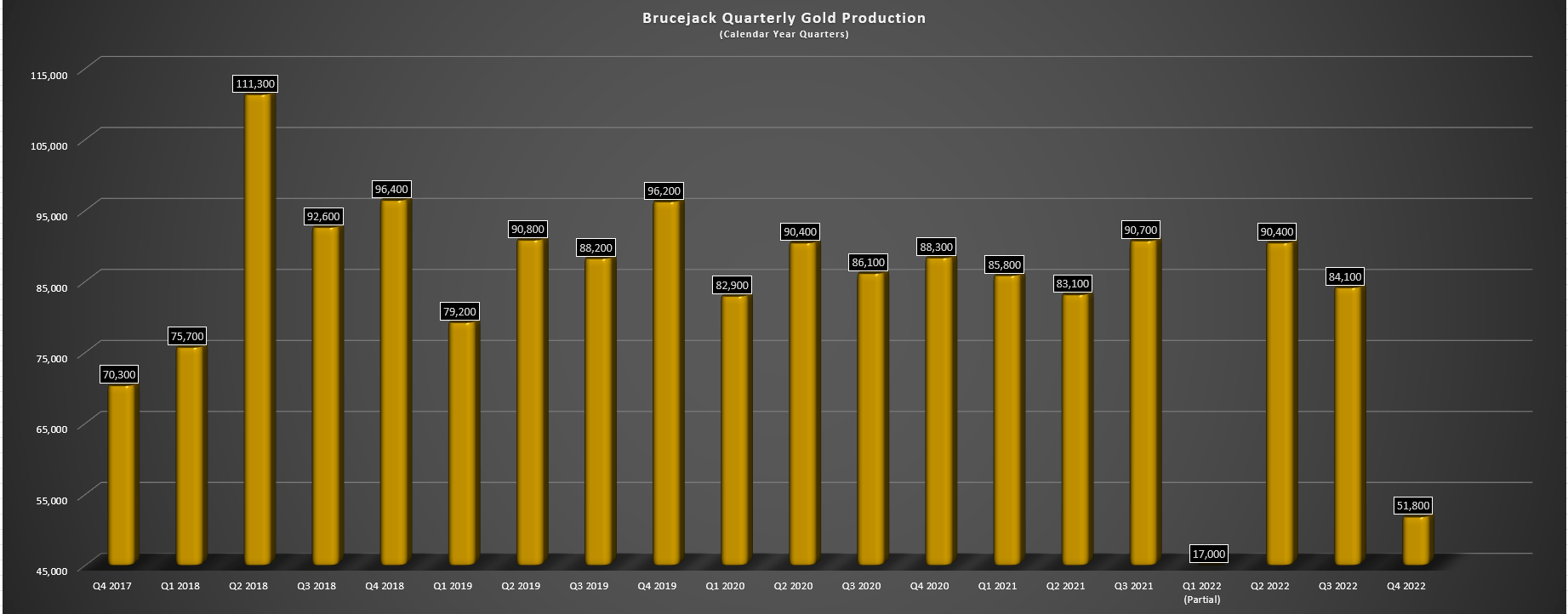

Finally, Brucejack had its weakest quarter in years, with a 21-day suspension of operations because of a tragic fatality among a contracting partner at the underground mine in late October, with this marking the third death at the mine since 2018. Given the much lower throughput rate (~244,000 tonnes vs. ~360,000 tonnes) and lower grades sequentially (6.72 grams per tonne of gold vs. 7.59 grams per tonne of gold), gold production fell 38% to ~51,800 ounces. Looking ahead to H2 2023, Newcrest expects a much stronger performance, but we should see the asset deliver into the lower end of FY2023 guidance (320,000 to 370,000 ounces), with year-to-date production of just ~136,000 ounces of gold.

