NWL - Newell Brands' 2023 Restructuring Plan And Its Valuation

2023-04-29 06:18:11 ET

Summary

- In Q1 2023, the company's revenue decreased by 24%, and the management held a pessimistic view.

- The company unveiled "Project Phoenix" in January 2023, a reorganization plan intended to cut expenses and simplify the operating system.

- We analyze its valuation from the perspective of a turnaround and discover that its stock is still unattractive.

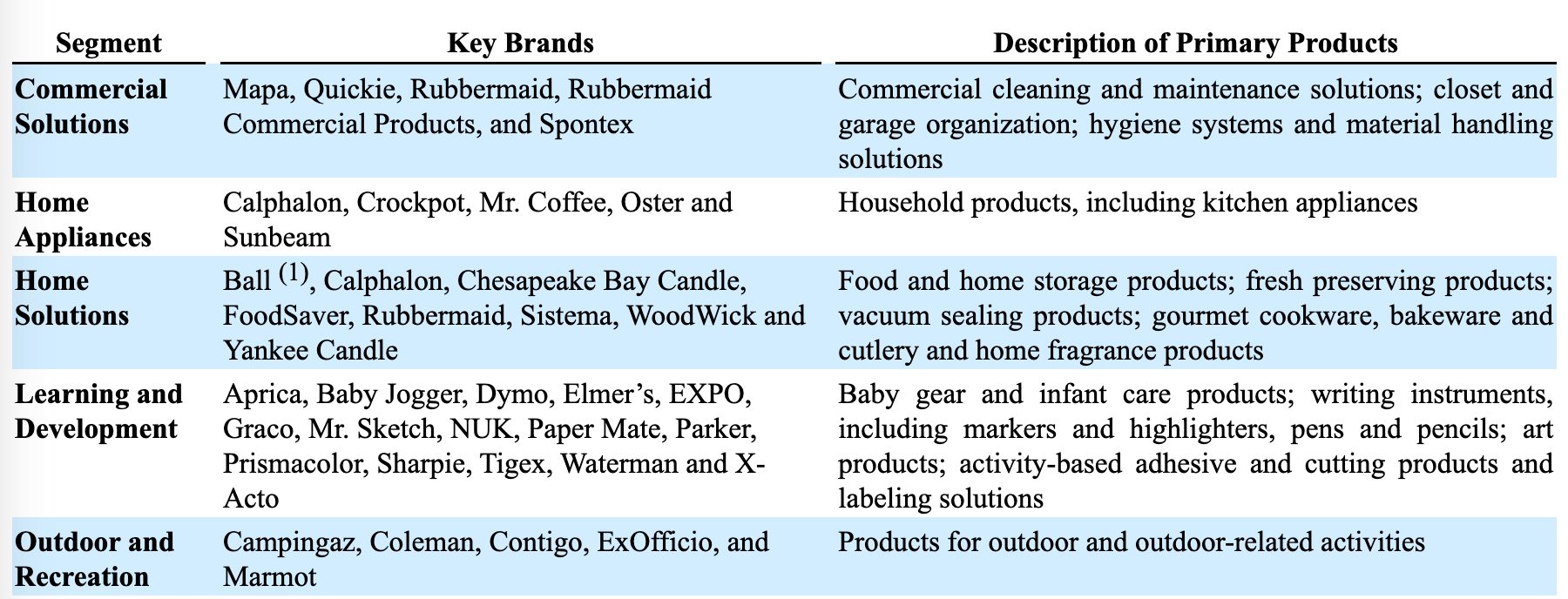

Company Profile

Newell Brands Inc. (NWL) is a company founded in 1903 with a diverse portfolio of products that includes many household brands and operates in various segments such as writing, home solutions, commercial products, baby and parenting, outdoor and recreation, and process solutions.

Business segments (Company's filing)

{kind=link}

Key Takeaways from Q1 2023 Earnings:

We will start with the highlights of its Q1 earnings. In Q1 2023 , the company decreased its revenues by 24%, further decelerating from Q4 2023. Gross margin contracted more severely, and SG&A expenses deleveraged more than in Q4. Inventory was down 7%. The management held a more pessimistic view, and clearly, the company underperformed more than the management expected .

