NWL - Newell Brands Plunged On Serious Concerns Over The Company's Future

2023-10-27 17:55:38 ET

Summary

- Newell Brands' shares plunged 9.9% after reporting disappointing financial results for Q3 2023.

- Revenue for the quarter was down 9.1% compared to the previous year, falling short of expectations.

- The company is facing challenges such as inflationary and supply chain pressures, labor shortages, and weak consumer sentiment.

- Current initiatives may help, but it's too early to tell and while shares are cheap, the risks with this name are high.

October 27 was not a great day to own shares of consumer products company Newell Brands ( NWL ). After management announced financial results covering the third quarter of the company's 2023 fiscal year, shares plunged, closing down 9.9%. This is not the first time that the company has experienced pain this year. Year to date, the stock is down 50.8%. And it is down over 65% over the past five years. Clearly, things are not going well for the company. In its third quarter earnings release, the company did manage to report adjusted earnings that exceeded analysts’ expectations. But both revenue and GAAP earnings fell short of forecasts. While the company is working hard on turning its operations around and we are seeing some evidence of that coming to fruition, it is difficult to get terribly enthusiastic about the company for now. At a time when not even management can come close to forecasting results, the best option for investors might be to sit on the sidelines until greater clarity comes into play.

Tough times

No matter how you stack it, Newell Brands is going through some difficult times right now. To see what I mean, we need only look at the most recent financial data reported by the company. This involves the third quarter of the 2023 fiscal year that management just reported on October 27. According to their press release on the matter, revenue for the enterprise came in at $2.04 billion. That's down 9.1% compared to the $2.25 billion generated one year earlier. Not only that, it's also down significantly more than what other parties anticipated. Analysts, for instance, expected revenue to be $80 million higher than it ultimately was. Even management proved to be wrong. They had forecasted revenue of between $2.11 billion and $2.16 billion. This means that they were ultimately off to the tune of $87 million.

{kind=link}

Author - SEC EDGAR Data

The company, unfortunately, experienced weakness across the board. Revenue under its Home and Commercial Solutions segment, for instance, declined by 7.3%, falling from $1.21 billion to $1.12 billion. A similar decline totaling 7.6% was seen with the Learning and Development segment. That took revenue down from $751 million last year to $694 million this year. And the company’s smallest segment, known as Outdoor and Recreation, reported a 20.1% plunge in sales from $289 million in the third quarter of last year to $231 million the same time this year. Collectively, even the company’s core sales dropped by 9.2%.

