NWL - Newell Brands: Mixed Outlook Keeps Me On The Sidelines

2023-08-29 12:01:16 ET

Summary

- Newell Brands' sales growth is expected to be under pressure due to tightening consumer discretionary spending and normalization of demand.

- The company's margins are expected to benefit from price increases, cost-saving initiatives, and easier comparisons.

- The stock's valuation is slightly above historical average, leading to a neutral rating.

Investment Thesis

Newell Brands Inc.’s ( NWL ) sales growth is expected to remain under pressure for the next few quarters. This is due to the continued tightening of consumer discretionary spending given the restarting of student loan repayments, inventory destocking, and the normalization of consumer demand from peak levels during the pandemic. These headwinds are expected to more than offset benefits from price increases and easy comparisons in the second half of 2023.

The margin outlook for the company is slightly better and the company’s margins are likely to benefit from price increases, moderating inflation, easier comparisons, and cost-saving and productivity-enhancement initiatives taken by the company. So, the company’s overall outlook is mixed with revenue seeing headwinds while margins recover. The valuation is also slightly above the historical average based on the FY23 consensus EPS estimate. Given the mixed outlook and not so cheap valuation, I prefer to be on the sidelines and have a neutral rating on the stock.

Revenue Analysis and Outlook

In my previous article , I discussed Newell’s near-term concerns regarding its topline growth due to lower consumer discretionary spending, demand normalization from peak levels during the pandemic, and retail inventory destocking. These concerns made me stay on the sidelines. The company has reported its earnings for the first and second quarters since then and similar dynamics were seen there as well.

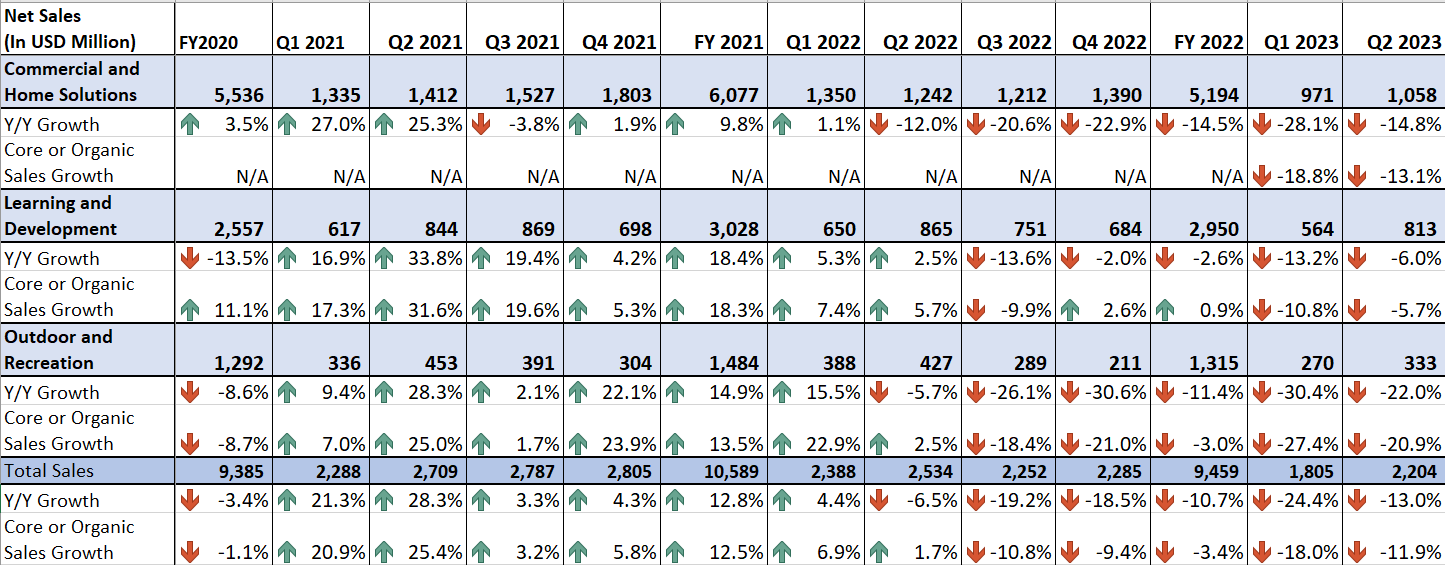

In the most recent quarter, the company's sales growth continued to face challenges due to consumer demand returning to more normalized levels in general merchandise categories from peak levels during the pandemic. Furthermore, continued retail inventory reduction in response to an economic downturn also had a negative impact on volume. Moreover, lower consumer spending on non-essential items, due to the inflationary environment, also contributed to these challenges. Lastly, the bankruptcy of a major retailer - Bed Bath & Beyond ( BBBYQ ) - in the quarter also impacted volume levels. This resulted in sales for the second quarter of 2023 declining by 13% YoY to $2.2 billion, which included a 70 bps headwind from foreign currency and a 40 bps headwind from the divestiture of the low-performing Connected Home and Security (CH&S) business. Excluding the impact of foreign currency and divestiture, core sales declined by 11.9% YoY.

