YETI - Newell Brands: Turnaround Opportunity For This Undervalued Company With Strong Brands

2023-05-15 10:47:46 ET

Summary

- I cover Newell Brands' vast portfolio and explain why it reminds me of a recent company I covered: Hanesbrands Inc.

- I explain why we should learn from these comparable companies in the consumer discretionary sector and be careful when evaluating Newell Brands.

- I cover the current state of Newell Brands, recent earnings and transcripts along with details on Project Phoenix and Project Ovid and how it explains our turnaround story and valuation.

- I explain why Newell Brands is undervalued through Discounted Cash Flow Analysis, Historical Multiples, and Comparative Multiples.

- I provide a roadmap of how I will invest in Newell Brands moving forward.

Lovely Brands

Newell Brands ( NWL ) has a vast portfolio of well-known brands in which they design, manufacture, source, and distribute. They announced a restructuring and savings initiative called Project Phoenix, implemented January 23, 2023. This project is the consolidation of originally five operating segments, into three: Home & Commercial Solutions, Learning & Development and Outdoor & Recreation.

NWL Learning and Development (NWL Website)

{kind=link}

NWL Home and Commercial (NWL Website)

{kind=link}

NWL Outdoor and Recreation (NWL Website)

{kind=link}

I can take one walk around my place and eye several of these brands. I can open a drawer to uncover some Reynolds wrap, meal prep my food in my crockpot and store it in some Rubbermaid locking containers. I have kicked my expensive Keurig (KDP) and pods after it broke, and replaced it with an affordable Mr. Coffee. I then store this coffee in my favorite Contigo cannisters throughout the work day. And at the end of the day, I can open up my Coleman cooler that probably has the same heat transfer properties as a more expensively priced YETI ( YETI ).

I recently wrote an article on Hanesbrands Inc. ( HBI ) and I see a lot of similarities between these two companies. Like Hanesbrands, Newell has a vast collection of strong, affordable brands that are competitive in quality, but perhaps lack a special sparkle in the marketing sense.

In other words, they are boring.

And as a Peter Lynch fan, I love boring stocks. These are all brands I buy, use, touch and feel on a daily basis, and when economic times worsen , I can say for myself, I prefer these "boring" brands even more. Maybe I'm boring, but the money I'm saving on these products compared to over-the-top competitors, can be reinvested in these companies.

They are also brands that I see staying around for my lifetime, which initiates long term value investor interest.

But like Hanesbrands, Newell Brands has seen a lot of similar economic headwinds and issues. They have high inventory, manufactured from expensive raw materials, slowing sales, and massive debt. They also have a dividend reaching near 10% that probably raises questions from investors if Newell Brands can even afford it. Management has commented in their recent earnings, that a capital allocation plan may change. This has led to investors sitting on a seesaw of decisions:

- Wait to hear of a dividend cut or reduction, flushing out dividend investors, sending the stock price down, and allowing value investors to hop on board.

- Or, invest now, regardless of plans of the dividend, under the assumption that Newell Brands is already undervalued.

Personally, I'm allocating more to Hanesbrands Inc, because they have already eliminated their dividend and are focusing on debt, sending the price to deep value territory. I am allocating a smaller portion to Newell Brands because I think it's a reasonable price now, but I could see a dividend reduction or elimination in the future with prospects of lowering the stock price. If this happens, I will start to dollar cost average more to Newell Brands. This is why I perceive a "Buy" rating to Newell brands where I have a "Strong Buy" towards Hanesbrands. Rest assured, if this gets a small haircut, the seesaw will lean more towards a "Strong Buy" as I'm in this baby for life.

The Current State

Newell Brands is in a turnaround phase.

I wanted to cover their recent earnings, transcript and discussions, along with details on their new projects to help paint the picture of this current restructuring state.

Newell Brands had mixed results during their latest earnings , touting a miss on Earnings Per Share ("EPS") and a beat on revenue. There were also quite a few key points in their recent earnings call and transcript :

- CEO Change: Ravi Saligram, the CEO of Newell Brands, announced that he will be retiring on May 16, 2023. Chris Peterson, the current COO of Newell Brands, will be taking over as CEO following.

- New Projects : Newell Brands is implementing Project Phoenix, a new operating model and implementing Project Ovid, a new distribution and transportation system (these are explained in greater detail further down).

