NWL - Newell Brands: Not Attractive At This Price

2023-08-29 12:27:19 ET

Summary

- Newell Brands has been performing poorly in recent years, with a significant decline in share price and poor sales growth.

- The new CEO is implementing cost-cutting measures and streamlining operations to improve efficiency and profitability.

- The company's financials are not impressive, with high levels of debt and low profitability, indicating a need for a turnaround.

Investment Thesis

Newell Brands ( NWL ) has been steadily moving downwards for many years now and has recently reached levels it hasn't seen since '09. I wanted to take a look at the company's financials and its outlook to see what the ideal risk/reward for me would be to enter into a position in NWL. With the recent dividend cut, which may signal a step in the right direction, the company is not a buy at these prices yet due to efficiency and profitability ratios not improving. For this reason, I assign the company a “Hold” rating until sales and profitability improve substantially.

Outlook

There's no hiding the fact that the company has been hit very hard in recent years. In the last year alone, the share price is down over 45% while being down around 65% from the most recent major peak in May '21. There are a lot of reasons why the company has been performing so badly over the last decade or so, from very poor sales growth figures to contracting margins, which were caused by the recent high inflation that's been plaguing the US economy. The macroeconomic headwinds cannot be blamed for all of the company’s poor performance either because a lot of it had to do with how the company was managed in the recent past with the constant changing of CEOs also not giving much confidence. A lot of investors are looking at the company and are seeing a shipwreck that is yet to be fixed, as more and more captains jump ship. So, what does the company have in store for us going forward?

Project Phoenix

I am encouraged by the initiatives that the new CEO is taking currently. He is being much more assertive in righting the ship by doing a lot of cost-cutting measures. Project Phoenix (announced under the previous CEO Ravi Saligram) is looking to streamline the company's operations, leverage its scale, and reduce complexity, which will in turn improve efficiencies throughout its operations. The management said that it is targeting around $200m-$250m in savings by the end of '23 alone, which seems like a decent goal that can be achieved.

One thing that is encouraging is that the company is looking to trim a lot of its SKUs (stock-keeping units). Currently, the company has well over 100,000 different SKUs from many different companies that it owns. The management is looking to cut that to around 25,000 SKUs, which should translate to a lot of savings in the long run and be much more streamlined. Focusing on the most profitable brands and products is the way to go for a company that has been way too bloated in my opinion. A lot of the products it produces have little to no margins and have a lot of competition from other companies that may be able to offer a better price to consumers, especially in these times, where inflation is seriously hurting the consumer who is not willing to fork up the cash right now and may wait for the inflation and interest rates to come back to Earth in the near future.

Inflation

Speaking of inflation, there is no doubt the company saw a massive hit to its revenues in the last year when y-o-y sales were down 11% from FY21. Consumers delayed their purchases of NWL's products because most of them are not necessary for day-to-day life. There are also many alternatives to a lot of the products that Newell sells, that may be cheaper but slightly worse quality and that was a good tradeoff for many.

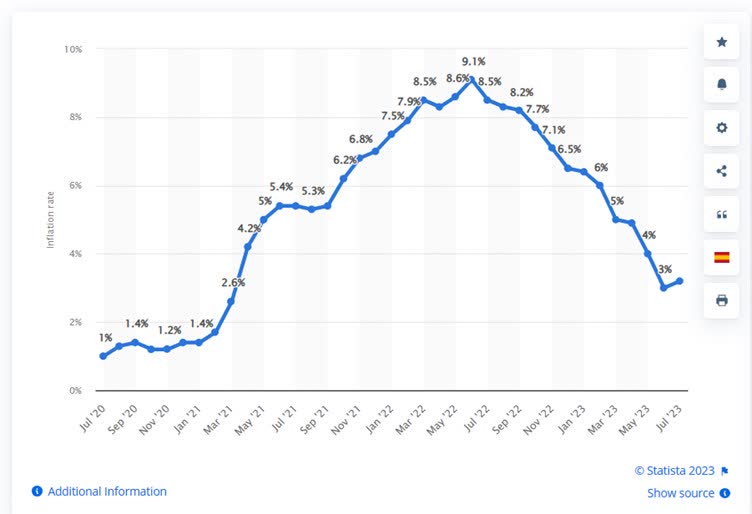

Now that inflation numbers are well off from their peak in June ’22, I could see sales picking up in the next couple of quarters, especially with the back-to-school season in full force. Interest rates may have to stay elevated for a little longer to make sure that inflation doesn’t come back up as we already saw a tick up in July’s numbers compared to June’s as the graph below shows. I am also encouraged by the team’s efforts of reducing inventory levels significantly, which translated into an improvement of over $700m in operating cash flow according to the latest transcript.

