NWL - Newell Brands: Too Many Financial Issues

2024-01-04 05:25:38 ET

Summary

- Newell Brands manufactures and sells consumer products in three segments: Home & Commercial Solutions, Learning & Development, and Outdoor & Recreation.

- After a merger in 2016, the company's revenues have started to decline with a large amount of divestitures.

- The company has large current profitability issues with a large debt balance left, weaker revenues, and a poor macroeconomic sentiment, but also concerns about the company's brands' performance.

- At the current price, the risk-to-reward still seems poor, as I estimate the stock to have a good amount of downside.

Newell Brands (NWL) manufactures and sells consumer products in three segments: Home & Commercial Solutions with 55% of 2022 revenues, Learning & Development with 31% of 2022 revenues, and Outdoor & Recreation with 14% of revenues. The company has a large portfolio of brands, including names such as Graco, Coleman, Oster, and Rubbermaid.

{kind=link}

The company hasn't had a very fantastic performance - a series of divestitures, very high debt, and issues in profitability have driven the stock price lower, making the ten-year price change a poor -73%. Demonstrative of Newell Brands' issues, the company cut its dividend from a quarterly amount of $0.23 to $0.07, making the dividend yield 3.20% at the time of writing.

{kind=link}

Acquisitions & Merger Have Turned into a Series of Divestitures

In the company's earlier years, Newell Rubbermaid had a fair amount of cash acquisitions, including $602 million in 2014 and $574 million in 2015. In 2016, Newell Rubbermaid merged with Jarden Corporation, creating a larger combined entity. The merger was a weird move in my opinion - afterwards, the company has started a series of divestitures to simplify the merged brand portfolio, deteriorating Newell Brands' revenues. From 2017 as Jarden Corporation's revenues were fully included, the company has had revenue decreases at a CAGR of -5.0%.

{kind=link}

The divestitures have been quite extensive. From 2016 to Q3/2023 figures, divestitures include an amount of $9096 million in cash flows. For example in 2017, the company sold its Tools business including three brands for approximately $1.95 billion, Fire Starter and Fire Log business for an undisclosed amount, and Winter Sports business for around $240 million. In 2018, the divestitures accelerated with around $5.1 billion in cash proceedings.

Profitability Issues

The divestitures aren't the only thing driving down Newell Brands' equity value - in recent quarters, the company's financials have been highly disturbed. Revenues were down by double digits in H1 and by -9.1% in Q3 despite no divestitures effecting revenues. All of Newell Brands' segments were down in revenues year-over-year in Q3.

With the poor revenues, Newell Brands' profitability has also been cut. The current trailing GAAP EBIT margin stands at 4.7%, compared to a 2022 figure of 8.7%, also quite representative of previous years' performance. The low revenues have affected Newell Brands with negative operating leverage, and so far the company's gross margin is 1.6 percentage points below with trailing figures compared to 2022 figures. In Q3, the gross margin trend reversed into a year-over-year increase due to Newell Brands' pricing initiatives, but I wouldn't expect the pricing changes to attribute too much to the company's bottom line - as can already be seen, Newell Brands has troubles in keeping up a good sales level, and higher pricing could add to the issue.

As a poor surprise to investors, Newell Brands also updated its 2023 guidance with the Q3 report. The company anticipates $8.02 billion to $8.09 billion compared to analysts' previous consensus estimate of $8.30 billion, and a normalized EPS of $0.72 to $0.77 compared to a consensus estimate of $0.84. The given guidance is estimating a revenue decrease of -12.6% in Q4 with the given revenue middle point. Newell Brands relates the issues to a poor macroeconomic situation, retailers' inventory reductions, and the bankruptcy of Bed Bath & Beyond in the Q3 earnings call . I believe that most of the revenue decreases can be attributed to such impacts fairly, but do still raise some concerns for the long-term future. Often, consumer-oriented everyday items are quite defensive, but that doesn't seem to be the case for Newell Brands.

Newell Brands has launched a plan to cut costs called Project Phoenix. The project is expected to cut annual costs by $220 million to $250 million, of which around $140 million to $160 million is already realized in 2023. On the other hand, the company expects $100 million to $130 million in total costs related to the implementation of Project Phoenix, most of which is seen in 2023 - as a result, the benefits of Project Phoenix aren't largely seen in 2023 yet. The profitability should improve very significantly from 2024 forward, but as the current profitability is very poor, the likely achieved level still doesn't seem to be too great in a base scenario.

Adding to the weak profitability, the 2016 merger was financed largely with debt, as Newell Brands had $11.3 billion in long-term debt at the end of 2016 on the company's balance sheet . The company has been able to pay off a good chunk of its debt, as the long-term debt now stands at $4.8 billion, but the amount is still significant - with the divestitures, the scale of operations has shrunk with the debt, making the amount still very high. With currently weak operating earnings, and higher interest rates, interest expenses take up around 70% of Newell Brands' trailing EBIT.