- Unchanged Category Growth : Peter Grom from UBS asked about the underlying category growth and whether it has worsened since the last earnings call. Chris Peterson responded that the underlying category growth has remained relatively unchanged, but that retailer destocking has had a significant impact on the company's results. He also said that the company is optimistic about the back half of the year, but that it is monitoring the macro environment closely.

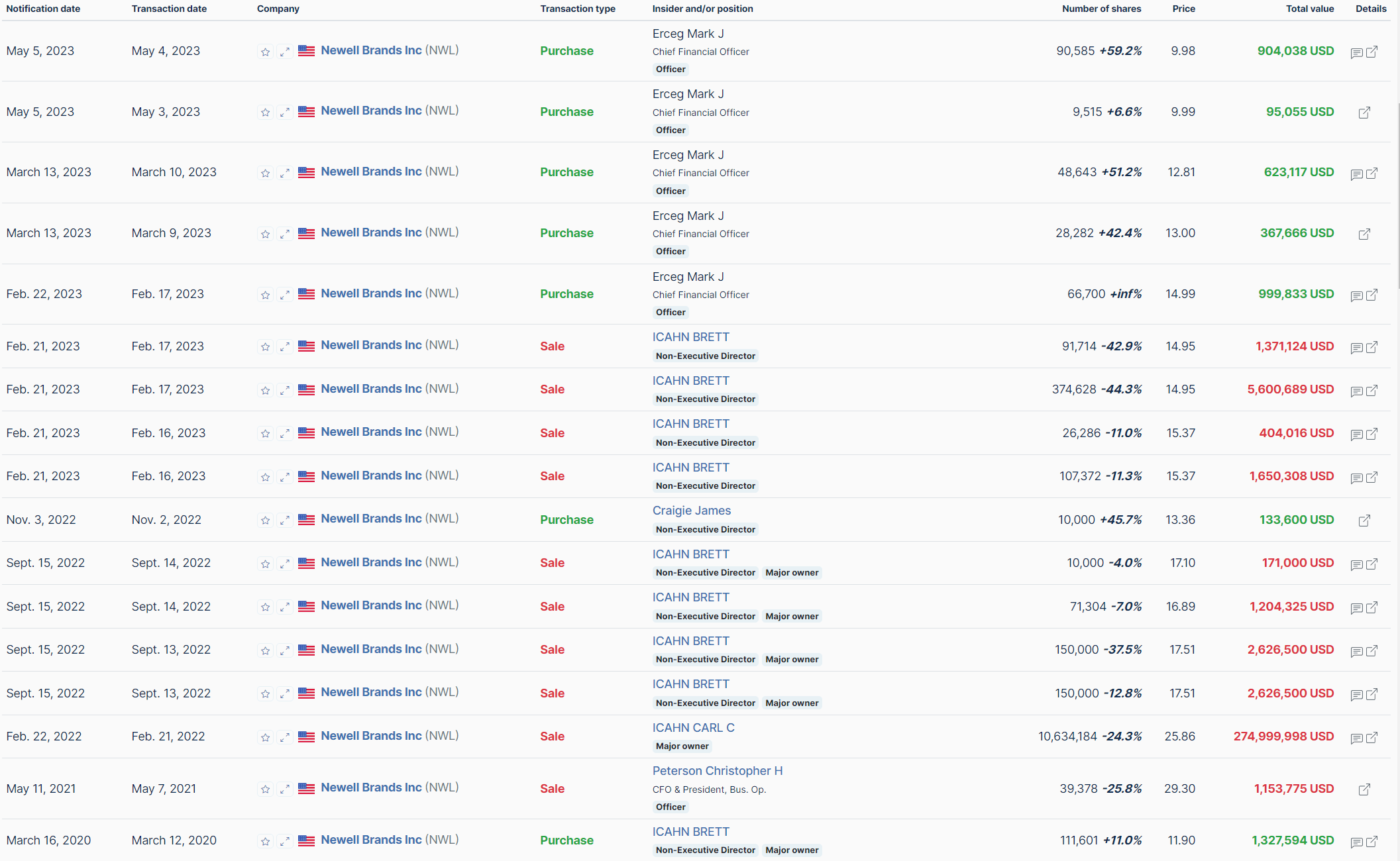

- Normalized Cash Flow and Capital Allocation Strategy: Kevin Grundy from Jefferies asked about the company's cash flow outlook. Mark Erceg responded that the company is confident in its ability to generate $700 million to $900 million in operating cash flow for the year. In fact, it appears Erceg is so confident with this value, he's purchased over $2 million worth of shares in the months of March and May. He also said that the company is evaluating its capital allocation strategy and that the dividend will be part of that discussion.