Brucejack - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

Regarding optimization initiatives underway at the mine, Newcrest noted that its de-bottlenecking strategy continues to progress, with an aim to increase throughput to 4,500 to 5,000 tonnes per day, with plans to submit permit applications by Q2. Meanwhile, the ore sorting project has seen encouraging results according to Newcrest, though this is still quite early stage. Assuming the implementation of both initiatives, we would see a much leaner and meaner Brucejack operation, with the potential to produce 400,000 ounces per annum at a head grade of 7.5 grams per tonne of gold (~4,750 tonnes per day), and a potential to lower the cut-off grade depending on success of the ore sorting studies underway. Let's look at Newcrest's cost and margin performance:

Costs & Margins

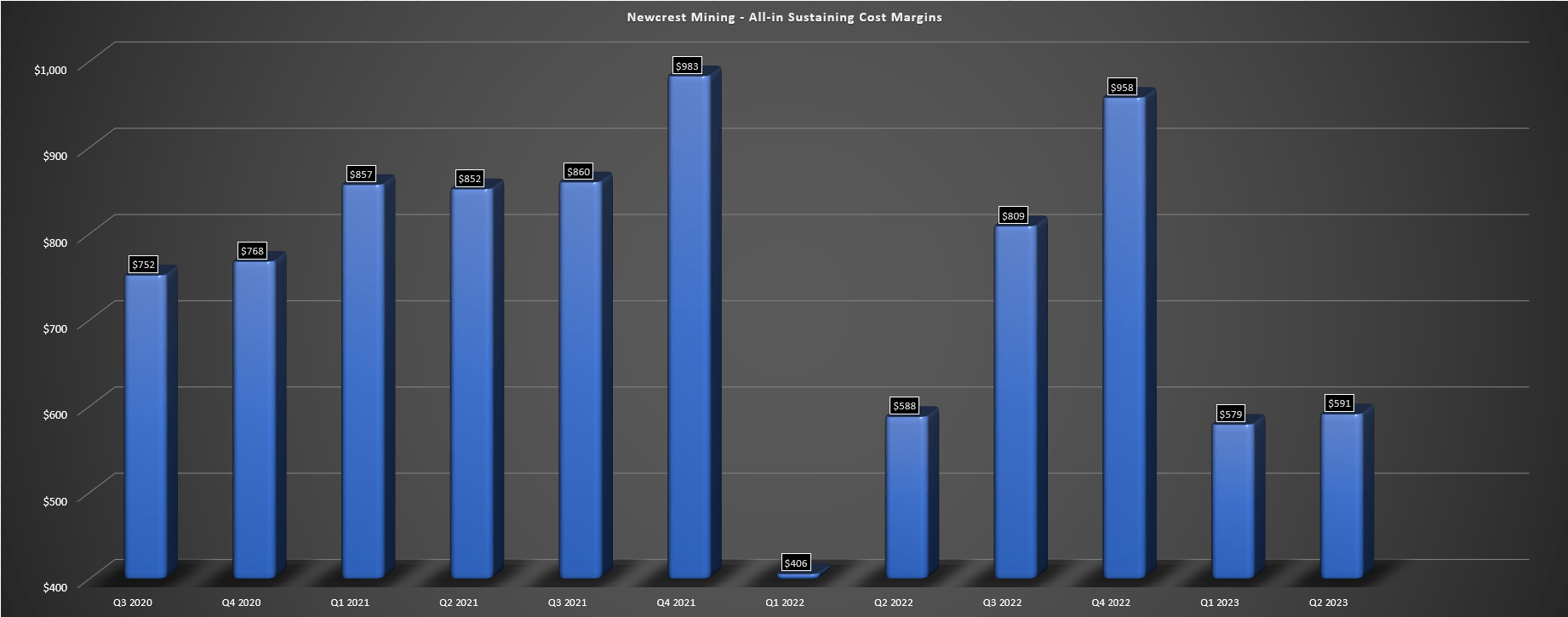

Digging into operating costs, Newcrest reported all-in-sustaining costs of $1,082/oz in fiscal Q2, a 4% decline year-over-year despite inflationary pressures and a weaker average realized copper price. Increased copper sales volume offset the weaker copper price ($3.66/lb vs. $4.37/lb), and Newcrest also benefited from weakness in the Australian and Canadian Dollar on a year-over-year basis, a tailwind for costs where it has most of its operations (all but Lihir). This cost performance was far better than the industry average (Q4 2022 AISC: ~$1,290/oz), and it's quite impressive that Newcrest posted lower unit costs despite a softer quarter at two assets combined with inflationary pressures and continued labor tightness. That said, Newcrest is unique vs. peers given its copper credits, and it certainly helps when you have a Tier-1 scale mine running at near-negative AISC (Cadia).