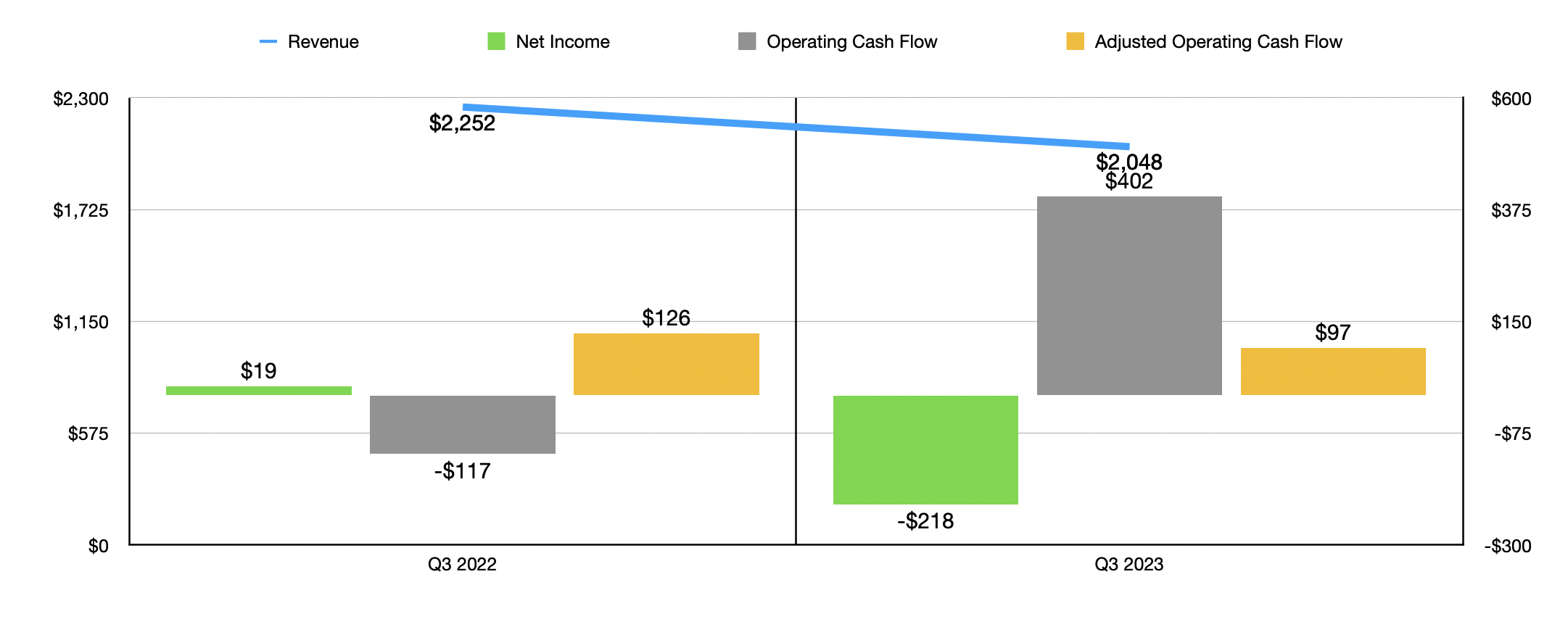

On the bottom line, the picture was a bit more complicated. The company actually posted a loss per share of $0.53. That was far worse than the $0.05 per share profit generated one year earlier and it was $0.73 per share lower than what analysts anticipated. But on an adjusted basis, the company generated a profit per share of $0.39. While still lower than the $0.50 per share profit generated in the third quarter of 2022, it was comfortably higher than the $0.23 per share profit analysts thought that the company would achieve. In addition to that, it also far exceeded the $0.20 to $0.24 in per share profits that management had forecasted when second quarter earnings came out. The earnings reported by management translated to a total net loss of $218 million, or $163 million profit on an adjusted basis. That compares to the $19 million profit and the $208 million in adjusted profits achieved one year earlier. Other profitability metrics were mixed but mostly negative. While operating cash flow went from negative $117 million to positive $402 million, the adjusted figure for this went from $126 million to $97 million.