Insider Buying From Newell Brands (Insiderscreener.com)

{kind=link}

- Improved Gross Margins and Pricing Strategy: Chris Carey from Wells Fargo asked about the company's gross margin outlook and its pricing strategy. Mark Erceg responded that the company expects gross margin to trend sequentially higher in the second half of the year. He also said that the company is confident in its ability to achieve its net pricing target of 2% to 3% for the year. However, he noted that the company is monitoring the macro environment closely and that it may need to adjust its pricing strategy if the consumer starts to get weaker.

- Back-to-school Sales: Andrea Teixeira from JPMorgan asked about back-to-school sales and inventory levels. Chris Peterson responded that he is optimistic about back-to-school sales, but that inventory levels are still elevated. He also said that the company is expecting a more normalized back-to-school season, with retailers ordering inventory later in the season.

- Reduced Inventory: Stephen Lengel from Stifel asked about the company's inventory levels and its plans to reduce them. Chris Peterson responded that the company is making progress in reducing its inventory levels, but that it is a long-term process. He also said that the company is focused on reducing inventory levels in a way that does not impact customer service or sales.

- Cost-Based Approach to Pricing: Filippo Falorni from Citi asked about the company's pricing strategy. Chris Peterson responded that the company is taking a cost-based approach to pricing, and that it is confident that its competitors will follow suit. He also said that the company is prepared to lose some market share in the short term if necessary.

As for the details on Project Phoenix :

- Newell Brands expects to realize annualized pre-tax savings in the range of $220 to $250 million when Project Phoenix is fully implemented.

- The company expects to incur restructuring and related charges of $100 to $130 million in connection with Project Phoenix.

- The restructuring plan is expected to result in the elimination of approximately 13% of office positions.

Project Ovid is a major transformation of Newell Brands' supply chain. The new model will be more efficient and customer-friendly, and it will help the company better compete in the omnichannel retail environment. Newell Brands has over 100, 8 business units and over 23 unique supply chains in the U.S. Project Ovid will streamline these supply chains into a single integrated supply chain. The new model will improve service delivery and support omnichannel needs. "Customers can now combine orders across businesses and ship those from shared service centers in full truckloads".

Overall, these details will help paint a story that we are betting on a turnaround from Newell Brands. This will be represented in our valuation not as a massive turnaround of the century, but just a return to normal.

Valuation

I perceive Newell Brands to be undervalued through a Discounted Cash Flow Analysis ("DCF") and a Multiples Analysis.