"We are reaffirming our full year 2023 outlook, although we now expect to be towards the low end of the range since consumer discretionary spending in our categories remains under pressure making us incrementally more cautious on the overall operating environment. "

Project Phoenix

The company faced a headwind as a result of the inflationary environment. In January 2023, the company announced "Project Phoenix," a restructuring and savings initiative aimed at leveraging its scale to streamline its operating model, reduce complexity, and reduce overhead costs, with an expected completion date by the end of 2023.

Hence, we would like to focus on the stock's potential under its turnaround plan.

Valuation

The goodwill impairment recovery test

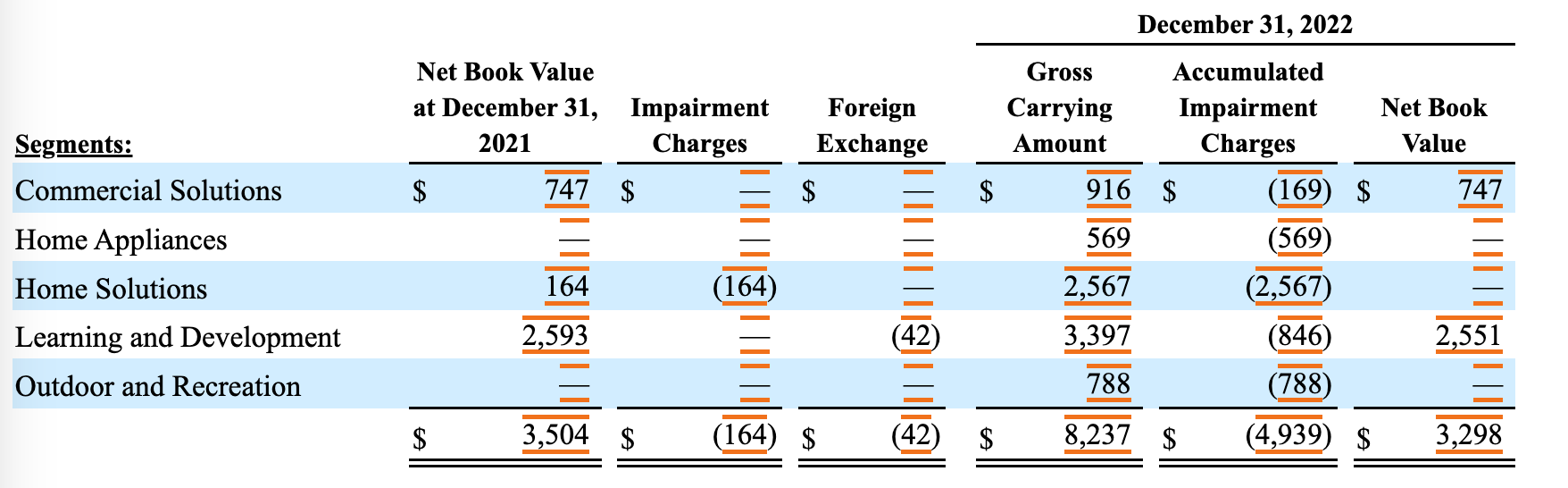

In its 10-K , three of its five operating segments wrote off all of its goodwill in 2022. Goodwill represents the difference between the purchase price of a company and the fair value of its assets and liabilities.

Goodwill impairment (Company's filing)

{kind=link}

To determine the fair value of goodwill, companies use a variety of valuation methods, including the income approach, the market approach, and the cost approach. These methods involve analyzing various factors, such as the company's earnings potential, industry trends, and market conditions.

The goodwill write-off test is typically conducted at least once a year or whenever events or changes in circumstances indicate that the goodwill asset may be impaired.

The decision to write down all goodwill implies that the affected segment is not expected to generate any future cash flows, and therefore its total value is equivalent to its book value.

Consequently, to evaluate the company's worth, it is necessary to focus on its Commercial Solutions and Learning and Development segments.