{kind=link}

Author - SEC EDGAR Data

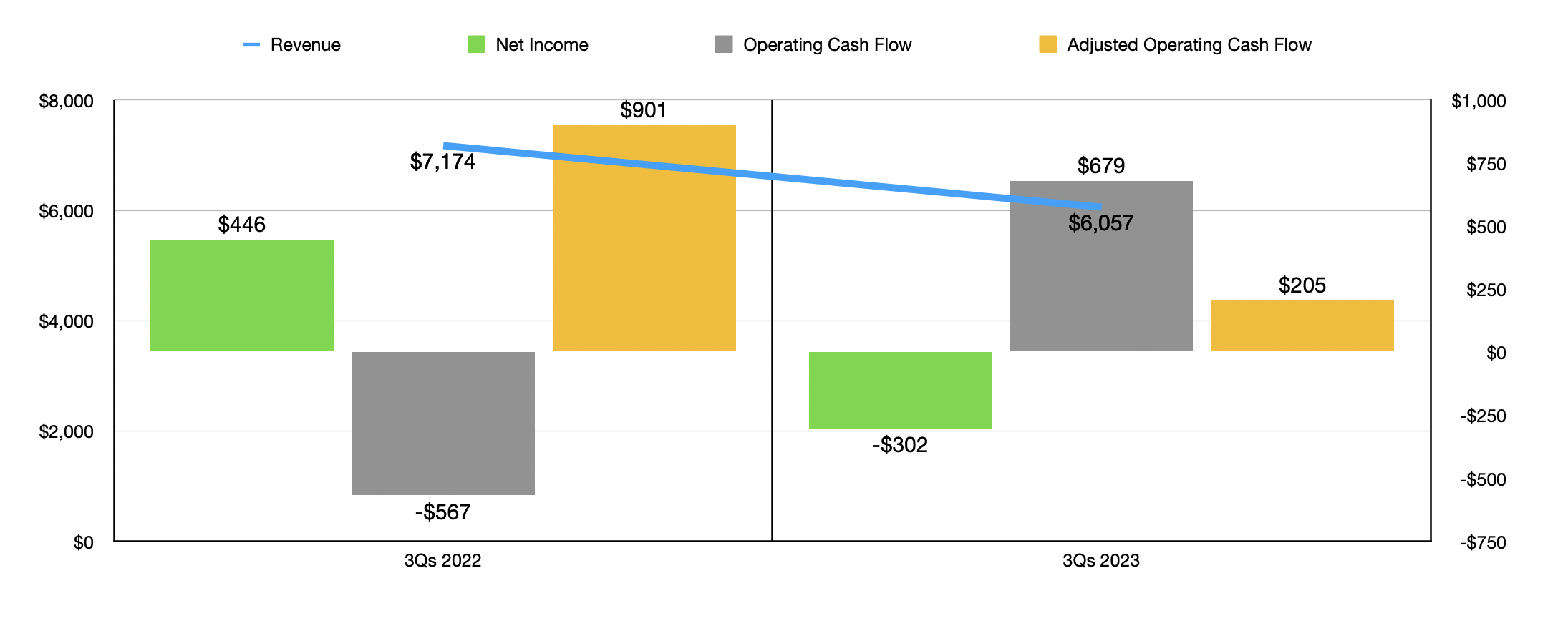

The third quarter was not a blip on the radar. It has been part of a rather disturbing trend for the company. As you can see in the chart above, revenue for the first nine months of the 2023 fiscal year in its entirety was substantially lower than what was achieved the same time last year. Net profits and adjusted operating cash flows also worsened during this time, though regular operating cash flow did manage to improve drastically.

Management has been fairly clear regarding the issues the company has faced. They claim that there is a sizable indirect macroeconomic impact imposed upon it by the conflict between Russia and Ukraine. But more importantly, the company has been hit hard by inflationary and supply chain pressures, labor shortages, and other similar issues. While the company owns multiple name brands such as Rubbermaid, Yankee Candle, Ball, Paper Mate, Coleman, and others, many of these brands still center around markets where the products have become largely commoditized. While there might be some exceptions like the candle business, most people don't care about the name brand of their paper. So when there is the option to use a cheaper generic brand, in order to save costs during difficult times, consumers will often do so. Add on top of this the fact that we are talking about consumer discretionary products for the most part, and it's not surprising to see weakness here. In a report published earlier this year, with data covering through the third week of August, consulting firm Deloitte looked at spending intentions of consumers when it came to discretionary products. For the ‘all categories’ option, they saw a negative sentiment of 19%. That's almost twice as bad as the negative 10% projected out one year earlier.

The bottom line becomes more complicated to unpack. And that's because the company is going through some significant changes internally. In January of this year, for instance, the company announced the launch of Project Phoenix, which is a restructuring and savings initiative aimed at cutting between $220 million and $250 million in annual pre-tax expenses. That comes at a one-time costs of between $100 million and $130 million, with $78 million already incurred as of the end of the most recent quarter and an estimated $101 million and annualized savings realized. This particular initiative is really focused on simplifying the company's organization, selling off unused assets like real estate, improving supply chain operations, and more.

In May of this year, management also launched the Network Optimization Project, which they claimed was a restructuring and savings initiative focused on simplifying and streamlining its distribution network within North America. At a one-time cost of between $37 million and $49 million, they believe that they will be able to save between $25 million and $35 million annually here. But they will also have to spend between $30 million and $40 million on capital expenditures as part of this. About $17 million has already been incurred for this particular initiative as of the end of the third quarter. All of this follows another project, known as Project Ovid, there has been a multi-year initiative aimed at transforming the company's operations.