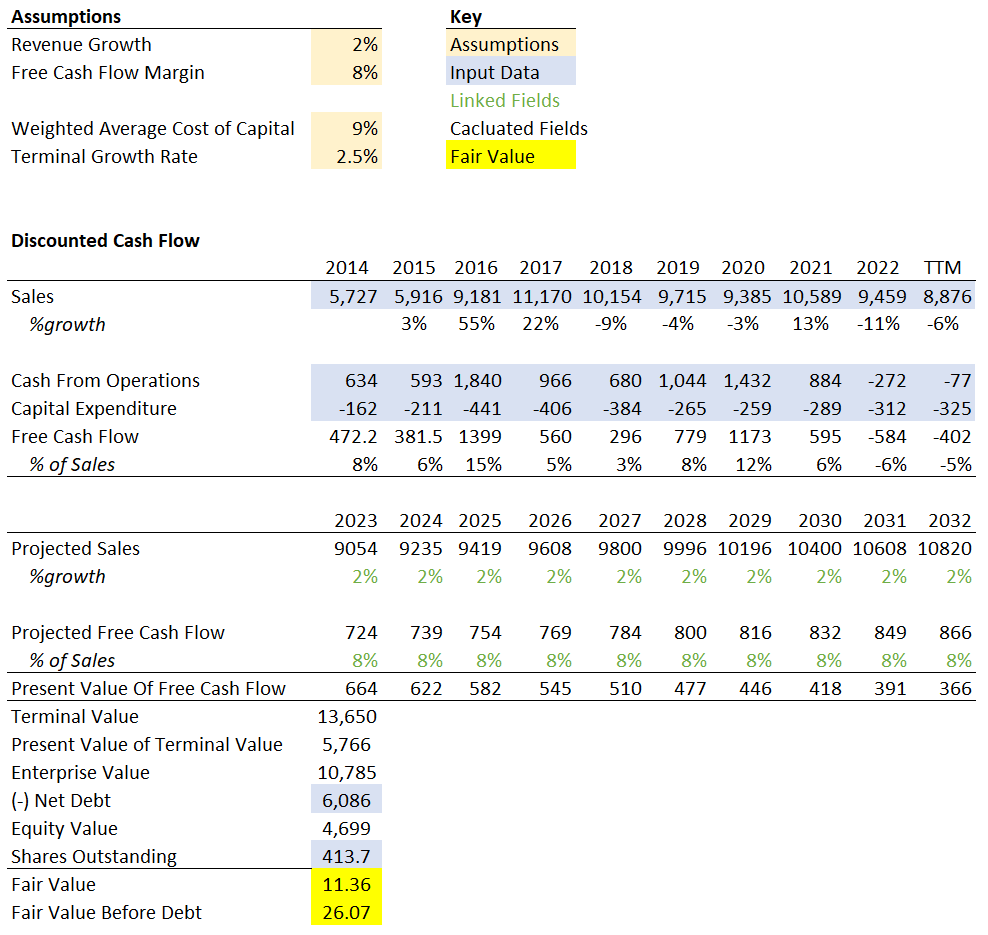

For the Discounted Cash Flow Analysis, I make the conservative assumption of a 2% revenue growth rate over the next 10 years. This assumption is based on historical growth numbers of Newell Brands, along with Seeking Alpha's analyst projections .

I make an 8% Free Cash Flow Margin assumption which is an average of years 2014-2021. This is based on my story that Newell Brands will return to baseline margin levels after the high cost inventory makes its way through, new projects help streamline operations, and macroeconomic headwinds soften in the upcoming years.

Furthermore, I make the assumption the discount factor will be a 9% Weighted Average Cost of Capital ("WACC") and a 2.5% Terminal growth rate ("TGR"). These values will be used to calculate the terminal value through the perpetuity growth model .

After I project future cash flows 10 years and discount back, I add the sum to the Present value of the terminal value, subtract net debt, and divide by the number of diluted shares outstanding to arrive at a fair value of $11.36 or $26.07 before debt is applied. This implies the company is undervalued at current prices.

The complete table is shown with access to the spreadsheet here:

Newell_Brands_DCF_5-14-2023.xlsx

Newell Brands Discounted Cash Flow (Seeking Alpha Raw Data with Author's Spreadsheet)

{kind=link}

To compliment the DCF, we can take a look at historical multiples. Newell Brands is trading around 0.44 Price/Sales at the time of writing this passage. This is nearly an all-time low over the last 10 years. We can also look at an Enterprise Value ("EV") /Sales Ratio of around 1.13 to encapsulate the massive debt they carry. Based on multiples, I perceive this strengthens the thesis that Newell Brands is indeed undervalued.

Historical Price To Sales (Seeking Alpha)

{kind=link}

Historical EV To Sales (Seeking Alpha)