Newcrest - All-in Sustaining Cost Margins (Company Filings, Author's Chart)

{kind=link}

Looking at margins, the performance was solid, with Newcrest reporting a marginal increase in margins in the period vs. margin compression sector-wide ($591/oz vs. $588/oz). Not only did these margins represent some of the best figures sector-wide among gold producer peers even with Newcrest reporting one of the weakest average realized sales prices for gold sector-wide ($1,693/oz), and a $50/oz decline year-over-year. So, on a constant gold price basis ($1,743/oz like fiscal Q2 2022), AISC margins actually would have increased materially year-over-year. Year-to-date, Newcrest's AISC is sitting at $1,089/oz, and should come in below $1,050/oz on a full-year basis with the benefit of rising copper prices.

Finally, from an inflationary standpoint, Newcrest noted that while it continues to see labor constraints like many other producers operating in prolific regions (Ontario, Quebec, Western Australia, Nevada), it is seeing some relief among certain items like steel, and also reduced cost pressures among shipping. This is somewhat consistent with what we've heard from some other producers, with Equinox ( EQX ) noting that its view is that inflation has peaked, and Northern Star's ( NESRF ) CFO noting that while it's not seeing "significant reductions" , it is seeing some relief, and it called out diesel and steel. Hence, from an inflationary standpoint, the worst appears to be over even if costs will remain elevated this year and have remained sticky at significantly higher levels than 2020.