{kind=link}

Author - SEC EDGAR Data

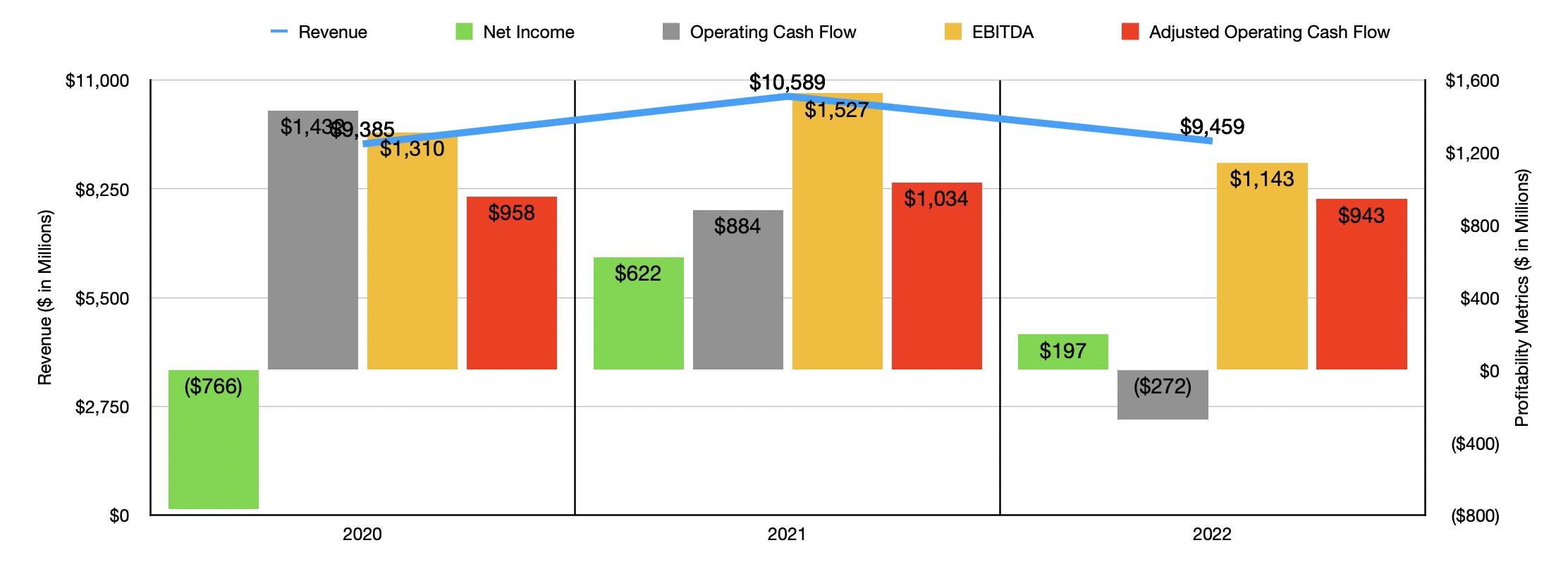

You would think that, with all of these different initiatives, the company would be seeing some concrete defects. But those are questionable. Yes, some of the bottom line results this year are not awful. But declining sales make it difficult for profits and cash flows to remain attractive. And over the past few years now, we haven't seen anything other than deterioration. As you can see in the chart above, after seeing revenue and profits spike from 2020 to 2021, we then began to see a meaningful slide lower on all fronts. 2022 was materially worse than 2021 was. Some of that pain was driven by the company’s decision to exit certain categories of products. The firm was also hit to the tune of $300 million by foreign currency fluctuations. But most of the drop was driven by overall weakness in core products.

{kind=link}

Author - SEC EDGAR Data

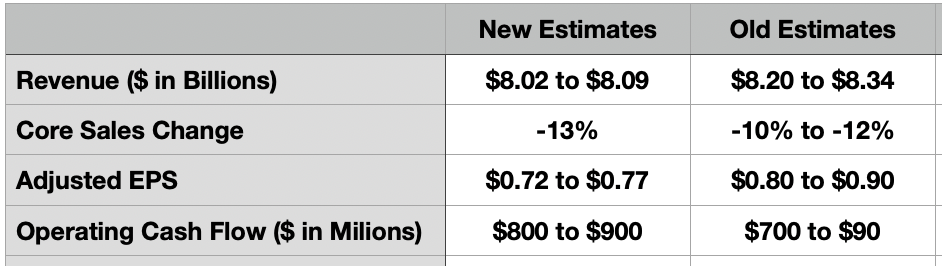

To make matters worse, management continues to struggle when it comes to providing quality guidance for investors. As you can see in the table above, new guidance provided in the third quarter calls for revenue this year to come in lower than last year, with core sales leading the way lower. Core sales are supposed to be a company's strength, not its weakness. Earnings per share guidance, on an adjusted basis, has also taken a beating. Management was expecting between $700 million and $900 million worth of operating cash flow this year. At least that has been revised higher to between $800 million and $900 million. But outside that, matters just seem to worsen.