{kind=link}

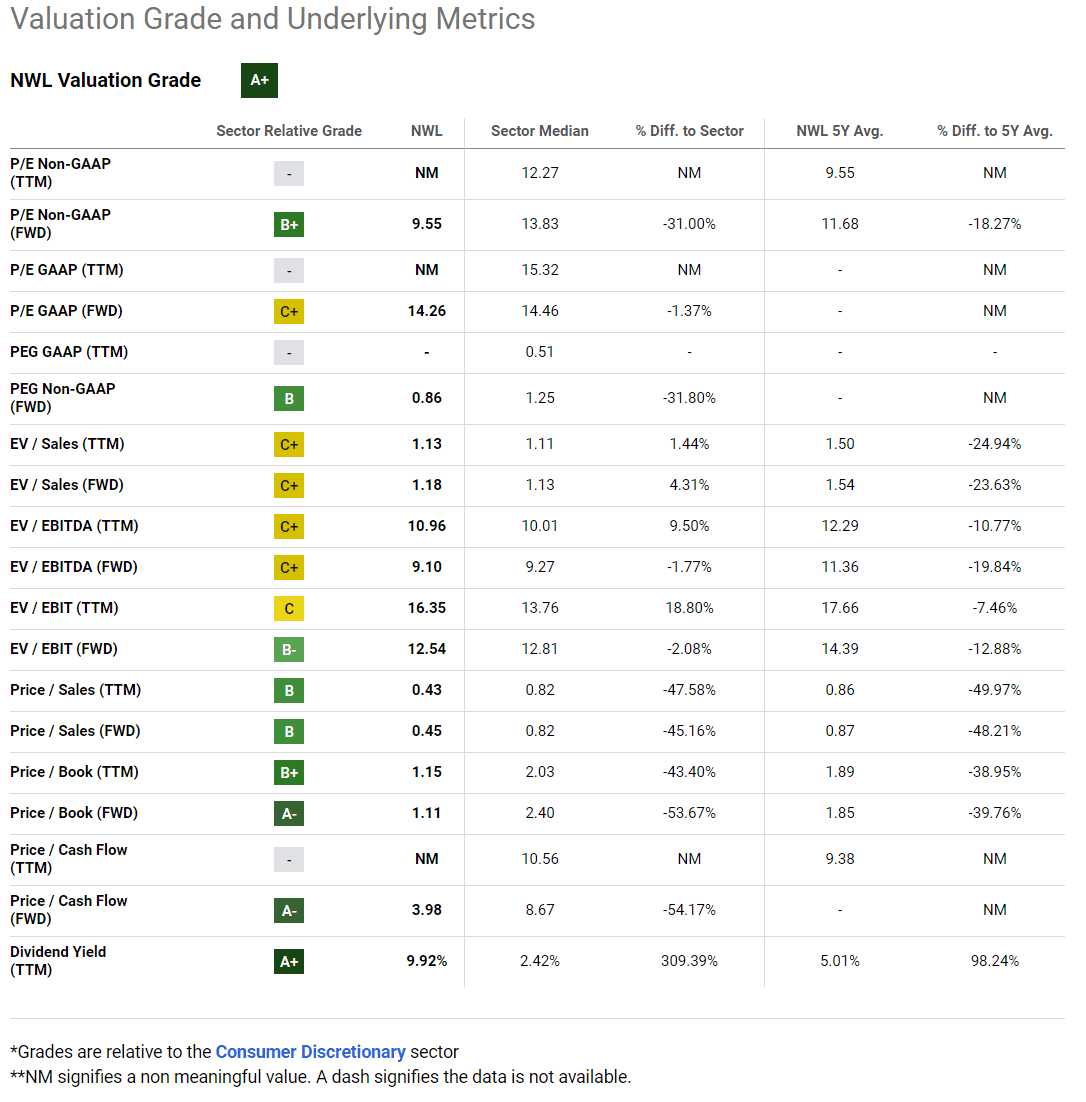

To compliment the DCF, and historical multiples, we can also take a look at their valuation scorecard compared to the consumer discretionary sector. In this case, Newell Brands receives an A+ overall with juicy values in Price\Sales, Price/Book, Price/Cash Flow ("FWD"), and of course the dividend yield.

Comparative Multiples (Seeking Alpha)

{kind=link}

Takeaway

The main risk here is failure to properly allocate capital by management moving forward. If they are not strategic in paying down debt, it could spell disaster and lead to a situation similar to Hanesbrands Inc. Although management seems confident they will have the proper cash flows moving forward to pay down debt and still maintain the dividend, it worries me a little that even a slight slip could spell a dividend reduction or cut. I believe a dividend cut would bring the stock price down temporally as dividend investors flee and value investors eat up the scraps. Fortunately, for long term investors, it seems Newell Brands is trading at a very favorable price considering their strong brands. Personally, I have a position and will dollar cost average if it moves down. I see and use their brands every day and it gives me a warm fuzzy feeling I'm invested in such a company.

For further details see:

Newell Brands: Turnaround Opportunity For This Undervalued Company With Strong Brands