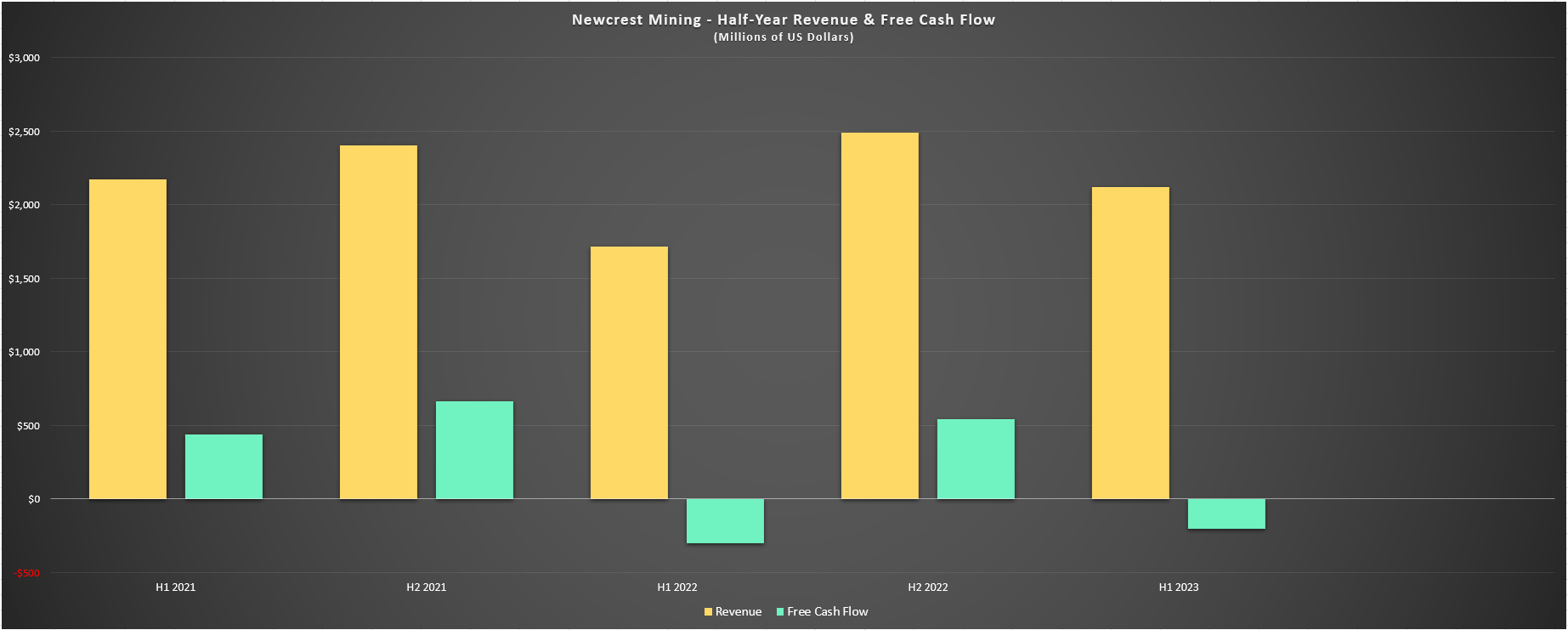

Newcrest - H1-23 Revenue & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Finally, looking at Newcrest's financial results, H1 2023 revenue came in at ~$2.12 billion, a 23% increase year-over-year helped by increased production from Cadia and a full quarter of contribution from Brucejack (excluding temporary shutdown). However, free cash flow remained negative in the period at $204 million and will remain pressured due to slightly higher spending relative to FY2022 levels. The good is that despite the significant investments at different projects and what's a capex-heavy period on deck, its balance sheet remains solid with just $1.7 billion in net debt despite the Pretium acquisition last year and a reasonable 0.80x net debt to EBITDA ratio, below its target of less than 2.0x.

Valuation

Based on ~895 million shares and a share price of $16.50, Newcrest trades at a market cap of ~$14.8 billion and an enterprise value of $16.5 billion. If we compare this figure with Newcrest's estimated net asset value of ~$11.9 billion, Newcrest trades at a premium to net asset value, which is certainly justified for a multi-million-ounce gold/copper producer with most of its operations in Tier-1 jurisdictions (Canada, Australia). Based on what I believe to be a conservative P/NAV multiple of 1.30x (given its strong track record of reserve replacement plus relatively low jurisdictional risk), I see a fair value for the stock of $16.2 billion or US$18.10 per share.

If we measure from a current share price of US$16.50, this translates to a 10% upside from current levels, suggesting that Newcrest is not that undervalued relative to its peer group following its outperformance. Of course, this outperformance can be attributed to Newmont's recent takeover offer and speculation that the company or another major might come in with a higher bid for the stock (vs. the initial offer that was immediately rejected). While it would not shock me to see Newmont try once more with a slightly sweetened offer (0.40 to 0.41 per share vs. 0.38 per share), I do not see a move by another major as being likely.

The rationale behind this view (no competing bid from another suitor) is that there are only three suitors capable of getting this deal done and Newcrest fits the best in Newmont's portfolio from a jurisdictional standpoint, with it already having a toe in British Columbia (Golden Triangle), and it also has a relatively large footprint in Australia (Boddington, Tanami), providing jurisdictional synergies. In Agnico's case ( AEM ), the company has just come off an M&A spree and has a very strong pipeline leveraging off existing infrastructure (Hope Bay, Detour Optimization/Underground, Malartic Excess Mill Capacity Utilization, San Nicolas JV), plus several smaller opportunities, suggesting no need to do M&A.

Finally, in Barrick's ( GOLD ) case, the company has extreme discipline for acquisitions, and if it passed on Kirkland Lake Gold despite the benefit of Canadian tax pools at ~1.1x P/NAV, I can't see it coming over the top of Newmont and offering ~1.30x P/NAV for Newcrest, especially when it has to use cheap currency (a much lower multiple than Newmont) to get the deal done. Instead, Barrick's capital is likely better directed towards buying back shares under US$16.00 vs. paying a higher multiple to scoop up a smaller producer, even if that producer has a very solid portfolio. Plus, while there is some shared commonality in Papua New Guinea, the better jurisdictional fit is Newmont or Agnico, not Barrick.

Besides, Barrick already ruled out a rival bid , so my opinion on the matter is irrelevant when they've confirmed they aren't interested.