{kind=link}

These are all positives for the company, however, only time will tell if the cost-cutting measures are working out as well as the management hoped, and if the company can improve its revenue numbers now that the inflation is very close to where The Fed wants it to be in the US. That will all depend on the company's performance of its employees under the new leadership of Christopher Peterson.

Financials

Just to note, all of the graphs below will be as of FY22 because that way I can see how the company has progressed throughout recent years, which may show more of a trend than looking at every quarter that may fluctuate quite a bit. I will include some of the most recent numbers if they are necessary for extra color.

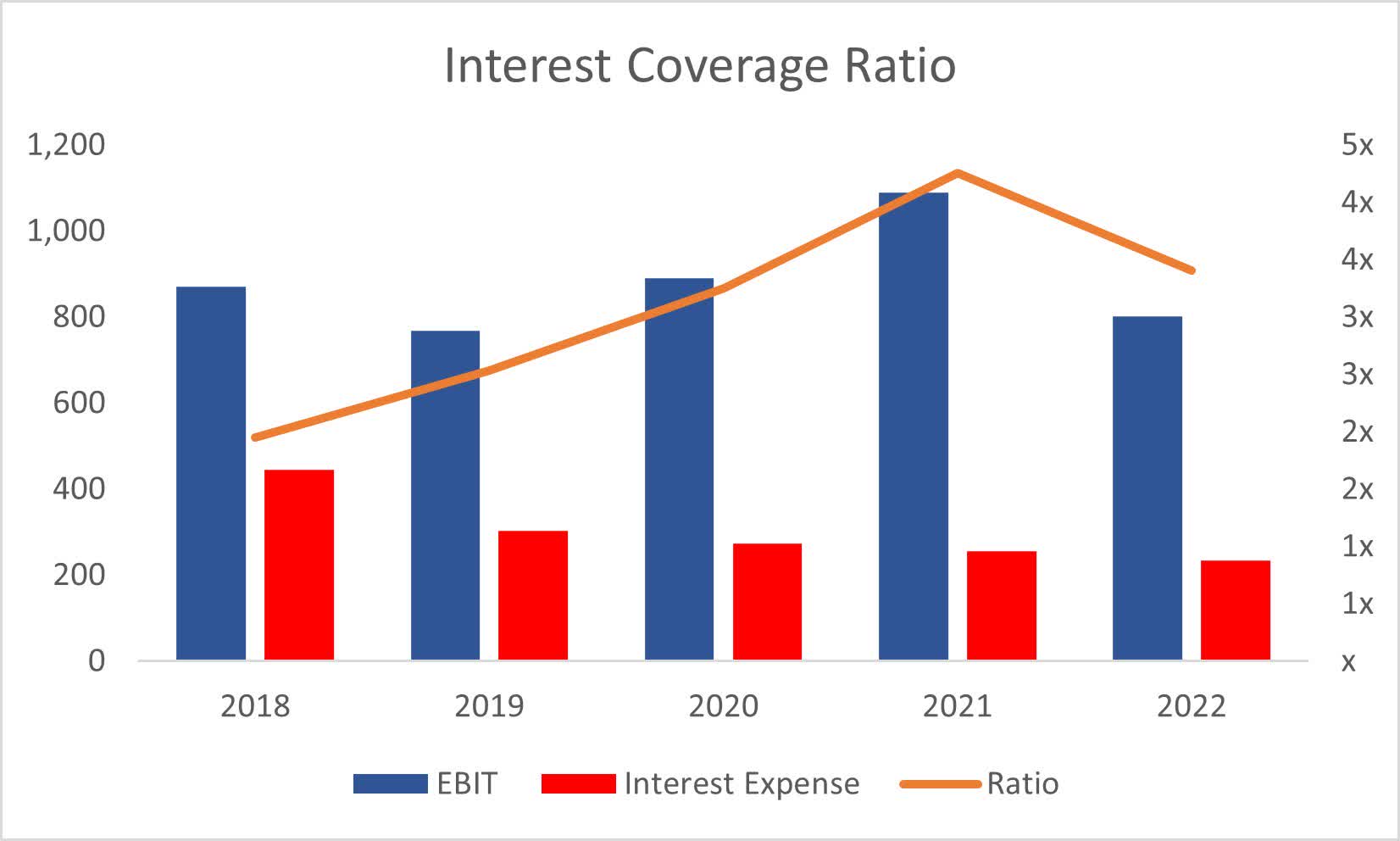

As of Q2 ’23 , the company had $317m in cash against a whopping $4.7B in long-term debt. I could see how this number alone would discourage people from investing. In the last 5 years, the company's interest coverage ratio has been around 3x, which is decent enough, however, it is dangerously close to being a problem in the future if the numbers don't pick up or if the company continues to hold this much debt going forward. The cut in the dividend should help the company slightly, however, it is a red flag for now because only time will tell how this debt is going to affect the company going forward. If everything goes the company’s way, then the current interest coverage ratio of around 3 is acceptable in my opinion and the company will have no insolvency risks.