{kind=link}

NWL’s Historical Net Sales ( Company Data, GS Analytics Research)

Looking forward, I believe that the company’s sales growth should face continued pressure from lower consumer discretionary spending, demand normalization, and inventory destocking for the next few quarters.

During the pandemic, Newell’s sales growth benefited from an increase in demand for discretionary products such as general merchandise (home and kitchen appliances, outdoor products) due to the government's stimulus checks. However, post-pandemic, as the effect of stimulus money faded away, demand for these products started normalizing. Moreover, these general merchandise items usually have longer purchase cycles, and given high volumes sold during the pandemic, consumers won't be required to purchase these products again in the quarters ahead. This is leading to continued normalization in demand for the company’s discretionary products.

In addition, as inflation increases, people generally find themselves in a situation of trade-off between purchasing discretionary or staples items, and due to the essential nature of staples, discretionary spending is generally put on hold or delayed. This tight discretionary spending in an inflationary environment further lowers demand for the company’s products. Moreover, the normalization of demand for general merchandising products and tight discretionary spending along with recessionary concerns also led to retail inventory destocking in the second half of 2022 which has continued Y-T-D as well.

Moving into the second half of 2023, management expects demand for general merchandising to continue normalizing due to their longer purchase cycle. Moreover, prices of staples are expected to remain high which should continue to put pressure on budget-conscious consumers. Moreover, the restarting of student loan payments in October is expected to have an additional effect on discretionary spending. As payments resume following a multi-year pause, many consumers will likely need to be more careful with their budgets, particularly due to the continued high core inflation. This has lowered the real consumer income and should further exert pressure on demand in the coming quarters. As a result, management is expecting inventory destocking to continue in the second half of 2023 as well, although the rate of retail inventory destocking should moderate as compared to the previous year's quarters.

These above-mentioned headwinds are expected to result in a volume decline for a few more quarters ahead and should more than offset benefits realized from price increases and easing YoY comparisons. So, the revenue outlook for the next few quarters remains under pressure.

Margin Analysis and Outlook

In the second quarter of 2023, NWL’s margins were impacted by volume deleveraging and inflationary headwinds. These headwinds more than offset the benefits of price increases and productivity savings. This resulted in a 320 bps Y/Y decline in normalized gross margin to 29.9%, whereas the normalized operating margin decreased 490 bps Y/Y to 9.1%. However, the company saw sequential improvement in the margins due to Project Phoenix's saving and restructuring initiatives.

NWL’s Historical Normalized Gross Margin and Normalized Operating Margin (Company Data, GS Analytics Research)

Looking forward, the company should be able to recover its margins to pre-pandemic levels. Moving into the second half, the company’s margin should benefit from price increases implemented at the beginning of July 2023 and potential price increases ahead. This should help it offset headwinds from volume deleveraging. In addition, inflation is also moderating. The company is seeing transportation costs involving trucking and distribution costs decrease as compared to the previous years' quarters. This should result in less of a drag on margins. Moreover, the company also expects FX to turn positive in the back half of the year which should also aid in margin recovery. Lastly, year-over-year margin comparisons in the second half of 2023 are becoming easier which should also lead to margin recovery in the coming quarters.

Further, the company is also focused on restructuring its operations. Newell launched Project Ovid last year to consolidate its supply chains and centralize manufacturing, aiming for cost savings through bundled shipments of orders from various product categories. The company also introduced Project Phoenix earlier this year to simplify operations, targeting cost reduction, efficiency enhancement, and annualized pre-tax savings of $220-$250 million once fully implemented by the end of 2023. These initiatives are in line with the company’s efforts to optimize its operations and, looking forward, I expect the company’s margins to improve.

Valuation and Conclusion

Newell Brands is currently trading at a 12.27x FY23 consensus EPS estimate of $0.85 which is slightly above its historical 5-year average forward P/E of 11.71x. The company’s top-line growth outlook is not good due to lower demand for discretionary products in an inflationary environment. While its margin outlook is positive, the valuation is not cheap with the stock trading above its historical average. I previously covered the stock with a neutral rating and the stock has declined since then. I still don’t find the company’s fundamentals and valuation attractive enough to warrant a rating change and prefer to remain on the sidelines for the time being with a neutral rating.

For further details see:

Newell Brands: Mixed Outlook Keeps Me On The Sidelines