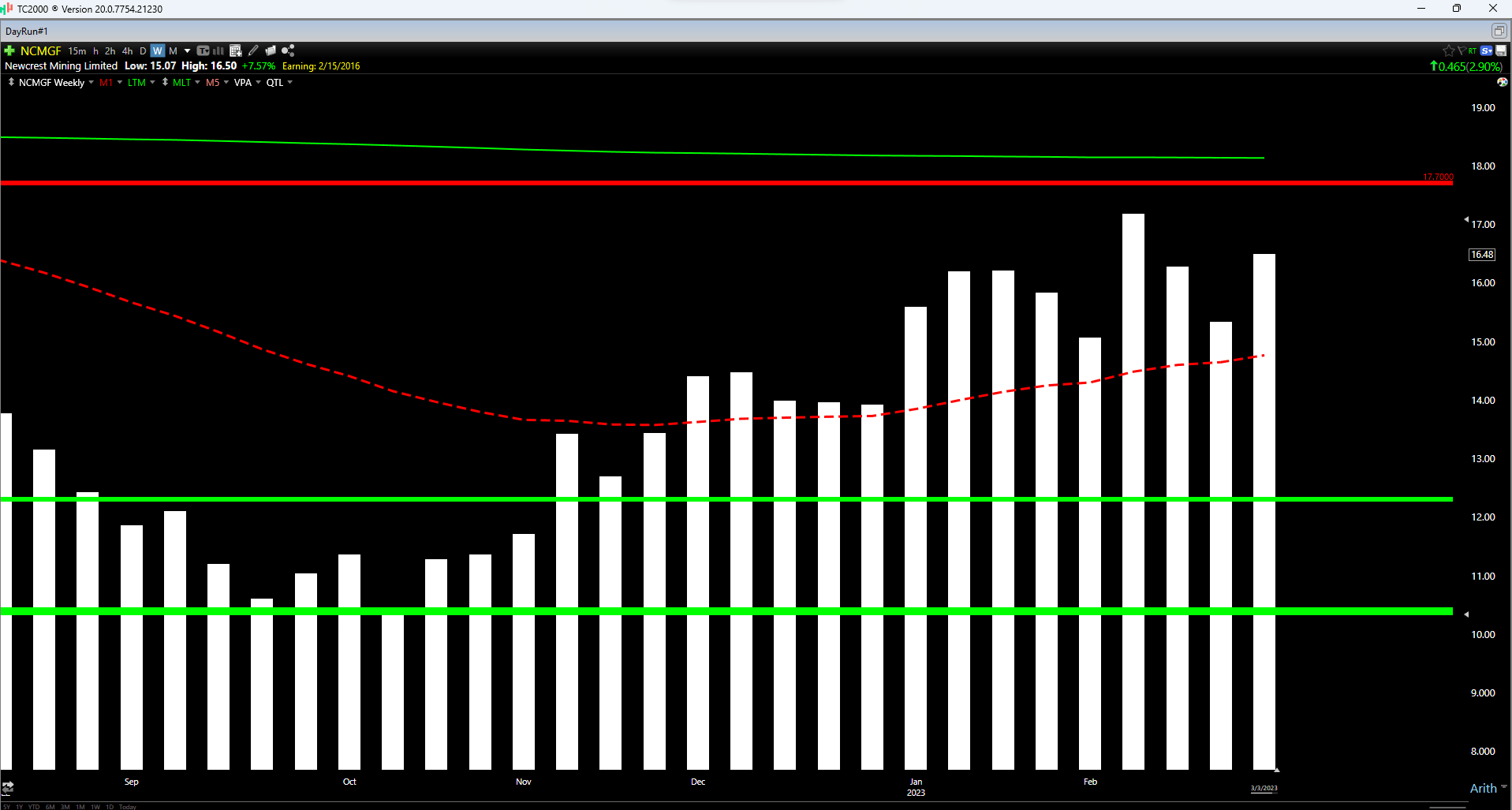

Finally, looking at the technical picture, Newcrest is trading in the upper portion of its support/resistance range after its recent rally, with upper support at US$12.30 and resistance at US$17.70. This translates to a reward/risk ratio of just 0.29 to 1.0, with $1.20 in potential upside to resistance and $4.20 in potential downside to support. The less favorable reward/risk ratio from current levels doesn't mean that the stock can't go higher, but I require a minimum 5.0 to 1.0 reward/risk ratio to justify entering new positions, so I see little value in entering the stock at current levels when it's already enjoyed a large move off its lows.

{kind=link}

So, from a valuation and technical standpoint, I see little upside for Newcrest here, hence my Neutral stance currently vs. a bullish stance last June when the stock traded at US$13.30.

Summary

Newcrest had a softer fiscal Q2 performance but due to a huge quarter from Cadia and exceptional performance from Fruta del Norte (32% equity interest) to help offset lower output elsewhere, the company remains on track to deliver on FY2023 guidance of 2.1 to 2.4 million ounces of gold at industry-leading margins. That said, the company is seeing weaker free cash flow generation due to significant capital spending which is expected to continue medium-term, and the goal is to buy cyclical stocks when they're hated and trading at deep discounts to fair value, not after ~60% rallies. So, while Newcrest is one of the better major producers, the stock would need to decline below US$13.10 to become interesting from an investment standpoint.

For further details see:

Newcrest: A Stronger H2 Ahead