{kind=link}

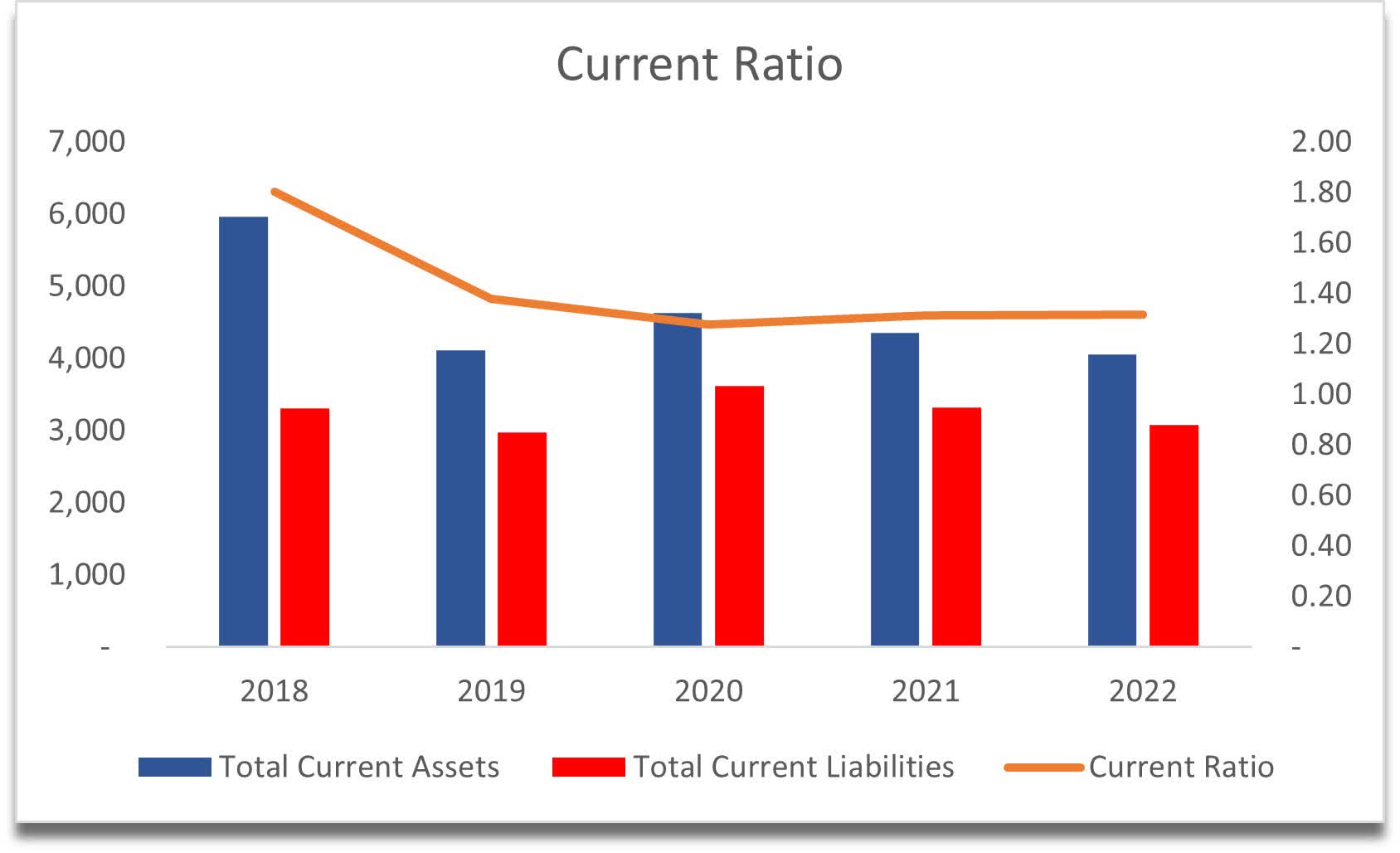

Looking at the NWL’s working capital ratio, or the current ratio, it’s about what I would consider the minimum acceptable ratio. I would like to see the company’s ratio be somewhere between 1.5- 2.0 which would tell me the company can easily pay off its short-term obligations and still have assets left over. NWL has been above 1 but slightly below 1.5, which still means that it is in no trouble in paying its ST obligations but not as safe as I would like it to be.