It is noteworthy that, starting in 2023, the company has combined its Commercial Solutions segment with its Home segment in its reporting. However, it is generally advisable to segregate the profitable segments from the unprofitable ones to enable investors to make informed evaluations.

The combined Home segment reported an operating loss in Q1. Therefore, it remains uncertain whether the Commercial Solutions segment will suffer a similar fate, or if the management can successfully turn around the Home segment.

The management explained below in the Q1 earnings call:

"First, we transitioned the company into the new operating model organized into three segments, Home and Commercial Solutions, Learning & Development, and Outdoor & Recreation. This should enable us to better leverage the scale of the organization, unlock new opportunities for growth while enhancing mobility for our talented employees."

"Thus, we are now expecting to take an incremental U.S. pricing action across roughly 30% of our U.S. business largely concentrated in the Home and Commercial Solutions segment in the third quarter."

"So we can't get into the specifics given the breadth of the pricing. But as Mark mentioned in the prepared remarks, it's largely focused in the home and commercial segment. And so it is where the majority of this analysis showed that we haven't fully priced for inflation. And in some cases, we -- because of that, we've got structural profitability challenge."

We began by analyzing the Learning and Development segment, and based on management's assumptions for 2023, we estimate that this segment will generate an operating income of $384 million and a net income of $111 million in 2023, assuming similar interest expense and tax rates as in 2022. Using a P/E ratio of 10x, the equity value of its Learning segment would be approximately $1.1 billion.

During the year 2022, the Home segment incurred a significant impairment of $3.3 billion. We conducted a scenario analysis to assess the impact on its valuation if its operating cash flow is recovered through its turnaround plan by 30%, 50%, or 100%. Our research showed that combined with the above-calculated valuation of the Learning segment, the company's equity worth might potentially range from $2.1 billion to $4.4 billion.

Income approach valuation

Furthermore, using the income approach to value the company, we assumed that the implementation of the company's turnaround plan would maintain half of the operating margins in its Home Appliances and Home Solutions segments in the 2021 level and increase the operating margin of its Commercial Solutions segment by 2%. This would result in the aggregate Home segment generating $528 million in operating income in 2023.

Assuming similar interest expense and tax rates as in 2022, we estimated that this would result in a net income of $508 million. Using a P/E ratio of 10x, the equity value would be approximately $5.08 billion, slightly higher than the current market cap of $4.9 billion.