Valuation

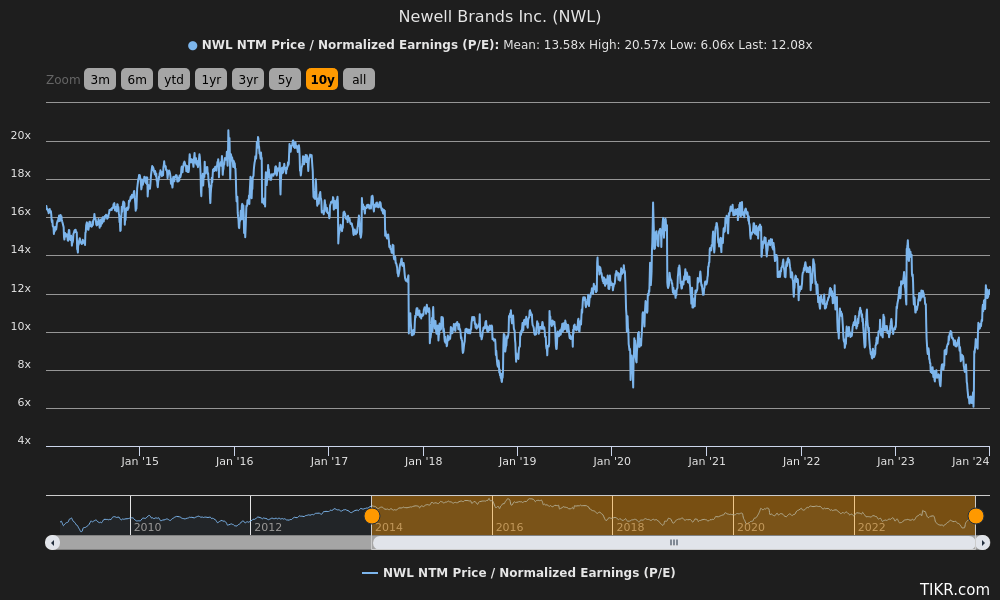

While Newell Brands seems quite cheap at a first glance with a forward P/E multiple of 12.1, below the ten-year average of 13.6, I don't believe that the company is cheap due to its lacking performance and high debt.

{kind=link}

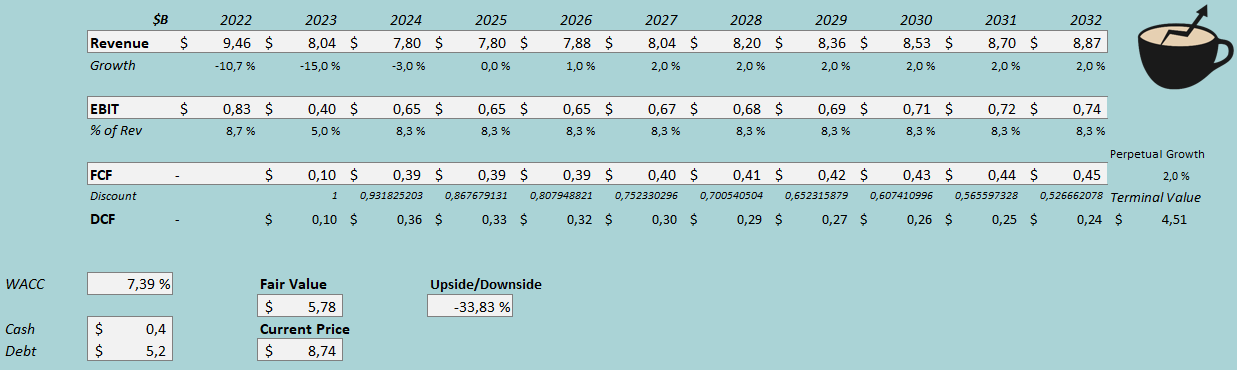

To demonstrate the valuation better, I constructed a discounted cash flow model. In the DCF model, I estimate the profitability to improve in 2024, but sales to still have challenges. In 2024, I estimate revenues to shrink by -3%. Afterwards, I estimate the performance to improve within the next couple of years into a perpetual growth of 2% - the estimate assumes no further divestitures, and a modest organic performance. With the Project Phoenix implementation and an improving macroeconomic situation, I estimate the 2024 EBIT to rise by $250 million from my 2023 estimate into $650 million, representing an EBIT margin of 8.3%. I estimate the margin to stay stable afterwards. Newell Brands' capital expenditure needs are moderate, and I believe that the company should have a modestly good cash flow conversion going forward.

With the mentioned estimates along with a cost of capital of 7.39%, the DCF model estimates Newell Brands' fair value at $5.78, around 34% below the stock price at the time of writing. The stock still seems to have downside, even after the price has fallen significantly in past years.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In the most recent reported quarter, Newell Brands had $69 million in interest expenses. With the company's current amount of interest-bearing debt, Newell Brands' annualized interest rate comes up to 5.28%. The company uses a very high amount of debt. The amount of debt is even larger when compared to the equity valuation - I estimate a long-term debt-to-equity ratio of 80%, as Newell Brands is focusing on deleveraging its balance sheet.

For the risk-free rate on the cost of equity side, I use the United States' 10-year bond yield of 3.97% . The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the United States, made in July. Yahoo Finance estimates Newell Brands' beta at a figure of 1.01 . Finally, I add a small liquidity premium of 0.2%, crafting a cost of equity of 10.14% and a WACC of 7.39%.

Takeaway

The 2016 merger still seems to have negative effects on Newell Brands' financial performance. The company has a large amount of debt left from the transaction, and the extensive brand divestitures have lowered the company's earnings. In addition, Newell Brands currently has profitability issues related to the macroeconomic situation and other issues, but also casting shadows on the company's organic long-term performance. At the moment, the stock seems like a poor investment despite the Project Phoenix restructuring likely improving profitability well from 2024 forward. With the DCF model estimating a significant downside, I have a sell rating for the time being.

For further details see:

Newell Brands: Too Many Financial Issues