{kind=link}

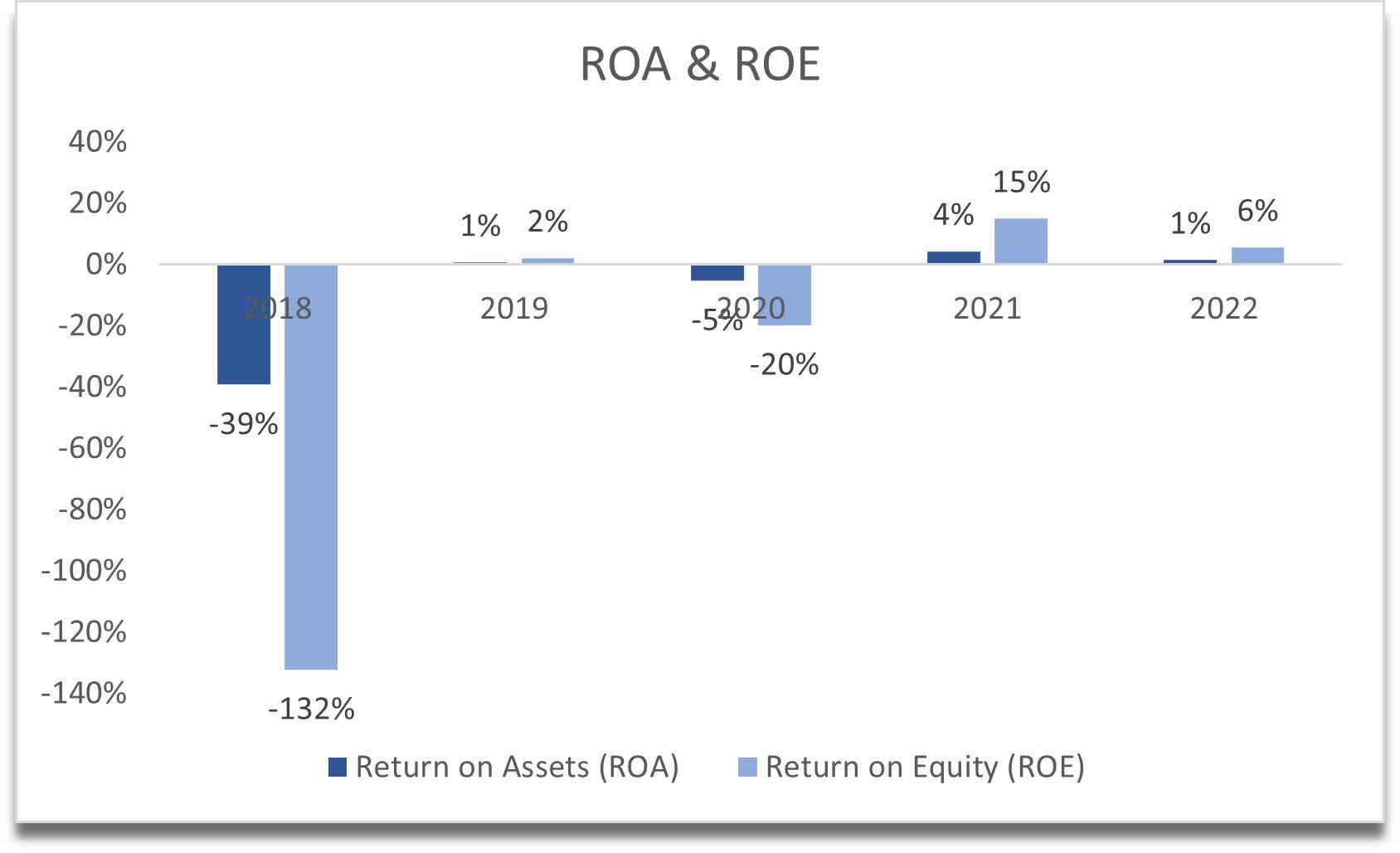

In terms of efficiency and profitability, the company’s ROA and ROE have not been great over the last 5 years and leave a lot to be desired. The minimums I would like to see are 5% for ROA and 10% for ROE. It seems like the management of the past has not been utilizing the company’s assets and shareholder capital very efficiently, which translated to no value creation for shareholders, and we can see that reflected in the company’s share price performance.

{kind=link}

The same story can be said about the company’s return on invested capital. It is well below my minimum of 10% and the company hasn’t seen those kinds of numbers since FY2015. This tells me that the company has lost its competitive advantage and it has no strong moat.

ROTC (Author)

Overall, the company’s financials are not the greatest in my opinion. These just don’t scream a turnaround yet and only time will tell how the new management fares and whether the cost-cutting initiatives will bear fruit in the long run. For now, I will have to assign a higher margin of safety.

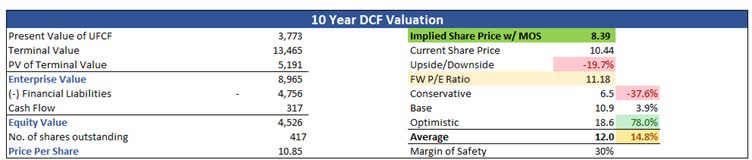

Valuation

In terms of revenues for the base case, I went with around a 12% decrease in sales for FY23, which matches analysts' assumptions. For the rest of the periods, I averaged around 1% growth until FY32 to be on the safer side. It may seem low, but the company’s past 5-year performance translated into -1% growth in revenues.

For the optimistic case, I went with 4.85% CAGR over the next decade, while for the conservative case, I went with -1% CAGR.