Management projection

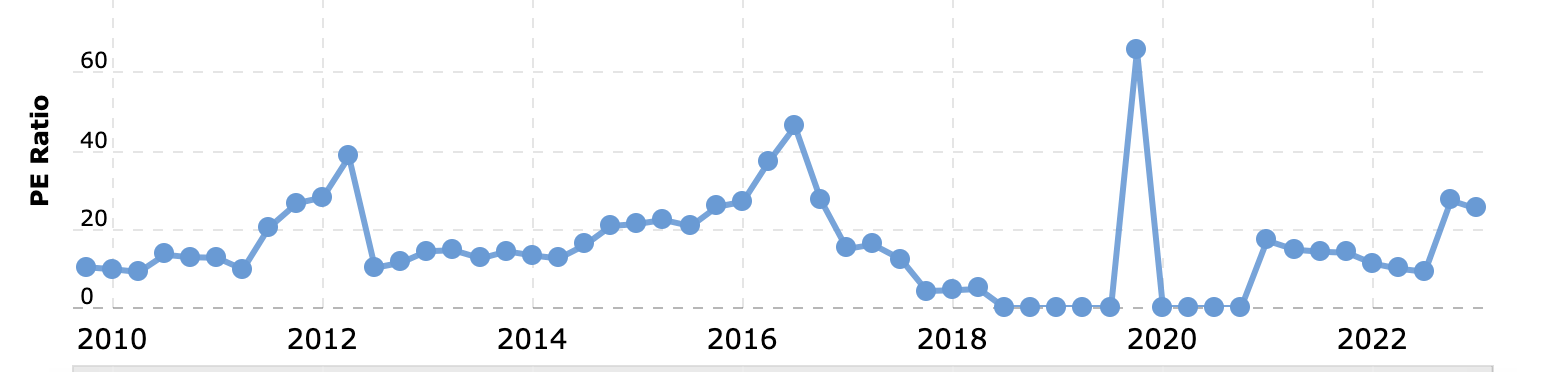

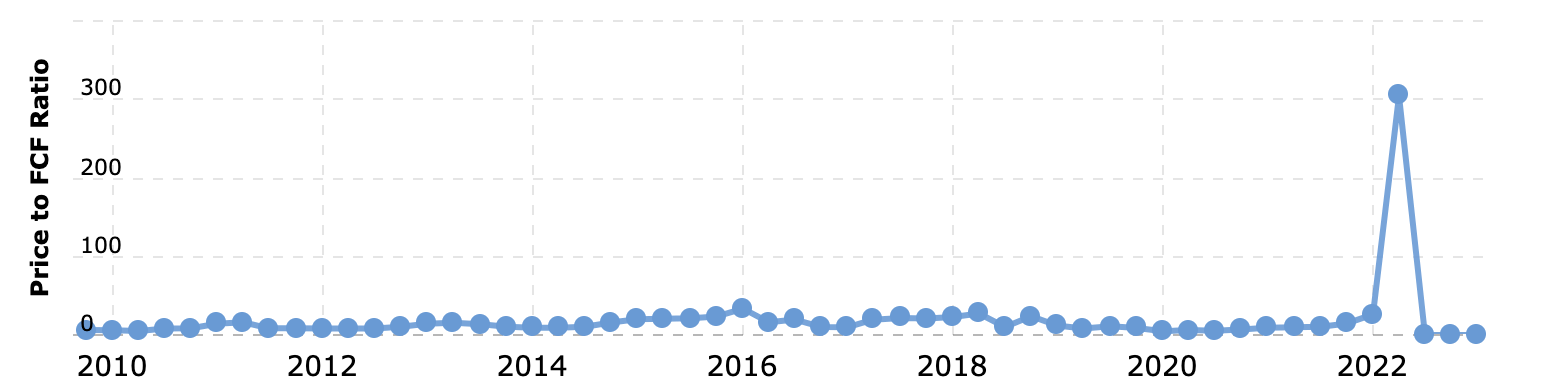

The company expected to generate operating cash flow in the range of $700-$900 million in 2023. If we assume flat CAPEX growth, it will generate $400-$600 million in free cash flow in 2023. Its FWD P/CF is 12.3x-8.2x. The management expected normalized EPS of $0.95-$1.08. Thus, its FWD P/E ratio is 12.8x-11.24x. Both metrics are traded at prices that fall within the median of their historical multiple ranges.

Historical P/E ratio (Macrotrend) Historical P/CF ratio (Macrotrend)

{kind=link}

{kind=link}

Potential catalyst

As part of its restructuring plan, the company intends to create a consolidated sales team to take advantage of its scale with retailers and centralize manufacturing within its supply chain. This approach is expected to result in cost savings and potential price increases, which could lead to improved profit margins. These initiatives may result in stock repricing and expansions of the valuation multiple if they are successfully carried out.

Second, we moved to a One Newell sales model for our top four customers to harness the scale of our portfolio while building win-win, enduring partnerships with our top customers. We are bringing a unified approach to selling our products to our major customers to simplify customer interactions, significantly improve their experience and strengthen our position as a best-in-class partner.

We maintain a cautious outlook on the company's restructuring plan due to retailers' recent aggressive efforts to promote their own private-label brands in order to save costs. Retail giants such as Target (TGT), Walmart (WMT), and Costco (COST) have been investing heavily in developing their own private-label brands as a strategy to combat inflation. Moreover, as the company's products range from home goods to learning materials and outdoor equipment, the potential for synergies from supply chain consolidation may be limited.

Conclusion

The scenarios presented above are based on the assumption of a successful turnaround in 2023. However, the valuation analysis concludes that the bull case valuation is still lower or slightly higher than the current level of $4.9 billion. Furthermore, the management's plan still faces uncertainties. Therefore, we do not consider the current price level to be attractive.

For further details see:

Newell Brands' 2023 Restructuring Plan And Its Valuation