{kind=link}

Author - SEC EDGAR Data

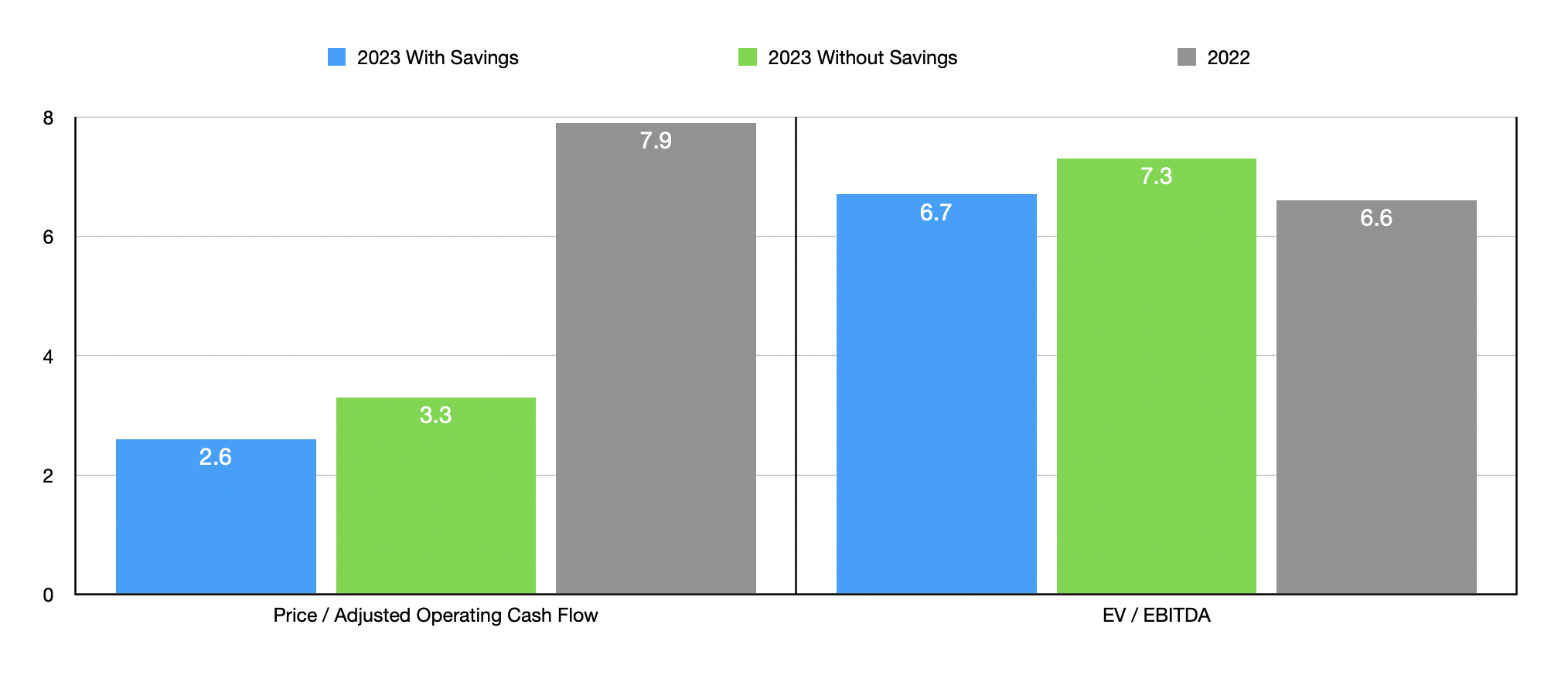

This doesn't mean that there isn't potential for shareholders. If we take some reasonable assumptions regarding what the rest of this year will look like, and we include a second scenario for this year that assumes full cost savings associated with cost cutting initiatives without any further loss in revenue, the stock does look quite cheap on a price to operating cash flow basis and on an EV to EBITDA basis. But as you can tell if you look closely at the disparity between these two metrics, there's the implication of high amounts of leverage. Depending on which forward estimate we use for 2023, the net leverage ratio for the company is between 4.23 and 4.58. This makes the company quite risky, especially when it looks as though the sales trend lower is worsening as opposed to improving.

Takeaway

Based on the data that I see, I don't believe that Newell Brands makes for a compelling prospect at this time. For investors who like to find the cheapest opportunities, this can be a tantalizing prospect. It's always great to be able to buy shares of a company when those shares are trading in the low to mid-single digits from a valuation multiple perspective. However, there seems to be no end in sight when it comes to sales weakness or worsening bottom line results. Add on top of this the hefty amount of leverage the company has, and I have decided to rate the company a ‘sell’ until such time that I can see some stabilization in its operations.

For further details see:

Newell Brands Plunged On Serious Concerns Over The Company's Future