In terms of margins, I assumed that Project Phoenix and any further cost-cutting measures would improve gross margins by around 500bps over the next decade while improving operating margins by 200bps or 2%. This will translate into net margins going from around 2% in FY22 to around 10.5% by FY32.

On top of these estimates, I will add a 30% margin of safety because the financials are nothing to write home about and are lacking a turnaround picture just yet. With that said, Newell Brand’s intrinsic value and what I would be willing to pay for it is $8.39 a share, implying that the shares are too expensive right now and do not offer the ideal risk/reward.

{kind=link}

Closing Comments

There are a lot of unknowns regarding the company’s potential in the future. Time will tell how the management is going to right the ship going forward and whether the company will become an attractive opportunity for investors yet again. I would be willing to buy the company at around $8 a share as that is a good risk/reward profile in my opinion. The share price was there recently, and it may not come back down to it again, however, anything is possible. If I missed the boat, there are other surefire stock picks out there for me to discover so I will not dwell on it and will keep the company on my watchlist and set a price alert at around $8 a share and take it from there.

I do not assign a sale for the company as I believe there isn't too much bad that can go in the future and a lot of it has been priced in. Now, it's time for the management to prove it is capable of righting the ship and attracting investors, new and previous ones.

For further details see:

Newell Brands: Not Attractive At This Price